ELEZF - Endesa: Watch Out For Gas Remember Nuclear Closures

2023-07-26 09:58:46 ET

Summary

- Comps from last year were weak due to a couple of factors, including really weak CCGT performance from high gas prices.

- High gas prices could come again at the end of this year, and that shouldn't be forgotten by market actors. At least Endesa is hedging more.

- Still, Endesa will see some margin normalisation coming this year, starting with the Q2, and we look ahead to the nuclear discussion.

- The EU is discussing plant extensions for nuclear but there is a lot of resistance, and Spain is seeing a lot of internal resistance too. It's not clear if increased lifespans are that good for Endesa in the end.

- Endesa stock isn't dirt cheap. You can get much cleaner stories elsewhere for similar multiples. Pass.

Endesa ( OTCPK:ELEZF ) just reported earnings . We expect that there will be the beginnings in some normalisation sequentially in the free power margin and in the gas margin which will continue this year. Thanks to hedging, the exposure isn't massive to another spike in gas prices towards the end of the year if the winter isn't as mild as last, but it is still a factor. In the longer term, we look at the nuclear assets. We once thought that extended lifespans would be a good thing for the company, and it might be if there aren't too many conditions, but it's not clear cut. Endesa themselves were fine with closures when they were decided in 2019. The complexity around the nuclear exposures is difficult to digest for markets, and in the dividends paid in the last two years any upside in the excessive nuclear discount might have already been depleted. A complex story with a multiple that can be matched by less complex ideas on international markets.

Thoughts on Earnings

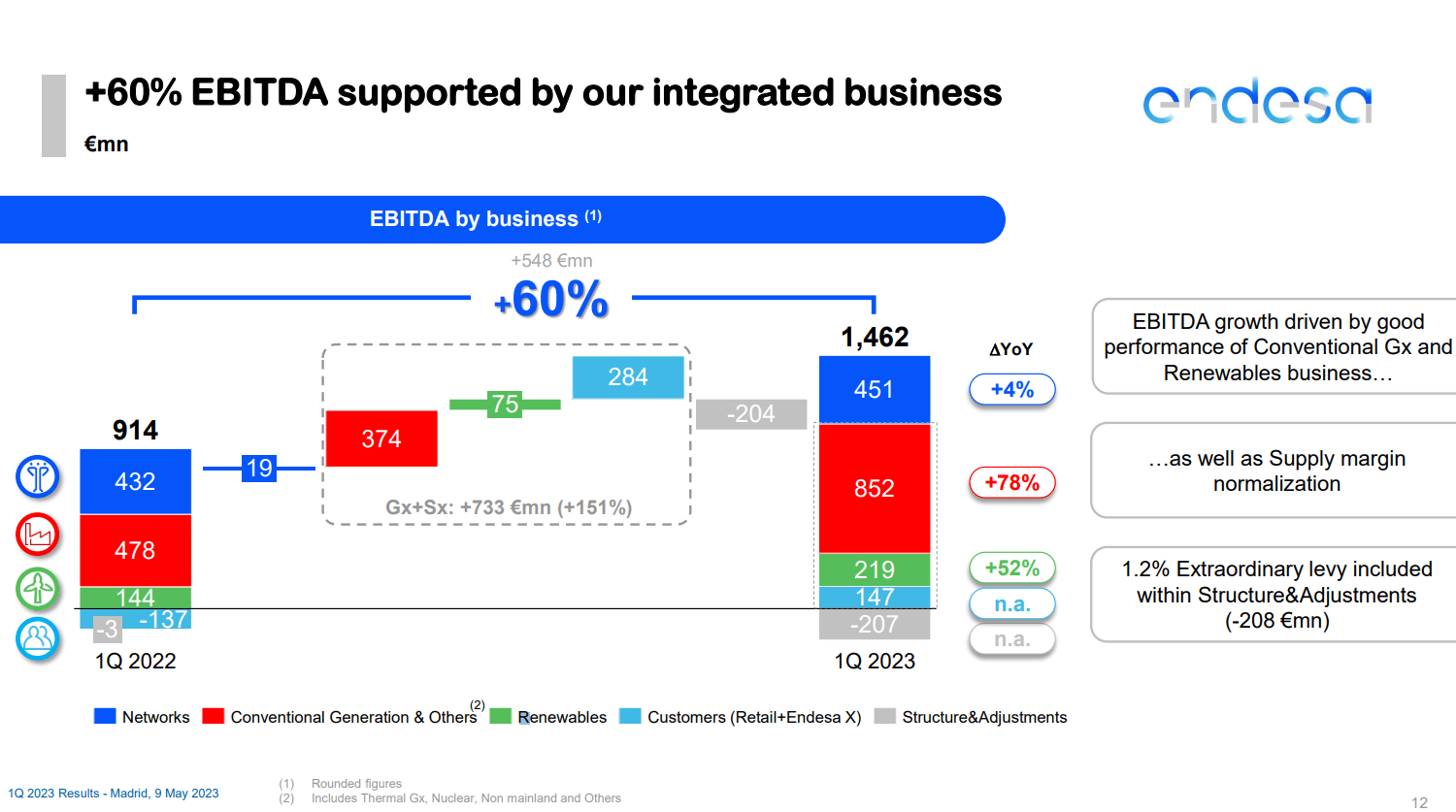

In the last report, EBITDA had climbed massively primarily on the recovery in major margin figures compared to terrible comps in 2022. This was partially thanks to the limited ability for Spanish utility companies to benefit from the high energy prices. EBITDA was up 60% . While the free power margin has some staying power, there is going to be a more intense normalisation in the gas margin. Endesa has hedged gas a fair bit in order to avoid a repeat performance of last year's results. Gas margins could fall around 50%, while free power margins are expected to fall around 20% only, although these are just vague indications by manage ment. Still, we expected that in the recent earnings, and indeed in the earnings reports to come, some margin normalisation could begin even on a sequential basis.

{kind=link}

EBITDA Evolution (Q1 2023 Pres)

Indeed, in the Q2 we saw the beginning of normalisation, with the free power margin down a little less than 10% sequentially, up 81% YoY thanks to weak comps. The gas margin collapsed back to 2022 levels sequentially, and is even below last year's margin now due to a fall in electricity prices.

{kind=link}

While renewables saw some pickup, their EBITDA contribution, especially relative to their power generation contribution which is about 2:3 with nuclear being larger, was not that high in Q1. This is the sink of the company's investments. It makes sense that traditional Gx is going to be a better EBITDA contributor since there are major costs not being accounted for in nuclear plant de-commissioning. The outsized contribution from Gx remains the case in the H1 results, except Q2 contribution from conventional Gx was more diminished as revenues fell in particular from coal but also CCGTs and nuclear which all saw decreased output. There are also hedging arrangements from last year that were still paying off in Q1 that are now seeing a decayed effect.

One is the thermal margin that we have got in this first quarter due to the exceptional conditions and due to the hedging that we did in the past year.

Jose Bogas, CEO of Endesa Q1 2023 Call

With the first closures coming in 2027, and more major closures in 2030, the assets are nearing the point where the EBITDA they'll produce till then may only cover the closure costs, where 5 years is the limit. The 2027 Almaraz I and II closures already are in the phase of just paying down decommissioning costs incoming. 2030 is when the nails are in the coffin for all of Endesa and all of Spain.

Bottom Line

The closures are going to be an issue. While there were some hopes pinned on extension of life, it's not certain Endesa would benefit from this that much since investment in these plants would fall on them. They agreed to the closures in 2019. There are mechanisms that may become instituted on the EU level that might help finance life extensions of nuclear, and France has a big interest in that, but it's not certain at all.

The management stresses normalization of the figures despite the company performing way ahead of their guidance. Thermal margins have already shown that they can't stay on the level of Q1 in the H1 report, and the massive increase in thermal EBITDA will not keep pace for the rest of the year as margin and output have fallen. There are cost considerations too as we approach the end of the year. Annualized profits are already coming down. The PE might be somewhere around 12-15x on forward figures which are anyone's guess. There are ideas on the market that are much less complex than this with less concern and overhang for a lower multiple. We don't want to get in the muck here.

For further details see:

Endesa: Watch Out For Gas, Remember Nuclear Closures