GMVHY - Entain: Betting On Gambling Adaption In The U.S.

2023-06-28 13:57:41 ET

Summary

- Entain's share price has underperformed compared to its main peer Flutter Entertainment, and the company is trading at a considerable discount to the sum of its parts.

- Entain's 50% stake in BetMGM offers significant growth potential in the US online sports betting and iGaming market, with the joint venture expected to turn profitable in H2 2023.

- A sum-of-the-parts analysis values Entain at 1686p per share, 38% higher than the current stock price, making it an attractive opportunity for long-term investors.

We present a long thesis on Entain (GMVHF) in the light of recent underperformance, while exploring different facets of the business. We think this is an attractive opportunity to accumulate shares in a growing company trading at a considerable discount to its sum of the parts.

Entain PLC

While the share price of its main peer Flutter Entertainment PLC (PDYPF) has risen by nearly 35% year-to-date, Entain’s share price has declined by 9%, underperforming by 44%, and widening the valuation gap on an EV/EBITDA basis massively: Entain is now trading at nearly half of Flutter’s multiple. As per our estimates, earnings are set to grow by 2.4x between 2023 and 2025 and underlying business fundamentals remain largely unchallenged, with the US BetMGM joint venture having a multiyear growth pathway.

However, the stock price performance seems to be reflecting less optimistic scenarios. Due to the speculative appeal of its BetMGM venture and the possibility of MGM Resorts coming back with an offer, Entain has long been a favorite of special situation investors, with a large number of arbitrage funds being invested in the name in early 2023. The hopes of such deal were quashed when MGM Resorts CEO Hornbuckle said “The simple answer on Entain is no, we’ve moved on. … We value the relationship with Entain. We value BetMGM.” in early February. The stock price tumbled as event-driven funds that categorized this as a pre-deal situation no longer had an event-oriented rationale to hold and started dumping the shares. Since then, Entain printed decent FY numbers in line with guidance, underwent a significant “clearing event” which removed regulatory uncertainty: the publication of the UK Gambling White Paper, announced a major acquisition in Poland earning the scold of Eminence Capital, and became the subject of a bribery scheme investigation .

We will do a deep dive into the events, analyze differing viewpoints on key issues and drivers, and assess the potential implications for investors.

A quick introduction to Entain

Entain plc ((GMVHF)) is a multinational sports betting and gaming group operating through online and retail channels. It was previously known as GVC Holdings until December 2020. Entain has grown exponentially in the last decade, organically and through M&A including a merger with online operator bwin.party in February 2016 which was followed by a successful integration, reaching all targeted synergies and addressing underlying growth issues at bwin; and the acquisition of retail operator Ladbrokes Coral for ~£4 billion in 2018, creating a gaming entity with solid brands and a strong regulatory profile.

Entain tends to look mostly at markets in which has little to no presence – in geographies that are either fully regulated or some form of regulation is being discussed, and across verticals, it has experience in and can leverage its technological platform, migrating newly acquired operators from third party solutions into its tech stack.

Entain owns 50% of BetMGM, its JV with MGM in the US. It is a top 3 operator and utilized Entain’s proprietary technology and MGM’s brand and customer database. The US opportunity is the most important driver of value creation for Entain going forward, given the TAM of $37 billion (company estimate), consolidated among the top 3 players.

We forecast growth (ex-US) in the high single digits range for the sector thanks to increased regulation in new markets and gain of market share vs land-based counterparts driven by an increase in internet access and penetration of smartphones.

Entain had revenue of ~£4.3 billion in 2022, with an underlying EBITDA of £993 million.

FY 2022 Results Presentation FY 2022 Results Presentation

{kind=link}

{kind=link}

BetMGM: Understanding the TAM and profitability

Entain owns a stake in BetMGM, a 50/50 joint venture with MGM Resorts to grasp the giant online sports betting and online casino gaming opportunity in the US. Although the JV lags behind Fanduel (owned by Flutter) and DraftKings in terms of market share due to a later start it ranks second in terms of profitability and its prospects look bright. BetMGM is poised to be a major player in a fast-growing and profitable oligopolistic market with significant economies of scale, sticky customer bases, and notable technological barriers to entry.

To put this into perspective, let’s get a look at the estimates presented in BetMGM’s May 2022 Investor Day. The total addressable market in North America is expected to reach $37 billion of Gross Gaming Revenue, with BetMGM expecting to reach a long-term market share of 20-25% and a long-term EBITDA margin of 30-35%. Analyst estimates on the TAM vary between $35 billion and $45 billion and EBITDA margins are reasonably in line with margins in mature gambling markets in affluent countries. BetMGM believes iGaming will be available to ca.38% of the US population and online sports betting to 80% of the population.

We believe the potential of BetMGM is still somewhat lost to investors as the JV is still producing losses. However, as it turns into profitability in H2 2023 we believe it will start driving the group’s valuation multiples down and delevering quickly

FY 2022 Results Presentation

iGaming vs OSB

Due to MGM Resorts’ expertise and capabilities in casino gaming, BetMGM is particularly strong in iGaming. Moreover, the average iGaming GGR per adult is expected to be $160 whereas the average online sports betting GGR is ca. 45% lower at $90. Hence we believe that any positive surprise in terms of higher-than-expected iGaming adaption would have a disproportionate positive effect on BetMGM. The legalization of online gambling is a lot trickier politically than online sports betting given its addictive nature. However, we believe that the legalization of online sports betting will facilitate the legalization of iGaming as states become more accustomed to these practices, and the experience of states which have already legalized it successfully such as New Jersey, Pennsylvania, etc. without negative consequences will serve as a positive catalyst. In addition, serious lobbying work done by gambling interest groups and the positive impact on state budgets should further incentive legalization. We will delve deeper into the value of BetMGM in our Valuation section.

Past bids

MGM made a bid approach for Entain in January 2021 at 1383p/share at a 22% premium which was rejected.

In September 2021, Entain also received interest from DraftKings, initially at an undisclosed price. Later Entain disclosed that the proposed offer was at 2800p/share with 630p in cash and the rest in DraftKings shares. After discussions, DraftKings walked away. The large investment required from DraftKings and the complexity of integrating the two companies would have made finalizing a deal tough.

Can MGM Resorts still come back for Entain?

The street is torn on this one. It is important to note that MGM Resorts acquired LeoVegas in May 2022 to improve its digital presence and capabilities. In MGM Resorts’ words, this acquisition provides a unique opportunity for the company to create a scaled global online gaming business. Moreover, in May 2023 LeoVegas acquired Push Gaming Holdings, a digital games developer for betting and gaming companies, with a portfolio of over 30 games. The acquisition of LeoVegas reduces MGM Resorts’ need for Entain’s tech stack.

In addition, the statement by the CEO denying any interest seems to have put a lid on this. We believe a deal would still be compelling from a financial perspective and it would be a great way for MGM Resorts to fully own a great asset before it matures and becomes too expensive to acquire. We do NOT count on MGM Resorts acquiring Entain for this to be an attractive investment opportunity, however, we would be pleased to see an offer materialize.

UK White Paper

The UK government released the Gambling White Paper in late April. The report included: a £15 stake limit for players over 25; a £2 or £4 stake limit or a risk-based approach for players aged 18-24; financial vulnerability checks, and enhanced information checks. The government estimates the planned measures will have a total negative impact in the range of 8-14% for online Gross Gaming Revenue.

Nevertheless, due to self-imposed measures that have already been implemented, as per our forecasts the impact for Entain (and Flutter as well) should be a lot smaller in the range of 1-2%. This was a major relief in terms of providing regulatory certainty, as investors had been expecting the white paper from the DCMS for more than two years amid a string of delays.

STS Holding SA Acquisition

On June 13 th Entain announced the proposed acquisition of STS Holding SA the leading sports betting operator of Poland. Entain offered 24.8 Polish zlotys per share, in a £750 million deal, valuing STS at 11x EV/EBITDA. Entain and partner EMMA Capital will fund the STS offer in proportion to their ownership in Entain CEE i.e., about 75% and 25%. Entain expects a run-rate of £10m+ in synergies and EPS accretion since year 1.

Entain will be doing an equity raise of £600 million (ca. 8% of outstanding shares) with £450 million going towards the financing of the deal, and £150 million going for future acquisitions.

This acquisition is part of Entain’s strategy to consolidate the fragmented Central and Eastern European gaming markets. Specifically, Poland is a highly regulated high-growth market and STS is the market leader with around 40% market share.

Eminence Capital Letter

The shares dropped 10% on the news of the acquisition. Eminence sent an open letter to the board. Below is an excerpt from the letter:

“We were therefore disappointed to learn that Entain has decided to fund the recently announced purchase of STS Holdings by issuing shares representing approximately 8% of its market cap. This approach is perplexing on many levels. While we can support the Company pursuing seemingly rational acquisitions, funding them with highly undervalued equity is an empire building, shareholder value destroying strategy. Further, that the Entain Board has previously rejected multiple takeover approaches at materially higher prices on the grounds that those offers undervalued the Company, but then turn around and issue equity at depressed prices for an asset that is at best a “nice to have” is illogical.

Moreover, while calling this deal “accretive” on an EPS basis may be technically correct, it demonstrates that management either doesn’t understand finance or, worse, that they believe the Company’s shareholders are naive. Issuing Entain stock at ~7x EBITDA (excluding the value of the BetMGM JV) to buy an asset at ~12x EBITDA is value destructive to shareholders, even with incredible synergies.”

We fully agree with Eminence here. We believe this has been a ham-handed decision that erodes investor confidence. Entain has a solid track record of value-accretive M&A and the STS deal clearly isn’t an example of that. We would like to see more constructive activism going on, to make sure the company doesn’t steer in the wrong direction.

HMRC Investigation into Turkish operation 2011-2017

Entain is being investigated for potential bribery offenses in its former Turkish subsidiary and expects a substantial financial penalty. Entain has also been fined in the past: e.g. in August 2022, it was fined £17 million for social responsibility and anti-money laundering failures in 2022. We believe the impact is already reflected in the share price and do not expect major negative surprises.

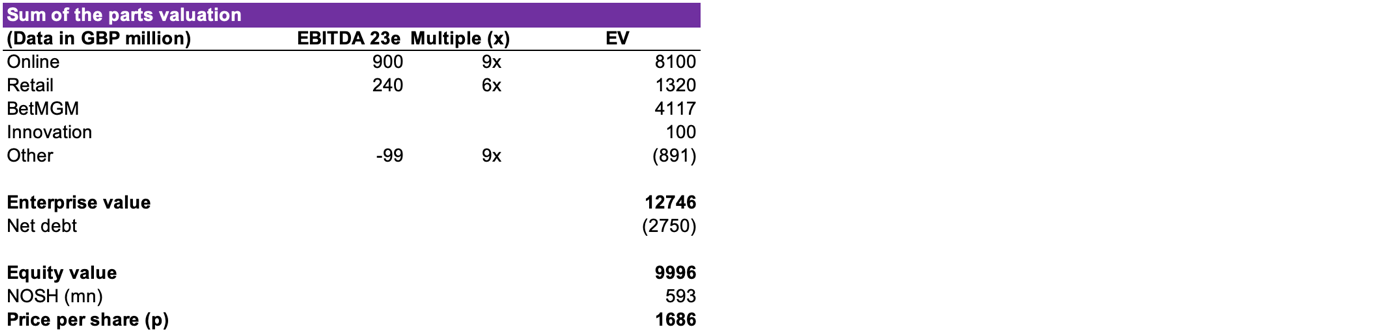

Valuation

We use a sum of the parts analysis to value Entain. This methodology properly reflects the differences between the JV and the rest of the business.

Valuing BetMGM: We assume the market size will be equal to the TAM by 2030 at $35 billion. BetMGM has a TAM of $37 billion in its investor day presentation. We assume a market share of 20% which is also on the low end of the company’s assumptions, and a bonus rate of 30%, hence 70% of the Gross Gaming Revenue converts into Net Gaming Revenue. We then assume an EBITDA margin of 30% and arrive at $1.4 billion of EBITDA in 2030. We value the business at 12x EBITDA in 2030, at $17.6 billion. We then have to discount this back to the present. Using a cost of capital of 8% we arrive to an equity value of $5.1 billion for Entain’s 50% stake in BetMGM.

{kind=link}

{kind=link}

We then value the rest of the business on the basis of our 2023 EBITDA forecast. We think 9x is fair for the online business given its current growth profile and historical trading multiples, while the retail business which is stagnant / in decline deserves 6x.

We arrive at an equity value of 1686p per share, 38% higher than the current stock price. Our price target is equal to $2.15 per share.

Risks

Risks that could challenge our long thesis on Entain include adverse macroeconomic conditions leading to a deterioration in business activity, slower than expected online sports betting and gambling adaption in the US, the emergence of additional competitors in the US leading to market share losses or a decline in profitability, unexpected regulatory restrictions, penalties for violations especially for past activities in unregulated markets such as Turkey, and value destructive M&A activity i.e. deals financed with undervalued equity (e.g. the latest deal).

Catalysts

There are no hard catalysts on Entain at the moment as we do not expect a deal to materialize. However, the swing into profitability of BetMGM in H2 2023 and further growth in the US is a key driver of the equity story.

Conclusions

We recommend building a long position on Entain, given the favorable growth backdrop in the US and the hidden value of the JV. The stock is trading at a discount to its sum of the parts, and we expect this gap to start closing as the JV becomes profitable and Entain’s valuation multiples start going down.

For further details see:

Entain: Betting On Gambling Adaption In The U.S.