ENIC - Enel Chile: An Undervalued Company With A Solid Yield

2023-10-25 16:30:52 ET

Summary

- Enel Chile is a Chilean electricity utility company involved in the complete energy supply chain, including generation, transmission, and distribution.

- The company achieved notable growth in its Generation segment, driven by increased solar and hydroelectric production.

- However, the Distribution & Networks segment experienced a decline in operating revenues due to changes in the company's consolidation perimeter.

- Despite rising sharply over the past year, ENIC stock remains undervalued amid its <2x forward EV/EBITDA and high dividend yield.

The Company

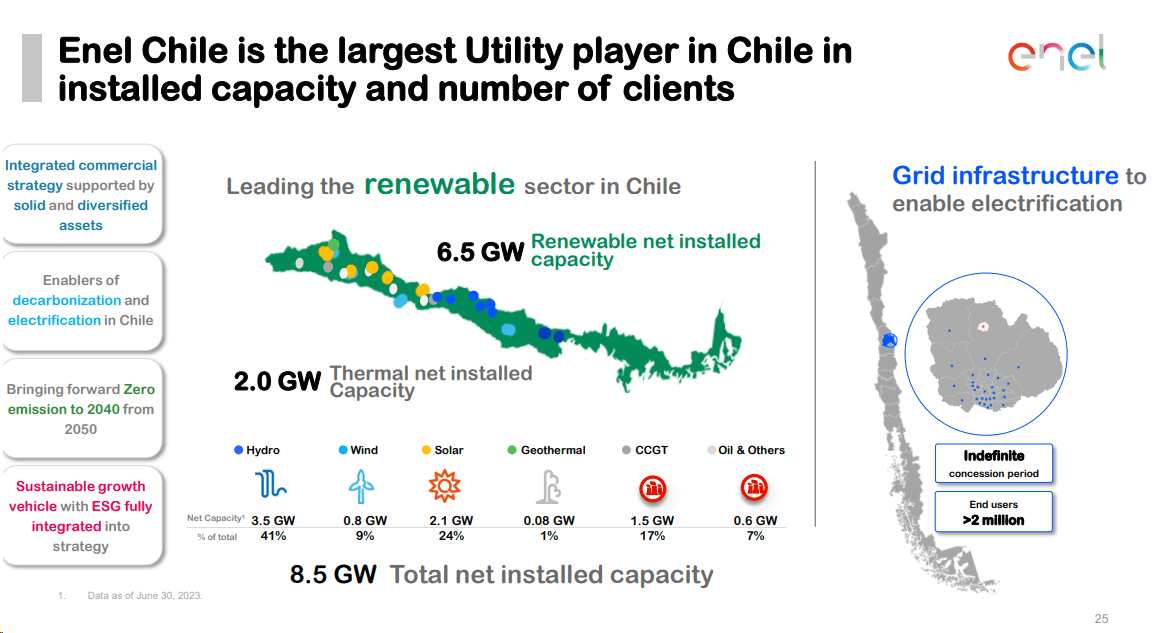

Enel Chile S.A . ( ENIC ) is a $3.8-billion market-cap electricity utility company based in Chile. They are involved in the complete energy supply chain, which includes generating electricity from diverse sources like hydroelectric, thermal, wind, solar, and geothermal power plants. Furthermore, they transmit and distribute electricity in various municipalities within the Santiago metropolitan region.

Enel Chile also provides natural gas transportation services and offers engineering consulting services. Their customer base includes residential, commercial, industrial, and other clients.

{kind=link}

So the company reports under 2 business units:

- Distribution and Networks - distribution of electricity to over 2 million customers in the Metropolitan Region of Santiago, which is the most populous region in Chile;

- Generation - generation of electricity from a variety of sources, including hydroelectric, wind, photovoltaic, geothermal, and thermal power plants.

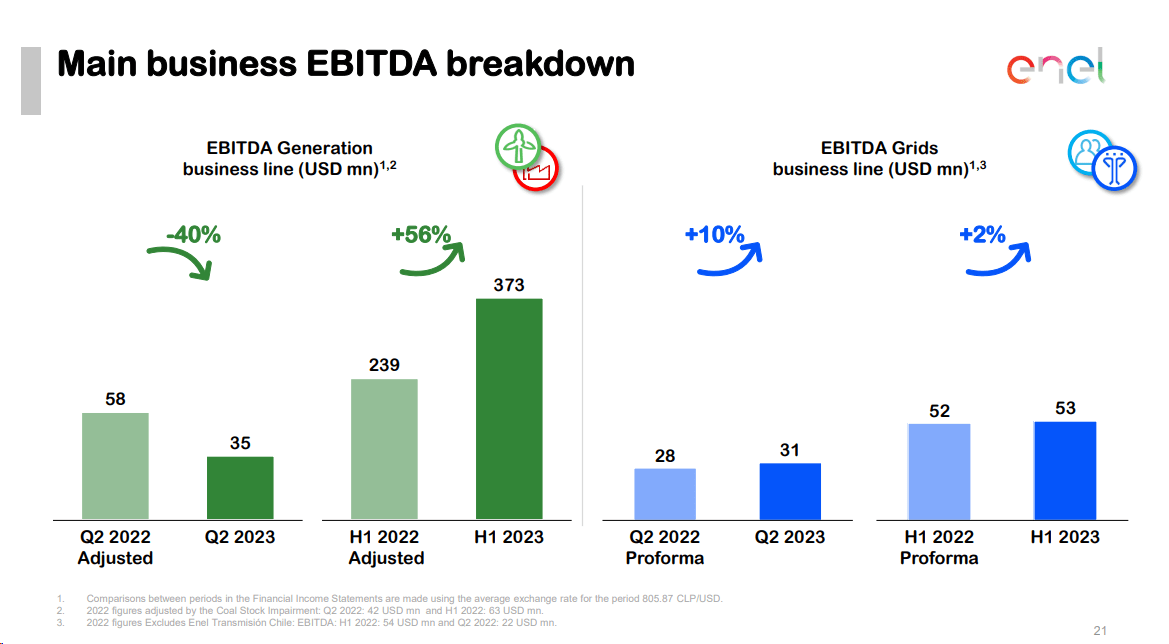

In the Generation segment, Enel Chile achieved notable results in 1H FY2023 . ENIC reported a 3.2% increase in net electricity generation, driven by greater solar and hydroelectric production resulting from new power plant commissioning and improved hydrology. Despite slightly lower physical energy sales, primarily due to reduced unregulated customer sales, operating revenues saw a substantial 17.7% increase, thanks to higher energy sales prices and increased gas commercialization. Procurement and services costs went up by 7.1%, primarily due to higher fuel consumption, increased gas commercialization costs, and elevated transportation costs. The positive outcome in this segment was reflected in a remarkable 112.9% growth in EBITDA, highlighting the strong performance of the segment.

On the other hand, the Distribution & Networks segment faced challenge s in 1H FY2023, particularly due to changes in the company's consolidation perimeter following the sale of Enel Transmisión Chile in December 2022. As a result, physical sales dropped by 16.7%, while operating revenues decreased by 2.8%. The segment did, however, experience a 2.4% increase in the total number of customers, primarily residential and commercial customers. Despite this growth, the effect of the sale of Enel Transmisión Chile and lower energy sales, especially to residential customers, contributed to the decline in operating revenues. Procurement and services costs increased by 4.3% due to higher transportation costs related to the consolidation perimeter changes. EBITDA for the Distribution & Networks business segment significantly decreased by 47.1% compared to the same period in 2022, mainly due to the effects of the Enel Transmisión Chile sale.

{kind=link}

The weakness in Q2 FY2023, as the management explained during the earnings call , was attributed to temporary factors such as increased thermal generation costs, higher spot prices, and a lower effect of gas optimization activities, resulting in a more challenging earnings performance. This is the reason why we see such a big difference between Q2 numbers and 1H numbers:

{kind=link}

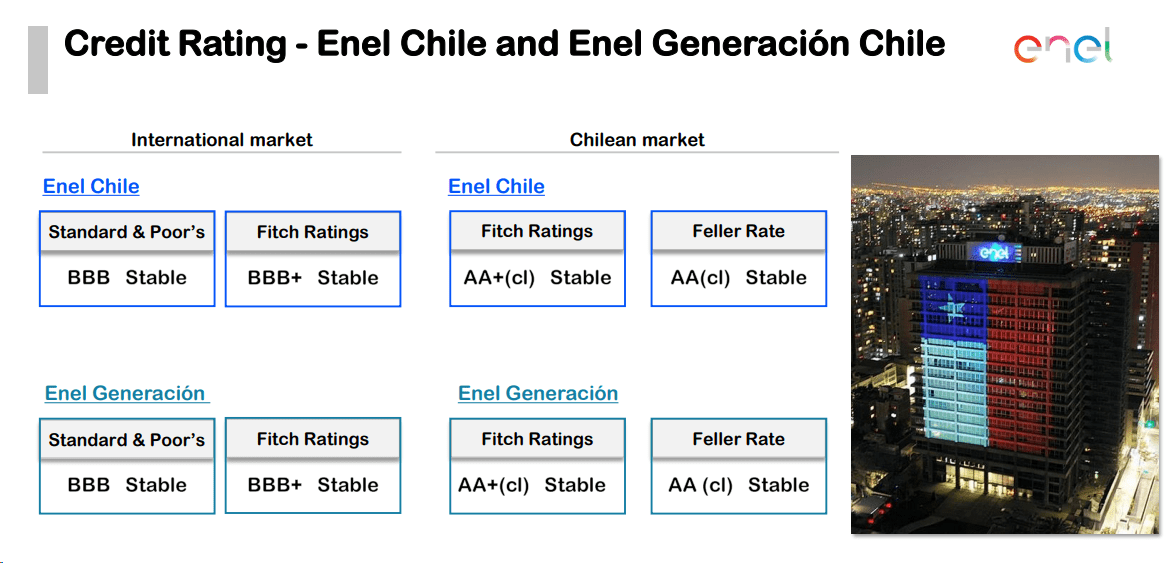

Turning to the balance sheet, it should be noted that Enel Chile's gross debt increased, reaching $5 billion in June 2023, attributed to various financial needs and the delay of certain payments. It is emphasized that this debt increase is temporary, with expected inflows from PEC 2 funds and asset sales. ENIC is working to maintain a net debt-to-EBITDA ratio lower than 3x by the end of 2023. The average debt maturity was 5.7 years, with the majority of the debt being fixed-rate (~77%). The company expects a $200 million maturity in FY2023, which was paid using a bridge instrument. The average cost of debt increased slightly to 4.7%, primarily due to changes in the debt profile and market conditions. But this is still quite small in the current conditions. At the same time, ENIC has quite high credit ratings from various agencies, which is also of interest to potential investors:

{kind=link}

The firm made a few strategic moves recently, involving the sale of its subsidiary, Arcadia Generacion Solar, to Sonnedix. The agreement entails Sonnedix acquiring the entire stake in Arcadia for $550 million, resulting in an estimated capital gain of $110 million and a cash impact of ~$500 million (net of $50 million in taxes) for Enel Chile in FY2023. This transaction is part of Enel Chile's broader asset rotation initiatives, aimed at optimizing and diversifying its portfolio to unlock value and strengthen its financial position. With the execution of this sale, along with prior agreements, I think Enel Chile is well-positioned to explore accretive market opportunities and maintain a solid financial balance. The company's strong operating performance in the first half of the year, coupled with favorable hydrology and natural gas availability, supports their confidence in achieving their FY2023 targets: the earnings call's commentary confirmed that ENIC expects to generate 1 to 2 terawatt hours more of hydroelectric power in 2023 compared to the original forecast of 9.3 terawatt hours. Each terawatt hour of additional generation is estimated to contribute around $50 million more to EBITDA.

Overall, ENIC's business is growing and modernizing - but what about the stock's valuation?

The Valuation

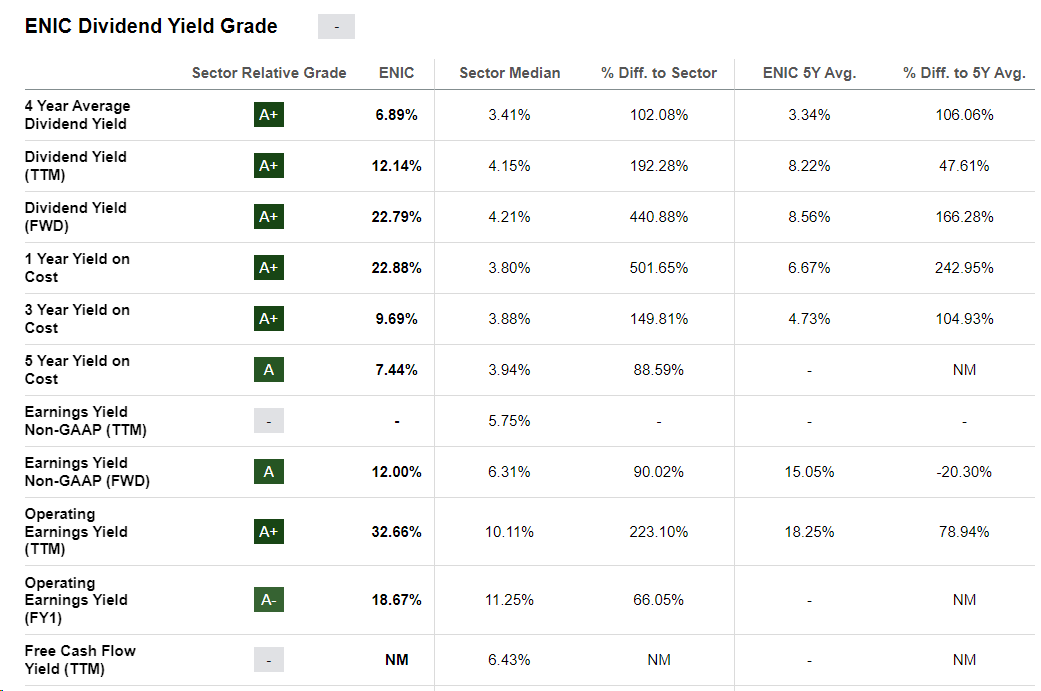

Like almost all companies in the Utilities sector , Enel Chile pays dividends, and its dividend yield of >12% is well above the industry average:

{kind=link}

However, according to Wall Street analysts , this yield will fall to ~7% by FY2024 and remain about the same in FY2025, assuming no change in ENIC's share price over the time horizons discussed:

{kind=link}

At the same time, the company is trading at 4.3 times TTM EV/EBITDA, which includes the ugly Q2 results, and just 1.8 times next year's EV/EBITDA, which looks absolutely cheap compared to most competitors and on an absolute basis.

The Bottom Line

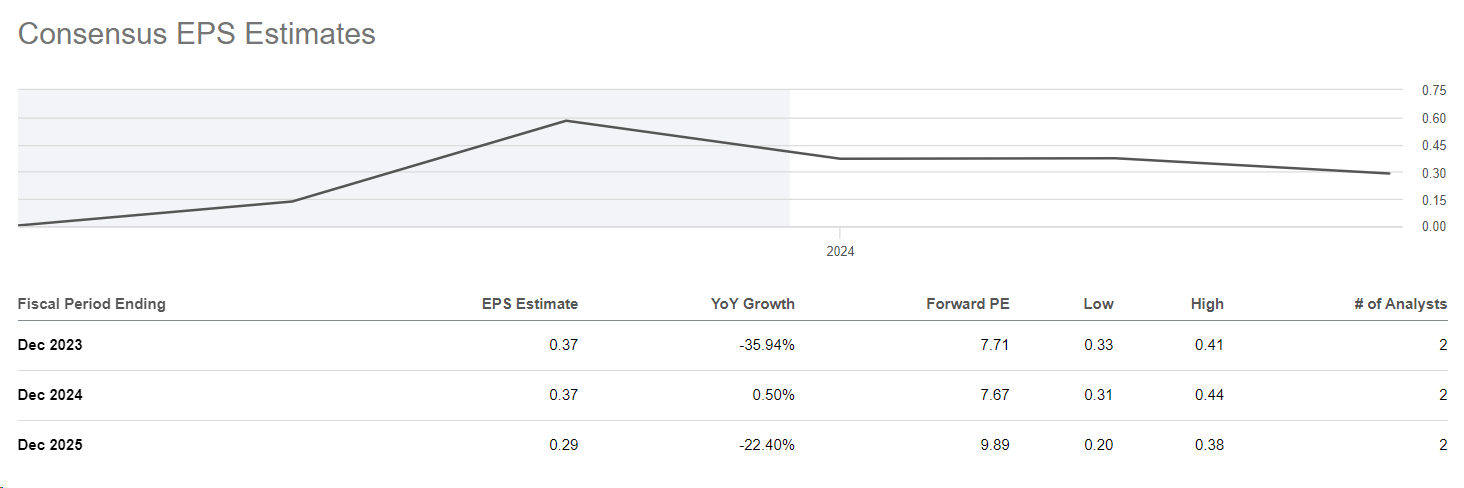

Despite the company's growth prospects, its investments in renewable energy, and quite solid growth, Wall Street analysts expect ENIC's earnings per share to decline significantly in the near future.

{kind=link}

Maybe I don't know something, and that will indeed be the case. But ENIC's enterprise value is currently valued at less than 2 times next year's EBITDA, while the company's debt is of relatively high quality and not onerous.

Of course, potential investors should understand the risks of ENIC. First off, it's risks related to the Chilean energy sector, including economic slowdown, increased competition, and regulatory changes. Enel Chile also faces business-specific risks, such as reliance on intermittent renewable energy sources, exposure to foreign exchange volatility, and high debt levels.

But it seems to me that ENIC still has growth potential despite its stunning YTD growth [+36%]. In any case, the company should maintain a dividend yield in the high single digits for the next few years, which is a kind of protection for a potential investor given the possibility of multiple expansions.

So I rate ENIC stock as a "Buy" this time around.

Thanks for reading!

For further details see:

Enel Chile: An Undervalued Company With A Solid Yield