ELEZF - Endesa: Higher Finance Costs Biting Down Hard And Spanish Tax Tendencies

2023-11-09 13:29:37 ET

Summary

- Endesa, S.A. has seen decent operating results despite declining electricity prices and lower demand, but higher financing costs and windfall taxation are impacting the bottom line.

- Capacity for non-CO2 emitting generation has increased slightly, but lower demand and lower electricity prices have been a bit of a headwind too, offset by lower gas prices.

- The high financing costs and taxes, along with uncertainties surrounding nuclear assets, make Endesa an unattractive investment option.

- There are also questions around gas reserves and the risks of a colder winter this year than last that may come to affect margins.

Endesa, S.A. ( ELEZF ) has seen decent operating results with the fact that while electricity prices have declines, so have input prices for a decent proportion of its assets. Demand has been lower, so the lower volumes have hit slightly. The issue is when you move below the operating line. One thing is the higher financing costs - indeed a problem and likely a somewhat enduring one. But the other issue is what is going on with windfall taxation.

More than the majority of other European countries, so not even by American standards, Spain has always had socialist tendencies with respect to its public utilities. Regulated utilities in the region are always been hindered by penny pinching by the CNMC, and in this case there's been a windfall tax on revenues in a year where electricity prices have anyway fallen. Endesa is absolutely affected, and the tax should affect next year's results too. The nuclear question continues to weigh on Endesa as well. While the 15x P/E might appeal to some, it is not nearly low enough for us to take on all this complexity. Clear pass.

Quick Results Breakdown

Capacity is up slightly by 6% for non-CO2 emitting generation, and overall investments are up 2% . It's not that much.

As one of the major energy producers in Spain, with a very significant proportion of the nuclear assets, this might be the company's way of protesting the windfall tax that has been levied from energy producers due to high electricity costs in 2022, unavoidable (the high electricity prices I mean) due to the speculation, hoarding and WC acceleration after the Ukraine war's outbreak.

{kind=link}

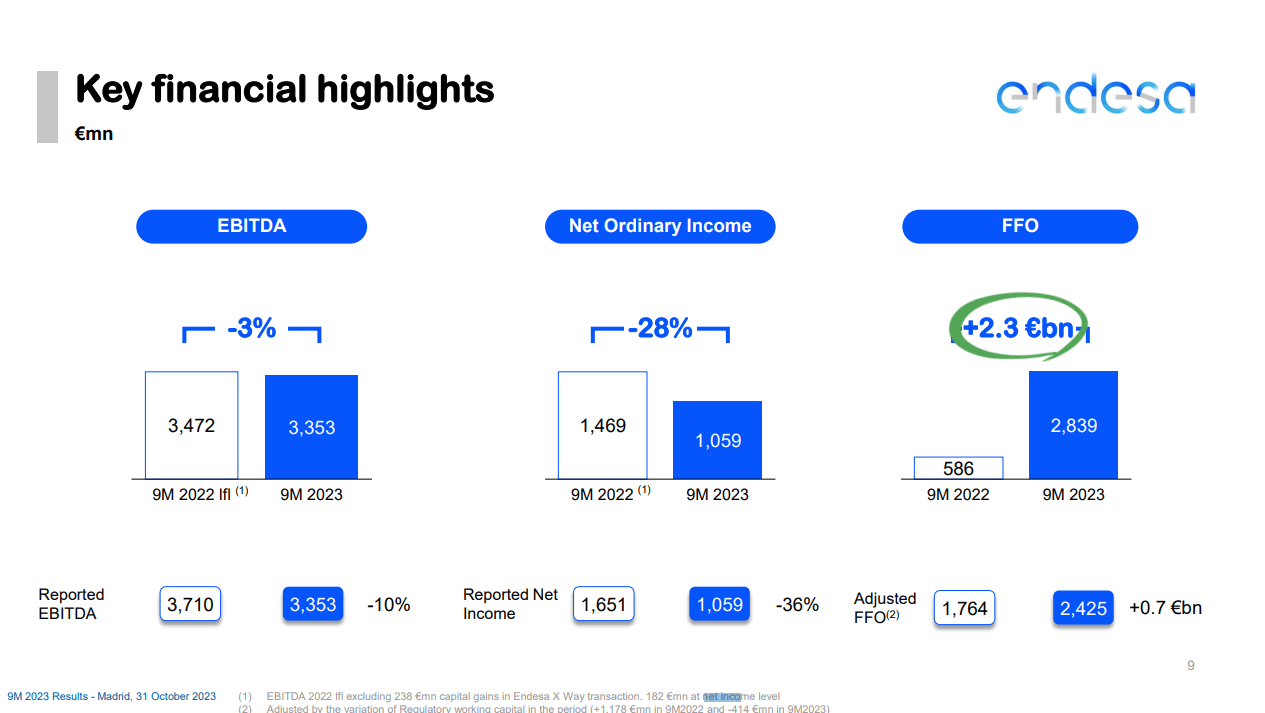

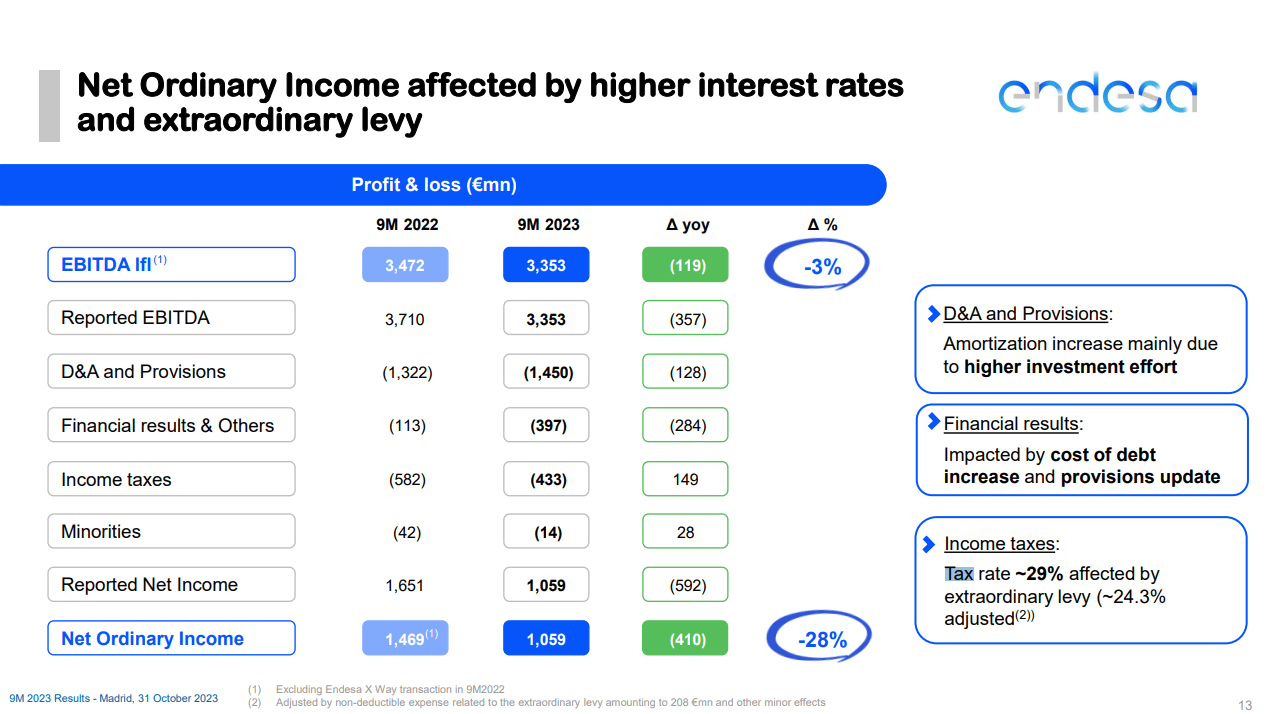

While lower electricity prices have come in, decreasing by about 50%, gas prices have come down even more. The lower demand for electricity with volumes falling 8% but higher margins actually preserves the EBITDA into a resilient 3% decline only.

Again, the extraordinary levy, meant for 2023-2024, has really hit the bottom line, punishing these companies for the high prices of last electricity year. It's perplexing, because last year EBITDA evolutions were flat . They weren't benefiting from the high prices whatsoever, as high gas prices damaged CCGT margins where CCGT is still around 15% of their capacity. Moreover, the windfall tax is on revenue, not on income, so it seems greedy by the government. In general, we have observed over many years of coverage of utilities in Europe that Spain has always been especially heavy-handed in its taxation and remuneration of regulated utilities, even more so than Italy. We have always made it a point to not invest in Spanish utility companies as these negative developments, whether it be lower CNMC remuneration rates, or other sudden taxes, are more common than not when a Spanish company with a substantial stake-holding of government performs well.

{kind=link}

Bottom Line

The other issue is the financing costs.

{kind=link}

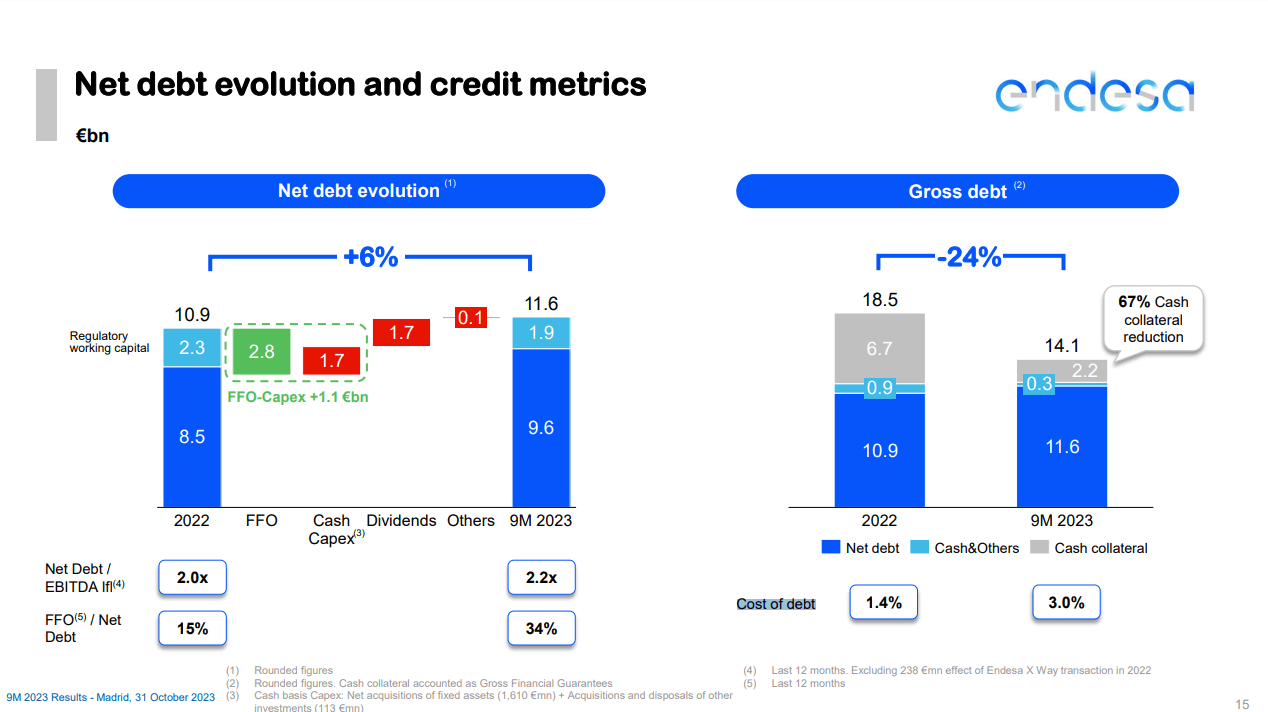

Net debt has come down substantially, but with the rate hike regime in Europe imitating, although to a less extreme extent, the rate hike regime in the US, costs of debt have doubled. We think that the EU rate situation is probably better than that of the U.S., because there are more signs of recession in the EU than the U.S. where there is still jobs growth and substantial wage growth.

Nonetheless, underlying inflationary factors like deglobalization remains a bit of a problem, and put quite a high floor on debt costs, so higher debt costs is going to be an enduring situation in the medium-to-long term, as well as being as high as they are now for the foreseeable future.

Endesa trades at around a 15x P/E on an annualized basis. That is quite high and in line with historical market averages, which have not be subject to a higher cost of capital environment. Moreover, upside in Spanish utilities to a certain extent has capped upside, evidenced by the indiscriminate windfall tax on a relatively green producer as well.

The only upside is that the taxes should come to an end in a year, but with enduring financing costs and general capital intensity from the renewable investment regime, as well as the outstanding questions around Endesa's large nuclear assets, including potential financial burdens if their licenses to operate are extended beyond intended retirement dates, all introduce liabilities that limit the value of the stock. Even adjusting the income for the end of the windfall tax, there are still so many safer opportunities that trade at better multiples, so Endesa, S.A. stock is a pass.

For further details see:

Endesa: Higher Finance Costs Biting Down Hard, And Spanish Tax Tendencies