ENIC - Enel Chile: Renewable Energy Utility With A 9% Dividend Yield

2023-07-19 12:45:48 ET

Summary

- Enel Chile S.A. has seen its shares soar in 2023.

- There may be room for further upside; the stock has still underperformed its country ETF over the past three years.

- Chile is uniquely well-suited for being a leader in renewable energy production, and electrification should drive significant sector growth going forward.

- Enel Chile isn't my favorite company in Chile, but I'm bullish on the overall economy and expect a rising tide to lift all boats.

Enel Chile S.A. ( ENIC ) is a leading Chilean power utility. Shares plummeted in recent years amid the twin blows of a prolonged drought and unfavorable political developments. However, the skies have cleared in 2023, with ENIC stock more than doubling off its lows from last year:

Can the rally keep going, or has the bounce just about played itself out? Let's take a look.

Why Chile Is An Attractive Utility Market

Chile prides itself on being one of the countries adopting green energy fastest within the Western Hemisphere. Chile is aiming for 80% renewable power generation by the year 2030. It will phase out its last coal power plant before 2040, with the hopes of achieving that milestone as early as 2030. The country will be net carbon zero by 2050, and as a big part of that, Chile plans to forbid the sale of internal combustion vehicles by the year 2035.

As you can imagine, this creates a wide array of both opportunities and issues to deal with for a major Chilean power utility. The upside is clear; fast-moving electrification of the transportation sector -- combined with favorable Chilean demographics -- will lead to a sharp increase in total demand on the grid. According to a National Energy Commission technical report from December 2021, total Chilean energy demand will rise 28% by 2030. That's a lot of growth for the traditionally staid utility sector.

Unlike many utilities aiming for a green future, there should be limited execution risk at Enel Chile. That's because the company is already at 76% renewable as a portion of its total installed capacity. Hydro makes up 41% of the company's overall power generation. Wind, solar, and geothermal combine for another 34%. The company also plans to utilize hydrogen in coming years to add to its renewable energy mix. It should be noted that Chile's northern zone has the highest solar radiation on the planet, making it a favorable area for deploying solar capacity.

The renewable power generation does come with one major headache. Hydro power is normally a dependable low-cost source of green power. However, Chile faced major droughts in prior years, which forced Enel to curtail its hydro output and substitute in higher-cost and dirtier alternatives.

The drought overhang has now cleared up, which is in part why ENIC stock has performed so well over the past year. However, there can be no guarantees that the more favorable climatological conditions will persist indefinitely.

Chile's Improving Economic Outlook

Utility companies are heavily tied to macroeconomic conditions in the regions that they serve. This leads to the second positive point for Enel Chile, which is that the benchmark iShares MSCI Chile ETF ( ECH ) is breaking out higher. In fact, shares are trading at new 52-week highs as I'm writing this:

Why has sentiment improved so markedly for Chile? Some is simply due to the global rally in equity markets that we've seen. However, there are specific positive factors at play as well. The Chilean Peso, to give one data point, has rallied 20% versus the dollar from its lows last October.

Capital is flowing back into the country because Chile's left-wing president, Gabriel Boric, has seen his popularity diminish. The proposal for a new left-leaning Chilean Constitution was voted down overwhelmingly, dealing him a sharp blow. Instead, voters have approved a new constitutional drafting committee which will be led by more conservative politicians.

There was talk of purported nationalization of the lithium miners earlier this year, along with concerns around heavier regulation of the copper sector. But with Boric's political influence on the decline, it seems that Chile will stick to a more moderate economic path going forward. That, combined with strong demand for key Chilean exports, has led to returning investor favor for the country.

ENIC Stock Verdict

There are two ways to look at Enel Chile shares right now. The first is that the stock is up 210% over the past 12 months, shares are dramatically overbought, and that the near-term catalysts such as better rainfall and an improving political backdrop have already played out. There's a case for taking some trading profits on the name, it's a totally logical viewpoint.

On the other hand, Enel Chile shares have really only recovered from the drubbing they took in 2021 and the first half of 2022. Over the past three years, Enel Chile has still meaningfully underperformed the benchmark iShares MSCI Chile ETF:

Since July 2020, ECH stock has delivered a total return of 36% compared to 12% for Enel Chile. With this longer-term vantage point, Enel Chile's recent run merely looks like playing catch-up rather than being a dramatically overdone move to the upside.

What's my opinion? I'm bullish on Chile, and as such, I'm also bullish on core operating companies there such as utilities. The long-term upside case around profitable renewable power generation combined with a growing economy and boom in mining makes a lot of sense. Even after the big rebound in the share price this year, Enel Chile shares hardly seem aggressively valued at the current price.

To that point, the stock is going for 13 times forward earnings today. Analysts project a slight increase in profits in 2024 followed by a dip in 2025. That speaks to a company that seems to be at a reasonable, if not dirt cheap, valuation.

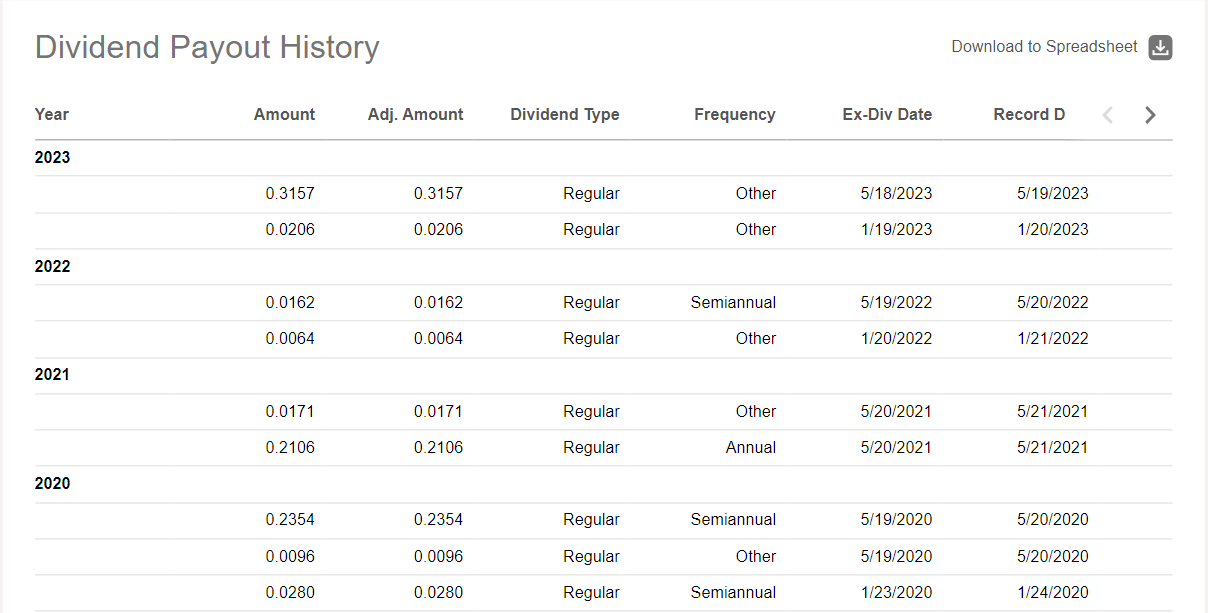

The company is also normally a large dividend payer, albeit with variable and highly fluctuating payouts:

{kind=link}

For 2023, the company paid out more than 33 cents per share, which works out to a greater than 9% dividend yield at the current stock price. The dividend payments in 2020 and 2021 were also quite generous. Do note, however, that Enel reduced its dividend to just 2.3 cents per share in 2022 amid the company's dramatic profit decline that year. As such, investors can expect generally large but not always consistent dividend payments from the company. Chile also charges a high withholding tax, it can run as high as 35% ; yield-focused investors should consider the tax situation around the stock before putting capital to work.

Overall, my view on Enel Chile is positive. I personally don't own shares (aside from my exposure via the Chilean ETF) as I see more upside in other parts of the Chilean economy. For investors looking for emerging market utility holdings with a high dividend yield, however, Enel Chile checks the right boxes.

For further details see:

Enel Chile: Renewable Energy Utility With A 9% Dividend Yield