CMSD - Entergy: This Renewable-Focused Utility Could Be Worthy Of Purchase Today

2023-04-25 17:27:32 ET

Summary

- Entergy Corporation is a large electric utility serving the Gulf Coast region of the United States.

- The company is the beneficiary of population growth throughout its region and favorable conditions for the deployment of renewables.

- The company has remarkably stable cash flows, which could prove beneficial as the near-term economic outlook is uncertain.

- The company is positioned to deliver a 10% to 12% total return on average for the next three years.

- Entergy stock appears to be undervalued at the current price, so might be worth adding to a portfolio today.

Entergy Corporation ( ETR ) is a regulated electric utility that serves the states of Texas, Louisiana, Mississippi, and Arkansas. The utility sector in general has long been a favorite among conservative investors, such as retirees, due to its relatively stable cash flows and high dividend yields. Entergy Corporation is certainly no exception to this rule about high yields as the stock yields 3.93% at the current price, which is well above the sector average. In addition, the company boasts surprisingly strong prospects in the renewable energy sector as much of its service area is perfect for the use of solar and wind power.

Unfortunately, some sources point to Entergy stock being fairly expensive at the current price, so investors will have to pay through the nose for all the good things that the company offers. However, I disagree and believe that this stock is most likely undervalued today.

About Entergy Corporation

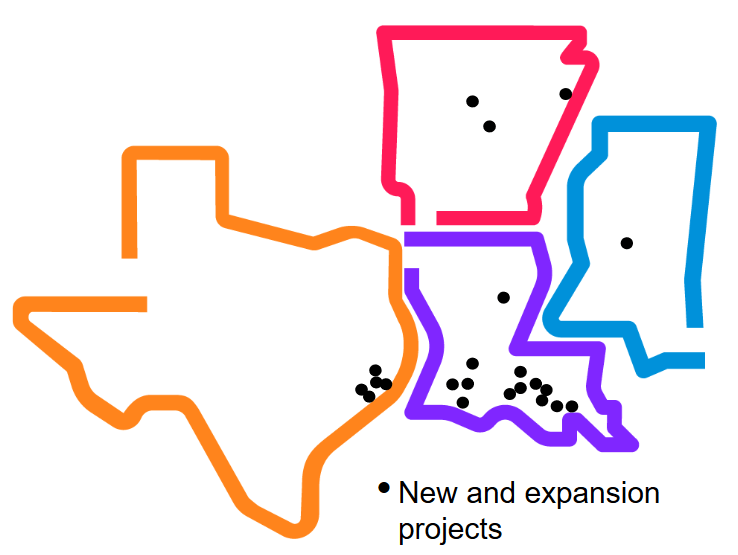

As stated in the introduction, Entergy Corporation is a regulated electric utility that serves the states of Texas, Louisiana, Mississippi, and Arkansas:

{kind=link}

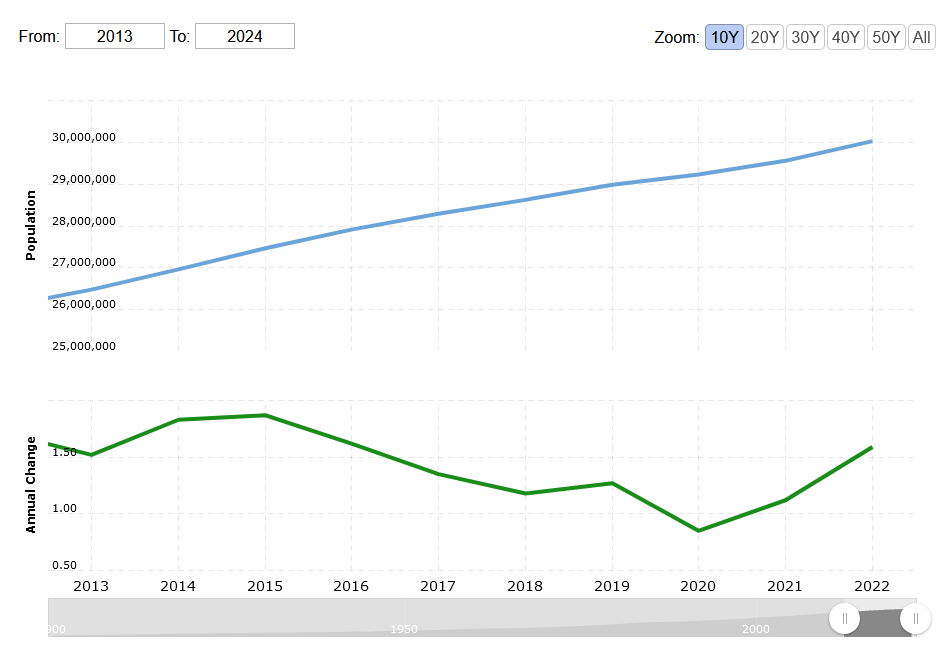

This is one of the more rapidly growing areas of the United States. After all, we have all seen the stories throughout the mainstream media about people leaving areas such as California and Illinois in favor of Texas. Indeed, the population of Texas grew by 1.59% in 2022 alone, which was the continuation of a long trend:

{kind=link}

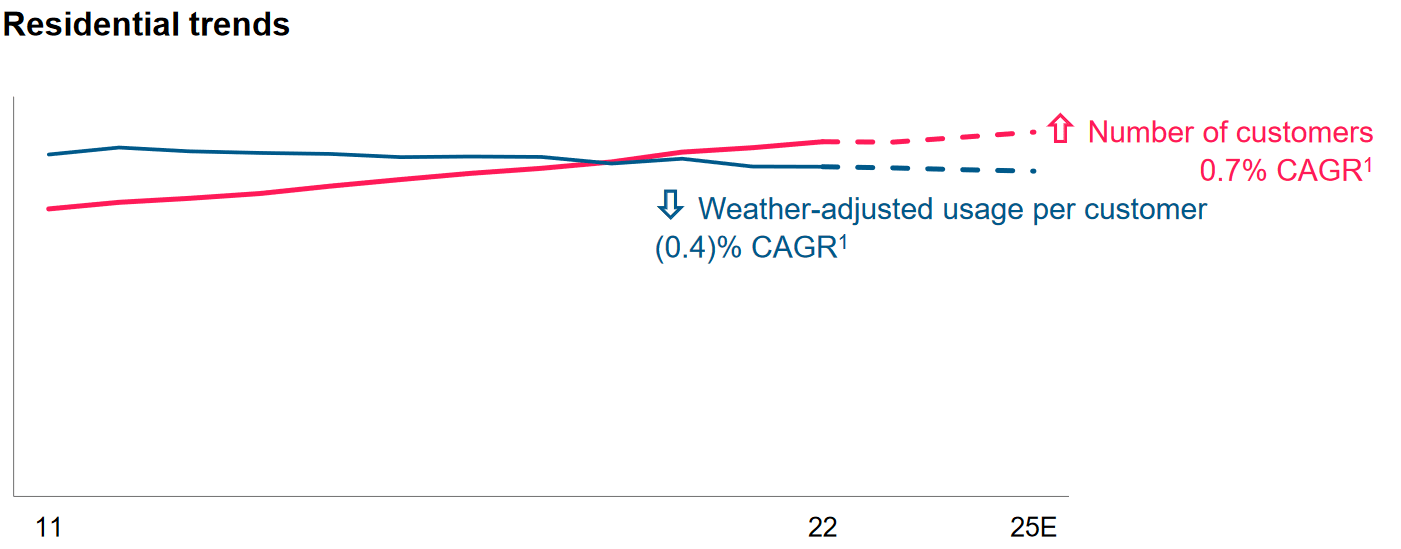

This is important because population growth is one of the only ways that a regulated utility can grow. After all, Entergy is a monopoly whose operations are generally restricted to its service area by regulators. Thus, the only way that it can realistically increase the number of people paying their monthly electric bills is if the population of the service area goes up. This certainly seems to be the case, which gives it an advantage over some other utilities that are servicing areas with less favorable demographics. The company has certainly benefited from this population growth as its customer growth is expected to keep growing going forward, giving it a 0.7% compound annual growth rate over the 2011 to 2025 period:

{kind=link}

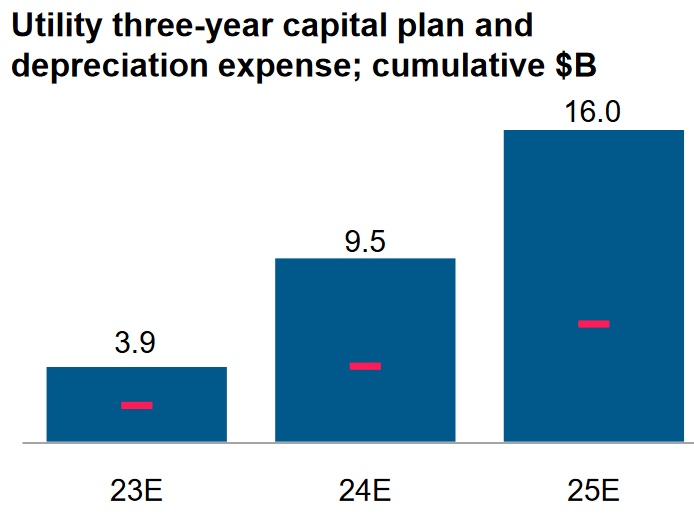

A growing customer base is not the only way through which Entergy can generate profit growth though, which is good as few investors would be satisfied with a 0.7% growth rate. The most important source of growth comes from the expansion of the company's rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any growth of the rate base allows the company to adjust the prices that it charges its customers upward in order to generate that specified rate of return. The usual way through which a company grows its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure. Entergy Corporation is planning to do exactly this as the company recently unveiled a plan to spend $16 billion on this process over the 2023 to 2026 period:

{kind=link}

This should have the effect of increasing its rate base by approximately $7 billion over the period. It is almost certain that at this point some readers will point out that the estimated increase in the rate base is substantially less than the company plans to spend. This is typically due to a few factors. The first of these is depreciation, which means that something put into service in 2023 will be worth less in 2025. As the rate base is the value of the company's assets, the rate base will steadily decrease as a result of depreciation if the company does not continually invest sufficient sums to overcome the depreciation. The second reason for the discrepancy between spending and rate base growth is that Entergy will be retiring some assets during the projection period. Naturally, retired assets have their values removed from the rate base so that will offset some spending. The company's rate base growth should allow it to grow its earnings per share at a 6% to 8% rate, which gives it a total average annual return of 10% to 12% when we factor in the current dividend yield. That is one of the highest total returns currently available in the utility sector, and it is certainly a return that any investor should be reasonably satisfied with.

Renewable Prospects

One of the biggest stories in the financial media over the past several years has been the energy transition and the electrification of the economy. The Inflation Reduction Act of 2022 even included a number of provisions that are meant to encourage this process. At its roots, this refers to the conversion of things that have been traditionally powered by fossil fuels to the use of electricity instead. In the minds of many policymakers, this electricity will be provided by renewable sources such as wind and solar as opposed to coal and natural gas, which currently produce most of the electricity generated in the United States.

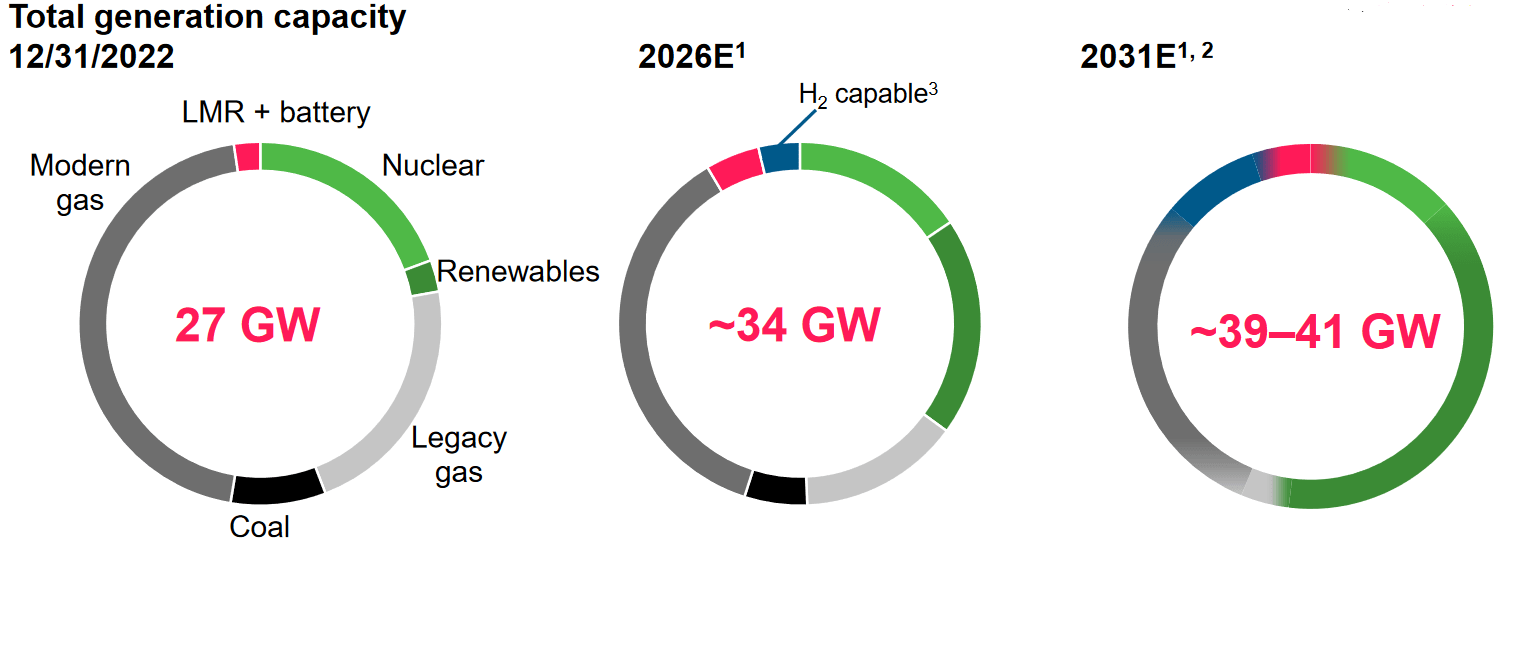

Perhaps surprisingly, Entergy Corporation has been one of the most aggressive utilities at deploying renewable sources of energy. The company currently has 27 gigawatts of generation capacity, most of which is driven by natural gas. As we can see here, it expects to increase its capacity to 39 gigawatts to 41 gigawatts by 2031, with renewables accounting for a sizable percentage of its future capacity:

{kind=link}

This may be surprising for a utility that operates around the Gulf Coast. After all, Texas and Louisiana are generally considered to be the headquarters of the American fossil fuel industry. These are also red states that have not been as aggressively pushing the environmental goals of more progressive regions. However, Texas is perhaps one of the best areas in the United States to deploy renewable energy. After all, Texas is mostly flat, which works pretty well for wind power as it allows for unobstructed breezes. This is the same reason that offshore wind is generally superior to onshore wind. Texas also experiences more sunshine than most other states, which works well for solar power. These positive characteristics mean that Entergy should be able to deploy renewable energy generation with less reliance on storage solutions, such as expensive batteries or natural gas turbines. That results in somewhat lower costs for both the company and its customers than could be delivered by renewables in other areas .

In a few previous articles, such as this one , I discussed how the incredibly large purchasing power of environmental, social, and governance funds can have positive effects on the stock price of any company. This is why we have seen most companies across a variety of industries emphasize their environmental credentials and commitment to diversity in many of their investor presentations over the past few years. Entergy is no exception to this and as it proceeds with its renewable power plans, it could begin to attract the attention of these fund managers and the trillions of dollars that they have under management. This attention could result in a buying wave and push up the company's stock price. It goes without saying that any investor would like to see a company's stock price go up after adding it to their portfolios.

Financial Stability

In the introduction to this article, I stated that utilities like Entergy Corporation tend to enjoy remarkably stable cash flows regardless of economic conditions. This is one of the reasons why these companies are very popular among retirees and other investors that are worried about taking on too much risk. Entergy is certainly no exception to this, as we can see by looking at the company's operating cash flows. Here are the company's numbers over the past ten years:

{kind=link}

As we can clearly see, there was not a great deal of fluctuation despite the fact that there were a great many events that affected the economy over this period. The reason for this is that Entergy Corporation provides a product that is generally considered to be a necessity for modern life. After all, not very many people do not have electric service to their homes or businesses. As such, most people will prioritize paying their electric bills ahead of making discretionary expenses during times in which money gets tight. As I have pointed out in a number of previous articles and blog posts (such as this one ), the average American household is becoming increasingly cash-strapped as the nation has now experienced 24 months of negative real wage growth. There are widespread predictions that the economy will enter a recession later this year, which would pressure the finances of many people even more. In such an economic climate, we want to own companies that are unlikely to be affected much. Entergy is clearly such a company, so having it in a portfolio could help reduce our overall risks should a recession occur.

Debt Considerations

It is always important to analyze the way that a company is financing its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is normally accomplished by issuing new debt to repay the existing debt, which can cause a company's interest expenses to increase following the rollover depending on the conditions in the market. This is something that can be an especially big concern today as interest rates are currently at the highest level that they have been since 2007, so any debt rollover will almost certainly cause interest expenses to increase. In addition to this, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company's cash flows to decline could push it into insolvency if it has too much debt. Although utilities such as Entergy Corporation typically have remarkably stable cash flows, bankruptcies have occurred in the sector so we should not ignore this risk.

One metric that we can use to evaluate a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly owned funds. The ratio also tells us how well a company's equity can cover its debt obligations in the event of a bankruptcy or liquidation event, which is arguably more important.

As of December 31, 2022, Entergy Corporation had a net debt of $26.7962 billion compared to shareholders' equity of $13.2843 billion. This gives the company a net debt-to-equity ratio of 2.02 today. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity |

| Entergy Corporation |

| 2.02 |

| DTE Energy ( DTE ) |

| 1.85 |

| Eversource Energy ( ES ) |

| 1.45 |

| CMS Energy ( CMS ) |

| 1.87 |

| Exelon Corporation ( EXC ) |

| 1.61 |

As we can clearly see here, Entergy Corporation has somewhat higher leverage than many of its peers. This is a concern that I discussed in my last article on the company. This could mean that the company is using an excessive amount of debt in financing its operations, which would result in added risks to shareholders relative to the company's peers.

Dividend Analysis

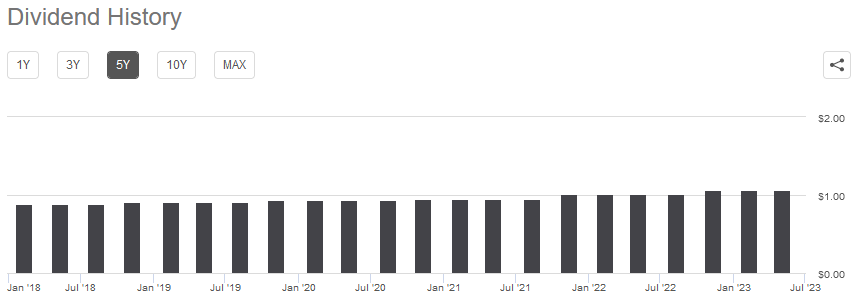

As mentioned earlier in the article, one of the reasons that investors purchase shares of utility companies is that they have a higher yield than many other things in the market. Entergy Corporation is no exception to this as the company's 3.93% yield is quite a bit higher than the 1.57% current yield of the S&P 500 Index (SP500). It is also better than the 2.42% yield of the U.S. Utilities Index ( IDU ). Entergy Corporation adds to its dividend appeal with the fact that the company has a long history of growing its dividend over time:

{kind=link}

The fact that the company increases its dividend on a regular basis is something that is quite nice to see during inflationary periods, such as the one that we are in today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it feel as though we are getting poorer and poorer with the passage of time. The fact that Entergy increases the dividend that it pays out offsets the effect and helps ensure that the dividend maintains its purchasing power.

As is always the case though, it is critical to ensure that the company can actually afford the dividend that it pays out. After all, we do not want to be the victims of a dividend cut as that would both reduce our incomes and most likely cause the company's stock price to decline.

The usual way that we analyze a company's ability to pay its dividend is by looking at its free cash flow. The free cash flow is the amount of cash that was generated by the company's ordinary operations that is left over after it pays all of its bills and makes all necessary capital expenditures. This is the money that can be used for things such as buying back stock, reducing debt, or paying out to shareholders via a dividend. In the twelve-month period that ended on December 31, 2022, Entergy Corporation reported a negative levered free cash flow of $4.133 billion. That was obviously not enough to cover any dividend, but the company still paid out $841.7 million to its shareholders. At first glance, this is likely to be concerning.

However, it is common for utilities to finance their capital expenditures via the issuance of equity and debt, while paying their dividends out of operating cash flow. This is because of the extraordinarily high costs involved in constructing and maintaining utility-grade infrastructure over a wide geographic area. If the company were to rely solely on its free cash flow for the dividend, it would never be able to pay one. During the twelve-month period that ended on December 31, 2022, Entergy Corporation reported an operating cash flow of $2.5855 billion but only paid out $841.7 million in dividends. Thus, the company was able to cover the dividend with a substantial amount of money left over that can be used for other purposes. Overall, Entergy should not have any particular difficulty maintaining or growing the dividend.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to generate a suboptimal return on that asset. In the case of a utility company like Entergy, one metric that we can use to value it is the price-to-earnings growth ratio. This ratio is a modified form of the familiar price-to-earnings ratio that takes a company's forward earnings per share growth into account. A price-to-earnings growth ratio of less than 1.0 is a sign that a stock may be undervalued relative to its earnings per share growth and vice versa. However, there are very few companies that have such a low ratio in today's still overheated market. This is especially true in the utility sector, as most of these companies have fairly low growth rates. As such, the best way to use this ratio today is to compare Entergy to its peers in order to see which company offers the most attractive relative valuation.

According to Zacks Investment Research , Entergy Corporation will grow its earnings per share at a 2.84% rate over the next three to five years. This seems rather low as the company's rate base growth should result in higher earnings per share growth rate than this. Nonetheless, this gives Entergy a price-to-earnings growth ratio of 5.73 at the current price. Here is how that compares to the company's peers:

| Company |

| PEG Ratio |

| Entergy Corporation |

| 5.73 |

| DTE Energy |

| 3.08 |

| Eversource Energy |

| 2.87 |

| CMS Energy |

| 2.50 |

| Exelon Corporation |

| 2.76 |

As we can clearly see here, Entergy Corporation looks incredibly expensive compared to its peers. However, this is using the 2.84% earnings per share growth rate, which is probably lower than what the company will actually deliver. As we discussed earlier, Entergy should be able to grow its earnings per share at a 6% to 8% rate based on its rate base growth. If we assume the midpoint of 7%, we get a price-to-earnings growth ratio of 2.32, which makes the company look incredibly cheap relative to its peers. Even at the low end of the range, 6%, Entergy Corporation has a price-to-earnings growth ratio of 2.71, which is still a bit cheaper than its peers. I am inclined to discount the Zacks estimate in this case and go with the one calculated from the rate base growth, which points to Entergy Corporation being fairly valued at worst. The company is most likely undervalued here, however.

Conclusion

In conclusion, Entergy Corporation appears to have a lot to offer for an investor today. The company boasts one of the highest yields in the utility sector, which when combined with its solid rate base growth should give investors a very respectable total return. The company's focus on renewable energy is also appealing, considering the rising dominance of environmental, social, and governance funds in the market. The biggest concern here is that the company's debt load is a bit high, but its apparent undervaluation makes up for that. Entergy Corporation could be worth purchasing today.

For further details see:

Entergy: This Renewable-Focused Utility Could Be Worthy Of Purchase Today