EMRAF - Emera: 6.2% Yielding Utility Deserves An Upgrade

2023-11-01 00:17:45 ET

Summary

- Our initial coverage of Emera started with a Sell rating.

- The company has navigated some of the challenges, though many remain.

- We give you three reasons why we are giving this an upgrade.

Stories seldom evolve exactly how you envision them. Along the way, the twists and turns give you opportunities to change your mind. We have had a few twists and turns in the case of Emera Incorporated ( EMRAF ) ( EMA:CA ) and it has certainly been one we are ready to change our tune. Let's go over where we started and where we are at.

The Company

Headquartered in Halifax, Nova Scotia, Emera Incorporated is an owner and operator of regulated utilities in Canada, the US and the Caribbean. Till recently, it followed a broad-based capital investment program. The decision in Nova Scotia which limited its return profile from investments, changed that. The company has decided to focus its investments more on Florida, where it sees less regulatory risk and a stronger return profile.

Prior Coverage

When we started coverage of Emera, it was all about the fact that the utility was one of the most leveraged in the space and teetering on credit downgrades from all the 3 rating agencies. Moody's ( MCO ) actually had this one ready to go into junk territory. The biggest issue was still that the company was priced for rainbows and butterflies and that led us to a sell.

That does give it some time, but we have to put our weight behind Moody's here and think the Baa3 (one step above junk) with negative outlook, is more representative of the risks. We are issuing a Sell rating here and expect the combination of these headwinds to warrant a dividend freeze, large equity issuance and a move to 15X normalized earnings. That gets us to about $45 CAD per share.

Source: Don't Chase That Yield

That said, there are three reasons today that Emera warrants an upgrade.

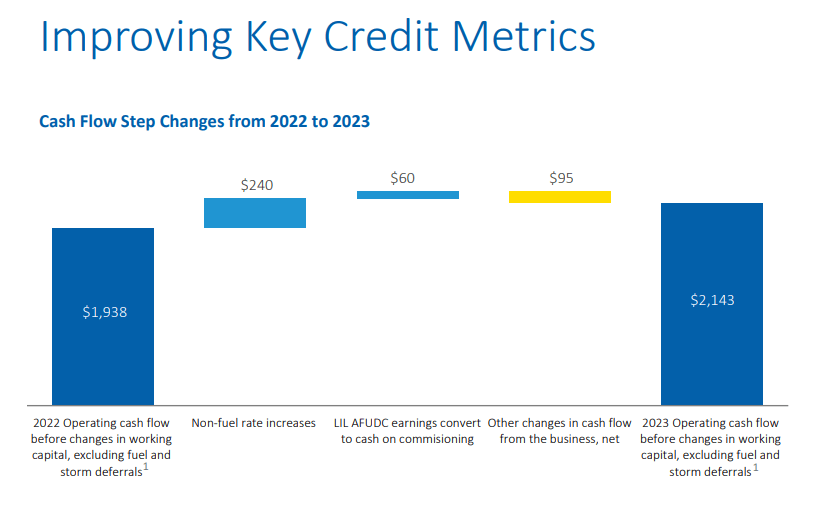

1) Improving Cash Flow Profile

EMA's Q2-2023 was solid and cash flow improved year over year.

{kind=link}

Emera focused on the key metrics which credit agencies had stressed. The move from 11% to 11.5% is material considering that we still have some tailwinds for further improvement.

Emera Q2-2023 Presentation

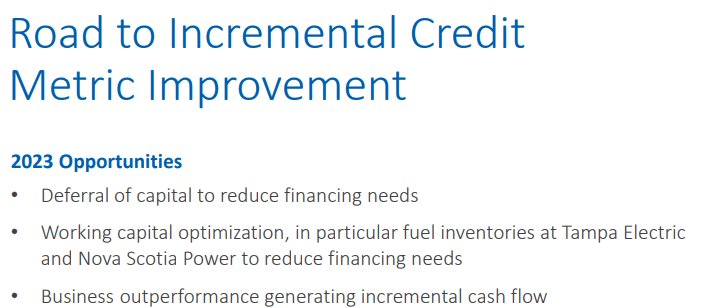

In the back half of the year, Emera committed to deferral of some capital spending and getting some mileage out of optimizations.

{kind=link}

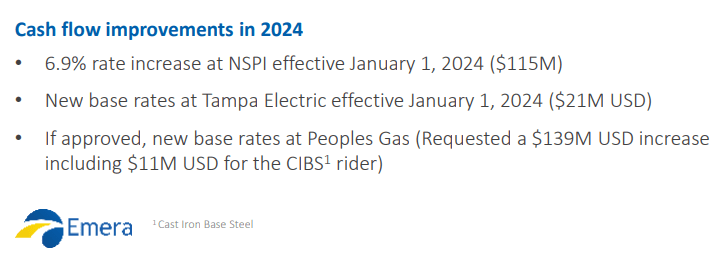

It has some further step-ups in 2024 that should help it a little more.

{kind=link}

The combination of these actually helped Emera avoid extensive equity issuance.

Mark Jarvi

That’s good to hear, thanks for that, Archie.

Just one last question for Greg, just in terms of not seeing the ATM usage here in the first half of the year. Is that partly just a reflection of the deferral of the investment in LIL?

Greg Blunden

Yes, it’s a combination of things, Mark. Obviously share price has been depressed, but maybe equally so the volatility around it has been hard to land on. But yes, we’ve seen significantly stronger cash flows, in particular the fuel recoveries that we had, and we’re deferring some capital, but you should expect that you’ll see us back into the ATM market in the second half of the year, kind of consistent with prior periods.

Source: Emera Q2-2023 Conference Call Transcript

2) Loonie Going The Right Way

For a Canadian utility with operations primarily in US, the exchange rate is a big factor in the total revenue and cash flow profile. In this regard, let us look at the chart of the USD-CAD exchange rate from January 1, 2022 till June 30, 2023. We are using June 30, 2023 in this first one to show you where it traded at in the timeframe that Emera had its first two fiscal quarters.

It is pretty clear that the "Loonie" was weaker in 2023 versus 2022. Emera dropped this tidbit for the investor base in its Q2-2023 results.

The weakening Canadian dollar also increased the earnings contribution from U.S. operations by $8 million for the quarter.

Ok, so that was that. Now let us look at that same exchange rate from June 30, 2023 onwards.

Yep. You get it and that is our point. The weaker Loonie is one terrific tailwind to earnings and possibly was the reason for the 4% dividend hike . We don't think that hike was the right move as the focus should have been on getting the credit metrics in order and preserving cash. But possibly this is a back alley gambit at raising the stock price to allow an equity issuance.

3) Valuation Not Compelling, But No Longer A Headwind

In our earlier piece we had suggested that we would turn constructive under $45 CAD. We actually went well below that number and are currently trading just 1% over it.

We also went from about 19X 2023 earnings to just under 15X 2024 earnings.

We think this is in fair territory though we think it can get cheaper. One aspect here that analysts may be underestimating is the impact from the weaker Loonie. Those earnings estimates may prove slightly conservative.

Verdict

We are upgrading Emera to a "hold/neutral". Emera has done what it should have since our first article and on the sell ratings the potential returns are never going to be as high as make as they can be on the buy side.

Seeking Alpha

We have to also factor in the extremely hefty dividend yield which is near 6.3% as we write this. To reiterate a Sell, we would need the expected total returns to be at least negative 10%. That means the price would need to fall another 16%, considering the dividend. While possible, we don't think it is probable.

Keep in mind that while Emera has moved into the fair value zone, many utilities have actually become quite cheap as they were already fairly valued to begin with. Algonquin Power and Utilities ( AQN )( AQN:CA ) is definitely one worth considering.

So Emera with the Sword of Damocles (read that as 3 potential credit downgrades) hanging over its head, is possibly not the best choice for your capital even today. We continue to monitor this and will update if conditions warrant a buy rating.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

For further details see:

Emera: 6.2% Yielding Utility Deserves An Upgrade