LGGNY - Enterprise Products Vs. Legal & General - Which Of The 2 Superior Yield Stocks To Choose

2023-12-13 02:47:14 ET

Summary

- Enterprise Products is considered a golden standard for high-yield stocks, but British Legal & General may be a better choice for many.

- Both companies offer a high yield, secure distribution coverage, strong balance sheets, and probable dividend growth of 5% in 2024.

- LGEN's yield and stock appreciation potential are higher but the tax-deferred status of EPD distributions makes it preferable for high-bracket US taxpayers.

Until very recently, I have thought of Enterprise Products ( EPD ) as the best dividend play around (being an MLP, EPD technically pays distributions but for simplicity, we will use "distributions" and "dividends" interchangeably). However, UK Legal & General ( OTCPK:LGGNY ) ( OTCPK:LGGNF ) (LGEN on LSE) may rival this status.

No doubt, my readers know EPD much better than LGEN. Accordingly, I will start with a short description of EPD and proceed with a more detailed review of LGEN. Finally, I will compare them.

But does it make sense to compare a midstream player to a life insurer? The SA audience is uniquely susceptible to yield - just take a look at the most popular articles on the site. In this regard, I believe the comparison is justified.

Enterprise Products

I have published regarding the company several times (here is the latest one ) and a new article about it appears on SA every other day. So, I will limit myself to simply repeating important points from my previous posts.

EPD is the dividend investor's dream. The list of reasons is long and well-known to every EPD holder: the yield is high; distributions are tax-advantaged due to the MLP structure but without its negatives such as incentive distribution rights; distribution coverage is secure, and the balance sheet is strong (~3.0 leverage and A-/BBB+ credit ratings); the payment history is perfect - 25 years of uninterruptible dividend growth at 6+% CAGR; insiders own about one-third of the company and the management is competent and reasonably conservative; its midstream oil and gas assets are irreplaceable as long as humanity uses oil and gas; the company is more exposed to natural gas than to oil which arguably makes it more protected from fossil fuels' multiple foes.

Still, the paragraph above has a major flaw: what is precisely high yield? For example, is a 7% yield high or not? For some reason, EPD is almost always yielding more than 7%.

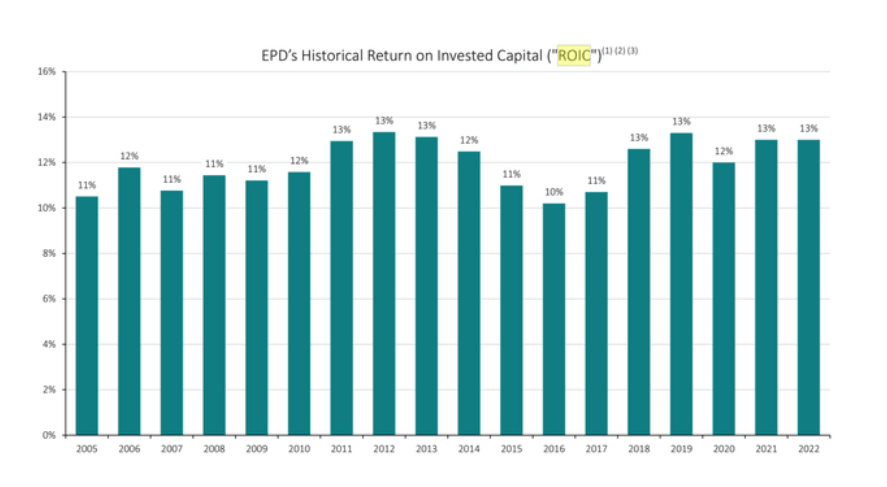

In previous articles, I did the following: based on the average reported EPD's ROIC of 12% (as in the picture below), its financial model, and certain assumptions, I calculated the expected rate of distribution growth and further applied simple math to account for the eventual replacement of fossil fuels.

{kind=link}

EPD

Please note that I do not take any position regarding this issue. But when half of the voting population thinks that fossil fuels must be replaced, it is prudent to account for this eventuality rather than dismiss it entirely.

In the end, I came up with a threshold of 7.5% yield. If EPD trades at a yield higher than 7.5%, it is a buy. Otherwise, it is not. We can say that a 7.5% yield is an estimate of EPD's fair value as long as the company sticks to its existing financial model.

Since it is only an estimate, we need to add a margin of safety. Here is my final guideline: buy EPD when its yield equals or exceeds 8%.

This guideline triggers counterarguments from two groups of investors. Optimists believe that EPD's future will be better than its past and typically indicate some future projects that should change EPD's economics as quantified in its ROIC. Another group of investors simply thinks that a 7% yield is good enough to bother. I responded to both counterarguments in my previous posts and will not discuss them again here.

Opportunities to buy EPD at yields equal to or above 8% are rather scarce and usually present themselves when commodities drop. But let us assume it is possible and that a 5% annual growth rate for distributions is likely in line with the last several years.

This is what we can expect from EPD. And now it is time to turn our attention to LGEN.

What is Legal & General?

It is a venerable UK company (started in 1836) that is usually described as a life insurer. It is correct but tells only half of the story.

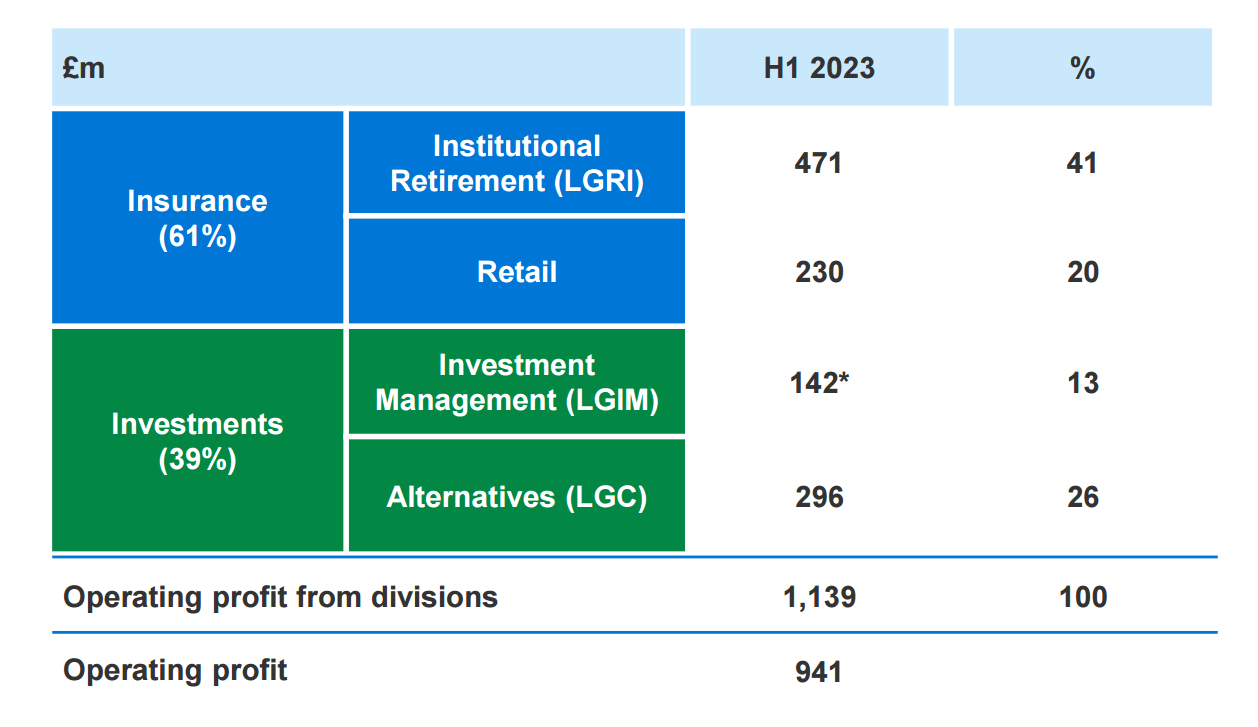

The company has experienced many transformations during its long history and currently consists of 4 well-defined divisions/segments:

- L&G Retirement Institutional ("LGRI") is the biggest division doing exclusively Pension Rist Transfers ("PRT") which are also called group annuities. A company with a defined benefits plan can offload pension obligations by transferring related assets and liabilities to LGRI. LGEN is a PRT market leader in the UK with a ~25% market share. It is also expanding into the US, Canada, and the Netherlands - the countries with the biggest defined benefits plans.

- Retail is the division writing individual annuities and life insurance policies that is also engaged in other financial services - primarily issuing rather unique mortgages to people in or close to retirement. It also controls several Fintechs. Retail is doing business mostly in the UK but also in the US.

- L&G Investment Management ("LGIM") is the UK's biggest asset manager with ~ £1.2T AUM with a third of them being international. Most assets are defined benefits and defined contributions pension plans split between traditional (both active and passive) stock and bond funds and ETFs. It also manages LGEN's internal investments.

- L&G Capital ("LGC") is involved in alternative investing such as various forms of real estate (it owns one of the bigger UK builders and several other real estate businesses), renewables, private credit, etc. The division is growing quickly and helps the other three divisions by manufacturing alternative assets for both internal purposes (alts are on LGRI and Retail balance sheets) and third parties.

Please take a look at the recent H1 2023 results to size divisional inputs:

{kind=link}

LGEN

The current high-rate environment is favorable for annuities and adversarial for LGIM as AUM shrinks due to migration to cash and depressed bond values.

Group and individual fixed annuities are the most important products for LGEN but the company is different from its US peers such as Apollo's ( APO ) Athene, KKR's ( KKR ) General Atlantic, F&G Annuities & Life ( FG ), and American Equity ( AEL ).

First, group annuities business dwarf individual annuities. Secondly, LGEN offers many other financial services in addition to annuities. Thirdly, while having an internal alt asset originator LGC, it is less reliant on alternative assets and private credit.

LGEN's market cap is about £14.5B which makes it comparable to Athene. However, due to Apollo's support, Athene is more aggressive and nimble simultaneously. In its presentations, LGEN compares itself with BlackRock ( BLK ) and even Blackstone ( BX ) but I doubt these comparisons have merit.

The company's leverage is easily manageable. It is reasonable in size (~ £4.3B) and consists mostly of £3.7B subordinated bonds that mature from 2045 to 2064 and pay interest within a range of 3.75-5.55%.

Insiders own about 1% of LGEN.

Easy accounting

The life insurance industry is the best proof that profit and equity are accounting concepts that cannot be always grasped intuitively.

European insurers report under two standards - IFRS for financial reporting and Solvency II ("SII") for regulatory purposes similar to GAAP and SAP (Statutory Accounting Principles) in the US. Regulators developed both SAP and Solvency II to make sure that insurers will remain solvent, i.e. have enough capital to pay claims even at the time of stress. However, while SAP is relatively rarely mentioned in investment posts, it is impossible to cover a European insurer without referring to SII. A short accounting tour that follows represents a gross oversimplification of a complicated SII regime.

SII is concerned only with insurers' balance sheets. It defines an equivalent to equity called "Own Funds" that is split into two parts - SCR (solvency capital requirements) and surplus. Any insurer in decent shape has to have its Own Funds exceeding SCR. The ratio of Own Funds to SCR (SCR ratio) is the best measure of an insurer's balance sheet strength. LGEN's balance sheet is very strong as indicated by the SCR ratio of 230%.

This is important for our story as the ability to pay dividends depends on the SCR ratio more than on anything else. Only surplus (i.e. Own Funds above SCR) can be paid out in principle.

While SII accounting is complex at times, the concepts of SCR and surplus should be natural for most of us. Say, you are employed but may lose your job. You have to have cash (or T-bills) equal at least to your several months of expenses until you find a new job. This is your personal SCR that you cannot spend or invest in illiquid or risky assets. Your savings on top of it is your personal surplus that can be spent or invested. Regulators require insurers to have SCR sufficient to pay claims for a year even under dire circumstances.

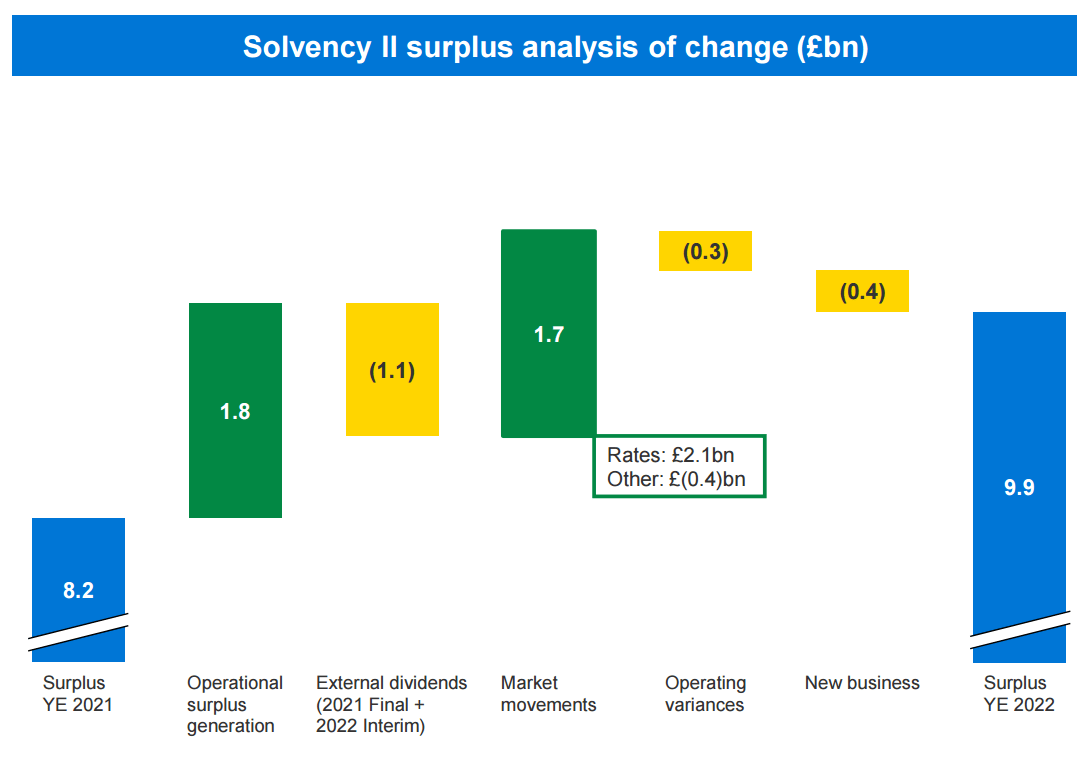

Every year LGEN enters into multiple life insurance/annuities contracts with their long-duration cash flows. The present value of these cash flows is the main source of the insurer's capital generation. Unfortunately, new insurance contracts require an initial outlay of capital due to expenses (such as agents' commissions) and insurance reserves. These outlays are called new business strain. The slide below illustrates the surplus evolution for LGEN in 2022:

{kind=link}

LGEN

LGEN started 2022 with a surplus of £8.2B. Booked business increased this surplus by £1.8B but dividends paid required £1.1B. New business strain cost £0.4B. Two other items (Market movements and Operating variances) are less important for our purposes as they fluctuate from year to year depending on outside factors. Please note that operational surplus generation minus new business strain was more than dividends paid (1.8-0.4=1.4>1.1). It means that the company increased its ability to pay dividends in 2022.

Below is the most recent SII balance sheet on June 30, 2023:

LGEN

A surplus of £9.2B should be compared with annual expected dividends of ~£1.2B. It is rather obvious that the LGEN's dividend is safe for at least the next several years.

To finish this section, I have to mention that IFRS accounting was dramatically changed in 2023 as the IFRS 17 standard became mandatory for insurers. It makes 2023 and restated 2022 incomparable to previous years.

Valuations

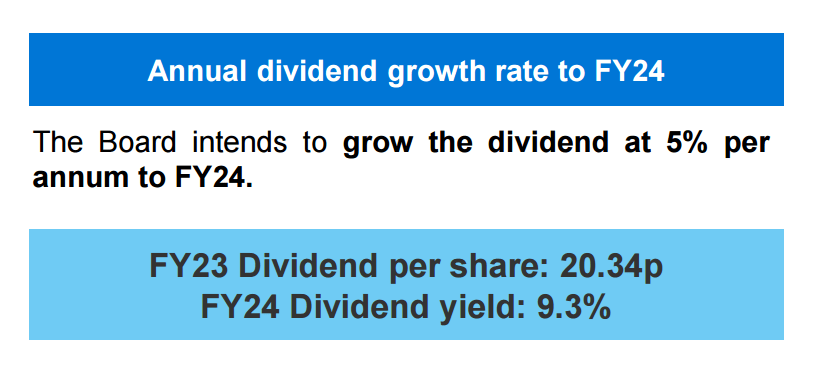

LGEN's policy is to grow dividends at 3-6% annually. Even though the Board has not made final decisions regarding 2023 and 2024 dividends, the company let everybody know its firm intentions:

{kind=link}

LGEN

So, it will be 20.34p per share for FY2023 and 21.36p for FY2024. The company pays dividends twice a year - an interim dividend in August of the same year and a final dividend in April of the next year.

If the next year's dividend is 20.34p and we assume 3% as the long-term dividend growth rate (both numbers are on the low side since the company will pay a higher interim dividend in 2024 and dividends have grown at CAGR of 8% since 2013), the simple dividend discounting model produces a value of 20.34/(10% - 3%) ~291p vs ~240p of LGEN's current price.

The same equation can be interpreted differently: LGEN's fair value corresponds to a 7% dividend yield while it is trading at 20.34/240~ 8.6% yield. Today's price also corresponds to a 2024 yield of 21.36/240 ~ 9.0%.

I have also valued LGEN using SOTP to avoid being solely dependent on the archaic dividend discounting model. My calculations (that I will not publish here) produced LGEN intrinsic value of £3.03 in line with our calculations above.

Besides the strong Solvency II ratio, there is another reason to be optimistic about LGEN's dividend. The company's main business of group annuities is booming with record PRT inflows in 2023 and an abundant pipeline.

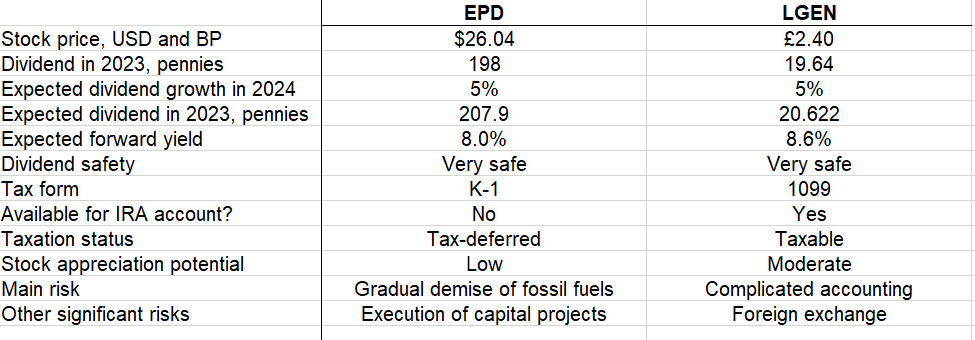

EPD and LGEN dividends comparison

Here is a table summarizing dividend cases for both companies:

{kind=link}

Author

Both companies appear comparable. LGEN has a higher yield and, in my opinion, better appreciation potential. EPD's distributions are preferable for US taxpayers due to their tax-deferred status and there is no currency exchange risk.

Taxation is a big consideration here. High-bracket US taxpayers should prefer EPD. For low-bracket US taxpayers, both companies appear more or less equivalent. For foreign taxpayers, LGEN should be preferable in many cases, since MLP's distributions are often taxed high abroad.

Please note that the UK does not have a withholding tax and you will receive your dividend intact without any deductions.

I suggest buying LGEN on LSE instead of dealing with US OTC markets. The liquidity is much better without any hidden expenses. However, when purchasing you will have to pay 0.5% British stamp duty which will be added to your commissions. At this point, I do not know if LGEN's dividends are qualified for US tax purposes. My messages to LGEN and my broker remain unanswered. Commenting from those who know it will be welcome.

Finally, I suggest using Interactive Brokers for buying LGEN because of two reasons. The first is obvious - lower commissions. The second is less obvious and not applicable now but may become relevant in the future. IB has unusually low margin rates. If interest rates get low in the future, you can borrow British pounds and hedge your foreign currency risk at a small cost. I have often done it, especially when USD was weak. Currently, BP/USD rate stands at ~1.26 which is close to its average value over the last several years.

For further details see:

Enterprise Products Vs. Legal & General - Which Of The 2 Superior Yield Stocks To Choose