CEQP - Energy Transfer's Massive Purchase Of Crestwood Equity Partners Makes Sense

2023-08-18 11:52:41 ET

Summary

- Energy Transfer LP has agreed to acquire Crestwood Equity Partners LP in a $7.1 billion all-stock transaction.

- The deal brings solid financial and operational benefits, including cost synergies and potential revenue growth.

- The acquisition should validate Energy Transfer's undervalued stock price and provide long-term value for shareholders.

August 16th ended up being a monumental day for both Energy Transfer LP ( ET ) and Crestwood Equity Partners LP ( CEQP ). Shares of both companies rose after news broke that the former had agreed to acquire the latter in an all-stock transaction worth nearly $7.1 billion.

Digging into the details, I found that there are solid financial and operational reasons why such a deal has been made. As a shareholder of Energy Transfer, with the company making up my second-largest holding with 12.9% of my overall portfolio, I am a big fan of any deal that brings value for shareholders. Certainly, the price paid for the business was attractive - though, personally, I would have preferred the transaction involved at least some cash given how discounted shares of Energy Transfer are. But in the grand scheme of things, this is only a small complaint, and the overall picture for both firms moving forward should be considered very positive.

An accretive transaction

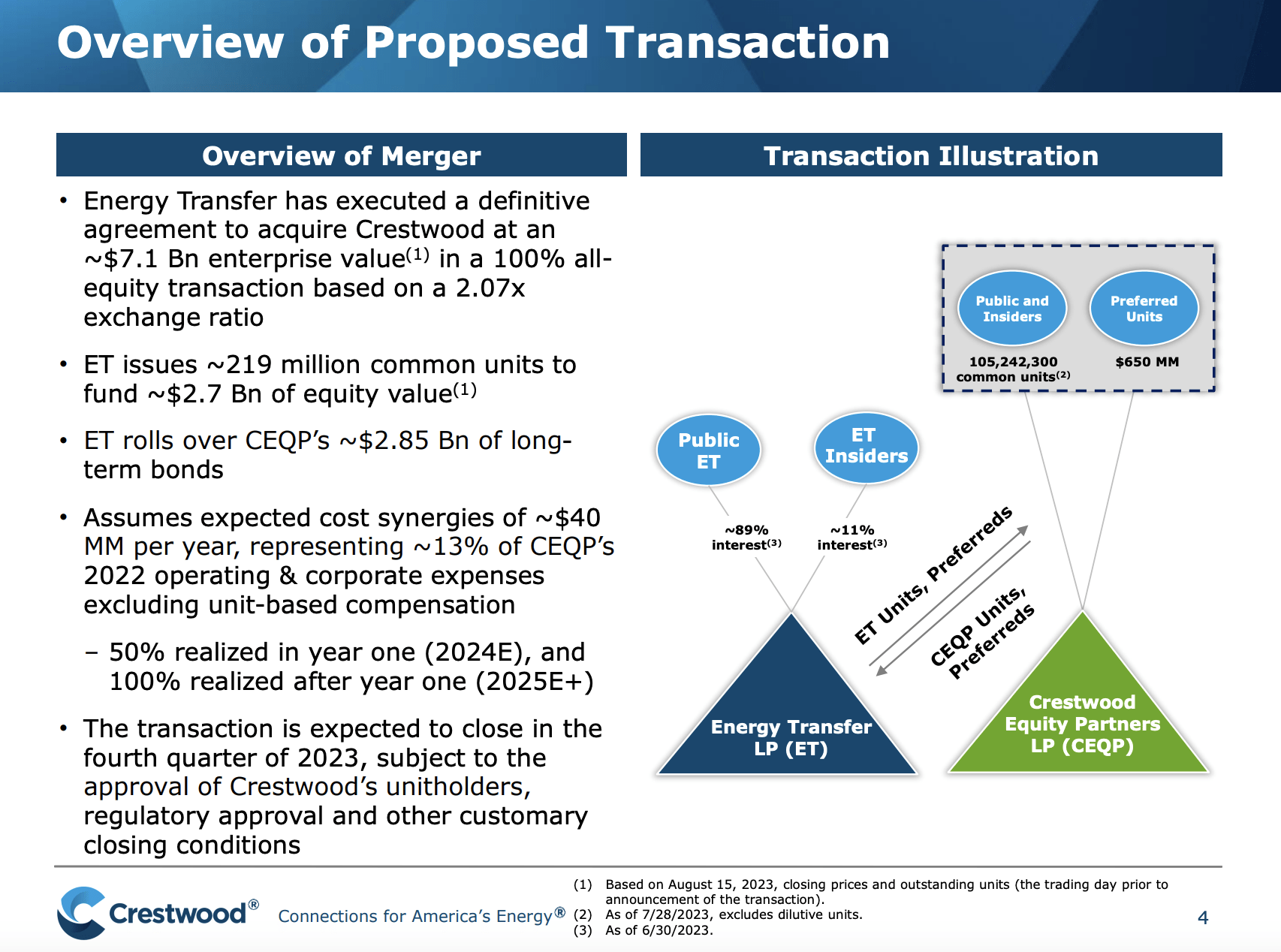

On August 16th, the management team at Energy Transfer announced that it had reached an agreement to acquire Crestwood in an all-stock transaction with an implied enterprise value of nearly $7.1 billion. For each share of Crestwood that an investor has, they will receive 2.07 shares of Energy Transfer when the transaction closes in the final quarter of this year. Based on the price that shares of Energy Transfer was trading at immediately before the transaction was announced, this would imply an equity value of $2.75 billion. To get up to the $7.1 billion of enterprise value, we add $3.25 billion of net debt, $434.2 million of non-controlling interests, and $650 million of preferred stock that Crestwood has.

This price does not really represent any premium for shareholders of Crestwood. The implied buyout price works out to approximately $26 per share, using the price that shares of Energy Transfer were trading at on August 15th. Even so, that did not stop Crestwood stock from climbing 4.6% for the day, while shares of Energy Transfer popped higher by about 1.7%. It is unclear why Crestwood is trading at a premium to the buyout price, but this usually means that the market anticipates some other firm stepping in with an offer.

{kind=link}

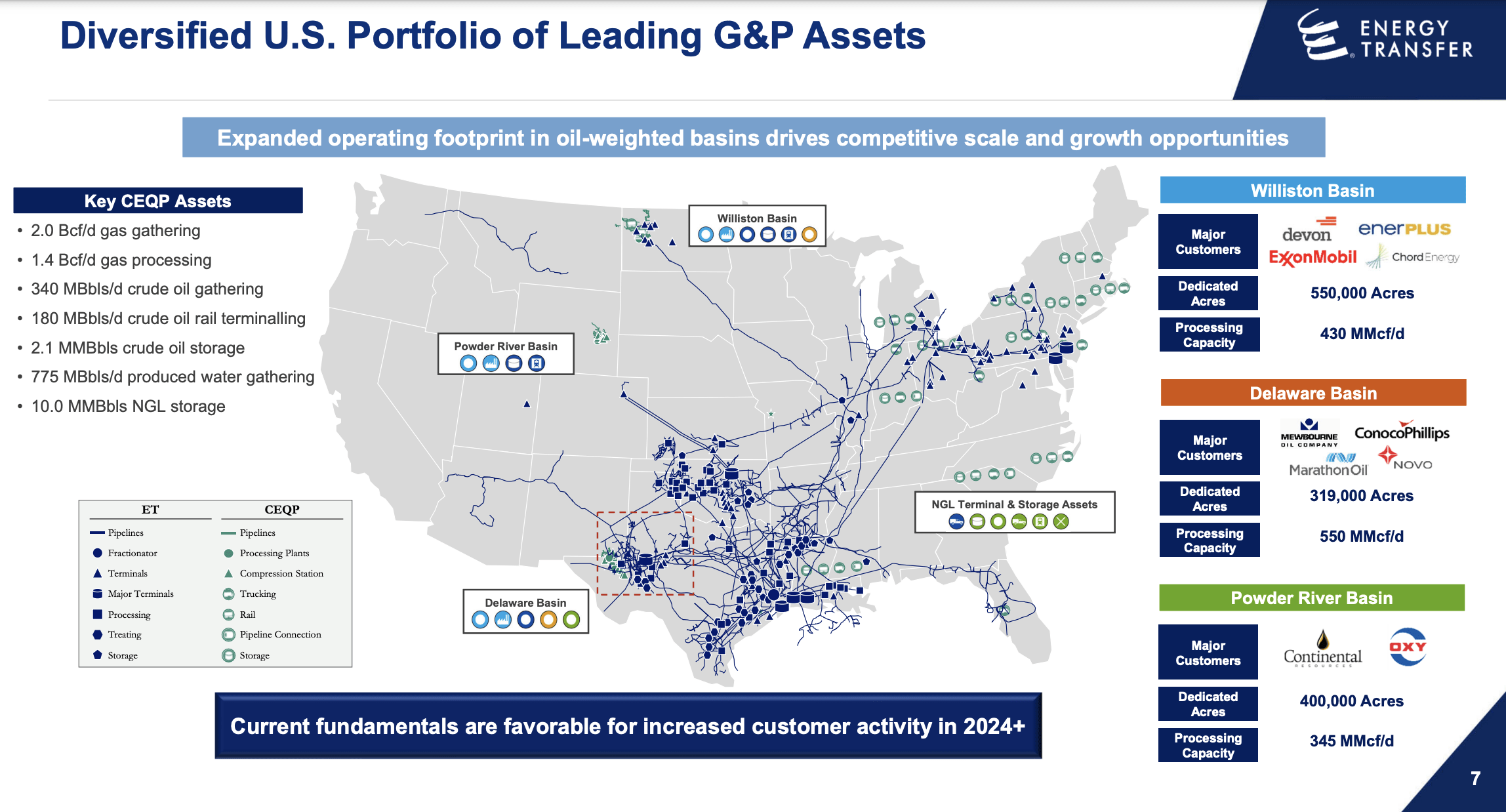

As you can see in the image above, the two companies do have some rather substantial overlap in terms of the assets that they have in operation. Beyond any doubt, Energy Transfer is the larger of the two, as made clear by the $40.33 billion market capitalization of the company. So, this means that its physical footprint is also substantially larger. The assets that seem to be particularly appealing to Energy Transfer are those focused on the Williston and Delaware basins, that should complement the acquirers’ downstream fractionation capacity at Mont Belvieu and its hydrocarbon export capabilities in both Texas and Pennsylvania.

There are, of course, other assets that Crestwood would bring to the table that are valuable to the company. For instance, it opens up the door to the Powder River basin because of the gathering and processing system that Crestwood has located there. Combining the storage and logistics business that Crestwood has with Energy Transfer’s NGL, refined products and crude oil assets pave the way for operational synergies. The location of oil and gas exploration and production drilling and completion activities, as well as operations geographically close to the assets that Crestwood has, opens the door for various growth prospects, including, management said, the potential to make bolt-on acquisitions.

{kind=link}

Another reason for this deal is the financial side of matters. For starters, Energy Transfer believes that it can capture around $40 million in annual run rate cost synergies from the deal. And that is even before factoring in the benefit from potential revenue growth. Even though this may not sound like much, when compared to the $300 million in core costs that Crestwood incurs each year, that is a rather sizable amount of capital on a relative basis. Management also indicated that some synergies could come from debt refinancing in the years to come. Over the next five years, Crestwood should have around $1.1 billion worth of debt coming up for refinancing or repayment.

Frankly, I am skeptical about any benefits here. The $500 million of debt coming due in 2025 bears an annual interest rate of 5.75%. And the $600 million coming due in 2027 bears a rate of 5.625%. The last sizable amount of debt that Energy Transfer raised, which was back in December of last year for $2.5 billion, was in the form of senior notes. This was done in two different tranches, with the cheapest of the two bearing an annual interest rate of 5.75%. I would be surprised, especially with interest rates having risen since then, if the company could get better terms on refinancing. Where it might get some benefit, however, would be on the credit facility side of matters. As of the most recent quarter, Energy Transfer had a weighted average interest rate of 6.33% on its credit facility. That compares to the 7.56% that Crestwood had. But on only $417.4 million, we are looking at potential cost savings of only $5.1 million on an annual run rate basis. That truly is a rounding error.

It was also mentioned that, in two years, there could be the opportunity to essentially refinance the preferred units of Crestwood. The $650 million that's currently outstanding bears an annual interest rate of 9.25%. The cheapest of the preferred units that are publicly traded for Energy Transfer have a rate of 7.375%. But those are fixed floating rates. And as I detailed in an article not too long ago, the switch to floating, given current interest rates, could take the amount paid on those securities up to nearly 10%. So I really don't see much of an opportunity on that front unless there is something that management knows that I don't. It is worth noting that, in some instances, the decision to not follow through with the agreement by either party could result in Crestwood having to pay a $96 million breakup fee to Energy Transfer.

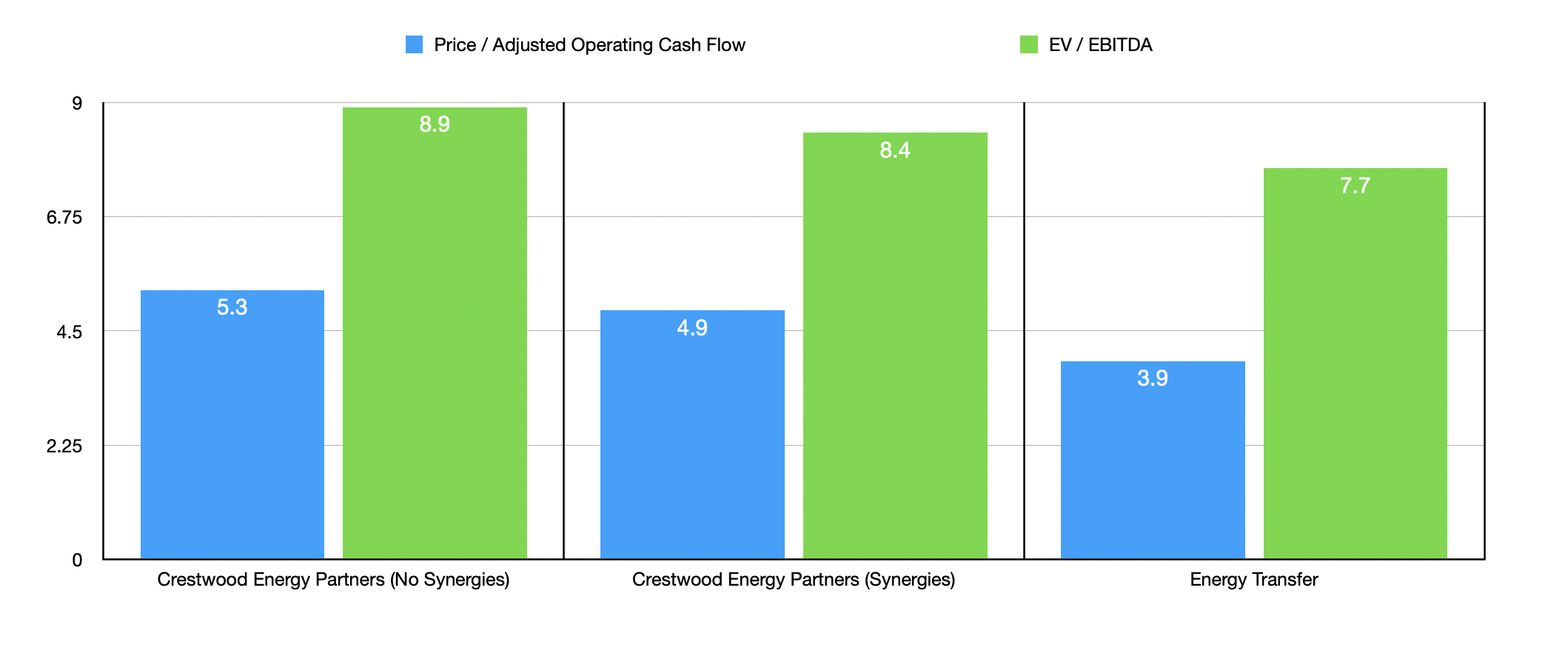

The big question that investors likely have is whether this deal ultimately makes sense for Energy Transfer. It does, but I would argue that the firm should have used cash to pay for the transaction instead. For the current fiscal year, Crestwood said that EBITDA should be somewhere between $780 million and $860 million. They did say that it will likely be in the lower half of that range. So for the purpose of this article, I assumed that EBITDA will be $800 million. If we strip out interest expense on its current debt and a modest amount of taxes that the company pays, we would end up with operating cash flow of roughly $576.2 million. For the purpose of this analysis, since I am focused on the common stock as opposed to the preferred, I decided to strip out the preferred distributions from this to get us a bit lower at $516.2 million.

{kind=link}

Using these figures, I was able to create the chart above. On a forward basis, Crestwood is trading at a price to operating cash flow multiple of 5.3, while the EV to EBITDA multiple should be 8.9. The numbers dropped to 4.9 and 8.4, respectively, if we assume that synergies forecasted by management come into play. While this is very cheap and is definitely affordable compared to similar firms, it's not as cheap as Energy Transfer. It is trading at a price to operating cash flow multiple of 3.9 and at an EV to EBITDA multiple of 7.7.

This price disparity is why I would have preferred the deal being done entirely or mostly in cash. It's painful, as a shareholder, to see undervalued equity being used to acquire a more expensive company. But because shareholders of Crestwood will only own 6.5% of the combined business, the overall multiples of Energy Transfer, even without the synergies, won't change much. The price to operating cash flow multiple will remain 3.9, while the EV to EBITDA multiple will inch up slightly to 7.8. It is because of this minimal impact on the company's valuation that I am still optimistic about the deal.

{kind=link}

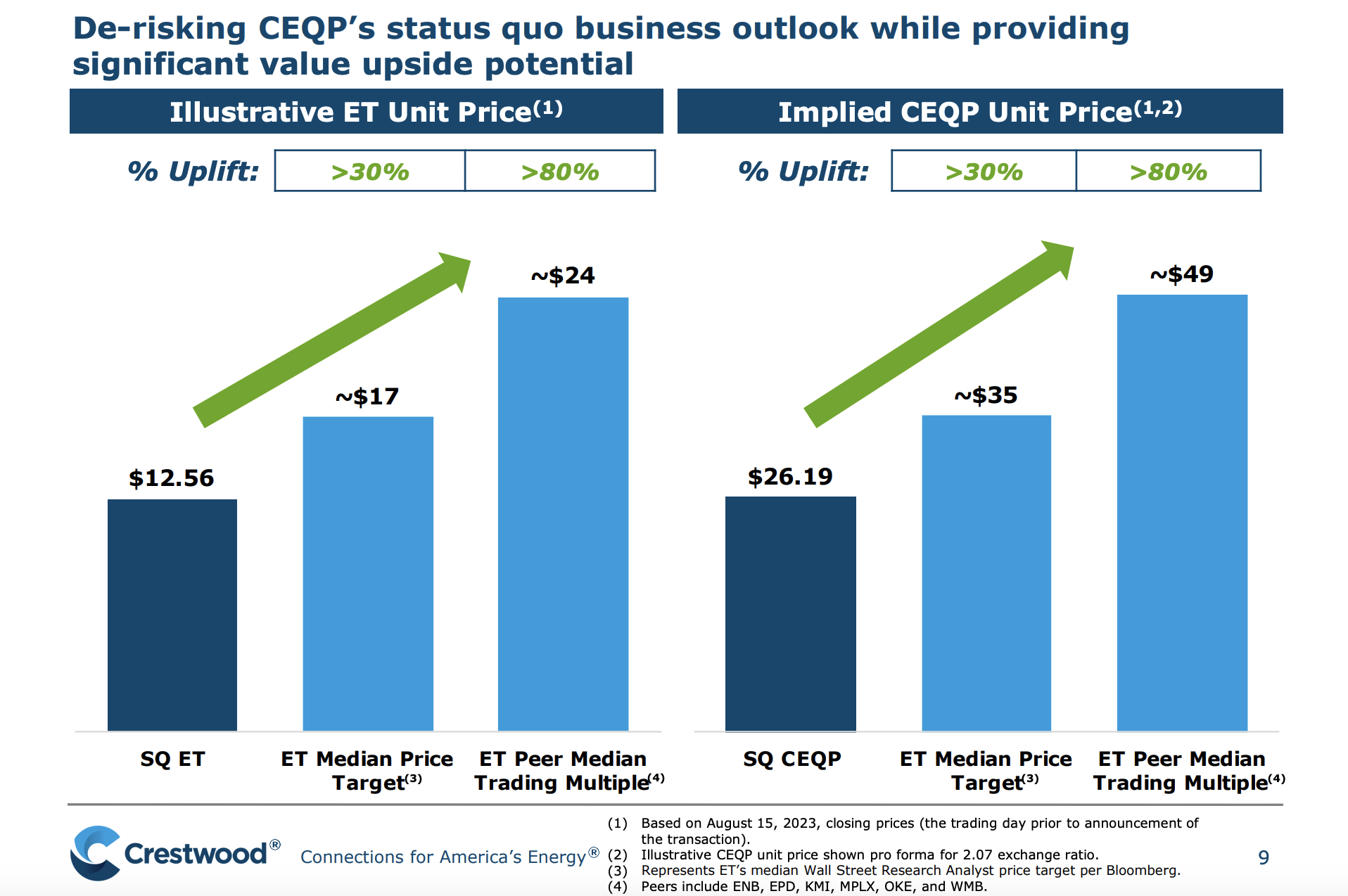

Interestingly, in its own presentation regarding the transaction, Crestwood made its case for why this deal makes sense for its shareholders. They also argued, in the same way that I have in prior articles , that, relative to similar firms, Energy Transfer is drastically undervalued. Using August 15th closing prices, the transaction assigned a value of $26.19 to shares of Crestwood. But seeing Energy Transfer hit the median price target set for it by Wall Street analysts of $17 per share would result in an implied value for Crestwood investors of $35 per share. That is upside of 33.6%. And if the company is compared to similar enterprises, using the median trading multiple for them, we would get an implied share price for Crestwood of $49 per share. That translates to an upside of 87.3%.

It is refreshing to see some other party perform an analysis like this. It means that they also are of the opinion that shares of Energy Transfer are significantly undervalued, and they believe that, by latching themselves to the company now while it is cheap, they can experience the upswing that will eventually come to pass.

Takeaway

All things considered, I must say that I am fairly happy with this transaction. Even though the deal is not structured the way I would have preferred, it does represent a valuable opportunity for Energy Transfer to get a quality asset that will benefit it in the long run, while simultaneously giving shareholders of Crestwood the opportunity to experience strong upside once the market realizes just how cheap Energy Transfer stock actually is. I am skeptical of some of the benefits, such as refinancing debt and preferred stock. But in the grand scheme of things, these are fairly small qualms. With a deal does more than ever is validating my prior bullish stance on Energy Transfer, which makes me happy in these uncertain times.

For further details see:

Energy Transfer's Massive Purchase Of Crestwood Equity Partners Makes Sense