XLK - EOS: Solid Performance From This Covered Call Fund With An Attractive Discount

2023-12-27 11:23:20 ET

Summary

- Eaton Vance Enhanced Equity Income Fund II has had a strong year of performance due to its heavy allocation to the technology sector.

- The fund's share price has not kept up with its underlying portfolio performance, leading to a discount in its trading price.

- Despite concerns about the tech sector being overvalued, there is still potential for earnings growth in these companies, making the fund a fairly attractive option.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Enhanced Equity Income Fund II ( EOS ) has been having a strong year of performance thanks to its heavy emphasis on the technology sector. Six of the Magnificent 7 names are top ten positions, with the top five comprised of five of them for a nearly 40% allocation. In fact, the performance for EOS on a NAV performance basis has been so strong that's why the fund has started to trade at a discount. The share price simply hasn't kept up with the fund's underlying portfolio performance.

With that, it could be the wrong time to consider a fund so heavily invested in the Mag 7 names if an investor believes they've run too far at this point. However, there is also an argument to be made that it could still be worthwhile, too. After all, tech has essentially only clawed back what it lost in 2022, and this recovery brings it back to about where we were two years ago. Earnings are expected to grow, and quite rapidly, in several of these names, so what is expensive today might not be expensive next year or a few years down the road.

In addition, EOS' discount is still attractive at this time - as it trades at a similar discount level as it was in our previous update earlier in 2023. Since then, the fund's performance has been able to outpace the S&P 500 despite being a covered call-writing fund. However, that would be again thanks to the massive Mag 7 exposure.

EOS Performance Since Prior Update (Seeking Alpha)

The Basics

- 1-Year Z-score: -0.55

- Discount: -4.99%

- Distribution Yield: 7.40%

- Expense Ratio: 1.09%

- Leverage: N/A

- Managed Assets: $997.6 million

- Structure: Perpetual

EOS' primary investment objective is "to provide current income, with a secondary objective of capital appreciation." To achieve this, "the fund invests in a portfolio of primarily large- and mid-cap securities that the investment advisor believes have above-average growth and financial strength and writes call options on individual securities to seek to generate current earnings from the option premium."

They typically target around 50% of their portfolio being overwritten. The less the portfolio is overwritten, the more positions are left to "fly higher" in a bull market. Utilizing a covered call strategy in a bull market can generate lagging returns relative to a non-option strategy fund. As overall markets appreciate, the underlying positions can either get called away. Managers may also choose to close the position, which can result in some losses.

The fund's latest fact sheet reported that they are right around their target at a 49% overwrite. They wrote options that were, on average, 24 days out, and they allowed some upside as they wrote them at an average of 7.2% out-of-the-money.

Performance - Running Hot But Discounted

When looking at the performance for EOS as we get set to close out 2023, it certainly stands out as one of the best performing of the entire closed-end fund space. The table below shows the rankings in terms of total NAV return performance according to CEFConnect's data through November 2023.

| Ticker |

| Total NAV Return |

| Total Share Price Return |

| ( TWN ) |

| 48.82% |

| 42.57% |

| ( CEE ) |

| 36.19% |

| 8.72% |

| ( PDX ) |

| 35.83% |

| 41.41% |

| ( STK ) |

| 30.41% |

| 43.75% |

| ( QQQX ) |

| 30.14% |

| 17.66% |

| ((EOS)) |

| 30.09% |

| 20.38% |

Unsurprisingly, Columbia Seligman Premium Technology Growth Fund ((STK)) and Nuveen NASDAQ 100 Dynamic Overwrite Fund ((QQQX)) are also top performers as they are also tech-heavy funds or, in the case of STK, specifically a tech fund. Interestingly, they are also call writing funds like EOS. These are funds that only have partial overwrites, though, and that likely helped the results as not all of the portfolio would run up against a 'ceiling' in terms of potential appreciation.

Since the end of November, the market has only continued its upward climb from the depths of the latest lows in October.

YCharts

Despite this rapid climb, we can see in the above that the share price is being left behind this year. That's resulted in EOS moving and remaining to trade at a discount most of this year. A discount isn't that unusual for closed-end funds, and this discount is even starting to become normal now for EOS if we were to look over the last year.

That being said, over the longer term, EOS is looking like it is trading below the average of the last decade. Most of this average was helped out and lifted by the premium it began to trade at in 2018. That flirting with a mostly premium valuation throughout most of the last five years or so might not return, but even the current level suggests we are at a reasonable valuation to consider EOS.

YCharts

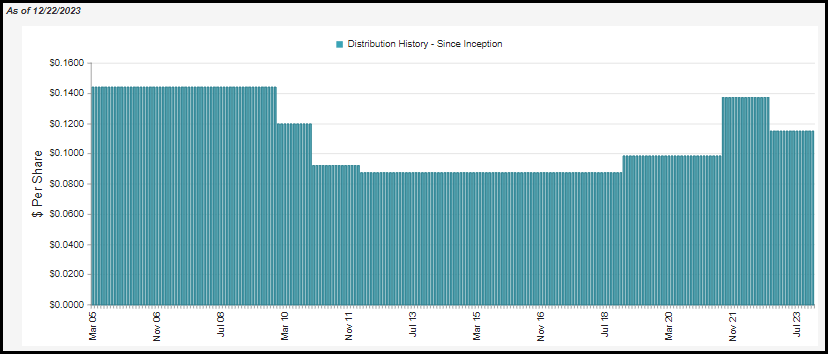

Distribution - Looking Reasonable And Attractive

As we mentioned in the previous update, one of the reasons for seeing this discount open up is likely the distribution cut the fund had in 2022. Most of the Eaton Vance equity funds were cut in 2022 as the market sank to a bear market level. As these funds all rely significantly or entirely on capital gains to fund their distributions, these cuts made sense, in my opinion.

Additionally, in defense of EOS, the fund also raised its distribution in 2021. When they cut in 2022, it was still higher than the previous level.

{kind=link}

EOS Distribution History (CEFConnect)

Doubly, in their defense, at a NAV distribution rate of 7.04% now, I wouldn't be shocked to see the fund increase its distribution again. That is, assuming the economy doesn't fall off the rails as we head into 2024.

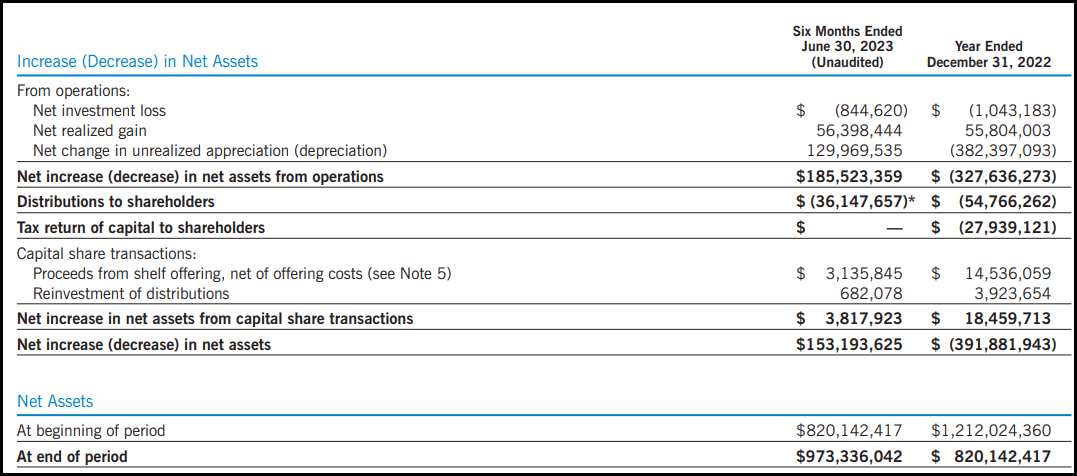

EOS is one of those funds that has a negative net investment income. This happens when the fund doesn't generate enough interest/dividends to pay its operating expenses. This results in a scenario where the entire distribution - and, in a way, the fund's expenses - are reliant on capital gains. In this semi-annual report, we can see that it wasn't a problem to generate those needed realized capital gains for the first six months of the year .

{kind=link}

EOS Semi-Annual Report (Eaton Vance)

Given that the NAV has risen only further since this report, the back half of the year is looking equally as well-covered.

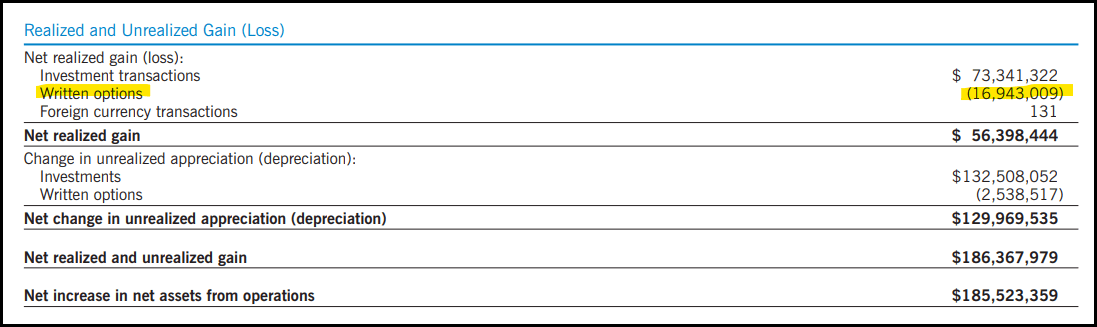

That said, the fund had been actually working against its covered call-writing strategy. That is to say, the fund's written options contributed to realized losses in the first half of the year; therefore, not only did the fund's underlying portfolio need to generate sufficient realized gains to cover the fund's expenses, but also its losses due to its options writing strategy.

Losses from writing covered calls can occur when the fund closes the options position at a loss instead of having the position called away. Sometimes, that's the better result than having a position called away if it is believed it will continue to have upward momentum.

{kind=link}

EOS Realized/Unrealized Gains/Losses (Eaton Vance (highlights from author))

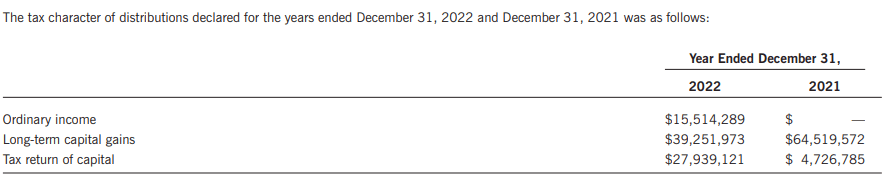

In our previous article, we touched on the tax classifications of the distribution for the prior two years. Here's a recap until we get the latest official tax data for 2023 sometime in early 2024.

The fund's tax character is mostly made up of long-term capital gains. However, return of capital would have also made up some of the distribution. For 2021, this wouldn't have been bad ROC, while 2021 would have been some destructive ROC. Even 'bad' ROC isn't all bad, as it defers an investor's tax obligation in a taxable account due to reducing one's cost basis. Ordinary income could have been generated in 2022 due to covered calls often producing short-term capital gains.

EOS Distribution Tax Classification (Eaton Vance)

{kind=link}

EOS' Portfolio

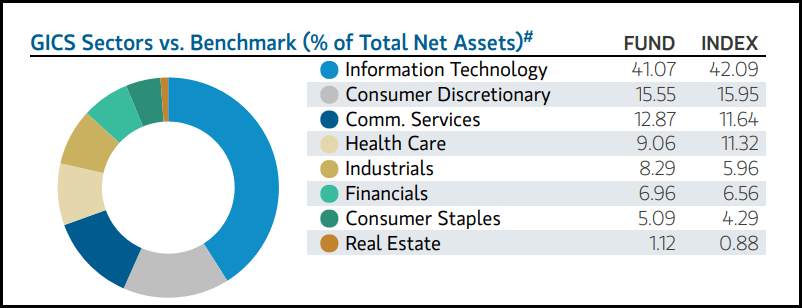

The fund's benchmark incorporated the Russell 1000 Growth Index, as well as the Cboe S&P 500 BuyWrite Index and Cboe NASDAQ-100 BuyWrite Index. However, it is the Russell 1000 Growth Index focus that tilts EOS' significant weight to the technology sector.

{kind=link}

EOS Sector Allocation (Eaton Vance)

Instead of the fund investing in 1000 positions, the fund actually only invests in 52 portfolio holdings. This makes it a fund that is quite narrowly focused but that can work for and against it at times. In this case, the heavy allocation to the Mag 7 names in the fund's top ten resulted in the fund performing quite well, but its benchmark is even heavier in the Mag 7 names.

The iShares Russell 1000 Growth ETF ( IWF ) shows that the Mag 7 names comprise nearly 48% of the fund. Even the IWF takes a sampling approach so that ETF carries around 447 holdings. Combining that with EOS' covered call strategy and against its straight, unconstrained benchmark as represented by the ETF, it did see relatively weaker performance.

YCharts

One of the primary names that is missing from EOS' top ten is Tesla ( TSLA ). Although it is in the portfolio, the weighting at the time was just 0.87%.

Additionally, Apple ( AAPL ) is a larger weighting for IWF at the number one spot with its 12.25% allocation. For EOS, as we can see below, they have it at a meaningfully lower allocation at the end of October. Instead, they've chosen to put Microsoft ( MSFT ) as the top weight, but it's still slightly below IWF's 11.77% weight at this time.

{kind=link}

EOS Top Ten Holdings (Eaton Vance)

Having TSLA at such a low weight was clearly one of the reasons the fund was detracted for this year. We know the fund held TSLA in a low weight heading into the year as well, as it was listed in their last annual report for the period ending December 2022 . At that time, it was a 0.6% allocation with a holding of 39,612 shares. The semi-annual report showed the same 39,612 shares being held, but it crept up to a 1.1% allocation by that June 30, 2023 report.

YCharts

The last report available that shows us the specific number of shares being held was the fund's September 30, 2023, N-PORT filing . At that time, we once again saw the share balance at 39,612.

Both AAPL and MSFT performed quite strongly on a YTD basis so far. However, MSFT has been able to edge out AAPL just barely through this year, at least partially contributing to EOS' MSFT position and extending its percentage weight. At the end of September 2022, EOS held 280,404 shares of MSFT. Their semi-annual report also showed us the same number of shares held, and that was the case for the fund's last annual report, too. So what started off as MSFT at an 8.2% weighting this year has climbed to just over 10.3% due to the appreciation.

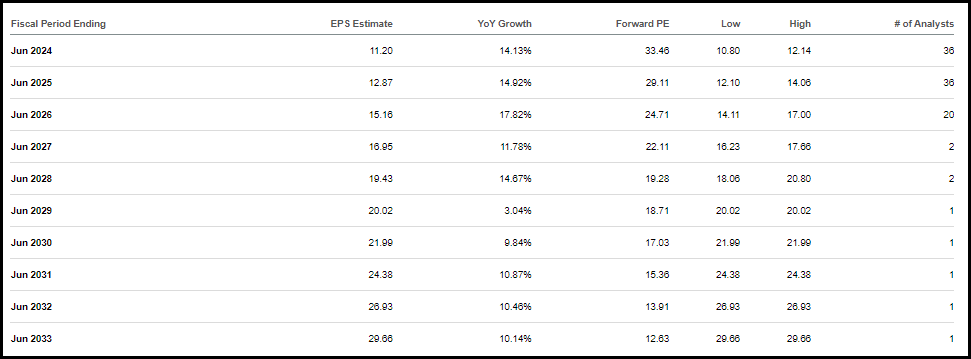

With MSFT at a forward P/E of 33.46x, it is easy to think that the company's shares are expensive. However, with growth expectations moving forward, we can see that what is expensive now really comes down in valuation if those earnings are achieved. By this time next year, we could be looking at a forward P/E of sub-30x. Three years from now, we could be looking at a valuation of sub-25x. If you are a trader looking for short-term opportunities, that's different and is a fair strategy.

{kind=link}

MSFT Earnings Outlook (Seeking Alpha)

For investors, three years really shouldn't be seen as hardly any time at all. If I made the definitions of short, medium and long-term periods, I would say that long-term isn't until five years in. Five years out, and if analysts are right, and of course, that is a big if, we'd be looking at a sub-20x forward P/E. On the other hand, fortunately, the IRS considers one year long-term, but that works even better for tax purposes.

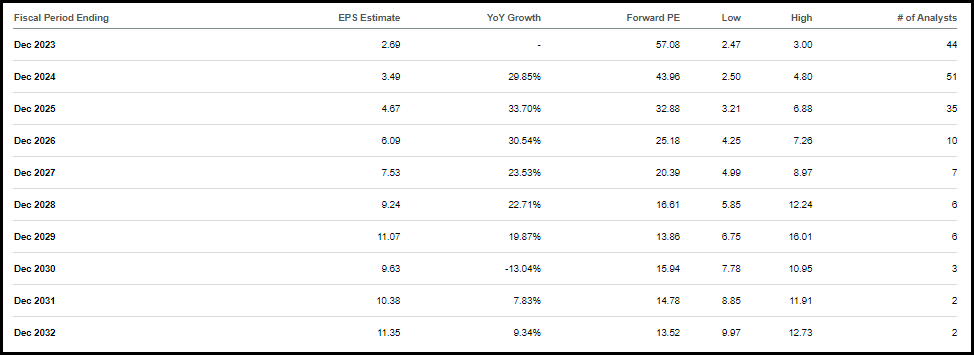

Even for Amazon ( AMZN ), which looks exceedingly richly valued at an over 57x forward P/E five years out, we could be nearly calling it a value stock at that point.

{kind=link}

AMZN Earnings Outlook (Seeking Alpha)

A final point in terms of the defense of the technology sector is that we are essentially where we were before. Though the latest push put us into more positive territory for the Technology Select Sector SPDR ETF ( XLK ), since the beginning of 2022 to date, we haven't made any sort of outlandish progress in terms of performance. The Invesco QQQ Trust ( QQQ ) is barely positive at this point in an almost two-year period.

YCharts

Conclusion

EOS' significant overweight allocation to tech has helped the fund produce solid results through 2023. The fund's covered call strategy did mean lagging results compared to its unconstrained benchmark. Though sometimes it is the opposite, in weaker years such as 2022, we see a contribution from the fund's call-writing strategy.

With such a significant weighting to the Mag 7 names, the fund's future really looks to be determined by how that basket performs going forward. I believe there is an argument to be made on both sides of the aisle. In terms of the overvalued camp, we are looking at relatively expensive earnings multiples. On the other hand, if growth expectations are met, those multiples can come down quite rapidly. An additional factor is the fund's discount still remains relatively attractive; even if it isn't at a dirt cheap valuation, we are looking at a fair valuation for a long-term investor.

For further details see:

EOS: Solid Performance From This Covered Call Fund With An Attractive Discount