CAPMF - Endava Management Is Cautious About Growth And Headcount

2023-06-01 14:21:15 ET

Summary

- Endava plc reported its FQ3 2023 financial results on May 23, 2023.

- The firm provides a range of technology consulting to companies worldwide.

- Endava stock has been hard hit in the past year and management has guided forward growth cautiously while being focused on limited headcount growth.

- I'm on Hold for Endava stock in the near term due to increasingly uncertain economic conditions ahead.

A Quick Take On Endava

Endava plc ( DAVA ) reported its FQ3 2023 financial results on May 23, 2023, beating revenue and earnings per share consensus estimates.

The company provides technology consulting and implementation services to companies worldwide.

Endava’s stock has been hard hit in the past twelve months, so it needs a considerable catalyst to reverse the downward trend in valuation.

Given management’s cautious outlook and the uncertain macroeconomic environment, I’m going to remain on the sidelines for Endava plc stock in the near term.

Endava Overview

The London, England-based software development outsourcing company was founded in 2000 to support enterprise teams throughout the lifecycle of their projects, from application delivery and testing to support, hosting and managed services.

Management is headed by Co-Founder and CEO John Cotterell, who was previously a Managing Director at Concise Group Limited.

Endava helps companies use Distributed Agile at scale, a method in which software projects are developed in rapid cycles by teams working remotely. This results in small releases with each building on the previous one.

The company’s offerings include the following services:

-

Strategy

-

Creative and User Experience

-

Insights through Data

-

Mobile and Internet of Things

-

Architecture

-

Smart Automation

-

Software Engineering

-

Test Automation and Engineering

-

Continuous Delivery

-

Cloud

-

Advanced Applications Management

-

Smart Desk

Endava’s Market & Competition

According to a 2021 market research report by 360 Market Updates, the global market for digital transformation strategy consulting was an estimated $58.2 billion in 2019 and is forecast to reach $143 billion by 2025.

This represents a forecast CAGR of 16.2% from 2020 to 2025.

The main drivers for this expected growth are a large transition from on-premises, legacy systems to cloud-based environments with complex architectures.

Also, the COVID-19 pandemic has likely pulled forward significant demand to modernize enterprise systems resulting in increased growth prospects for digital transformation consultancies.

Major competitive or other industry participants include:

-

Globant

-

EPAM

-

Slalom

-

Accenture

-

Deloitte Digital

-

McKinsey

-

BCG

-

Ideo

-

Cognizant Technology Solutions

-

Capgemini

-

Company in-house development efforts

Endava’s Recent Financial Trends

-

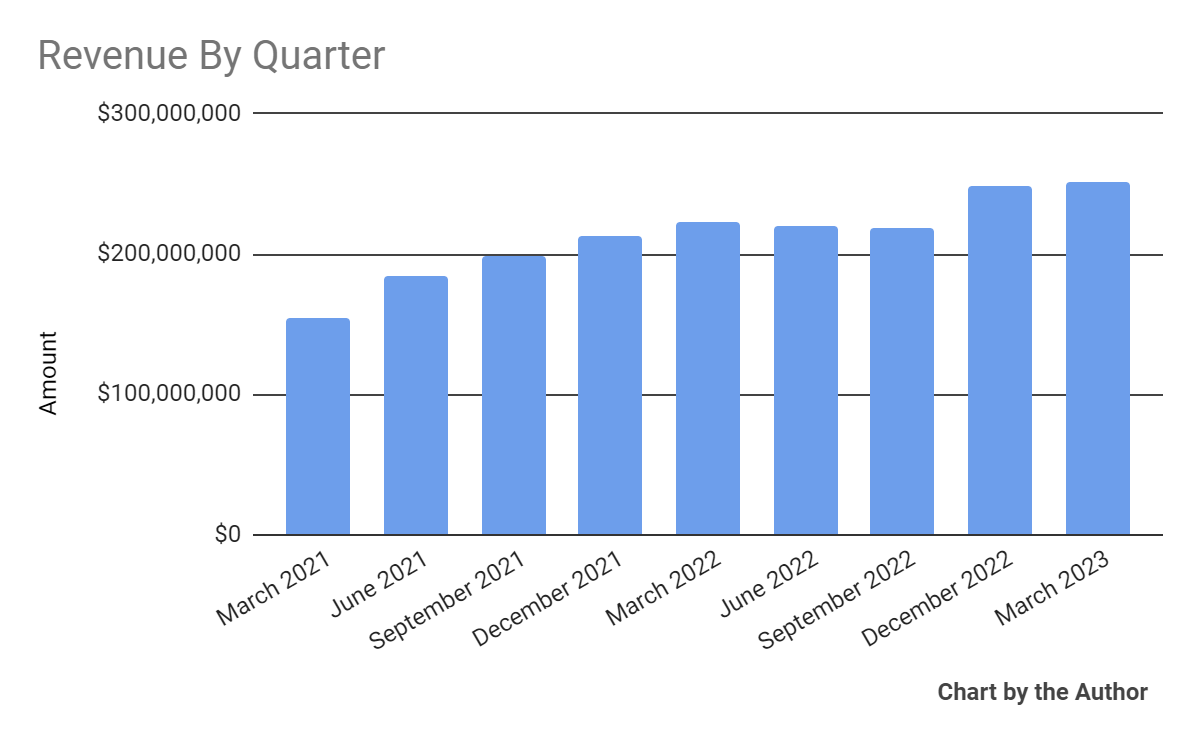

Total revenue by quarter has grown per the following chart:

{kind=link}

-

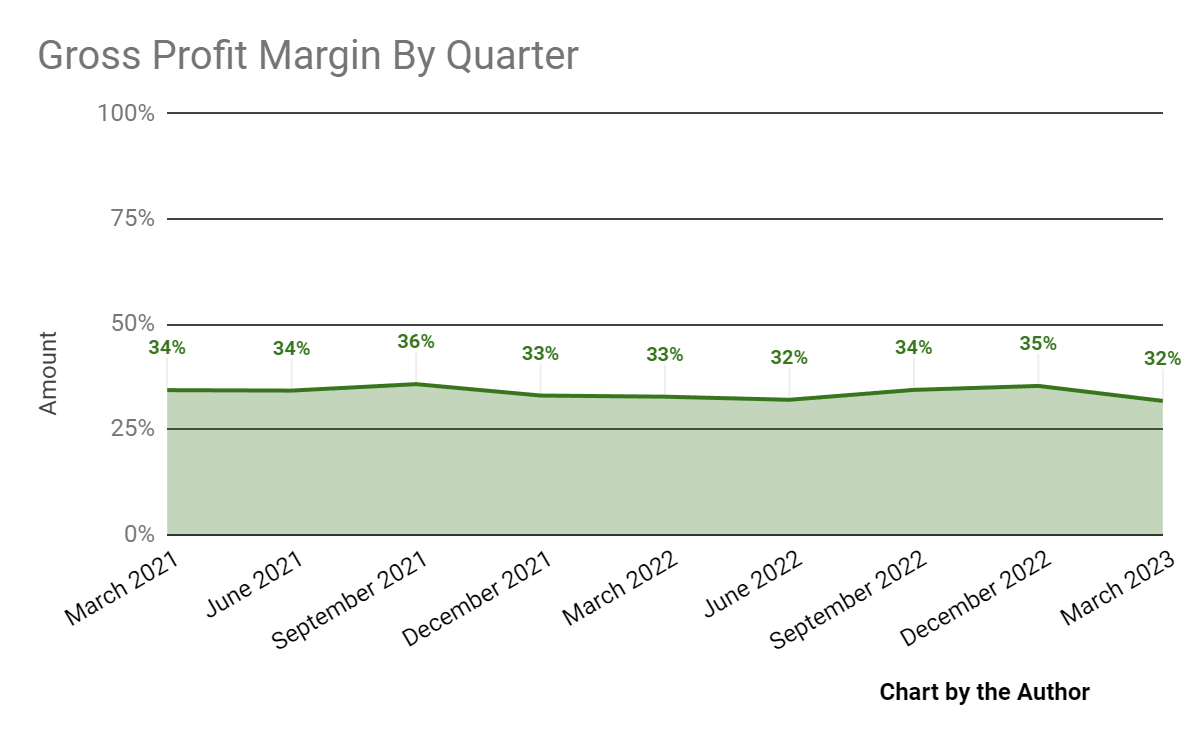

Gross profit margin by quarter fell in the most recent quarter:

{kind=link}

-

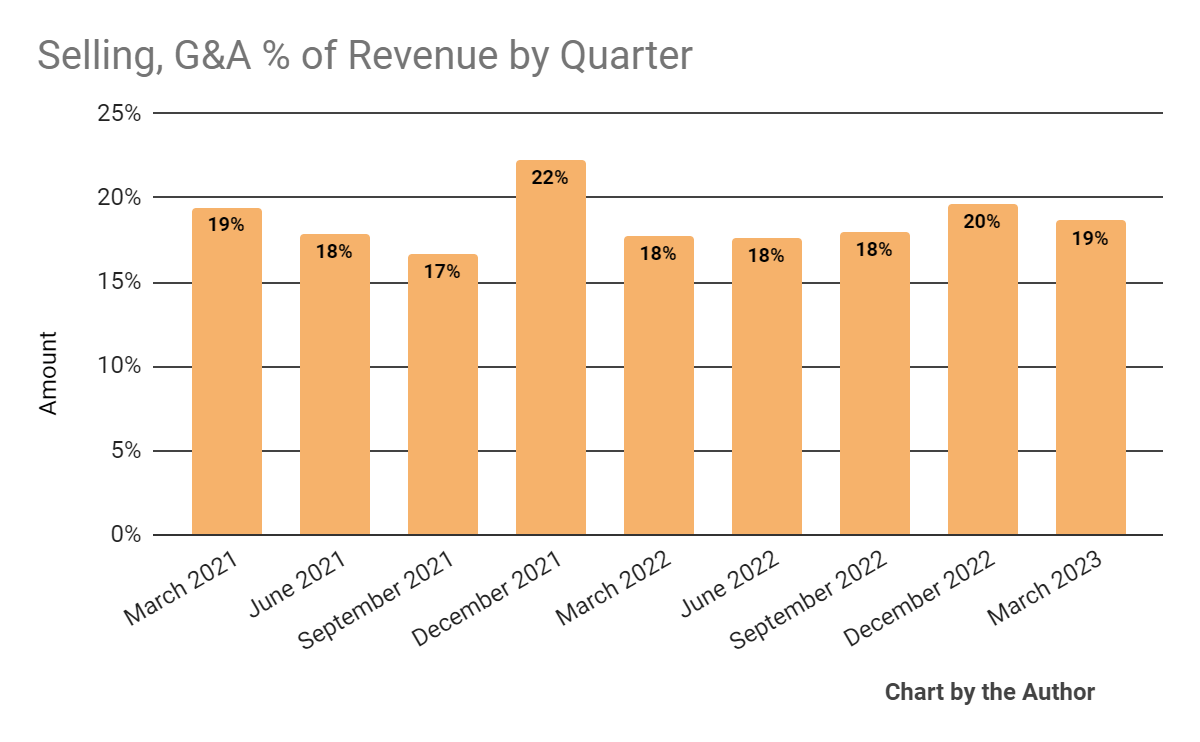

Selling, G&A expenses as a percentage of total revenue by quarter have varied within a narrow range:

{kind=link}

-

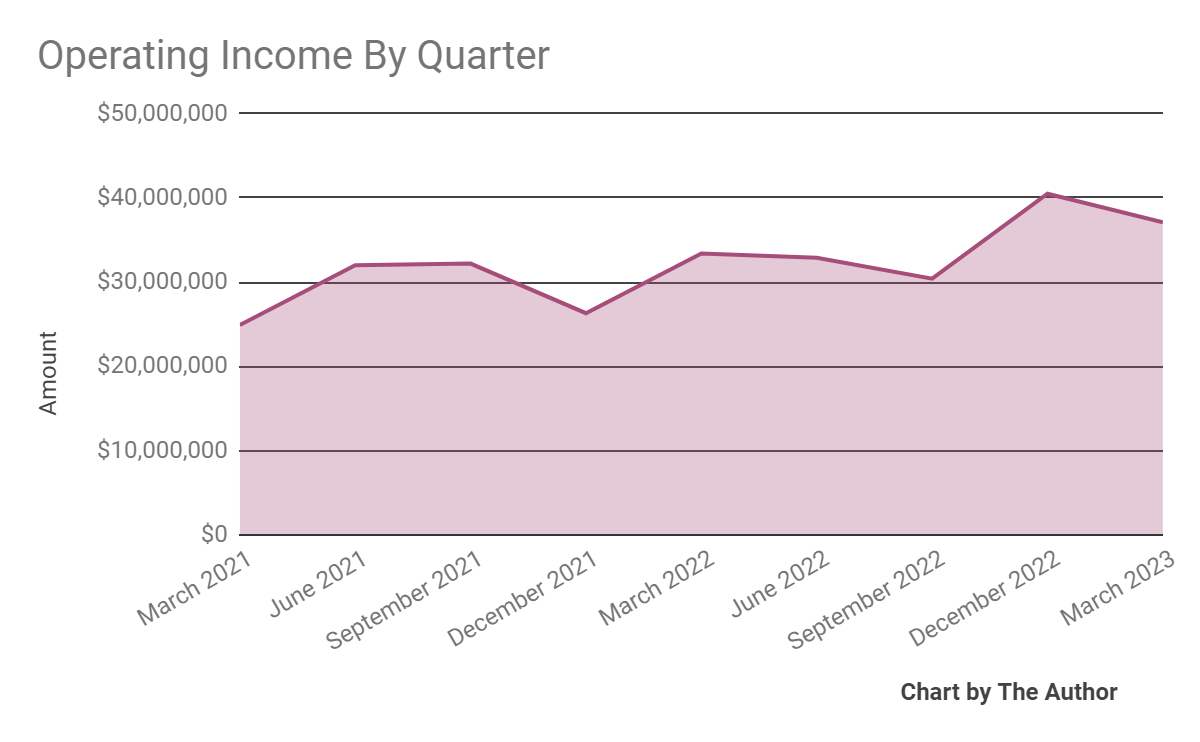

Operating income by quarter has trended higher more recently:

{kind=link}

-

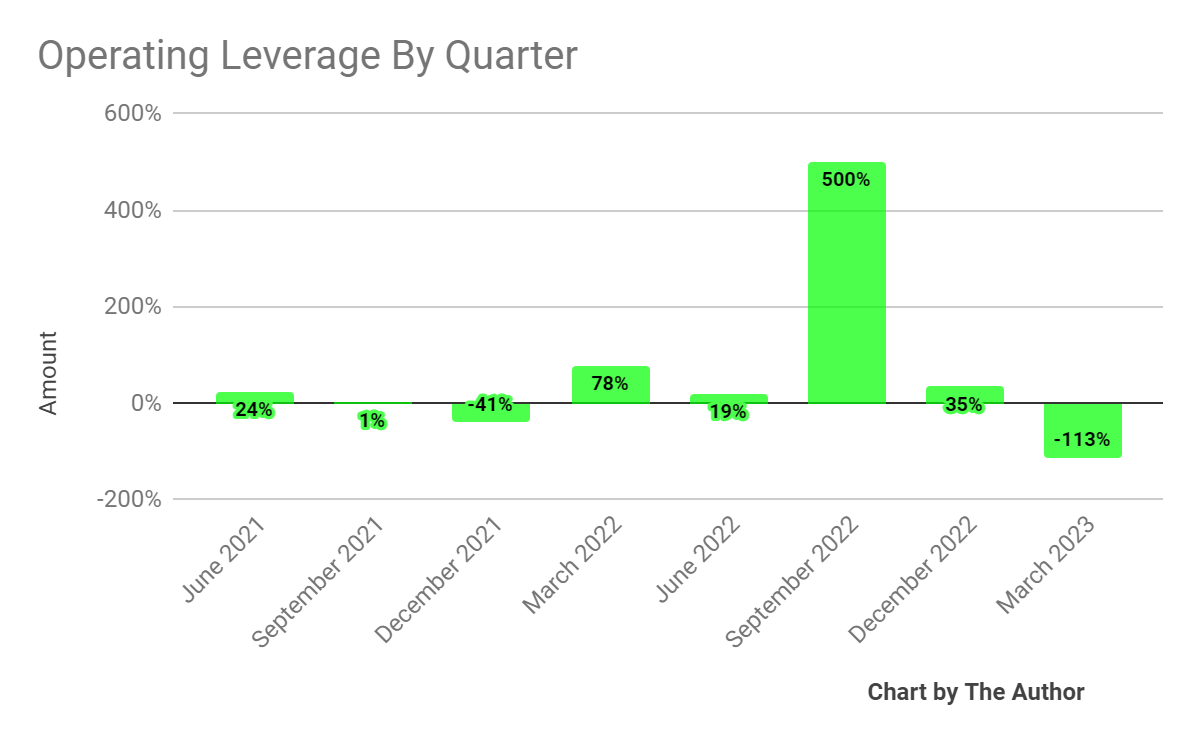

Operating leverage turned negative in the most recent reporting period:

{kind=link}

-

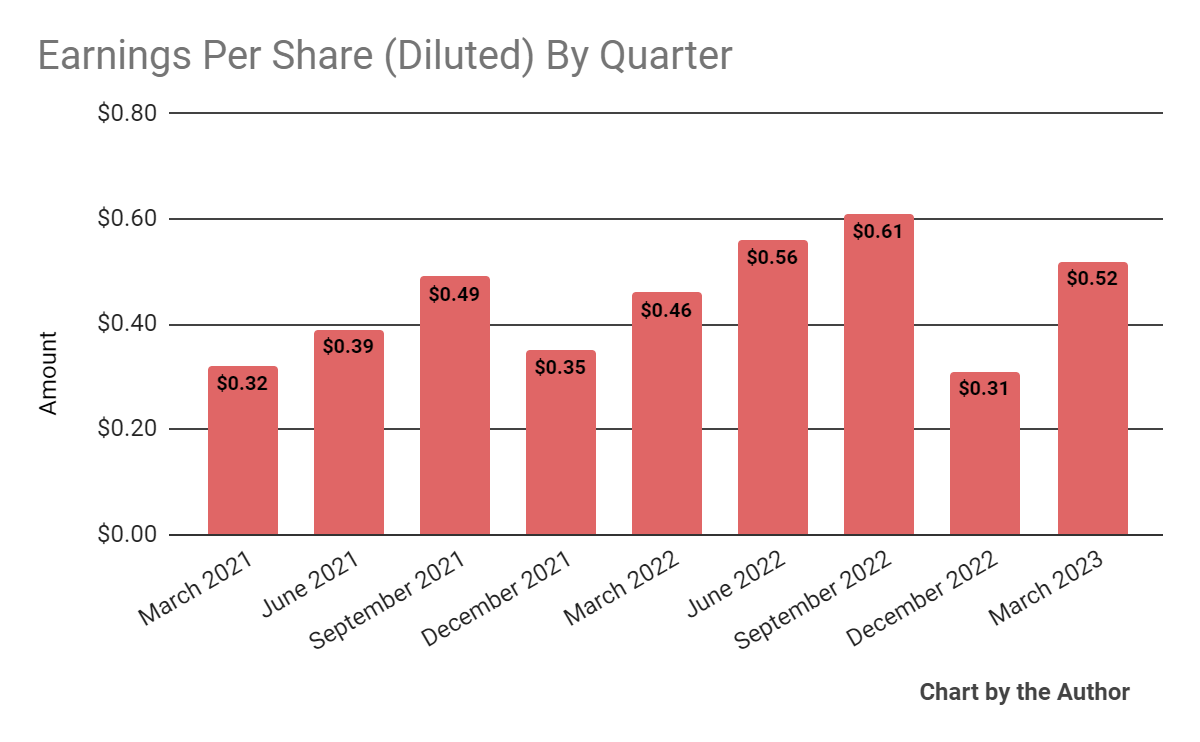

Earnings per share (Diluted) have varied as the chart below indicates:

{kind=link}

(All data in the above charts is GAAP.)

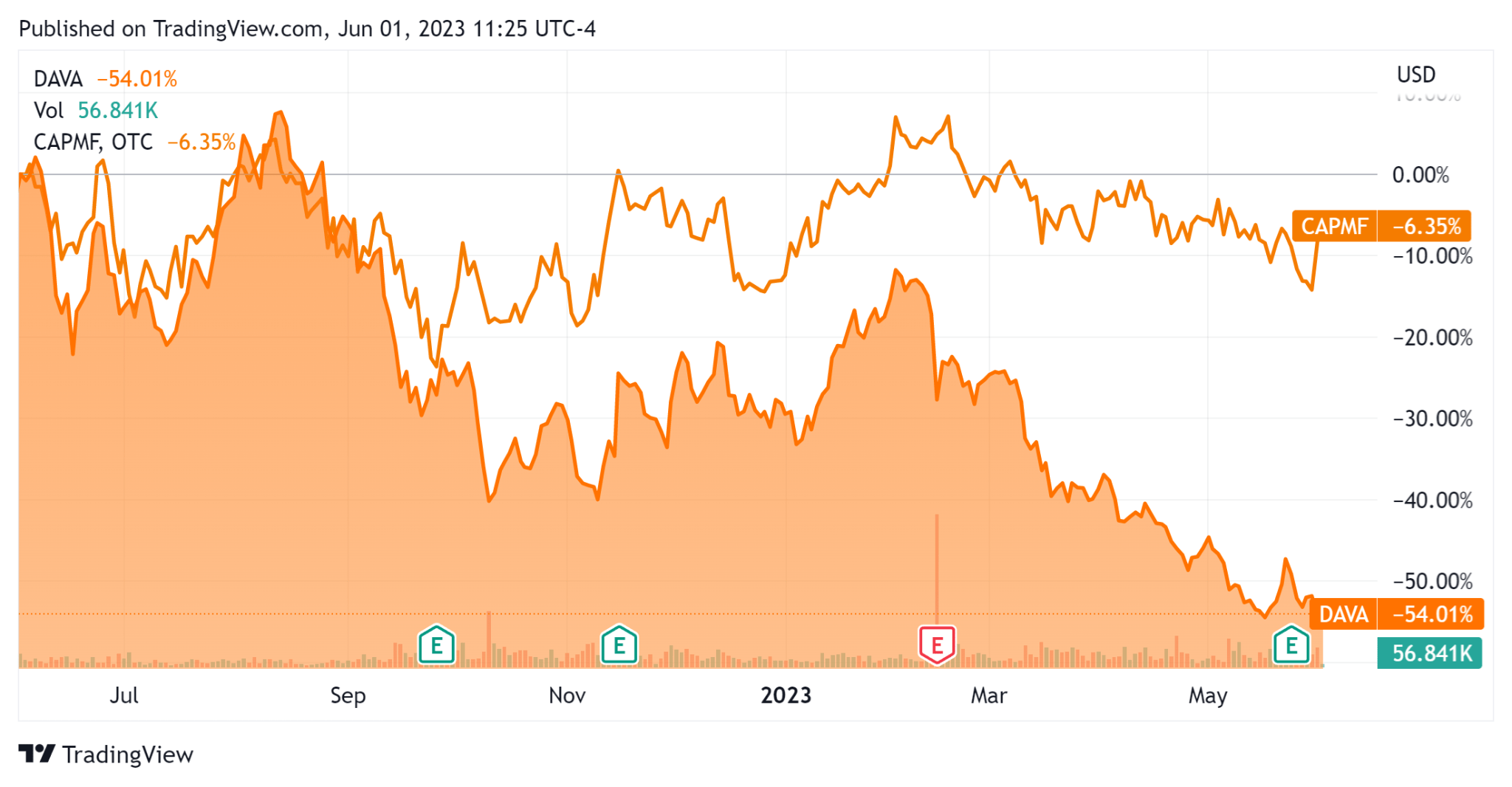

In the past 12 months, DAVA’s stock price has fallen 54.01% vs. that of Capgemini SE's (CAPMF) fall of 6.35%, as the chart indicates below:

{kind=link}

For the balance sheet , the firm ended the quarter with $245.7 million in cash and equivalents and no debt.

Over the trailing twelve months, free cash flow was $151.4 million, of which capital expenditures accounted for $19.2 million. The company paid $43.2 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Endava

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 2.8 |

| Enterprise Value / EBITDA |

| 16.2 |

| Price / Sales |

| 3.0 |

| Revenue Growth Rate |

| 29.2% |

| Net Income Margin |

| 12.5% |

| EBITDA % |

| 17.5% |

| Net Debt To Annual EBITDA |

| -1.4 |

| Market Capitalization |

| $2,920,000,000 |

| Enterprise Value |

| $2,750,000,000 |

| Operating Cash Flow |

| $170,620,000 |

| Earnings Per Share (Fully Diluted) |

| $2.00 |

(Source - Seeking Alpha.)

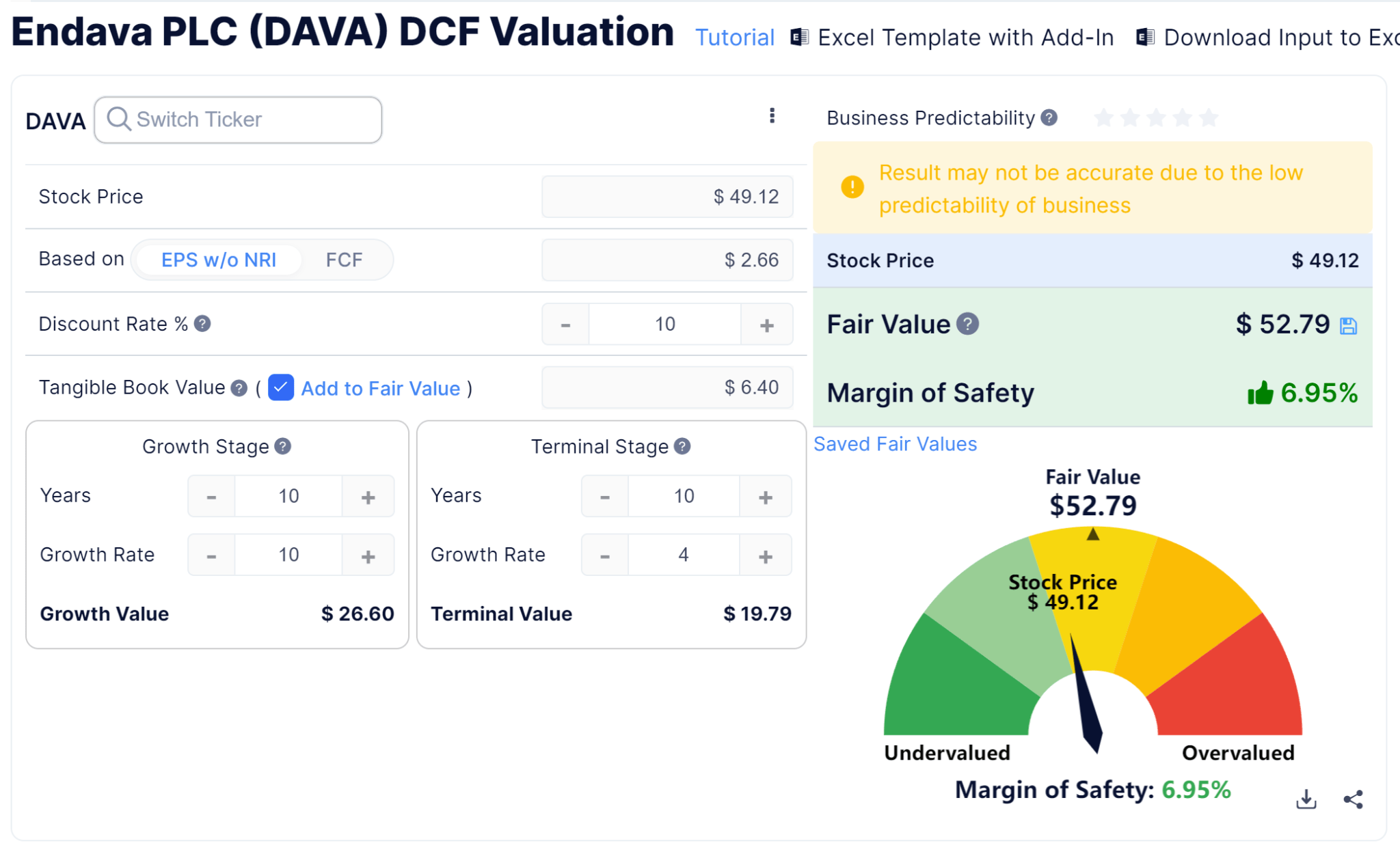

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and earnings:

{kind=link}

Assuming generous DCF parameters, the firm’s shares would be valued at approximately $52.79 versus the current price of $49.12, indicating they are potentially currently slightly undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

As a reference, a relevant partial public comparable would be Capgemini SE; shown below is a comparison of their primary valuation metrics:

| Metric [TTM] |

| Capgemini |

| Endava |

| Variance |

| Enterprise Value / Sales |

| 1.4 |

| 2.8 |

| 97.2% |

| Enterprise Value / EBITDA |

| 10.7 |

| 16.2 |

| 51.5% |

| Revenue Growth Rate |

| 21.1% |

| 29.2% |

| 38.1% |

| Net Income Margin |

| 7.0% |

| 12.5% |

| 77.8% |

| Operating Cash Flow |

| $2,700,000,000 |

| $170,620,000 |

| -93.7% |

(Source - Seeking Alpha.)

Commentary On Endava

In its last earnings call ( Source - Seeking Alpha ), covering FQ3 2023’s results, management highlighted the uneven market demand for its services during the quarter as a result of the recent bank failures.

As a result, clients have been reluctant to commit to new projects or have delayed activities for existing projects as they exert greater scrutiny on their IT investments.

Notably, management is prioritizing its focus on engagements with larger clients, seeking "relationships that can grow and scale."

Leadership also highlighted the growth in its data and AI-related work in "scale, value and complexity" more recently.

Management didn’t disclose any company or employee retention rate metrics but did say that it is increasing its "selectivity regarding our recruitment efforts and are focusing on areas of strong demand plus sales and marketing."

Total revenue for the first three months of 2023 rose 13% YoY and gross profit margin dropped one percentage point.

Selling, G&A expenses as a percentage of revenue grew by 0.9 percentage points while operating income increased by 11.1% YoY.

Looking ahead, management guided full-year 2023 revenue growth of 16.25% in constant currency terms at the midpoint of the range.

Adjusted EPS is expected to be GBP 2.155 at the midpoint.

The company's financial position is strong, with ample cash, no debt and strongly positive free cash flow.

Regarding valuation, my discounted cash flow calculation suggests that the stock may be slightly undervalued on a long-term basis.

The primary risk to the company’s outlook is slowing business conditions in important industry verticals the firm focuses on, such as technology and financial services.

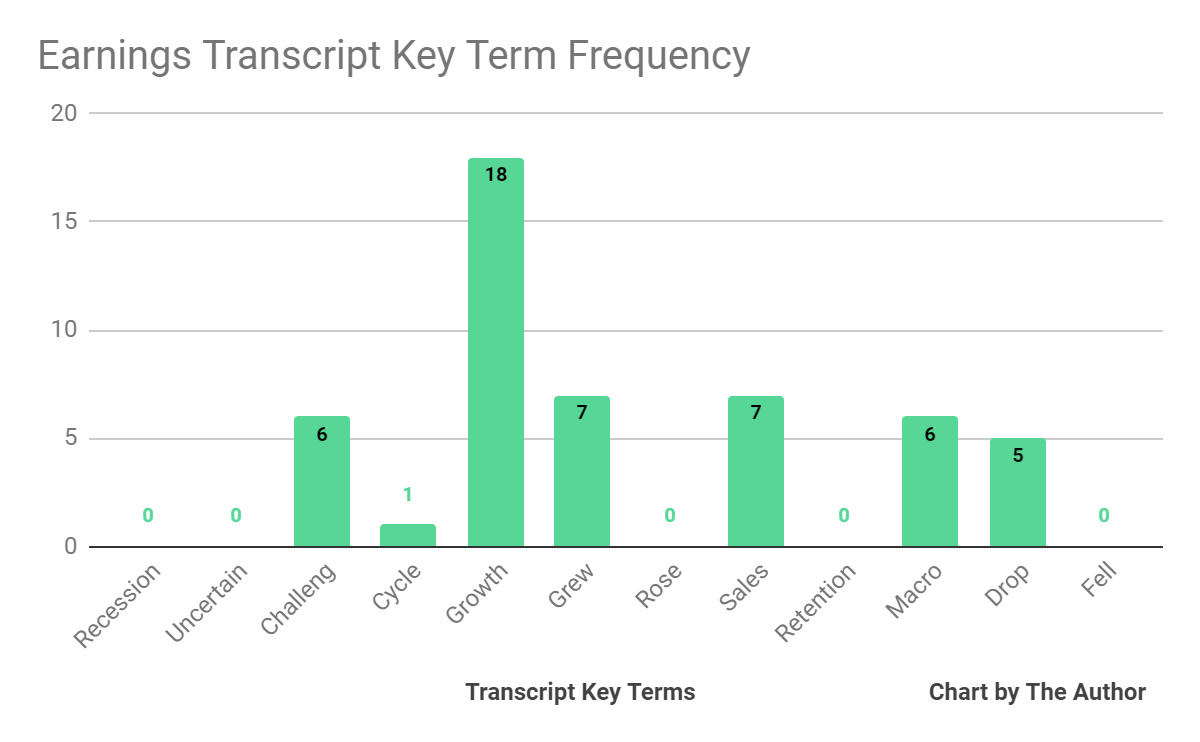

From management’s most recent earnings call, I prepared a chart showing the frequency of key terms mentioned (or not) in the call, as shown below:

{kind=link}

I’m most interested in the frequency of potentially negative terms, so management or analyst questions cited "Challeng[es][ing]' six times, "Macro" six times and "Drop" five times.

The negative terms refer to the difficulties in the macroeconomic environment and the negative outlook from a number of the firm’s customers, resulting in longer decision timeframes.

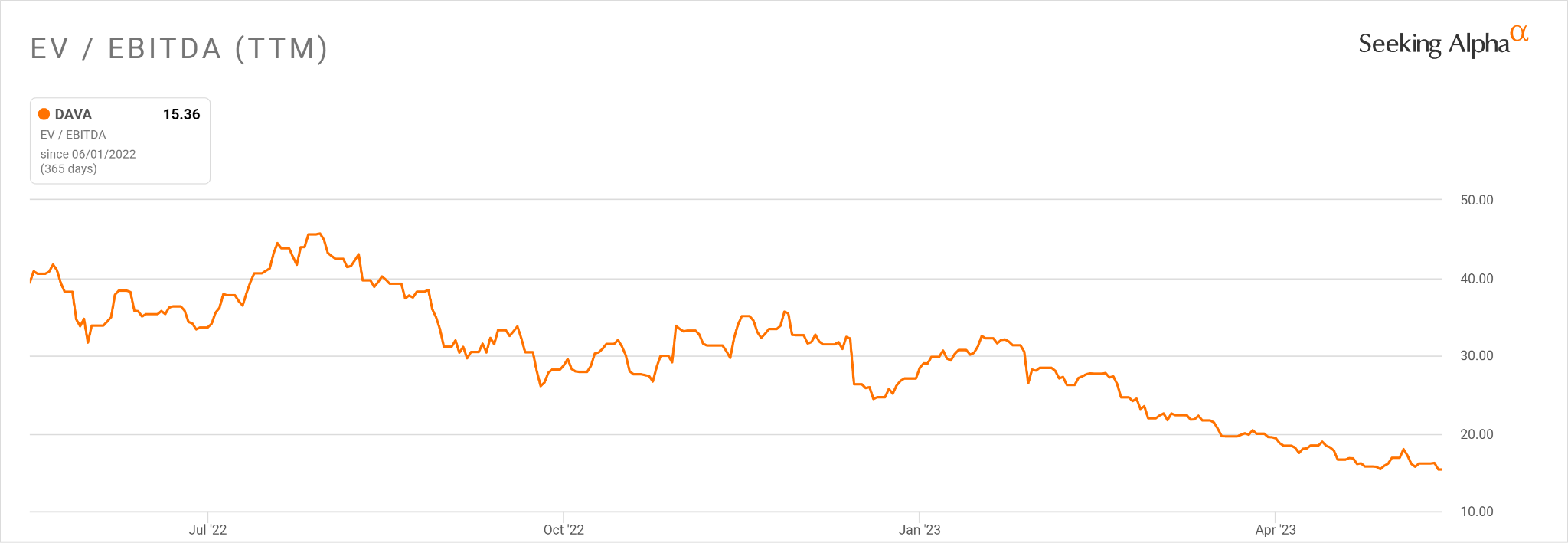

In the past twelve months, the firm's EV/EBITDA valuation multiple has dropped by a whopping 61%, as the chart from Seeking Alpha shows below:

{kind=link}

Endava’s stock has been hard hit in the past twelve months, so it needs a considerable catalyst to reverse the downward trend in valuation.

Given management’s cautious outlook and the uncertain macroeconomic environment, I’m going to remain on the sidelines for DAVA in the near term.

For further details see:

Endava Management Is Cautious About Growth And Headcount