EHC - Encompass Health: Rotating Capital Investments Into Market Valuation

2023-05-11 17:45:24 ET

Summary

- Encompass Health Corporation continues to deliver in 2023, with investors rating its market valuation higher after Q1 FY'23 earnings.

- The company's financial performance is matched by a deeper set of drivers underneath the hood.

- Encompass is incrementally rotating capital investments into market valuation and this could continue moving forward.

- Net-net, reiterate buy.

Investment summary

Investor funds are still in good hands with Encompass Health Corporation (EHC), in my opinion. Following the company's Q1 FY'23 earnings , the numbers show it is still recycling investment capital into profitable assets, that are generating cash flows for investors above the hurdle rate.

EHC's use of retained earnings has translated into market value appreciation over the last 12-months, and my analysis suggests these trends could remain in situ if certain milestone are met. EHC has fairly attractive business economics that are incrementally nudging its share price back above long-term range. Findings show this is a defensive versus growth holding that can balance equity risk for investors focused on the long-term.

In view of the rally since July last year, the market still rates EHC in-line with 5-year historical averages at 19x forward P/E and 3x book value. These are fairly expensive numbers if you ask me and put EHC well ahead of the U.S. equity benchmarks (UST 10-year and S&P 500). Hence, you're paying a premium at those multiples which must be considered. The long-term economic business characteristics under EHC's hood enable the investor to grow capital above the hurdle rate in my opinion. Amid the ebbs and flows, long-term capital gains are a key focus for the company. Net-Net, continue to rate EHC a buy with a $75-$90 price range.

Before continuing, checkout my last 3 EHC publications here:

- Health Encompasses Quality, Defensibility After Q2 FY22

- No Change To Buy Rating After Guidance Delta

- Incremental Returns On Capital Key, Confirm Buy

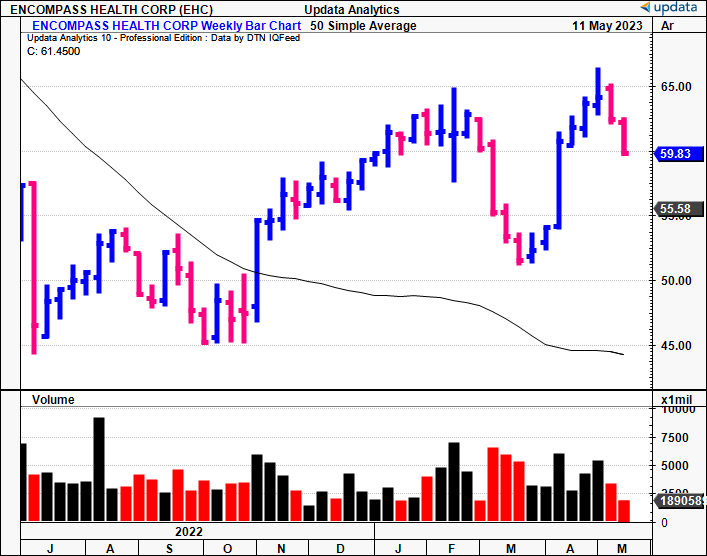

Fig. 1

- The 6-month rally in EHC's stock price has rolled over somewhat, but a rough finish to FY'22 was offset by the CMS' proposal to increase inpatient facility reimbursement rates in FY'24 by ~370bps, or $335mm.

- That was in April. The market swiftly discounted these positive expectations within 3-4 weeks into the EHC share price [Figure 1] and you are now back near 52-week highs after a decent run up the page, plenty of demand in the snap-back.

{kind=link}

Q1 continues long-term business trends

EHC opened up the year well with growth percentages and continues investing in de novo facilities to drive value. Good news is, management noted that peak occupancy rates continue to rise over time. This is a function of room skew (more private) which gives optionality, and from heavy investment into existing facilities to get more private rooms online. There doesn't appear to be a lag in new beds under occupancy and getting the beds online, either. Hence, there's good profitability early on in each new facility.

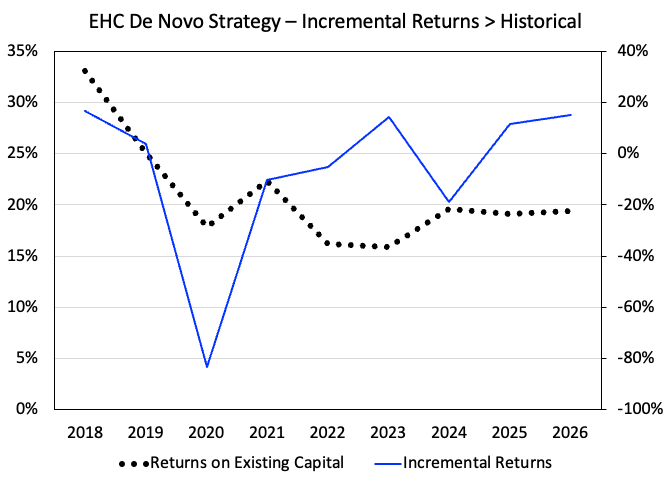

Most importantly, management's long-term growth strategy has begun to pay dividends in my opinion. Since FY'21, management embarked on a new capital budgeting strategy of adding de novos to the portfolio in order to grow earnings and free cash flow. The benefits of this move are observed in Figure 2. Here, the incremental returns, taken as the growth in annual post-tax earnings derived from EHC's incremental investments (productive assets) are plotted against the company's returns on existing capita each year. The growth in new capital has grown sharply in recent years. My numbers have incremental returns to reach c.20%. by FY'26. That will require a mammoth effort, but there's scope to get there.

Fig. 2

Note: Trailing returns taken as total capital invested (productive assets, not finance capital provided to the business), incremental returns taken as the change in NOPAT / change in total invested capital year-over-year. (Data: Author, EHC 10-k's)

{kind=link}

Looking to the quarterly numbers, there is plenty to discuss. Key takeouts in my notebook include the following:

- Top-line growth of 9.5% brought turnover to $1.16Bn on adj. EBITDA of~$230mm, a 17.5% gain. This, on same-store and total discharges of 5.9% and 9,4%m respectively. It brought this down to earnings of $0.88/share, flat on last year.

- Management noted the revenue upsides were largely volume related more than pricing. I'm looking to this point along with the 1.8x adj. operating leverage because it informs me of EHC's cost structure. That positive leverage at the operating line suggests fixed costs make up the bulk of business expense, meaning operating income can grow without the constraints of OpEx tying it down.

- On the expense side, there's chance EHC could benefit from tailwinds in labor pricing and expenditures going forward. For example Q1 contract labor tightened 50% YoY along with a 23% YoY decline in sign-on bonuses. These numbers have been trending lower over last 12 months.

- Patient volumes are up as well, per management, and this tells me another strong data point on contract labor cost. Number one, the Q1 FY'23 full-time equivalent ("FTE") was $183,000 vs. $240,000 in Q1 last year, and $211,000 in Q4. This is due to 230 fewer contract labor FTEs versus 2022. The good point is this pulled back against a 395 YoY increase in average daily census.

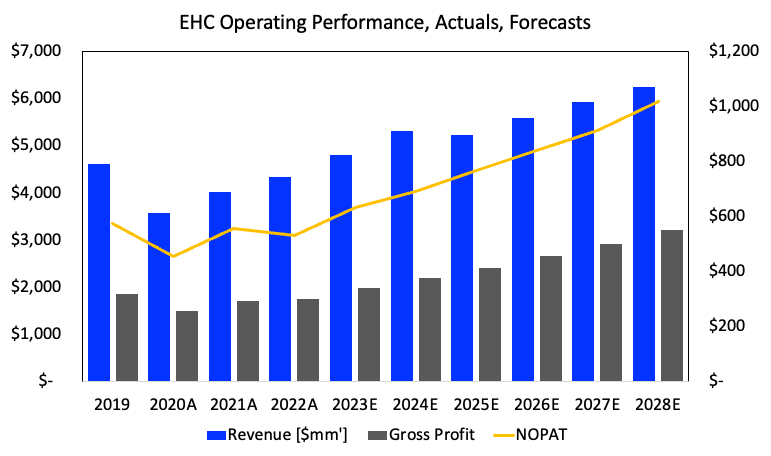

Hence, the firm's management over contract labor is clear and you'll find this is a pressing issue for many competing names right now. The pandemic plagued healthcare labor markets which has transposed onto corporate margins with no major offset. Hence, the trends in FTE contract labor and census figures are a good sign of internal controls from EHC in my opinion. With respect to financial performance, you can see the nice ramp on revenue and earnings exhibited across 2019-2022. I've rolled the company's Q1 actuals into my estimates, and look to a strong growth curve in gross and post-tax profit over the coming 5-years.

Fig. 3

{kind=link}

EHC's investment pattern of pouring capital into de novo facilities forms a constructive investment case in my view. There are layered benefits to getting new stores online for EHC. Each post-acute facility acts as a hub-and-spoke model to generate multiple recurring revenue streams. EHC is a platform company in this regard. Patients need post-acute care, clinicians need to treat them, EHC provides the primary means to do so. So you get multiple sources of income to this populous. For example, the firm has rolled out its on-site Tableau dialysis rollout to 64 of its hospitals. Expect further roll-outs this year as well.

Further, it has 18 de novos currently under development, one of which will mark the company's entrance into Connecticut. Four de novos has been brought online this year and this could provide revenue tailwinds going forward. EHC could do $4.8Bn in top-line revenues this year and pull this down to $750mm in operating income, calling for $400-$450mm in earnings for the year. The fact that 35-40% of its portfolio is joint-venture based is good too, as the upside is still with EHC at ~60% full ownership whilst spreading some of the risk with third parties. On the 4 de novos opened this year, the company had ~$4mm startup cost per site in the quarter, and projects ~$10-$12mm in FY'23.

The two paragraphs raised above are tremendously important to the investment debate. Intelligent investors know the market is a good judge of intrinsic value over time. Firms that generate >$1 in return on each $1 in profits they keep and reinvest are handsomely rewarded by the market in general.

In that vein, profits generated on retained capital are instrumental in creating future market value. As an investor, you'd expect your business to recycle profits back into the company only if it can yield a return above what investors can receive elsewhere. With long-term market returns in the 10-12% range, I'd expect at least 13% returns on retained/invested capital from any prospective company to demonstrate it is an efficient use of capital. If it can't even beat the market return on its own ventures, it is unlikely investors will push its market valuation higher in my opinion.

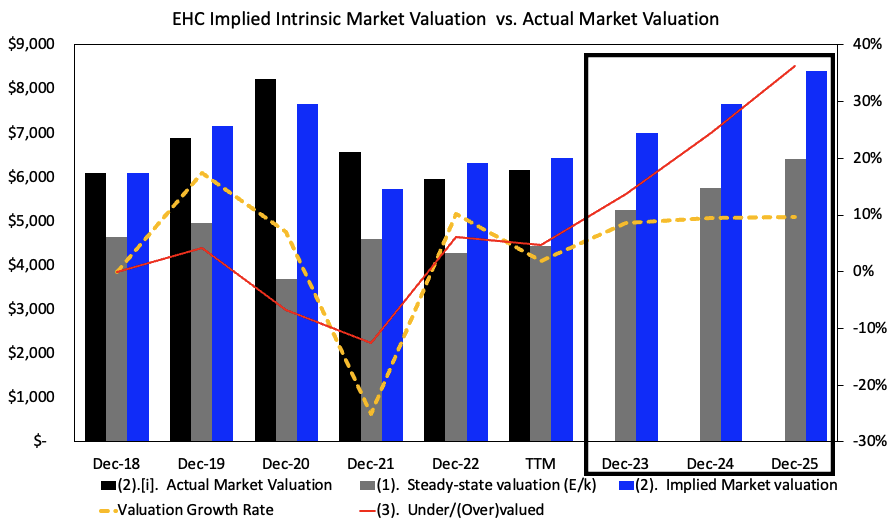

You can observe the relationship in EHC's profitability, implied valuation, actual market valuation and the growth rate in intrinsic value from 2018-the TTM in Figure 4. The company's steady-state value (forward earnings discounted at the hurdle rate of 12%) is shown in grey as well, along with the rating of under/overvalued. You can see several patterns in the data here:

- The Implied and actual market valuations track each other closely within a tight range over time.

- The steady-state valuation follows the same directional bias, although not at the same magnitude.

- In my opinion, the difference in steady-state value and the actual market price is the market's value on EHC's future prospects, discounted to that level.

Driving the implied market valuation is the intrinsic valuation growth rate, derived from the level of earnings reinvestment and return on invested capital (Growth = ROIC x Reinvestment Rate). EHC's numbers here show that it is turning its reinvested capital into additional market growth. For example, from December 2021 to the time of writing, the firm invested an additional $700mm in growth capital, with a corresponding $190mm positive change in market cap, or 27% return. Meanwhile, the trailing ROIC is 16% (ex-goodwill, 12% including). Looking to Figure 4, you'll see the FY'23-'25 forecasts:

- There's no actual market valuation bars shown, however, the under-overvalued line is compared to the current market cap.

- My numbers have EHC compound its intrinsic value by ~10% over this time should all go well.

- These assumptions could have EHC valued at the $7.5-$8Bn mark by FY'25, assuming the market will continue rewarding positive returns on the company's incremental capital.

Fig. 4

{kind=link}

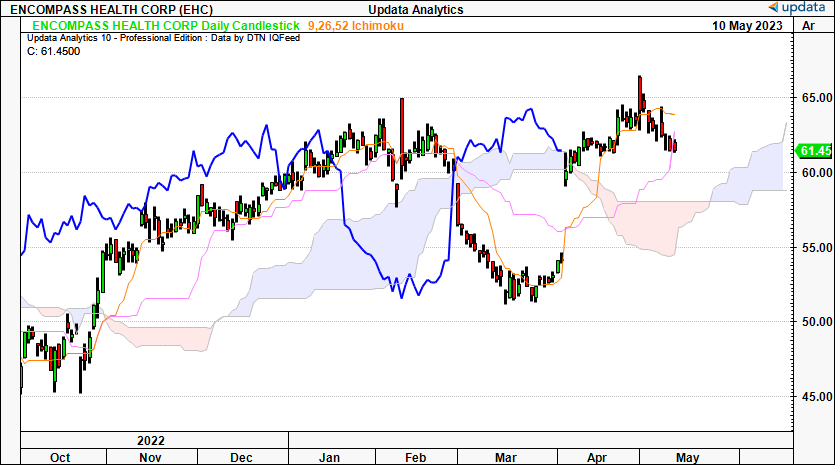

The technical picture

Not a great deal to add here other than EHC is trading above the daily cloud with the lagging line currently testing the cloud top. A push from the top here could ignite another rally in my opinion. We could be moving to $65 by end of May on this chart in my opinion. A break below the cloud would nullify this, but for the time being, there's plenty of room for volatility.

Fig. 5

{kind=link}

Further, there are upside targets to $76 on the daily point and figure studies shown below. This has me tremendously constructive especially given the vindication these targets have provided to date. A move to $76 would represent a sizeable move and should not be ignored. I'd say this target would be activated with a push above the $65-$67 mark.

Fig. 6

Data: Updata

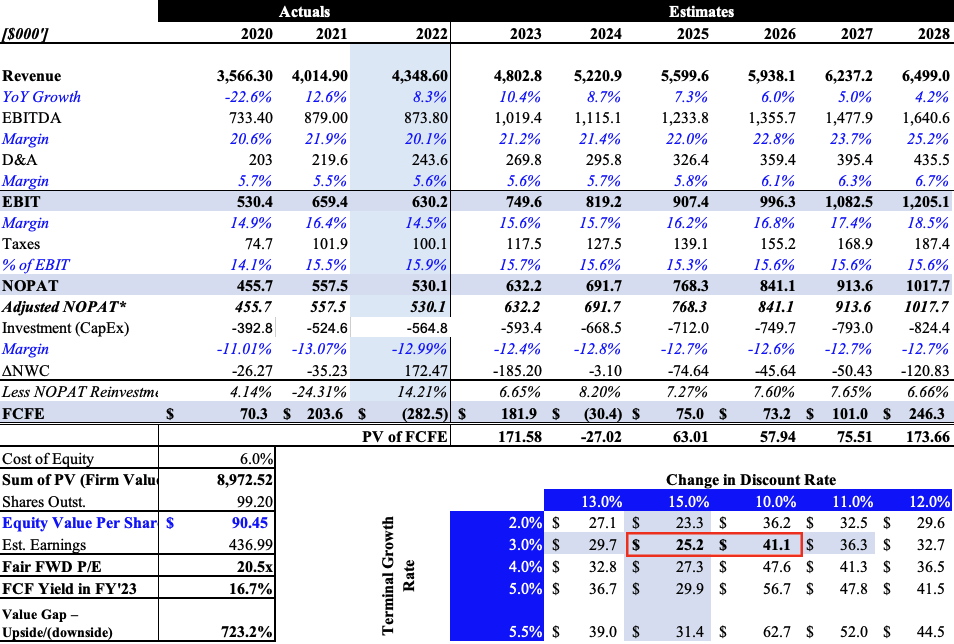

Valuation and conclusion

The quant system says 19x forward earnings is acceptable for EHC but rates it down on other multiples. At 4x book value, the company's 17% trailing ROE is far less appealing, as well. As my numbers shown above estimate, EHC could grow its intrinsic value by ~11-12% over the next 3 years. The market has been a fairly good estimator of EHC's fair value in my opinion, and I believe the company can throw off ~$180mm in cash to shareholders this year. Looking out to 2028, and discounting at the hurdle rate, I've got EHC at $90 per share, which tightens to $75 at a higher discount rate. Hence, the $7.8-$8Bn market cap range is a reasonable estimate in my opinion.

Looking to the data:

- My estimates have EHC valued at 20x forward P/E

- This represents 17% FCF yield this year

- A $75-$90 valuation range could be appropriate over a long-term horizon. This supports a buy thesis.

Fig. 7

{kind=link}

Net-net, I continue to rate EHC a buy on long-term value. The company has attractive business economics that are translating over into market valuation which enables the investor to establish value creation over time. Looking to $75-$90 as fair range and this is supported by the growth assumptions outlined in this report. Net-net, reiterate buy.

For further details see:

Encompass Health: Rotating Capital Investments Into Market Valuation