MCN - EOI: A Solid Equity CEF With A Fully Covered 8.39% Distribution Yield

2023-11-20 18:47:41 ET

Summary

- The Eaton Vance Enhanced Equity Income Fund offers a current yield of 8.39%, which is not particularly impressive compared to similar funds.

- The fund's recent performance has not been impressive, with shares down 6.62% compared to a 0.46% decline in the S&P 500 Index.

- The fund utilizes a covered call strategy and has a portfolio heavily exposed to mega-cap technology stocks.

- The fund's distribution yield appears to be fully covered by the performance of its underlying portfolio, so there is little danger of a near-term cut.

- The fund is trading at an attractive discount on net asset value right now.

The Eaton Vance Enhanced Equity Income Fund ( EOI ) is a closed-end fund, or CEF, that is designed to provide a very high level of current income to its investors. It is reasonably effective in this task, as the fund boasts an 8.39% yield at the current price. Unfortunately, this yield is not particularly impressive compared to that of other closed-end funds that utilize a similar strategy of writing covered calls against the stocks in their portfolio. I pointed this out in a recent article on a similar fund. We can also see this here, as this table shows the current yield of this fund and some of its peers:

| Fund |

| Current Yield |

| Eaton Vance Enhanced Equity Income Fund |

| 8.39% |

| Eaton Vance Enhanced Equity Income Fund II ( EOS ) |

| 7.72% |

| BlackRock Enhanced Equity Dividend Trust ( BDJ ) |

| 8.94% |

| BlackRock Enhanced Capital and Income Fund ( CII ) |

| 6.73% |

| Madison Covered Call and Equity Strategy Fund ( MCN ) |

| 10.29% |

We can see that the Eaton Vance Enhanced Equity Income Fund’s current yield only represents the median of this peer grouping, which may not make it the most appealing fund among those investors who are determined to get as much money as possible from the assets in their portfolios. However, this fund does do much better than its sister fund from Eaton Vance and both funds have very similar strategies and holdings so this one is almost certainly the more attractive of the covered call funds from this fund house.

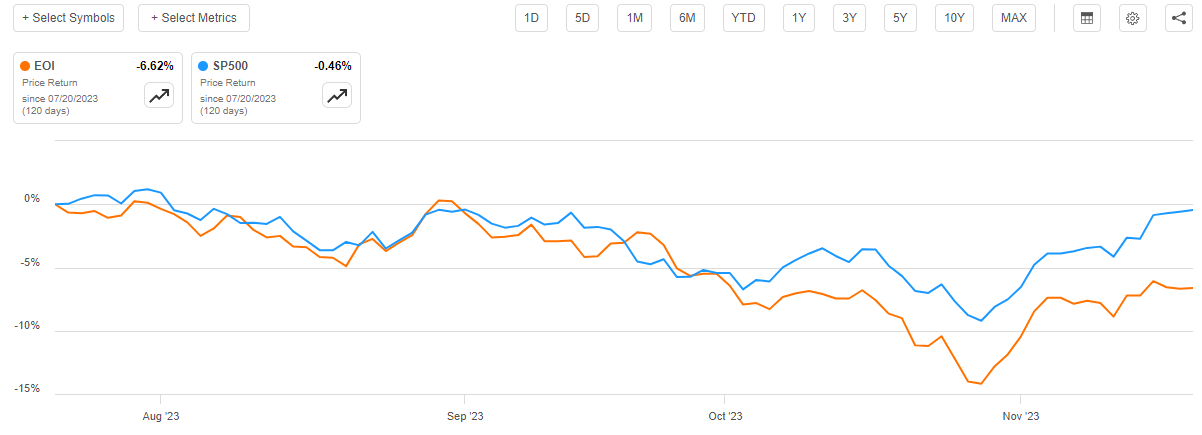

As regular readers may recall, we last discussed this fund in mid-July. At that time, the fund had a much lower yield, so we can conclude that the share price performance has not been particularly impressive. This is certainly the case, as the fund’s shares are down a massive 6.62% compared to a 0.46% decline in the S&P 500 Index ( SP500 ):

{kind=link}

The actual value of the assets held by this fund has held up much better, however. The fund’s net asset value per share is only down 1.60% over the same period. As such, it appears that the share price decline that we witnessed here has been unjustified based on the actual performance of the assets in the fund. This could create an opportunity for savvy investors to accumulate shares at a very reasonable price, which we will certainly want to investigate.

About The Fund

According to the fund’s website , the Eaton Vance Enhanced Equity Income Fund has the primary objective of providing its investors with a very high level of current income. This is somewhat unusual for an equity fund considering that common equities are not particularly attractive in terms of yield. After all, the S&P 500 Index ( SPY ) only yields 1.44% at the current price. The traditionally high-yielding utility sector ( IDU ) only yields 2.82% right now, which is also less than impressive. In fact, an ordinary money market fund boasts a higher yield than any American common equity index right now except for the Alerian MLP ETF ( AMLP ). As such, no ordinary equity fund is going to be able to match a fixed-income fund in terms of yield. For what it is worth, this fund is no exception to this as it is fairly easy to find fixed-income closed-end funds with yields well above 10% in the current environment.

However, the Eaton Vance Enhanced Equity Income Fund is not a straight equity fund. It does not simply buy equities and collect dividends from them. Rather, as the name of the fund suggests, it combines an options strategy with its equity holdings in order to generate a high effective yield from its portfolio. The fund’s website does not provide a description of its strategy, much to my annoyance. However, the fact sheet does provide such information. Here is what that document states on this matter:

The Fund invests in a portfolio of primarily large- and midcap securities that the investment advisor believes have above-average growth and financial strength and writes call options on individual securities to generate current earnings from the options premium.

This fund is essentially running a covered call strategy, in which it holds the stocks against which it writes options. The premiums that it receives from the call-writing strategy act as a sort of synthetic dividend, and the yields can be quite high when written on the correct stock.

This fund differs somewhat from most of Eaton Vance’s other option-income funds because it does not write naked call options. For example, funds like the Eaton Vance Tax-Managed Diversified Equity Income Fund ( ETY ), which I discussed last week, hold a portfolio consisting of about 60 or so common stocks and then write options against the S&P 500 Index. That fund does not own the index, so technically it is writing naked calls that could expose it to unlimited losses. The Eaton Vance Enhanced Equity Income Fund is not doing that. This fund owns the stocks against which the options are written, so the worst-case scenario here is that the fund will have to sell some of the stocks that it already owns. This is a much safer strategy overall, and it could make this fund a somewhat better choice for those investors who want to keep their money as safe as possible while earning the money that they need to pay their bills.

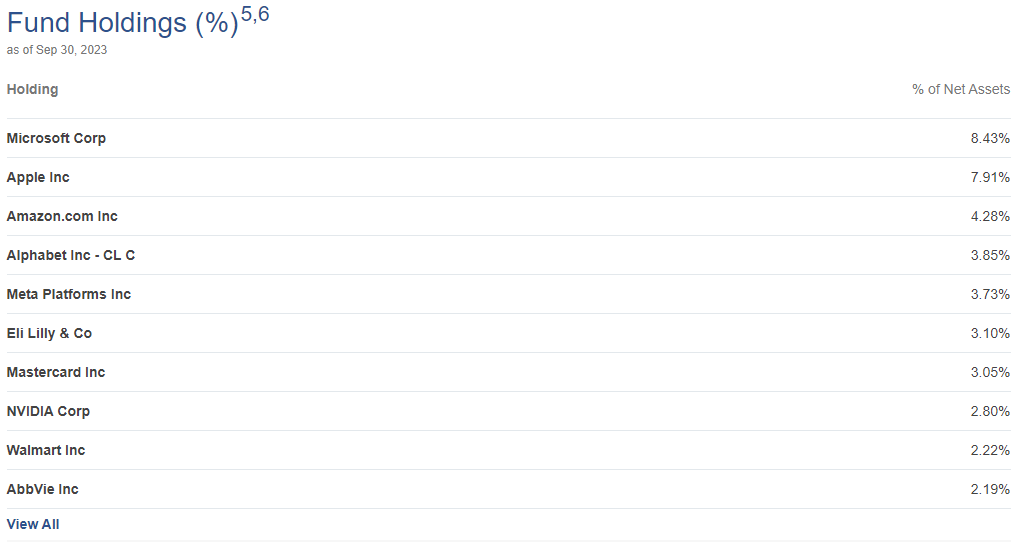

One of the characteristics of Eaton Vance’s equity closed-end funds is that their portfolios tend to be very heavily exposed to the “Magnificent 7” mega-cap technology stocks that have been responsible for pretty much all of the gains in the S&P 500 Index so far this year. This fund is certainly no exception to that, which we can see here:

{kind=link}

We can see that this fund includes six of the “Magnificent 7” stocks among its top holdings. The only exception is Tesla ( TSLA ), which is not included in the fund’s largest positions. That company is also not included in the top positions of most of Eaton Vance’s other closed-end funds either. It is uncertain why this is the case, as Tesla has outperformed all of the “Magnificent 7” stocks year-to-date except for Meta Platforms ( META ) and NVIDIA ( NVDA ). Maybe it is because Tesla is a much more capital-intensive business than any of the other stocks in the category and there are more concerns about its valuation than an all-digital company like Meta.

A look at this portfolio alone reveals that the Eaton Vance Enhanced Equity Income Fund is not trying to make money via the collection of dividends. After all, most of the companies in the fund’s largest positions list either do not pay dividends or have such a small yield that the dividend is meaningless. Here are the current yields of all ten stocks on the list above:

| Company |

| Current Yield |

| Microsoft Corp ( MSFT ) |

| 0.81% |

| Apple ( AAPL ) |

| 0.51% |

| Amazon.com ( AMZN ) |

| N/A |

| Alphabet Inc ( GOOG ) |

| N/A |

| Meta Platforms |

| N/A |

| Eli Lilly and Company ( LLY ) |

| 0.76% |

| Mastercard Inc. ( MA ) |

| 0.57% |

| Nvidia Corp |

| 0.03% |

| Walmart Inc. ( WMT ) |

| 1.47% |

| AbbVie Inc. ( ABBV ) |

| 4.48% |

The only one of these stocks that is reasonably competitive with other options in the yield category is AbbVie, and even it is not competitive with an ordinary money market fund right now. Thus, this fund is clearly not trying to earn money by collecting dividends. For its part, though, this fund does not claim to have any sort of preference for dividend-paying securities like Eaton Vance’s other funds that hold almost identical portfolios do.

As the fund’s description states, the Eaton Vance Enhanced Equity Income Fund derives the majority of its income from writing covered call options against the stocks in its portfolio. In order for this strategy to work, the fund will want to have stocks that have high implied volatility and high option premiums. Most of the stocks above fit this description. When we combine that with the fact that the “Magnificent 7” stocks have been responsible for essentially all of the gains in the S&P 500 Index year-to-date, it makes a great deal of sense for this fund to have the portfolio that it does. In short, the fund’s portfolio right now works very well to maximize investment profits considering its strategy.

There have been a few changes to the fund’s holdings since the last time that we discussed this fund. In particular, JPMorgan Chase ( JPM ), PepsiCo ( PEP ), and Accenture ( ACN ) have all been removed from the largest positions list. In their place, we have Nvidia, Walmart, and AbbVie. This actually increased the weighting that this fund has to the big technology companies, but the weighting of the S&P 500 Index to these companies has also been increasing over the course of this year. The fund’s fact sheet states that the fund’s allocation to the information technology sector is 27.84% right now, which is slightly above the 27.46% weighting of the index:

Fund Fact Sheet

However, the fact sheet’s weightings seem to be somewhat out of date. The Index in question is, according to the fact sheet’s footnotes, the S&P 500 Index. As of November 17, 2023, the information technology sector is 29.14% of the S&P 500 Index. The increase in this sector is almost certainly due to the performance of the “Magnificent 7” technology stocks over the past few months. It is reasonable to assume that this sector’s weighting has also increased in this fund as the portfolio does contain fairly high weighting to six of the seven companies whose outsized performance has been responsible for the growing representation of the information technology sector in the broader market index. However, the fact sheet is dated “3Q2023,” so presumably it is only offering a snapshot of how this fund looked at the end of September. The website’s information also carries the same date.

Despite the fact that three of the fund’s largest positions were replaced since the last time that we discussed this fund, the Eaton Vance Enhanced Equity Income Fund does not have an especially high annual turnover rate. The fund’s annual turnover sits at 50.00%, which is relatively in line with that of most equity closed-end funds. Indeed, it is actually a bit lower than many of them. Thus, the conclusion that we can draw is that this fund is not conducting a significant amount of trading activity. This is nice because this helps to hold the fund’s trading expenses down. After all, the more money that the fund has to spend on trading stocks, the higher the return it needs to generate in order to offset its costs and still provide a satisfactory return to investors.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Enhanced Equity Income Fund is to provide its investors with a very high level of current income. In order to accomplish this objective, it invests in a portfolio of common stocks that do not have particularly impressive yields per se. However, the fund writes call options against the stocks in its portfolio in order to receive option premiums that act as synthetic dividends. In some cases, the premiums can represent a significant percentage of the stock price, which causes the artificial yields to be quite attractive. In addition, the fund only writes options against part of its portfolio (44% as of September 30, 2023) so it is still able to generate capital gains from the non-overwritten securities. The realized capital gains, collected option premiums, and whatever dividends it manages to get go into a pool of money that then gets distributed to the fund’s investors, net of the fund’s own expenses. This allows the fund to boast a respectable distribution yield in most market climates.

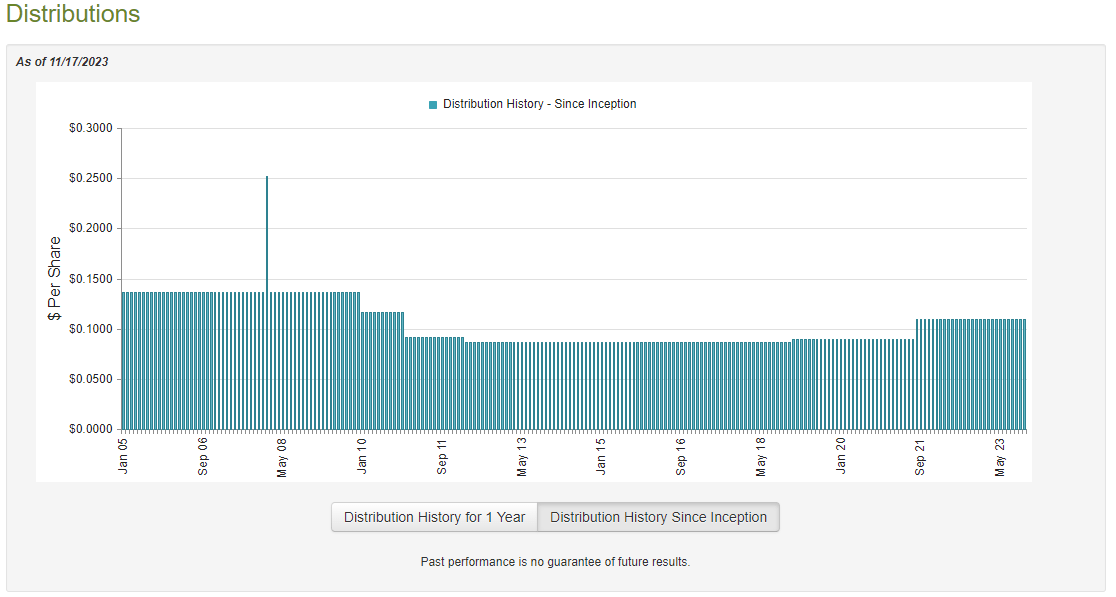

The Eaton Vance Enhanced Equity Income Fund currently pays a monthly distribution of $0.1095 per share ($1.314 per share annually) to its investors, which gives it an 8.39% yield at the current price. This is higher than most pure equity investments can deliver, but it is admittedly not very impressive compared to other covered call funds. The fund has generally proven to be very consistent with respect to its distribution over the years, though. We can see this here:

{kind=link}

As we can see, the fund has generally increased its distribution over the past decade. This is much nicer than Eaton Vance’s other option-income funds, such of which have had to cut their distributions in response to losses that they took in the reversal of the long-standing loose monetary policy last year. We certainly want to have a close look at the finances of this fund though, since it seems a bit unlikely that it would be able to avoid losses from last year’s bear market. This is especially true since a covered call strategy only provides partial protection against a market decline (the premiums offset some of the share price declines).

Unfortunately, we do not have an especially recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund’s most recent financial report corresponds to the six-month period that ended on March 31, 2023. As such, it is nearly eight months old at this point and will not provide us with any insight into the fund’s performance during the spring or the summer months of 2023. This is a disappointment because a great deal happened during that period, including a rather volatile market that included a period of euphoria characterized by incredible optimism that lasted until early July before turning into a period of rising yields and generally declining asset valuations. The first half of the year could have provided this fund with the opportunity to realize some capital gains, especially from the mega-cap technology companies in its portfolio. It could have had some success at this during the period covered by the report too, but the euphoria did not really get going until the spring months, which are after the end date of the most recent financial report.

During the six-month period, the Eaton Vance Enhanced Equity Income Fund received $4,799,344 in dividends from the assets in its portfolio. It had no income from any other source, so this number comprises the entirety of the fund’s reported investment income. It paid its expenses out of this amount, which left it with $1,393,061 available for the shareholders. As might be expected, that was nowhere close to enough to cover the distributions that the fund paid out during the period. The fund’s distributions totaled $26,423,024 over the six-month period, so the fund paid out far more than its net investment income. This could be concerning at first glance.

However, the fund does have other methods through which it can obtain the money that it needs to cover the distributions. For example, the fund might have been able to realize capital gains from the common stocks in its portfolio that can be paid out to the shareholders. The fund also brings in a significant amount of money from its option-writing strategy that is not included in net investment income but obviously does represent money that can be paid out to its shareholders. Fortunately, the fund did manage to enjoy some success at getting money via these alternative methods during the period. It reported net realized gains of $16,771,560 and had another $57,374,475 in net unrealized gains.

Overall, the fund’s net assets increased by $52,266,887 after accounting for all inflows and outflows during the period. This is exactly what we would like to see as an increase in net assets means that the fund did manage to cover its payouts over the period.

There are some reasons to believe that this fund has managed to cover its distribution during the period that followed the end of this reporting period as well. As we can see here, the fund’s net asset value per share is up 6.08% since April 1, 2023:

{kind=link}

This means that the fund’s assets have generated sufficient returns to both cover all of the distributions that the fund has paid out since the end date of the most recent financial report and give it a significant amount of money left over. Thus, unless some event causes the mega-cap technology sector to begin falling rapidly, the fund’s distribution is probably reasonably sustainable right now.

Valuation

As of November 17, 2023 (the most recent date for which data is currently available), the Eaton Vance Enhanced Equity Income Fund has a net asset value of $16.58 per share but the shares currently trade for $15.82 each. This gives the fund a 4.58% discount on net asset value at the current share price. That is in line with the 4.65% discount that the shares have had on average over the past month. Thus, the current price appears to represent a reasonable entry point for someone who wants this fund.

Conclusion

In conclusion, the Eaton Vance Enhanced Equity Income Fund appears to be a reasonably solid investment for anyone who is seeking to earn a very high level of income from the assets in their portfolio but does not want to give up the potential capital appreciation available from investing in common equities. The fund’s 8.39% yield appears to be well covered by the portfolio’s performance and the current share price represents a pretty reasonable discount on net asset value.

The biggest risk here is that the Eaton Vance Enhanced Equity Income Fund is very heavily exposed to the market performance of a handful of large technology companies, but the same could actually be said for the S&P 500 Index, so the relative risk is probably not that bad. Overall, this fund looks like a good investment right now if you are willing to accept a slightly lower yield than some peers offer.

For further details see:

EOI: A Solid Equity CEF With A Fully Covered 8.39% Distribution Yield