ENB - Enbridge: The More It Drops The More We Buy

2023-11-06 07:44:45 ET

Summary

- Enbridge has a unique ability to drive long-term shareholder returns despite being punished by the market.

- The company's cash flow remains strong and reliable, with 98% of EBITDA generated from cost-of-service and contracted assets.

- Enbridge is focused on expanding its renewable business, particularly offshore wind, to diversify and add support to its cash flow.

It's tough to purchase an investment with a 4% yield when bonds are giving 5%. It's much easier to do when bonds are yielding 0%. That logic has punished Enbridge (ENB) as interest rates have gone up. As we'll see throughout this article, the $70 billion conglomerate has a unique ability to drive long-term shareholder returns.

Enbridge Highlights

The company had a strong quarter, with a $71 billion USD market cap, as it's continued to be punished by the market.

{kind=link}

The company's YTD financial performance has remained on track and the company has put together the vast majority of the funding in place for its US gas utilities acquisition. The company's debt is coming in at the lower end of its range with ~$72 billion in debt ($53 billion USD), and we'd like to see that level remain lower, especially in a higher interest rate environment.

The company has continued to see high utilization with open season initiated on several pipelines. The company is targeting $3 billion in secured capital placed into service in 2023 ($2.2 billion USD) and it expects incredibly strong returns on its Dominion asset acquisitions with additional tuck-in acquisitions for the company.

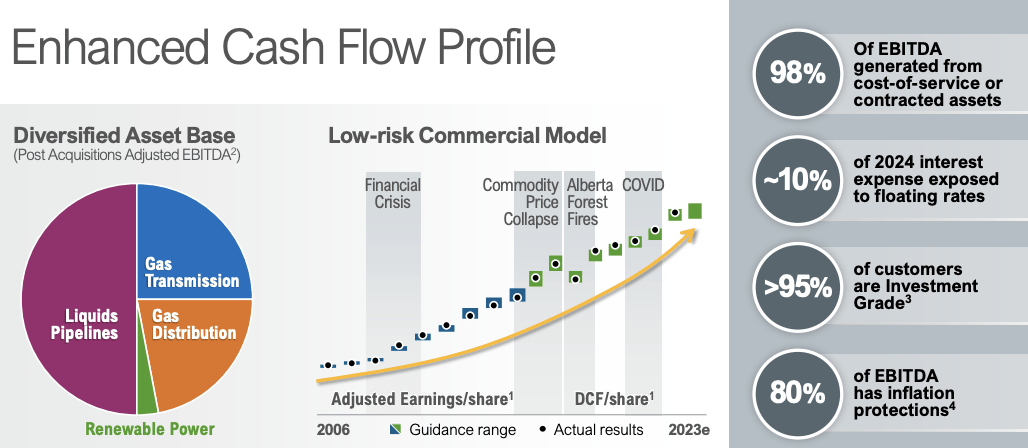

Enbridge Cash Flow

The company's cash flow remains incredibly strong and reliable despite the variance in earnings.

{kind=link}

The company has 98% of EBITDA generated from cost-of-service and contracted assets. That's almost perfectly reliable earnings, barring a major market downturn that puts these businesses out of business. The company maintains inflation protections and lines up with investment-grade customers. It also has minimal interest obligations at least in the short term.

Reliable cash flow for the company is key for the company to both maintain its dividend and drive shareholder returns.

Enbridge Gas Utilities

The company has been on a bit of a spending spree, especially for companies looking to get rid of their natural gas assets.

{kind=link}

The company's most recent massive $19 billion acquisition is at a 1.3x EV / rate base and 16.5x P/E ratio. That second part is potentially concerning. The company is utilizing some equity, but the acquisition is primarily debt-fueled. It's paying what's traditionally a low multiple for utilities but a high multiple for the company's valuation.

The company delivering shareholder returns off of these assets is based on the company receiving a rating re-evaluation from the market. By 2025 pro forma, the company will be serving a massive 7 million customers across the country.

The company is clearly committed to building up this business, and optimistically, a more reliable cash flow could lead the market to re-evaluate the company's multiple.

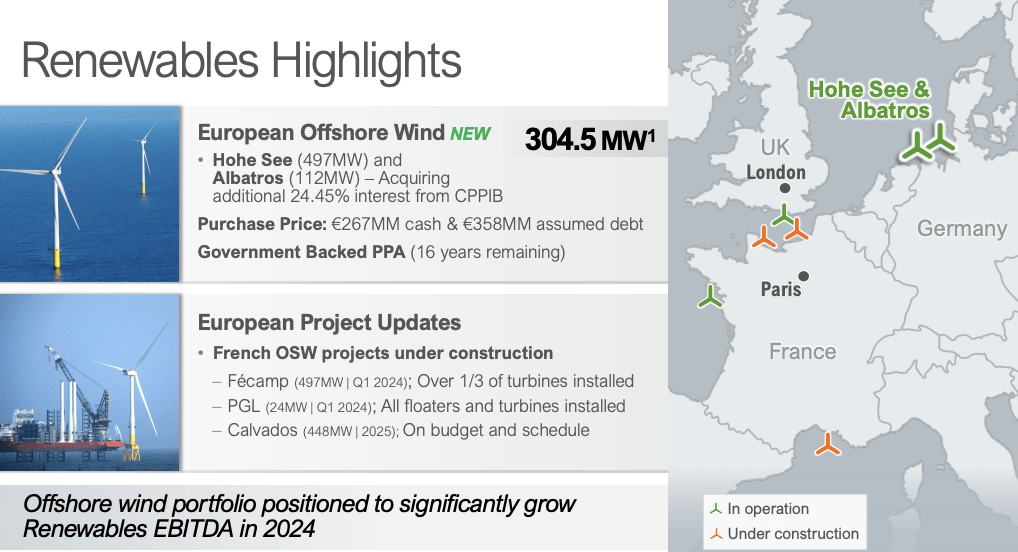

Enbridge Renewables

The company is focused on rapidly expanding its renewable business, and offshore wind remains a large part of that.

{kind=link}

The company expects its renewable EBITDA to grow substantially in 2024, with numerous new projects under construction. Especially in countries that have traditionally used natural gas, renewable projects remain huge. The company has spent roughly $600 dollars, with a 16-year power purchase agreement, for hundreds of megawatts worth of assets.

The company's focus on growing renewables will help diversify and add support to its cash flow.

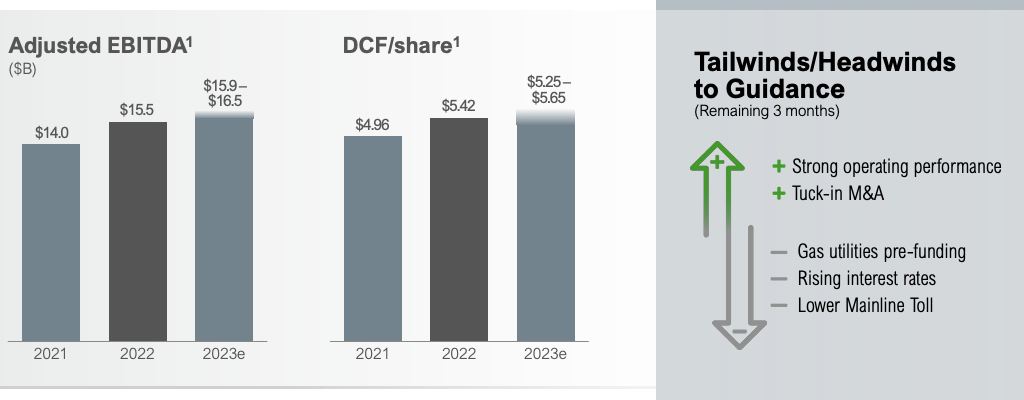

Enbridge Financials

Financially, the company did well. It's important to note that all of the below numbers are in Canadian dollars, with a USD to CAD exchange ratio of .73 to 1.0.

{kind=link}

The company earned $2.6 billion in DCF in 2023 from $3.8 billion in adjusted EBITDA. The majority of the company's financial impact came from financing costs, as the company's interest expenditures have remained high from its massive debt load. The company's EBITDA for the quarter was partially lower impacted by revised tolls and a lower ownership interest in DCP midstream.

{kind=link}

Annualized the company's financials remain strong. Midpoint EBITDA of $16.2 billion and DCF of $5.45 translates to $11.8 billion USD EBITDA and $3.98 / share USD in DCF. Versus the company's share price of just under $34 / share, that's an almost 12% DCF yield. That shows the company's strong financial positioning as it pays a dividend of >7.5% and has extra cash flow.

We'd like to see the company slow down the expansion rate and focus on driving some shareholder returns, rather than growth at all costs. Specifically repurchasing shares, or paying down debt in the current higher interest rate environment could go a long way. Regardless of how the company spends its cash though, it's a valuable investment.

Thesis Risk

The largest risk to our thesis is the company's long-term debt and its continued use of debt as a financing vehicle in a high-interest rate environment. The company's EBITDA forecast for the year is $16 billion and the company's target debt range is 4.5x-5.0x, implying $76 billion in debt. That's risky for the company.

Conclusion

Enbridge has been punished by the market. The company has a $71 billion market cap, and an enterprise value of roughly $125 billion counting its hefty debt load. The company has been punished by rising interest rates, with a dividend yield of more than 7.5%, which it can comfortably afford to pay. That comes from the company's strong DCF.

The company is focused on rapid growth. It's been spending many billions making acquisitions and growing, and many of those growth projects are coming into service. In fact, effectively all remaining cash flow post distributions is going into growth. That's worth paying close attention to if the growth doesn't pan out.

For further details see:

Enbridge: The More It Drops, The More We Buy