VOO - Embecta: Mammoth Effort Needed To Get Investors Over The Line Reiterate Hold

2023-07-21 18:00:35 ET

Summary

- Embecta Corp.'s stock has dropped 31% since its last publication, and analysis suggests this trend may continue.

- Despite securing key partnerships and signing multi-year agreements, projected revenue and earnings growth is flat.

- Net-net, reiterate hold on Embecta Corp.

Investment summary

Following my May report on Embecta Corp. ( EMBC ), the stock hasn't garnered any additional demand and curled over to the downside. it now trades 31% below my last article, and based on this rigorous analysis of the investment facts, my analysis reveals these trends may continue. For a review of the last two EMBC publications, click here .

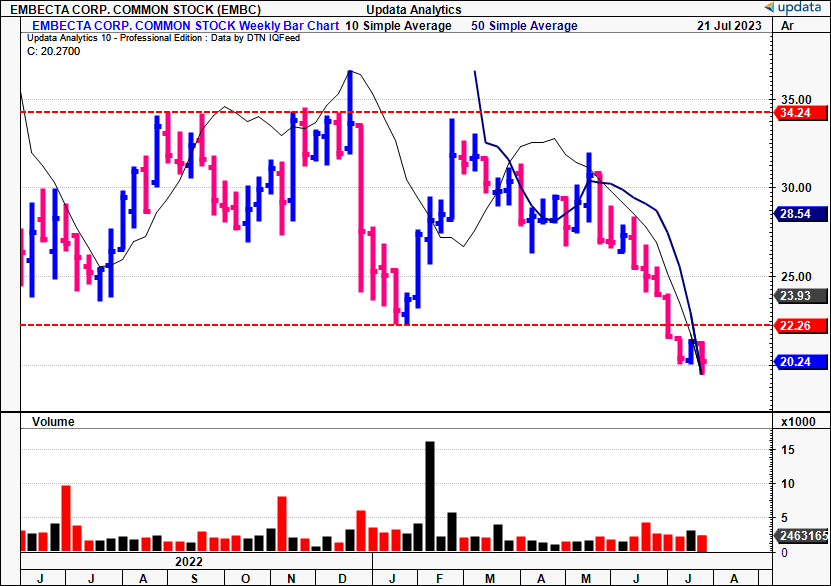

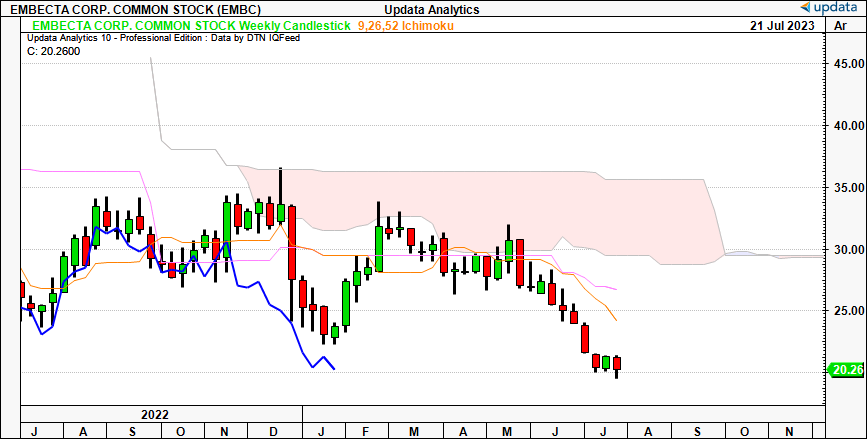

As a reminder, EMBC was formed as a carve-out from Becton, Dickinson ( BDX ) in April last year, and has languished since its new listing. In Figure 1, tracking the company's weekly performance, you can see that investors have priced it at lower market values than 12-months ago, telling me that expectations have also been revised lower.

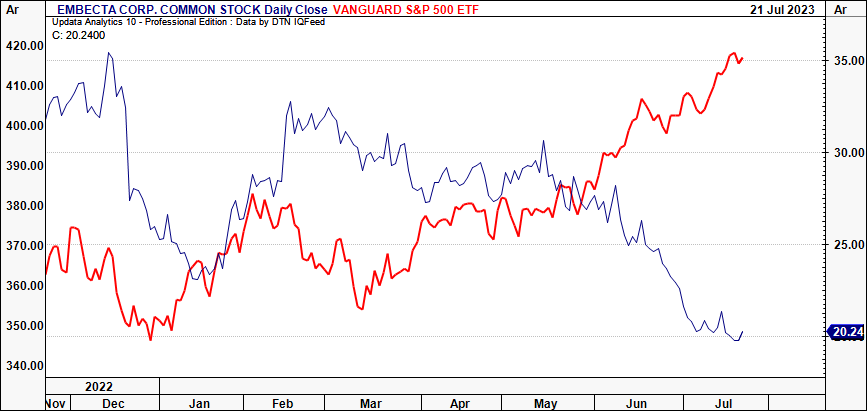

The stock has now set a series of lower-lows and lower-highs, supporting this view. Furthermore, the divergence in EMBC's equity line versus the benchmark index ( VOO ) is observed in Figure 2. Thus, the opportunity cost of holding EMBC since December last year has been in the realms of 16%. Net-net, I continue to rate EMBC a hold for reasons discussed in this report.

Figure 1.

{kind=link}

Figure 2.

{kind=link}

Updates to critical investment facts

Extensive analysis of the prevailing data shows EMBC has been quite busy in proofing up business growth for the coming years.

For one, it has been deepening partnerships with key customers, securing preferred brand status, and it signed multi-year agreements with (what EMBC calls) major retailers and payers earlier this year. Such initiatives looks have yielded positive results:

- For example, the company was awarded an exclusive preferred position on the Express Scripts National Preferred Formulary, and, it was awarded significant contract wins from the US Department of Veterans Affairs ("DVA"). Both of these suggest EMBC has obtained a level of credibility since listing.

- Further on the collaboration front, EMBC recently entered into a co-promotion agreement with PolyPhotonix to promote its sleep masks in the UK. This is relevant as the masks are designed for use in sleep disorders in patients with diabetes.

- It also signed a deal with Tidepool, to develop an automated insulin pump for patients with Type 2 diabetes. This is set to apparently include EMBC's patch pump.

Thus, you can see EMBC's proactivity in establishing these agreements, as mentioned. Alas, this isn't the issue for mine in the investment debate.

The issue is moving forward is threefold: 1) Financials are weaker, 2) sentiment is absent, and 3) valuations are unsupportive of a rating higher. In other words, there may not be any mis-pricings with the stock at 7.6x forward earnings—quite the discount.

To illustrate:

- The firm booked Q2 revenues of $277.1mm, a gain of just 90bps YoY, not conducive to catch a bid for its equity stock in my opinion. Backing out FX headwinds, the growth was 4%.

- U.S.-dominated revenues were up 360bps YoY to $146.4mm, compared to 440bps growth in international turnover to $130.7mm. These results actually surpassed internal expectations set by management in previous periods.

- It pulled this to operating income of ~$85mm (31% margin), from gross of 68.5%.

EMBC also revised its full-year growth assumptions as well. It calls for growth between 0—1%, but not much of a difference from the previous range of negative 1.5% to 0.5%. This still results in $1.1–$1.13Bn at the top line, and consensus has the same numbers for FY'23 and FY'24. It sees this on -37.5% and 13% YoY growth in earnings over the same time, respectively.

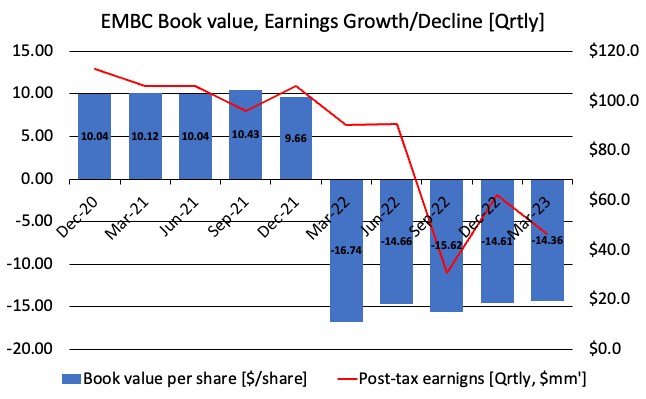

I'd also point out the fact that, since listing, the company's book value per share has remained negative [Figure 2]. Part of this stems from the $1.6Bn in debt on the balance sheet, leading to negative equity value of $822mm at the time of writing. This is compounded by the $545mm in accumulated deficits since listing as well, driven by the fact post-tax earnings have slipped off highs of ~$112mm in March FY'22, now at $46.4mm in the TTM.

Figure 2.

{kind=link}

The question we have to ask ourselves here is one of opportunity cost. Is it really worth buying a company today, that projects flat revenue growth and substantial wind backs in earnings for the next 2 years? Added to that, you're buying negative $14/share in book value, despite EMBC clipping $94mm in TTM earnings in Q2.

It is true that the pre-carve-out figures are based on particular accounting principles, and thus, "do not [necessarily] reflect what Embecta's financial results would have been, had Embecta operated as a standalone public company," according to the CFO. Nevertheless, it's been all downhill on the fundamental and valuation front since listing. By all measures discussed here today, these trends look to continue going forward, thus supporting a neutral view.

Market-generated data

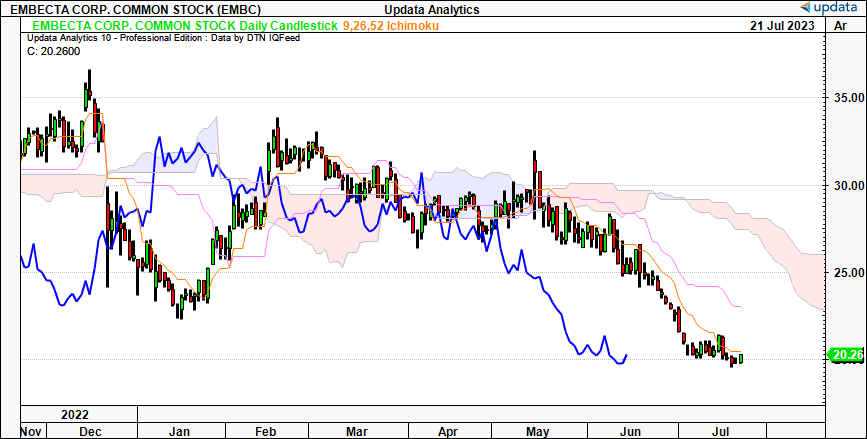

In the absence of robust fundamentals, it is imperative to rely on investor positioning and data gathered from price studies to guide price visibility into the future. Examining the cloud charts below [Figure 3 and Figure 4]— beginning with the daily chart, it is evident that the price and lagging line are situated below the cloud and diverging from it.

Unless there is a substantial shift, any bullish outlook is unwarranted based on this presentation. The daily chart provides insight into the weeks ahead, leading me to maintain a neutral outlook in the mid-term. The weekly chart in Figure 4 looks to the months ahead, and equally indicates a non-bullish trend. Unfortunately, no discernible catalysts (beyond the next earnings report) suggest a reversal is likely, thereby confirming my neutral stance.

Figure 3.

{kind=link}

Figure 4.

{kind=link}

Point and figure studies—like the one shown in Figure 5—are an effective means of removing extraneous factors and temporal noise in order to achieve a more objective view of price action. These studies saw the decline in the EMBC share price from $25 to $20, and currently indicate a possible downside target of $14.40 as shown. In my view, should the current price drop further, this target would be activated. Therefore, in light of this, it would be unjustifiable to assign a bullish rating at this time.

Figure 5.

Data: Updata

Data generated through the options market provides the most comprehensive insight into investor positioning, as it represents actual money at risk. Analysis of the options chain for August expiry reveals that demand is largely concentrated on the puts side. There is a heavy concentration of puts with a strike depth ranging from $30 down to $22.50, both above the current market price. These investors therefore have the option to sell at these prices in the event of a further downward trend. Conversely, there is a concentration of calls with a strike price of $35, even extending out to $50.

It is possible these pundits anticipate a move towards this mark by August. However, it is evident that the scale is primarily dominated by those positioned for EMBC to turn lower, or at least track sideways. On that point, we can't discount the fact some of this open interest could be options-based strategies that involve both calls and puts, in the event of a congested market (in other words, when the stock trades sideways with no directional bias).

Valuation and conclusion

Those hunting for deep discounts will potentially find value in EMBC trading at 7.6x earnings and 7x forward EBITDA. You've got EMBC thus priced at 62% and 48.7% discounts to the sector, respectively. That, and the stock comes with a 3% trailing dividend yield at the time of writing.

To these points, I'd link back to the question I raised earlier— is it worth buying negative growth for the next 2-years? Said another way, if you bought EMBC today, you'd be paying $7.60 for every $1 in future earnings—only for these to decrease by 37.5% and then another 13% over the next 2 years respectively. Then again ask yourself, just as I have done, what is the opportunity cost of doing this. Based on sound investment logic, and a thoughtful analysis of the future, it would appear the deep discounts EMBC is priced at are justified on a fundamental basis. A company's stock price is simply a set of expectations discounted to a certain mark. If investors believe the sector will trade at 20x earnings—as it does for broad healthcare—and EMBC to trade at 7.66x earnings, perhaps it suggests that EMBC will likely continue this negative spread. The narrative would be different if we had the fundamentals to say there is a mispricing, but in my opinion, the discount is warranted. This supports a neutral view.

In summary, the carve-out of EMBC from BDX was potentially an attractive play to offer investors exposure to diabetes management. To date, however, and looking forward, there doesn't appear to be the necessary fundamental catalysts to suggest Embecta Corp. will trade higher in the medium term. Management project flat YoY growth this year and the next, and both Wall Street plus my own internal expectations echo this view. In that vein, I continue to rate EMBC a hold until evidence suggests otherwise. Note this view is shared objectively with the quant rating system, that rates EMBC a hold.

Figure 6.

Data: Seeking Alpha

For further details see:

Embecta: Mammoth Effort Needed To Get Investors Over The Line, Reiterate Hold