ERJ - Embraer: Getting More Attractive

2023-11-28 06:52:05 ET

Summary

- Embraer affirms 2023 guidance for deliveries, margins, and FCF, with increased deliveries expected in 2024.

- The company's stake in Eve Holding should be considered a free option and a way to gain exposure to the eVTOL sector.

- ERJ's operating update shows higher revenue in Service & Support, increased deliveries in Commercial Aviation and Executive Jet segments, and improved margins.

Summary

In a meeting with the company, they affirmed 2023 guidance in terms of deliveries, margins, and FCF. They also added color for 2024 that suggested increased deliveries for most business segments that should continue to drive EBITDA. I have updated my estimates and price target to US$24.7 from US$19.3 for YE24.

Performance

Embraer S.A. (ERJ) has underperformed larger peers as it struggled to recuperate revenue and margins impacted by the pandemic supply chain disruptions. Its 75% stake in Eve Holding (EVEX) has not been incorporated into valuations and given the long lead times to market should be considered a free option. Perhaps, ERJ is one of the better ways to gain exposure to the eVTOL sector.

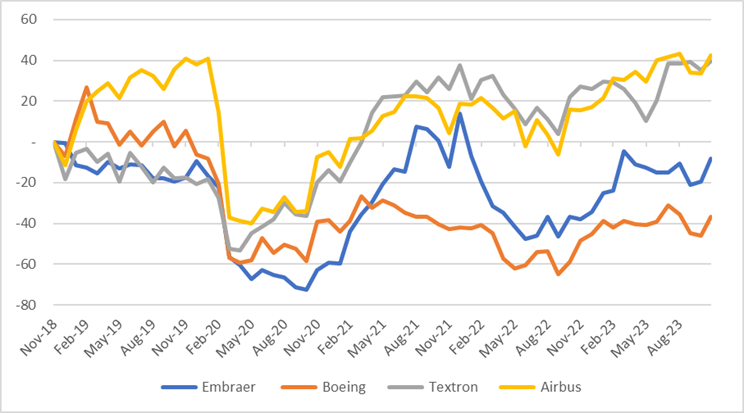

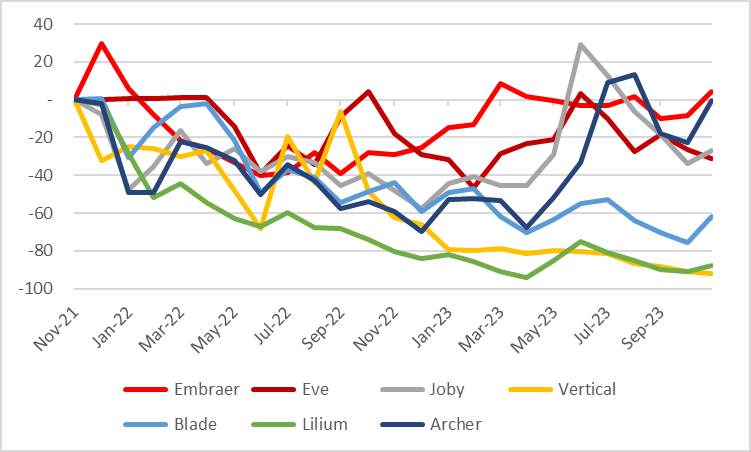

ERJ price performance vs peers (Created by author with data from Capital IQ) ERJ price performance vs eVTOL´s (Created by author with data from Capital IQ)

{kind=link}

{kind=link}

Operating Update

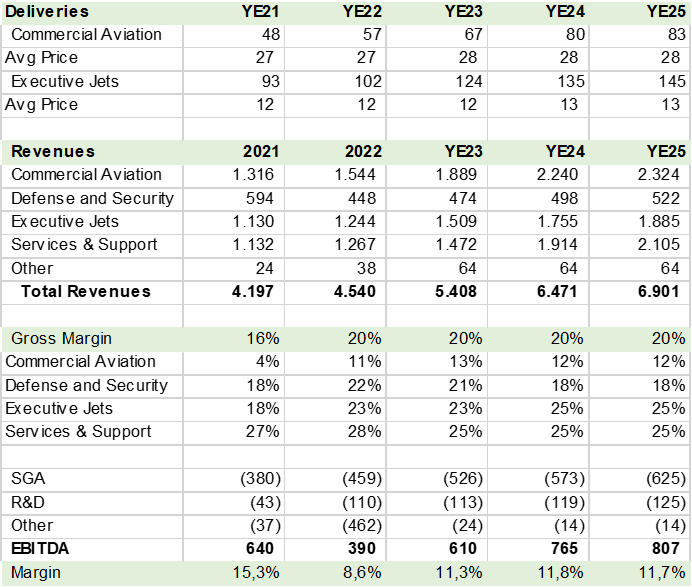

Following the 3Q23 results and meeting with the investor relations team I have updated my estimates, with the main difference being in higher Service & Support revenue due to the Pratt Whitney service contract that starts in 2024. In addition, deliveries in the Commercial Aviation and Executive Jet segments also increase per company backlog and guidance. The combination helps increase margins and more importantly, generates free cash flow that reduces debt and better prepares Embraer to develop the eVTOL and SAF aircraft to meet carbon neutrality.

ERJ Operating Forecast (Created by author with data from Embraer)

{kind=link}

Commercial Jets

In my last article; Embraer: Stock Cheap Despite Transition Risks , I was more positive on valuations than on operating recuperation given the stiff competition in the 100-120 seat segments where ERJ needed to prove that the E2's lower operating costs are worth integrating into Boeing or Airbus fleets. Since then, the company has added US$800m to its firm order book and is meeting delivery guidance in the commercial jets segment. ERJ may reach 80 units in 2024, 50% in the E1 -175 regional Jet category and the rest in E2 190-195.

Executive Jet

ERJ continues to gain share with its value proposition in the executive jet category, the key is the lower maintenance and rapid configuration of the jets. Embraer builds executive jets from resilient military and regional jet designs where aircraft are built to fly 3,000 hours vs competitors' 600 hours per year. The company should continue to increase deliveries as it builds out its dedicated service centers. The fractional ownership companies may replace and increase their fleets with ERJ units as seen in the NetJets US$5bn deal.

Services Centers

This is the most lucrative business line with gross margins of 25% which is growing at over 15% a year. ERJ recently signed an exclusive engine maintenance agreement with Pratt Whitney for the European market that may add US$500m to revenue in 2024. This is about 8% of consolidated revenue.

Valuation

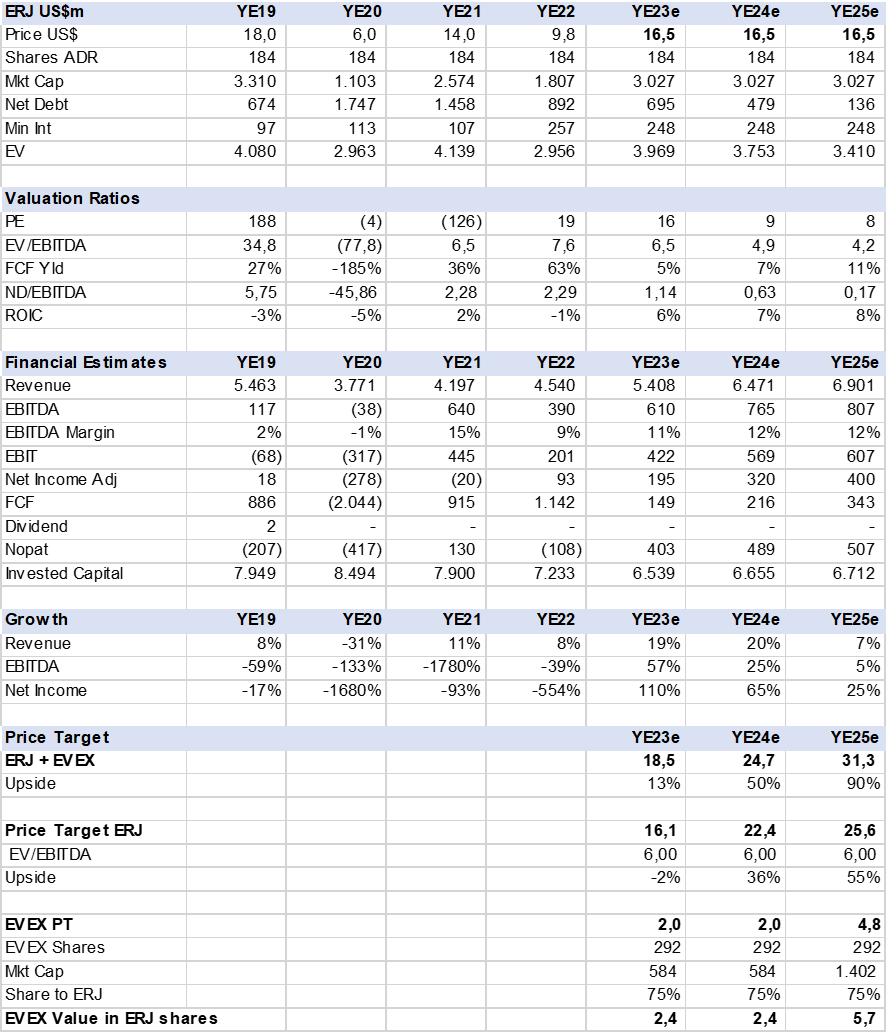

It may be tempting or "correct" to value ERJ on a sum of the parts basis, incorporating its stake in EVEX at the current price or even using a consensus price target. However, I prefer to be far more conservative and assign a US$2 per share valuation to EVEX, it is unlikely that the eVTOL will go into production until 2026 at the earliest. Thus, the bulk of ERJ's valuation depends on its EBITDA generation and a low EV/EBITDA multiple of 6x. This is considerably lower than most of its history.

ERJ Summary Financials and Valuation (Created by author with data from Embraer)

{kind=link}

Conclusion

I rate ERJ a Buy. The company continues to deliver its operating turnaround with an increasing focus on free cash flow generation and debt reduction. Its current valuation is attractive vs peers and historic levels while the stake and leadership of EVEX add significant upside without perceivable increased risk.

For further details see:

Embraer: Getting More Attractive