BNDW - EMD: This Emerging Markets Debt CEF Can Add Diversification To A Portfolio

2023-12-06 11:52:22 ET

Summary

- Western Asset Emerging Markets Debt Fund Inc offers income-focused investors the opportunity to diversify their portfolios with high-yielding emerging market sovereign debt.

- The EMD closed-end fund has outperformed other bond ETFs and indices year-to-date, delivering an 8.46% total return.

- The EMD fund invests in a mix of sovereign and quasi-sovereign bonds, with a focus on investment-grade securities and a reasonable level of leverage.

- The fund failed to cover its distribution during the first half of the year and appears to be failing to cover it during the second half of 2023.

- The fund is trading at a reasonable discount on net asset value.

The Western Asset Emerging Markets Debt Fund Inc ( EMD ) is a closed-end fund, or CEF, that income-focused investors can purchase to diversify their portfolios away from the United States while still receiving a very high level of income. As the name of the fund suggests, this one invests in emerging market sovereign debt, which is an interesting asset class that can provide a few advantages over developed nation debt. One of the biggest advantages is that emerging market debt tends to have higher yields than most developed countries’ sovereign bonds, which could be very attractive to investors who are seeking to maximize their income potential. The majority of emerging nations also have lower government debt relative to the size of their economies than developed countries. Unfortunately, there are some emerging nations that have a history of government instability or of defaulting on their obligations so the risks of investing in these securities can be somewhat greater than developed nation debt. Fortunately, this fund is taking some steps to protect its investors against this risk.

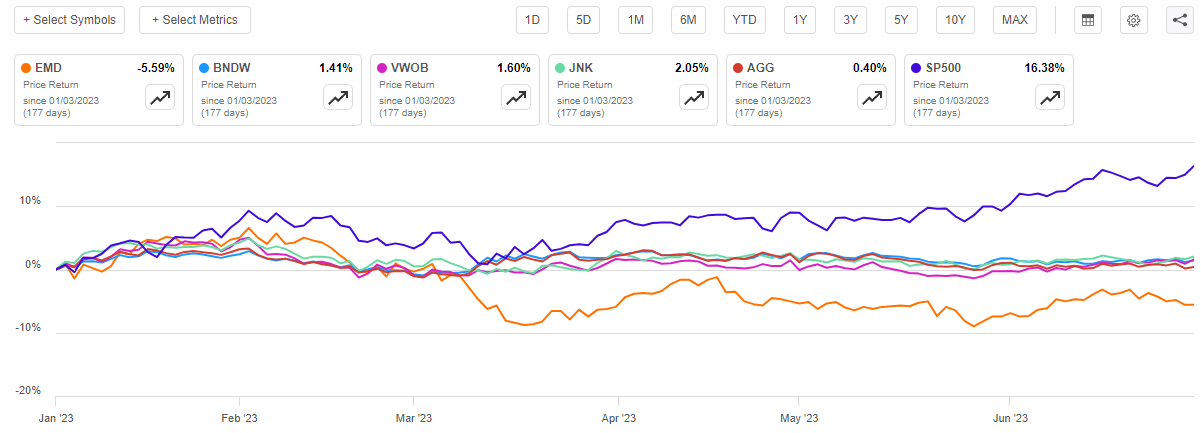

The Western Asset Emerging Markets Debt Fund has actually managed to deliver a very respectable performance year-to-date. After taking the distributions into account, investors in the fund have received an 8.46% total return since the start of 2023. This is quite a bit better than the Vanguard Total World Bond ETF ( BNDW ) or the Vanguard Emerging Markets Government Bond ETF ( VWOB ) have managed to deliver over the same period:

{kind=link}

While it is true that the performance of this fund cannot compare to a common stock index like the S&P 500 Index ( SP500 ), that is a completely different asset type and is therefore not comparable. The fact is that emerging market bonds have delivered a remarkably good year so far as this fund has outperformed the Bloomberg U.S. Aggregate Bond Index ( AGG ) and in fact, only the American junk bond index ( JNK ) has managed to beat it:

{kind=link}

Thus, the fund appears to have a lot to offer to income investors who are interested in investing in the bond space. The downside of the higher returns, though, is of course the risk.

About The Fund

According to the fund’s website , the Western Asset Emerging Markets Debt Fund has the primary objective of providing its investors with a very high level of current income. It does have a secondary objective of capital appreciation, but as I have mentioned in numerous previous articles it is very difficult to obtain capital appreciation from bonds because bonds do not have any net capital gains over their lifetimes. An investor purchases a bond at face value and receives face value back at maturity, so the only investment returns that these securities deliver over the long term are the direct payments that they make to their investors.

As mentioned in the introduction, emerging market bonds tend to have higher yields than their developed nation equivalents. The average coupon yield of the bonds in this fund’s portfolio is 8.53% right now, which is comparable to the average coupon in many domestic junk bond funds. It is important to note though that this is not the average yield-to-maturity of the fund. Unfortunately, neither the website nor the fund’s fact sheet provides the current yield-to-maturity of the fund. The only real information that we have about the yield of the bonds is this chart from the fact sheet:

Fund Fact Sheet

There is a big difference between the average coupon and the current yield-to-maturity, however. The fund is benchmarked against the J.P. Morgan Emerging Markets Bond Index Global Diversified ( EMB ), which has a 7.35% average yield-to-maturity right now so that would probably be a reasonably good guess for this fund. Regardless, we can clearly see that the bonds held by this fund boast yields that are well beyond that of most developed countries, although they no longer have the yield premium over domestic junk bonds that they had a few years ago.

The Western Asset Emerging Markets Debt Fund is not entirely invested in sovereign bonds, although they are the largest proportion of its holdings. As we can see here, emerging market sovereigns only constitute 43.91% of the fund’s total holdings:

Fund Fact Sheet

We do note that the fund has a 13.79% weighting to what it calls “quasi-sovereign” bonds. These are akin to agency securities in the United States. According to M&G Investments :

While the definition varies across market participants, an entity or company is typically defined as ‘quasi-sovereign’ if a government owns either more than 50% of its equity or more than 50% of the company’s voting rights.

Historically, developing countries have been using quasi-sovereign issuance to fulfill policy function, develop the hard currency corporate debt market, or promote international expansion of leading domestic players. As of the end of June 2015, there were about 170 quasi-sovereign issuers in emerging markets, more than 60 of which were fully owned (such as Petroleos Mexicanos, or Pemex, in Mexico) or issued bonds explicitly guaranteed by their respective governments (for example, Magyar Exim Bank in Hungary).

Clearly, the bonds issued by these entities function much like agency securities issued by Fannie Mae, Freddie Mac, or similar entities in the United States. They are not directly issued by a sovereign government but may have an implicit or explicit guarantee that the government will step in and ensure that the payments get made to the bondholders in the event of financial problems. After all, even if it is just a case of the government owning a controlling stake in the company, the government probably has sufficient control over the company and is using it to pursue its own interests. A company like Petrobras ( PBR ), which has very favorable treatment in the Brazilian oil industry could be an example of this.

The Western Asset Emerging Markets Debt Fund has a 13.79% weighting to quasi-sovereign securities. When we consider that these securities probably have some sort of government backing, we can see that over half of the fund’s assets probably have the safety of a government guarantee. Admittedly, that guarantee may not be considered as sound as if the government of a developed nation were backing it, but it is still better than ordinary corporate securities or junk bonds.

As mentioned already, emerging markets are generally considered to be at higher risk of default losses than developed markets. This is because some of these nations have a history of government instability, confiscation of private assets, or past defaults. For example, Mexico, which is the second-largest country weighting in the fund, defaulted on its debt in 1982 during the Latin American debt crisis. Other countries whose debt accounts for significant portions of the fund such as Argentina and Brazil have also defaulted on their national debt. As of right now, Mexican issuers account for 8.23% of the fund, Brazilian issuers account for 4.88%, and Argentinian issuers account for 4.18% of the fund’s total holdings:

Franklin Templeton

The fact that some of these countries have a history of defaults in the past is something that could concern potential investors. This is particularly true for those investors who are highly risk-averse and are worried about the preservation of principal, which is a category that would likely include many retirees. Fortunately, we may be able to obtain some comfort by looking at the credit ratings that have been assigned to the securities in the fund’s portfolio. Here is a brief summary:

Franklin Templeton

An investment-grade bond is anything rated BBB or higher. We can quickly see that this category includes 45.22% of the fund’s assets. Cash and cash equivalents are also typically considered investment-grade or better, so that brings us up to 45.80% of the fund’s total assets. We can also see that another 30.98% of the fund’s assets are BB-rated and 14.45% are B-rated securities. That puts 45.43% of the fund’s assets into one of the top two speculative-grade categories. According to the official bond rating scale , entities with a BB or B rating have sufficient financial strength to meet all of their current debt obligations even in the event of a short-term economic shock. Thus, we can probably be reasonably confident that 91.23% of the fund’s assets are at a pretty low risk of default. This is certainly a strong enough ratio that most risk-averse investors should be comfortable with the risks here.

One advantage that emerging market nations have over developed countries is that their government debt levels are considerably lower. For example, let us look at the debt-to-GDP ratios of the largest countries in the fund’s portfolio:

| Country |

| Debt-to-GDP |

| United States |

| 129% |

| Mexico |

| 49.6% |

| Indonesia |

| 39.9% |

| Brazil |

| 72.87% |

| Argentina |

| 85% |

| Oman |

| 40.2% |

| Dominican Republic |

| 58.56% |

| Peru |

| 33.8% |

| Columbia |

| 63.6% |

| Kazakhstan |

| 24.4% |

In addition to having a much lower level of debt relative to the size of their economies, many of these nations either have balanced budgets or are very close to it. They certainly are not running deficits in excess of 10% of gross domestic product, as the United States has done in recent years. This should give them a bit more flexibility when it comes to carrying their debt loads and making payments to investors than developed nations with higher debt. However, perhaps the most important benefit comes from the potentially higher economic growth.

Back in 2010, American economists Carmen Reinhart and Kenneth Rogoff published a paper in the American Economic Review that details the impact that high levels of government debt have on economic growth. The paper argues that when external debt exceeds 60% of gross domestic product, a nation’s economic growth declines by 2%, and its gross domestic product growth gets cut in half when external debt exceeds 90% of gross domestic product. This paper was admittedly criticized for containing a few errors in its calculations and assumptions, but further analysis by both the original authors and the International Monetary Fund also found the same effect to a lesser degree. In short, there is little argument among serious economists that a higher level of national debt relative to gross domestic product results in a lower level of economic growth. We can even see this in the United States, as the 4% to 6% year-over-year gross domestic product growth that the United States experienced regularly prior to 2007 has now declined to 1% to 2% on average in the past fifteen years or so:

{kind=link}

Thus, we can conclude that the lower debt levels possessed by the countries whose securities are represented in this fund give the potential to deliver higher economic growth than the United States and the rest of the developed world. That economic growth should make it easier for them to carry their debts over time. As such, it could be a smart decision to have some exposure to emerging market debt instead of investing solely in American or other developed-nation debt securities. The Western Asset Emerging Markets Debt Fund is one way to obtain that foreign debt exposure.

Leverage

As is the case with most closed-end funds, the Western Asset Emerging Markets Debt Fund employs leverage as a method of boosting the effective yield that it receives from the assets in its portfolio. I explained how this works in a number of previous articles. To paraphrase myself:

In short, the fund borrows money and then uses that borrowed money to purchase bonds issued by emerging market sovereign nations and corporations. As long as the interest rate that the fund has to pay on the borrowed money is less than the yield that the fund receives from the purchased securities, the strategy works pretty well to boost the effective yield of the portfolio. This fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates. In addition, the fund can borrow money in developed nations, which tend to have lower interest rates than most emerging markets. As such, it will usually be the case that the fund can borrow for less than it receives from its assets.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage as that would expose us to an excessive amount of risk. I do not typically like to see a fund’s leverage exceed a third as a percentage of its assets for this reason.

As of the time of writing, the Western Asset Emerging Markets Debt Fund has leveraged assets comprising 29.44% of its total assets. This is a reasonable level that is well below the one-third maximum level and represents a reasonable balance between risk and reward. This is quite nice to see since emerging market bonds can be somewhat more volatile and riskier than developed market bonds. Overall, we should not need to worry too much about this fund’s current leverage.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Western Asset Emerging Markets Debt Fund is to provide its investors with a very high level of current income. In order to achieve this objective, the fund invests its money into a portfolio that consists of both government and corporate bonds from issuers that are located in emerging markets around the world. These securities tend to have higher yields than comparable securities issued in developed markets, and this fund collects the money paid in interest by these bonds. The fund even goes so far as to borrow money so that it can control more securities than it ordinarily could, which results in even larger amounts of money coming into it. Finally, the fund might occasionally realize some capital gains by selling bonds that have appreciated in price. It pools all of the money that it receives from these various activities and then pays it out to its shareholders, net of its expenses. We might expect that this will allow the fund to have a very high yield.

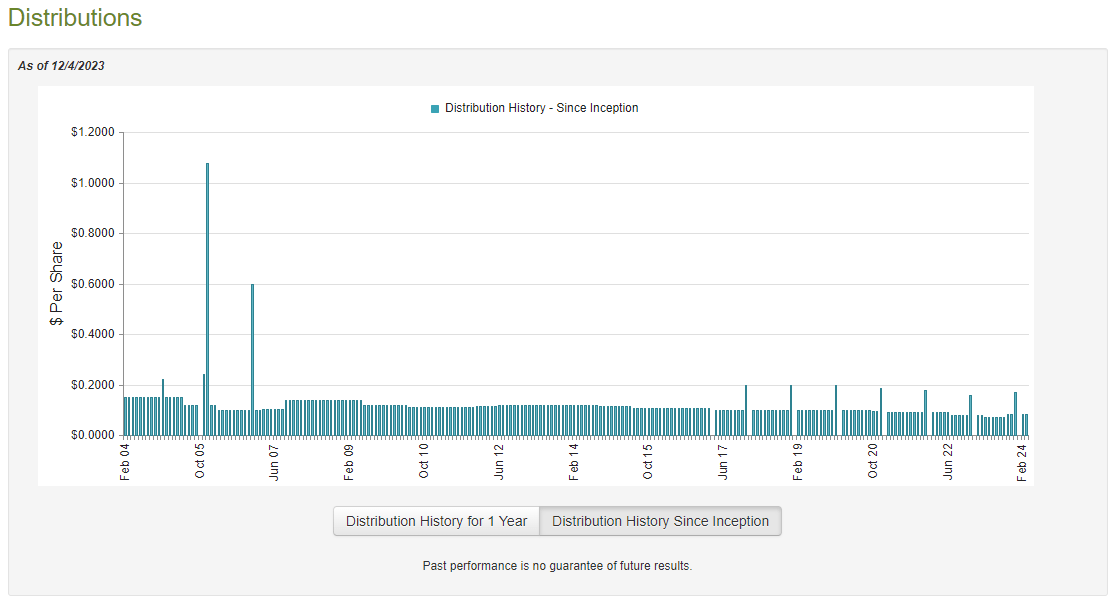

This is indeed the case, as the Western Asset Emerging Markets Debt Fund pays a monthly distribution of $0.0845 per share ($1.014 per share annually), which gives it an 11.44% yield at the current price. Unfortunately, the fund has not been particularly consistent with respect to its distribution over the years. In fact, as we can see here, the fund has both raised and cut its distribution numerous times over its history:

{kind=link}

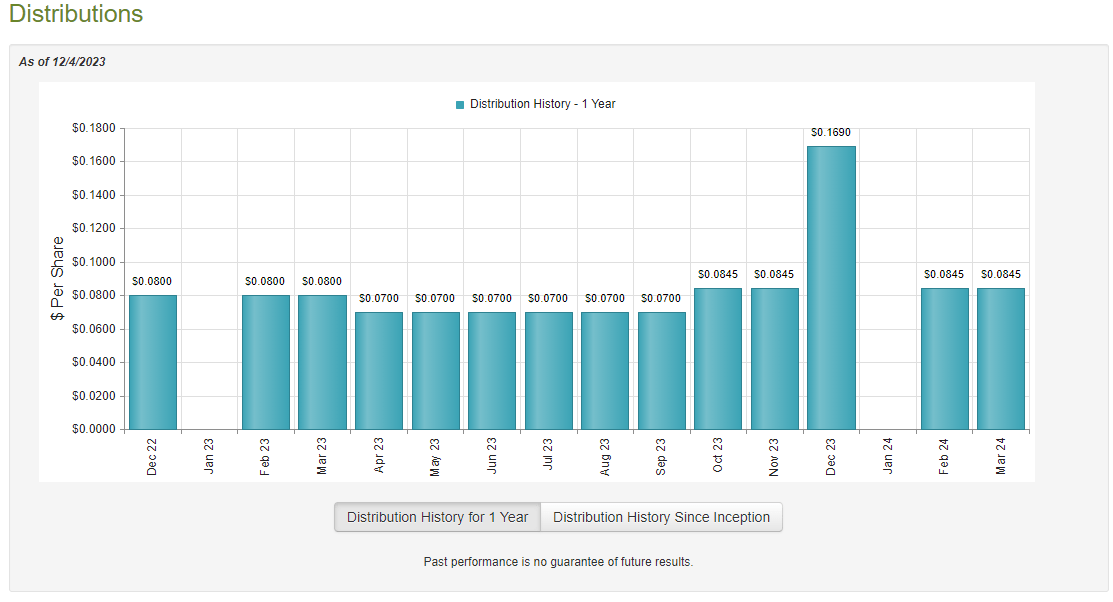

The fund has even altered its distribution twice in the past year:

{kind=link}

As such, the fund may not appeal to those investors who are seeking to earn a consistent level of income from their portfolios that can be used to pay their bills or finance their lifestyles. However, fixed-income funds tend to change their distributions regularly as things such as interest rate changes can have significant impacts on the value of their assets. This fund does not have much foreign currency risk though, so that does not appear to be a problem here.

As I have pointed out before, the fund’s history is not necessarily the most important thing for us to consider. After all, anyone who purchases this fund today will receive the current distribution at the current yield and will not be affected by actions that the fund has had to take in the past. The most important thing for any buyer today is how well the fund can sustain its current distribution. Let us investigate that.

Fortunately, we have a fairly recent document available that we can use for the purposes of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on June 30, 2023. This was generally a good period of time for the American markets, as the S&P 500 Index appreciated 16.38% over the course of six months due to the market’s euphoria surrounding artificial intelligence and the prospect of interest rate cuts. However, emerging markets did not do as well with sovereigns only being up 1.60% over the period:

{kind=link}

However, the fund might have still had the opportunity to generate some capital gains profits by selling securities that were appreciated during the period. This report will give us a good summary of how well the fund did at this task.

During the six-month period, the Western Asset Emerging Markets Debt Fund received $32,324,452 in interest and $112,716 in dividends from the assets in its portfolio. We naturally have to subtract out the foreign withholding taxes that the fund needed to pay over the period, which gives it a total investment income of $32,289,682 over the course of six months. The fund paid its expenses out of this amount, which left it with $21,424,562 available for shareholders. That was, unfortunately, not enough to cover the $26,508,245 that the fund paid out in distributions over the period. At first glance, this is likely to be quite disappointing and concerning since we usually would like a fixed-income closed-end fund to be able to fully cover its distribution with its net investment income.

However, the fund does have other methods through which it can obtain the money that it needs to cover its distribution. For example, it might be able to make a profit by selling appreciated bonds into a friendly market. Realized gains are not considered to be a part of investment income for reporting purposes but they obviously represent money coming into the fund. Unfortunately, the fund did not have a lot of success at this task during the period. The fund reported net realized losses of $27,648,316 that were partially offset by $25,235,713 in net unrealized gains. Overall, the fund’s net assets declined by $7,496,286 over the six-month period after accounting for all inflows and outflows. This is not exactly something that we want to see, as it suggests that the fund cannot sustain its distribution.

The fund has failed to cover its distribution during the second half of this year as well. As we can see here, the fund’s net asset value per share is down 0.49% since July 1, 2023:

{kind=link}

This strongly suggests that the fund is currently paying out more than it has been able to earn from its investment portfolio. Admittedly, this is only a slight decline, but it is something that the fund will need to correct if it wishes to sustain its distribution at the current level.

Valuation

As of December 4, 2023 (the most recent date for which data is currently available), the Western Asset Emerging Markets Debt Fund has a net asset value of $10.09 per share but the shares currently trade for $9.00 each. This gives the fund’s shares a 10.80% discount on net asset value at the current price. This is nowhere near as attractive as the 14.89% discount that the shares have had on average over the past month, so it might be possible to obtain a better price by waiting for a little while. With that said, a double-digit discount is generally representative of a reasonable entry price for any fund, so it is not a terrible idea to buy at today’s price.

Conclusion

In conclusion, the Western Asset Emerging Markets Debt Fund is one of the few fixed-income funds that provides exposure to a portfolio of debt issued by government and corporate entities located in emerging markets. There can be some advantages to investing in these securities, as the diversification benefits are quite high, and many emerging markets have lower debt levels and lower deficits than developed nations.

The real risk here seems to be that the Western Asset Emerging Markets Debt Fund is paying out more than its portfolio has generated. That is not sustainable over an extended period, so the fund will need to correct this problem. It is possible that it will accomplish that though, particularly if the current market strength holds.

For further details see:

EMD: This Emerging Markets Debt CEF Can Add Diversification To A Portfolio