EHC - Encompass Health Corporation: Solid Quarterly Report Makes For A Buy

2023-08-14 15:55:41 ET

Summary

- Encompass Health Corporation has seen 11.7% YoY revenue growth and a 30% increase in share price over the past year.

- EHC's recent Q2 results were impressive, with strong earnings and an increased 2023 guidance.

- EHC has solid margins, a sustainable dividend, and better growth prospects compared to its industry peer, Acadia Healthcare Company, Inc.

Investment Outline

Momentum continues for Encompass Health Corporation ( EHC ) as revenues grow by 11.7% YoY. Engaging in the healthcare facilities industry, EHC has built up a strong market position for itself. The valuation continues to look appealing, even after the run-up it has had in the last several months.

Looking at the returns from an investor in EHC over the last 12 months, I think you’d be very pleased as the share price has grown over 30%. After a solid recent quarter from the company, it continues to provide why it can be a viable investment and addition as a long-term position. The market seems to continue to value the company as a growth company with a p/e of 20 based on forward projections. However, I see this as a fair assessment, giving the EBITDA grew by 27% YoY. Concluding my view on EHC I am rating them a buy.

Recent Developments

Not that long ago, we got the Q2 results for FY2023 from the company. Results were impressive and seem to have further driven the share price higher. Where there were some disappointments that perhaps came in the shape of decreasing FCF year-over-year. Seeing as the earnings for the company remain strong, I think it doesn't do enough to harm the investment thesis. The dividend yield for the company is under 1% and has a payout ratio of 17%. It doesn’t seem like the continued dividend is going to hurt the future investment potential of the business.

Earnings Highlights (Earnings Report)

Looking at what the management of the company had to say about the quarter, the CEO Mark Tarr said the following, “Strong discharge growth of 9.8% combined with year-over-year improvement in labor costs to drive Adjusted EBITDA growth of 27.1%. Our value proposition and operating strategy continue to be validated, and we remain highly optimistic about the long-term prospects of our business. We are increasing our 2023 guidance to reflect our strong first-half results and updated expectations for the balance of the year”.

2023 Guidance (Earnings Report)

Guidance is now set to be $3.31 - $3.53 for the EPS. On the higher end, that puts EHC at a FWD p/e of 19.8. In comparison to the sector, it seems we are getting a slight discount here of about 5%. For growth companies, I do prefer some margin of safety to make it a buy, it seems like we are getting a sufficient one here right now.

Looking deeper at the earnings report, it is reassuring to see the interest expenses decreasing for the company as the debt position they hold continues to compress. For the six months of 2023, the interest expenses were at $72 million, compared to $100 million a year prior. This is enhancing the margins and creating strong foundations for EHC to build upon going forward.

Positioning And Catalysts

In the short term, I don't see any significant catalyst that would make the earnings shoot up or for EHC to be able to increase its prices significantly. Instead, growth is coming at a steady pace, which has been reflected in the share price. It's a story of the more you put in, the more you get out, basically.

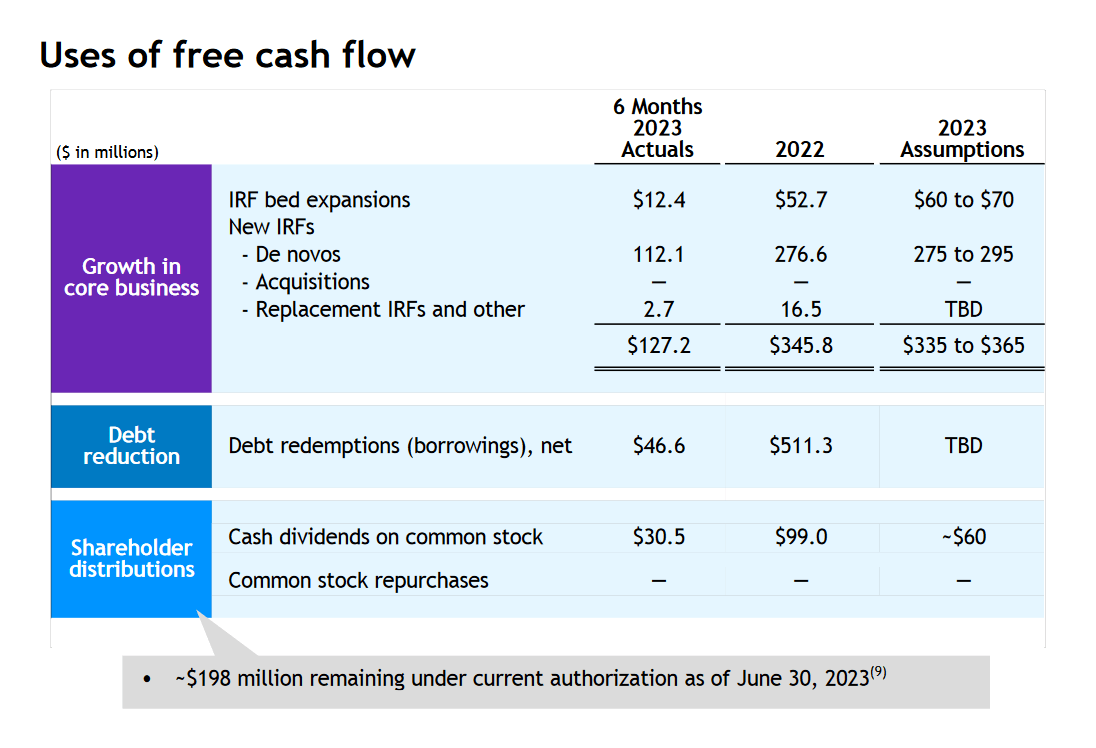

Cash Flows (Earnings Presentation)

{kind=link}

EHC's expansion trajectory hinges substantially on the purchases of new facilities and the addition of fresh "beds" to ensure shareholder value. This strategic approach necessitates a continuous commitment to investments, serving as the engine that propels the company's growth ambitions. However, as with any substantial growth initiative, the financial resources to fuel this progression must be secured. As a result of the solid market conditions that the company operates in, they were able to raise the guidance for 2023 in the last report and EPS is now projected to reach $3.31 - $3.51 for the full year. Maintaining margins will only add more capital to the company to continue expanding, and a reasonable assumption would be that EHC can grow the bottom line by at least 6% - 7% annually given the current amount they are allocating for growth ventures.

For EHC, the means of sourcing these necessary funds have entailed a dual approach. The first facet involves leveraging the issuance of new debt, and strategically tapping into the financial markets to access the capital required for its expansion endeavors. This measured use of debt allows EHC to secure the resources needed to construct and establish new facilities, while simultaneously managing its financial obligations. So far it has gone very well and with a net debt/EBITDA of 2.92, the company still sits in a place that I would consider safe from a debt repayment perspective. I doubt they will face significant challenges paying it down, and this further adds to the buy case in my opinion.

Margins

Margin Profile (Seeking Alpha)

Taking a look at the margins of the business, I think they remain very solid. The company has made a strong effort to maintain margins but also improve upon them. The net margins sit close to their highest levels in the last 5 years, and the gross margins are at their highest right now. This is reassuring to see despite the macro headwinds such as heightened interest rates and labor inflation. I do expect EHC to consolidate slightly around these margin levels, but once we get interest rates down, I do think it's reasonable to assume margins will improve once again. What makes me have this assumption comes down to that Medicare pricing is set to increase by 4% in Q3 and by 3.3% in Q4.

Value For Investors

The way that EHC right now is passing on earnings to investors comes from the dividend. It has a yield just shy of 1% and a payout ratio of just over 17%. I don’t find this to be unsustainable, and it seems like they are maintaining the $0.15 quarterly dividend. This is down from where they were in 2021 when the quarterly dividend was at $0.22 instead. I think that a wise decision from the company was to adjust it downward in the face of rising interest rates. This has created a financial condition for the company that lets them still invest quite heavily and grow both the top and bottom line as we saw in the last report. Where I do have some concerns is that the shares are being diluted slightly on a YoY basis, which, of course, is harming the investment thesis right now. However, the rate at which it's done isn't substantial enough to warrant a hold for the company.

Risks

One of the risks that investors face here is that there is a real possibility of a correction in the share price if we enter into a slower economic period. The share price has been steadily climbing, and I think some sort of consolidation is likely before potentially going higher. Volumes traded are quite low, and I think a slowdown would cause a quick severe decrease in the share price.

Some factors to look out for specifically with EHC here would then be decreasing margins and difficulty to raise them. A slowdown or plateauing of revenues would also be early signs that perhaps the growth cycle has come to a halt and a reassessment of the company is needed.

Company vs Peers

Comparing EHC to a peer in the industry like Acadia Healthcare Company, Inc. ( ACHC ) I think that EHC still seems to come out ahead. As for EHC, the p/e sits below that of ECHC by around 10% and the growth prospects seem better too. Averaging a 10% annual growth rate for the EPS for the next several years at least.

The lack of dividends from ACHC is also a contributing factor to the more positive view I have of EHC in comparison. Besides that, looking at the margins of the businesses, EHC comes out ahead with the least positive FCF. On the side of ACHC, it is instead negative, which is concerning for the company and the potential value that investors could extract. This concludes to me rather be in EHC than ACHC right now.

Investor Takeaway

EHC has made a name for itself in the healthcare facilities industry, where it provides post-acute healthcare services in the United States. Specializing in rehabilitative treatment, the company has been able to grow both the top and bottom lines rather well in the last few years. The Q2 report we got recently cemented the fact that EHC is a growing company with a valuation that doesn't quite match that. This leaves an opportunity for us to invest at what I think is a discount to the sector. Rating EHC a buy as a result.

For further details see:

Encompass Health Corporation: Solid Quarterly Report Makes For A Buy