ENFN - Enfusion: Still Very Attractive

2023-04-07 10:17:56 ET

Summary

- Enfusion remains over 50% below its all-time high in 2021.

- The company's fundamentals remain intact and the business is highly resilient thanks to its stickiness and efficiency.

- The latest earnings result was impressive with robust growth on both the top and the bottom line.

- The current valuation is significantly discounted compared to peers.

- I rate the company as a buy.

Investment Thesis

Enfusion ( ENFN ) was roughly flat since my coverage last June, but still down over 50% from its all-time high in late 2021. I believe the company remains a compelling buying opportunity as the fundamentals continue to be strong and the business is highly resilient. Despite facing macro headwinds, the latest earnings showed excellent growth on both the top and the bottom line. Its valuation is also attractive, as multiples are meaningfully lower than other SaaS companies with similar growth rates. The current price level looks discounted and should offer solid upside potential, therefore I rate it as a buy.

Highly Resilient

For those who are unfamiliar with Enfusion, you can check out my previous article where I discussed the company's business, market opportunities, and solutions. The fundamentals remain intact and I want to touch more on its resiliency in this article, which is often overlooked by investors in my opinion. This should also be important in the near term as the economy is starting to show signs of weaknesses.

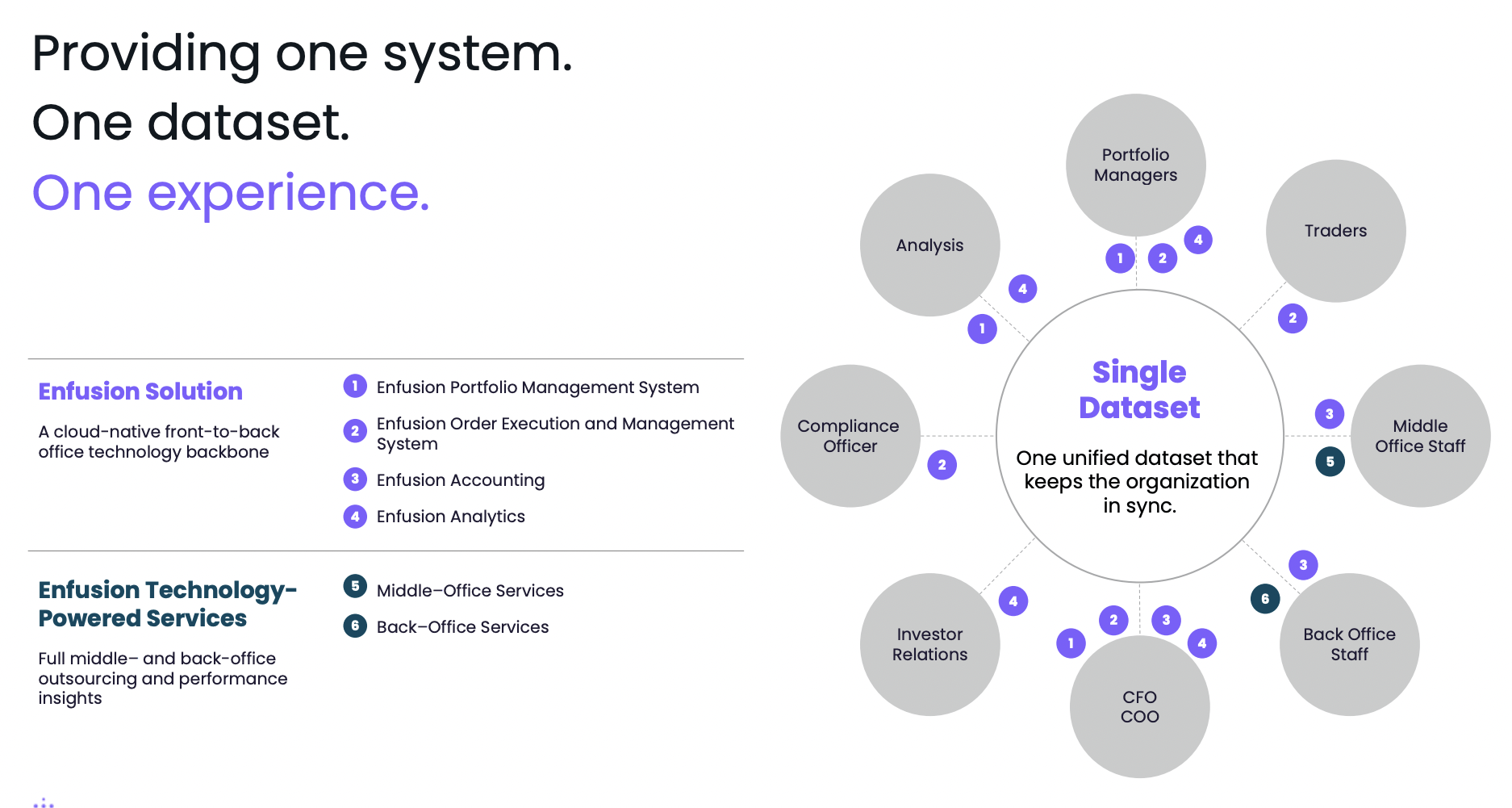

Enfusion operates as a vertical software company that specializes in the finance industry with its end-to-end solutions. Vertical software companies often have better resilience and lower churn rates due to their high stickiness, and Enfusion is no different. The company's solutions are often deeply integrated into the customers' workflow, which makes them almost impossible to switch as they rely heavily on it for operation. The switching costs are also high due to the complex nature of the workflow.

As mentioned in my previous article, the company's all-in-one solution is able to vastly improve efficiency and reduce costs, as it eliminates the need to run and pay for multiple products. This will even be more critical in an economic downturn, as customers will be looking for ways to streamline their operations and optimize their cost structure. As mentioned by the management team , they believe the ongoing economic uncertainty may actually be a tailwind for them. I believe Enfusion will be one of the few SaaS companies that can navigate upcoming volatility with relative ease.

Oleg Movchan, CEO, on macro uncertainty :

We believe our business is well positioned not only to weather the ongoing macroeconomic uncertainty, but also benefit from it. In terms of outside launch a tentative investment platforms and traditional asset managers are optimizing their cost structures by converting their legacy system to Enfusion software and relying on our services to support their business. That's a scenario what we typically saw throughout the history of the firm.

{kind=link}

Financials

Enfusion announced its latest earnings last month and the results are outstanding considering the current backdrop. The company reported revenue of $40.5 million, up 27% YoY (year over year) compared to $31.9 million. ARR increased 30% YoY from $127.1 million to $164.7 million. The growth is driven by the increase in customers and higher spending from existing users. The company ended the quarter with 819 customers, up 11.6% compared to 734. While the average contract value grew 12.5% from $184,000 to $207,000. The net dollar retention rate was 115.4%, up 40 basis points from 115%.

The bottom line was superb as the company committed to profitability. Operating expenses were $25.8 million compared to $314.2 million, but this is not comparable due to the timing of the IPO which artificially inflated the operating expenses in the prior year. The discipline in spending resulted in the adjusted EBITDA skyrocketing 113% YoY from $3.2 million to $6.8 million. The adjusted EBITDA margin also expanded 670 basis points from 10% to 16.7%. The operating cash flow flipped from negative $(5.8) million to $7.5 million, or 18.6% of revenue. Net income was $0.8 million, or $0.01 per share.

The company's balance sheet remains healthy with $63 million in cash and no debt. Its latest guidance for FY23 was also solid. Revenue is expected to be $185 million to $190 million, which translates to a growth of 25% at the midpoint. Adjusted EBITDA is expected to be $32 million to $34 million, or a growth of 70% at the midpoint.

Valuation

While the company continues to see upbeat momentum, its valuation has compressed significantly as the share price plummeted. The company is currently trading at an EV/sales ratio of only 4.7x, which is extremely cheap for a profitable SaaS company with a 25%+ revenue growth rate. As shown in the chart below, its multiple is substantially lower than other SaaS companies such as Procore ( PCOR ) and Bill.com ( BILL ). They are trading at an EV/sales ratio of 9.9x and 8.4x, which represent a whopping premium of 111% and 79% respectively. The company's valuation may be discounted due to the smaller TAM compared to peers, but there should still be ample room for further expansion as the current penetration rate remains low.

Investors Takeaway

I believe the massive drawdown continues to present a great accumulation opportunity for Enfusion. The company has solid fundamentals and its business nature also makes it highly resilient to macro uncertainties. The strength is translating to its earnings with strong growth across the board. Despite the quality fundamentals and superb growth, valuation is still substantially below other SaaS peers. I believe the valuation gap is unjustified and there should be meaningful upside potential as its multiple reverts to peers' levels. Therefore I rate the company as a buy.

For further details see:

Enfusion: Still Very Attractive