MCN - EOS: Some Attractive Characteristics Limited Diversity

2023-09-29 12:36:18 ET

Summary

- Eaton Vance Enhanced Equity Income Fund II offers investors a high level of income from an equity portfolio, with an 8.07% yield.

- The fund's recent performance has been better than the broader market index, but investors have still lost money overall.

- The fund employs an options strategy to generate income, but this strategy comes with limitations and risks.

- The fund's strategy will normally outperform the index during flat or bear markets, which we are likely to have over the next few years.

- The fund's distribution appears sustainable, and it currently trades at a reasonable discount on NAV.

The Eaton Vance Enhanced Equity Income Fund II ( EOS ) is a closed-end fund, or CEF, that provides an easy way for investors to maintain their equity exposure and still earn a high level of income from their portfolios. This is important because equities have an incredibly low yield. After all, the S&P 500 Index (SP500) only yields 1.52% at today's level, which means that a $1 million investment will only produce $15,200 per year in annual income. That is obviously nowhere close to enough to support the lifestyle of anyone who is capable of coming up with $1 million to invest. The Eaton Vance Enhanced Equity Income Fund II boasts an 8.07% yield, which is much closer to the yield that someone with a million dollars in savings needs to support a typical lifestyle.

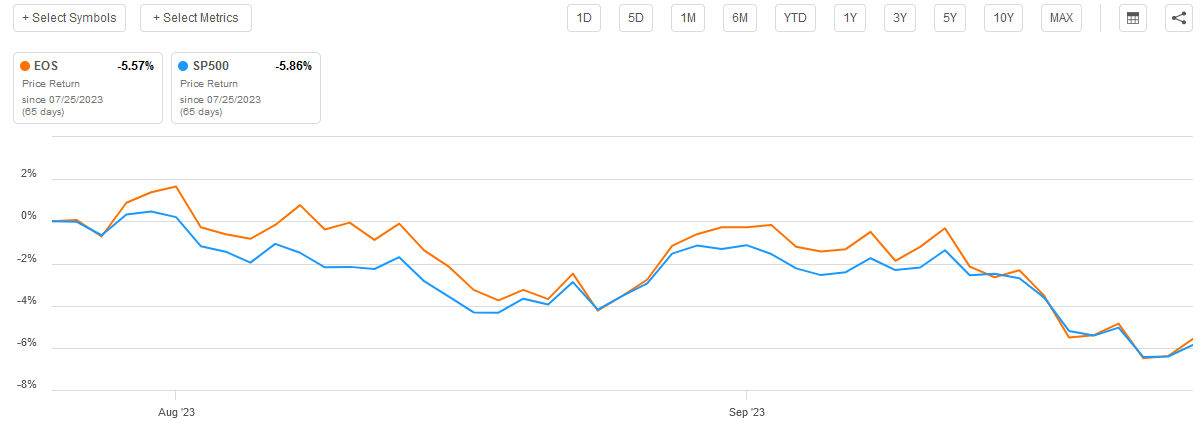

We last discussed the Eaton Vance Enhanced Equity Income Fund II on July 25, 2023. The fund's shares have performed relatively in line with the S&P 500 Index since that time:

{kind=link}

However, when we consider the higher yield of the Eaton Vance Fund, its performance has been much better but investors still lost money investing in it overall. The fact that the fund is delivering a better performance than the broader market index is pretty much what we would expect considering this fund's overall strategy. After all, as I stated in my previous article, this fund should outperform during flat or bear markets and underperform during bull runs. This is pretty much what we see here.

As a few months have passed, it could be time to revisit our thesis surrounding this fund and see if it makes sense to own it today. After all, a lot has changed in the overall climate as inflation has been getting worse due to rising energy prices, leading to a selloff of long-duration assets. There are even now a few Wall Street banking executives predicting much higher interest rates in 2024 than we have today. That is a fairly big change from the prevailing attitude back in July.

About The Fund

According to the fund's webpage , the Eaton Vance Enhanced Equity Income Fund II has the primary objective of providing its investors with a high level of current income. This is an unusual objective for a fund with a portfolio that is 99.66% invested in common equity:

CEF Connect

The reason that this is an unusual objective is that common equity is not a particularly good income vehicle. As mentioned in the introduction, the S&P 500 Index only has a 1.52% current yield. The high-yielding utility sector ( IDU ) only yields 2.99% today, which is much less than an ordinary money market fund. In fact, only the energy sector has yields that are sufficiently high to compete with fixed-income securities right now. Thus, anyone who is seeking income will normally want to look at an energy sector fund or something in the fixed-income sector. This is especially true now that the market appears to have re-entered the bear market that we witnessed in 2022, which handicaps its ability to reward its investors through capital gains.

However, as we discussed in the previous article on this fund, the Eaton Vance Enhanced Equity Income Fund II employs an options strategy to provide a high level of current income from an equity portfolio. As I explained in the previous article:

The fund invests in a portfolio of primarily large- and midcap securities that the investment advisor believes have above-average growth and financial strength and writes call options on individual securities to generate current earnings from the option premium.

The option premium acts like a synthetic dividend, effectively raising the yield of the securities in the portfolio. The synthetic yield here can be pretty high too, as evidenced by the Global-X buy-write exchange-traded funds reliably producing a payment of about 1% per month. Granted, those funds are writing at-the-money options and this one is not necessarily doing that, but the call premiums still tend to be sufficiently high to effectively create a yield that is above that of most fixed-income securities even in today's high-interest rate environment.

The use of options to create a synthetic dividend is not a perfect replacement for an actual dividend, however. This is due to the downside of this strategy. In short, the capital gains are capped at the strike price of the option. If the stock upon which the option is written has a higher price than the strike price of the option, then the fund is obligated to sell the stock to its counterparty. Thus, the fund does not actually benefit from any capital gains on the stock above the strike price of the option. If the stock was actually paying a real dividend, this would not be the case. However, as already mentioned, apart from investing in the energy sector or a handful of telecommunications companies and tobacco stocks, this strategy is pretty much the only way to get a 6% or higher yield from a common equity portfolio.

We can see then why this strategy will outperform during flat and bear markets. This is because the option premium offsets some of the losses from a declining stock price in a bear market. In a flat market, the option premium provides at least some investment return in the absence of capital gains. In both of these markets, we do not have to worry as much about the potential capital gains being limited because the option is much more likely to expire out of the money than it would be during a raging bull market. As such, a fund employing a covered call strategy like this one makes a lot more sense today than it did in 2021 or over the 2010 to 2020 period.

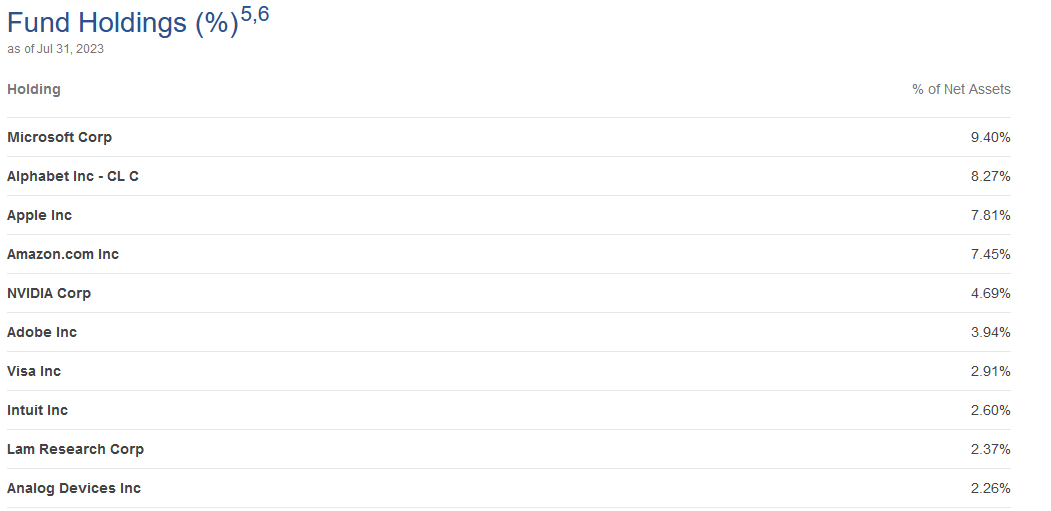

One thing that I have noted in numerous past articles about Eaton Vance funds is that this fund house tends to invest an outsized proportion of its funds' assets into American mega-cap technology stocks. This is certainly the case with this fund, as we can see by looking at the largest positions in the portfolio:

{kind=link}

As we can see here, Microsoft ( MSFT ), Alphabet ( GOOG ) (GOOGL), Apple ( AAPL ), and Amazon.com ( AMZN ) account for fully 32.93% of the fund's assets. When we add in NVIDIA ( NVDA ) and Adobe ( ADBE ), we are at 41.31% of the fund's total assets in just six stocks, all of which are in the technology sector. This is far above the 28.27% weighting that the technology sector has in the S&P 500 Index. As such, any investor in this fund should be comfortable with the outsized exposure to the technology sector. An investor should also ensure that their portfolio is properly diversified in order to avoid having too much exposure to that one sector. After all, the technology sector did underperform in 2022 and investors who were too heavily exposed to it took some big losses. It is possible that this could happen again, particularly if some of the concerns that executives at Goldman Sachs and JPMorgan have expressed about the risk of an energy shortage-driven stagflation environment in 2024 and beyond actually come to pass. It is best to be appropriately diversified in order to minimize your risks and sleep well at night, especially if you are retired and are depending on your portfolio.

With that said, I will not be as critical of the substantial technology exposure here as I am in articles about some of Eaton Vance's other option funds. This is because it does make a great deal of sense for a fund that is writing single-stock covered call options to be heavily weighted to this sector. In general, the technology sector has higher option premiums than short-duration sectors such as materials or energy, so the fund's technology-heavy portfolio allows it to generate a higher level of income from the option premiums than it could if it had a more balanced portfolio.

Interestingly though, we do see a more balanced portfolio in some other covered call funds such as the Madison Covered Call and Equity Strategy Fund ( MCN ). However, that fund tends to trade stocks much more often than the Eaton Vance Fund and so is trying to achieve capital gains from trading stocks rather than just writing options against a buy-and-hold portfolio.

Performance

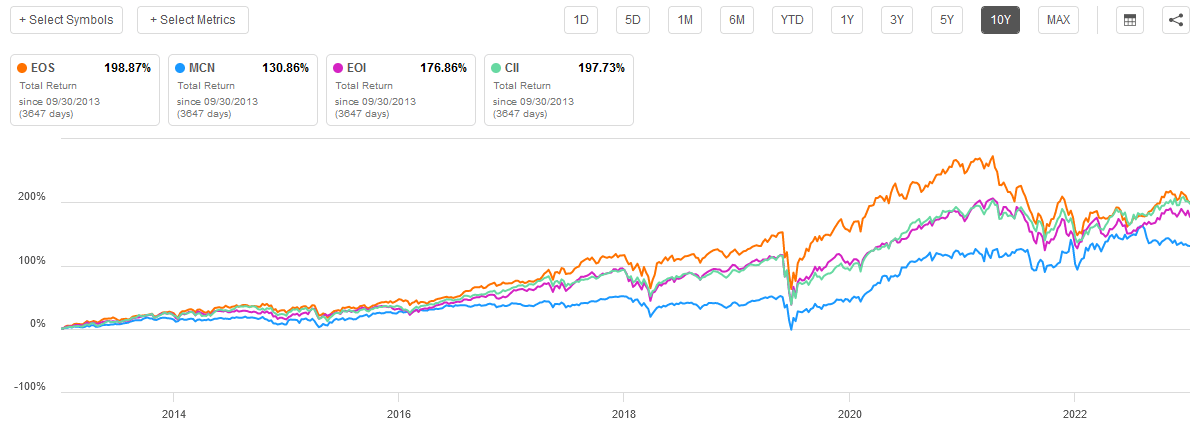

The Eaton Vance Enhanced Equity Income Fund II has delivered a very strong performance over time relative to its peers. We can see this by comparing its total return against that of other fairly well-known covered call funds. These other funds are the Madison Covered Call and Equity Strategy Fund, the BlackRock Enhanced Capital and Income Fund ( CII ), and the Eaton Vance Enhanced Equity Income Fund ( EOI ).

Over the past ten years, the Eaton Vance Enhanced Equity Income Fund II has delivered the highest total return of any of these funds, just narrowly beating the BlackRock fund:

{kind=link}

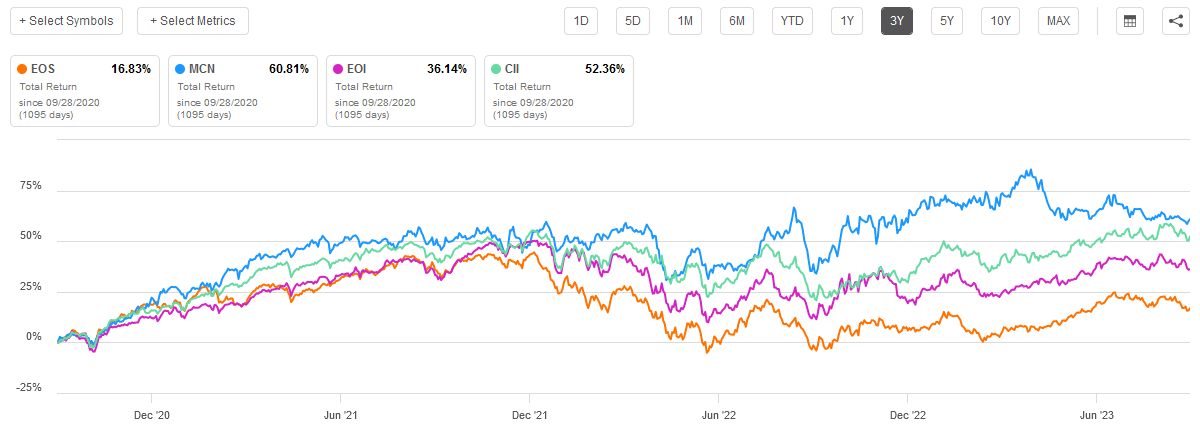

Unfortunately, the fund's performance deteriorates a bit over a shorter period of time. For example, over the past three years, the Eaton Vance Enhanced Equity Income Fund II was by far the worst performer of any of its peers:

{kind=link}

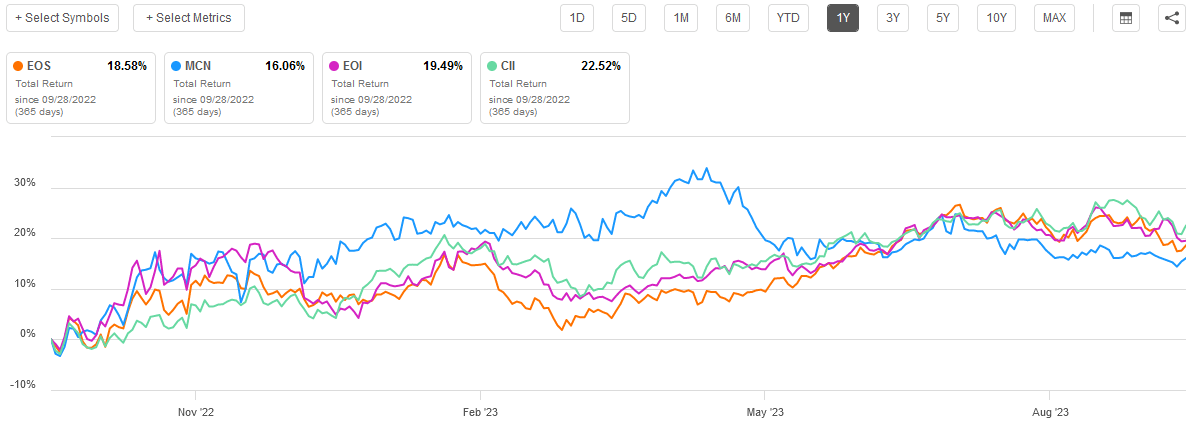

The fund's performance over the past year was also disappointing relative to its peers, but it was not the worst performer:

{kind=link}

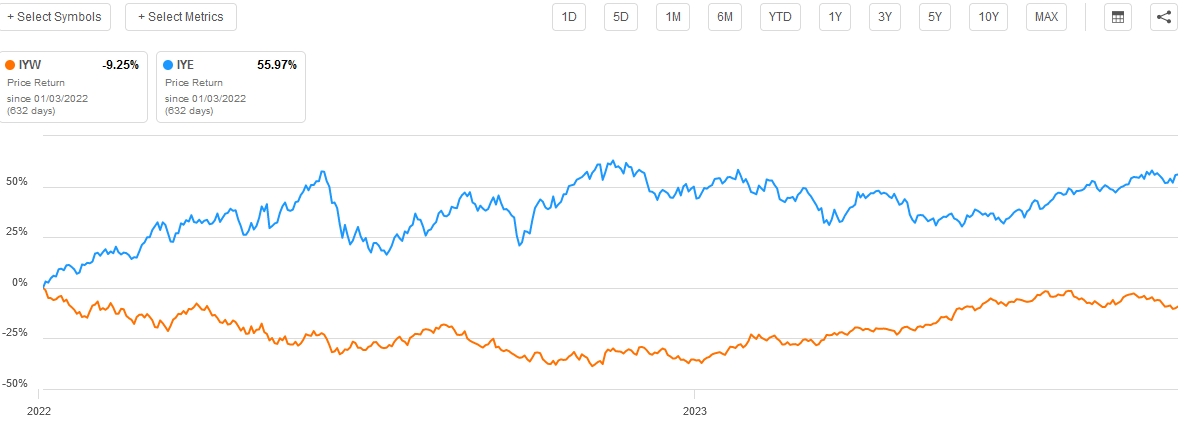

This probably has to do with the fund's portfolio. In particular, since the start of 2022, the energy sector ( IYE ) has outperformed U.S. technology ( IYW ) by quite a lot:

{kind=link}

The Eaton Vance Enhanced Equity Income Fund II has absolutely no energy exposure. The BlackRock and Madison funds that were used for comparison purposes both do. While a covered call strategy does put a limit on capital gains, these funds are not necessarily writing at-the-money call options, nor are they overwriting their entire portfolios. Thus, they still benefited from a better portfolio in the current environment. In addition, the BlackRock fund has much lower technology exposure, so it was not hurt as much by the technology weakness over the period as the Eaton Vance Enhanced Equity Income Fund II. This overall shows the value of diversification, thus effectively proving the argument that I made earlier about the need to maintain sufficient diversification throughout your entire portfolio.

Distribution Analysis

As mentioned earlier in this article, the primary objective of the Eaton Vance Enhanced Equity Income Fund II is to provide its shareholders with a high level of current income. In order to accomplish this objective, the fund invests in a portfolio of common stocks and then writes call options against them. The goal here is to have the option expire worthless, allowing the fund to keep both the underlying stock and the option premium. This strategy does work pretty well to generate a respectable level of income from a portfolio when it works. The fund collects the money that it earns from the option premiums as well as any capital gains that it manages to realize from the stock portfolio and then pays them out to the shareholders, net of the fund's own expenses. As such, we might assume that this allows the fund to pay out a fairly high distribution yield to its investors.

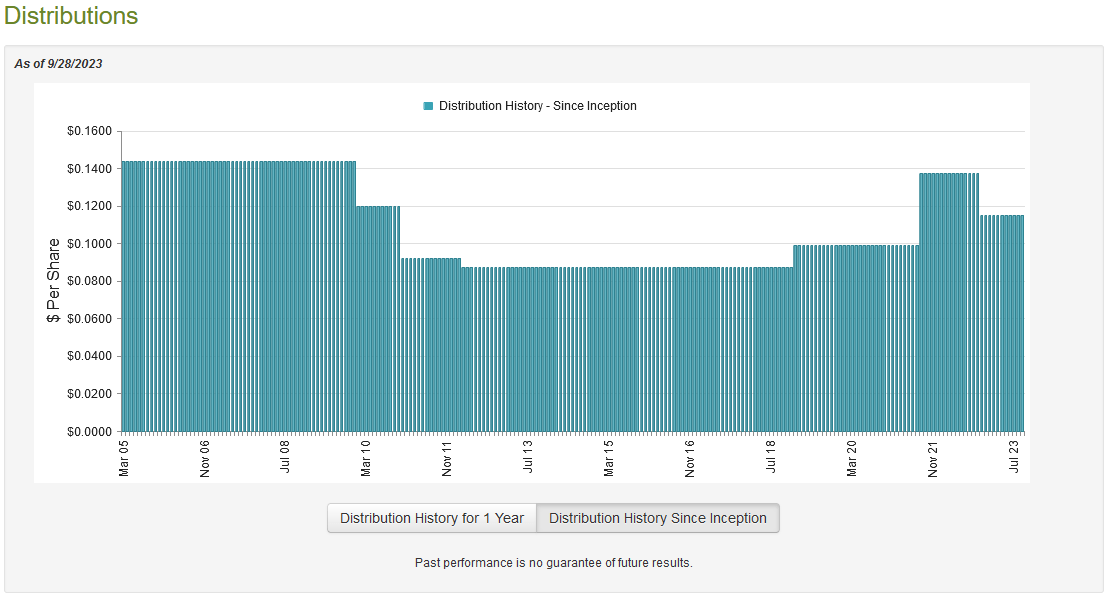

That is certainly the case as the Eaton Vance Enhanced Equity Income Fund II pays a monthly distribution of $0.1152 per share ($1.3824 per share annually), which gives the fund an 8.07% yield at the current price. Unfortunately, the fund has not been particularly consistent with respect to its distribution over the years, as it has both reduced and increased it numerous times since inception:

{kind=link}

The most recent cut came back in November when the fund cut its distribution by 19.18% from its previous level. Overall, this distribution history might prove to be a bit of a turn-off for those investors who are seeking a safe and secure source of income to use to pay their bills or finance their lifestyles. However, this fund has not performed nearly as badly in this respect as many other closed-end funds.

As I have mentioned numerous times in the past though, the fund's history is not necessarily the most important thing for anyone who is considering purchasing its shares today. This is because anyone buying the fund today will receive the current distribution at the current yield and will not be adversely affected by actions that the fund has taken in the past. The most important thing for any new investor is the fund's ability to sustain the current distribution. Let us investigate this.

Fortunately, we have a relatively recent document that we can use for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on June 30, 2023. This is a newer report than the one that we had available to us the last time that we discussed this article, which is nice to see. During the first half of this year, the market was fairly strong, particularly the technology sector that this fund is heavily invested in. That may have given it some potential to make some money via capital gains. In addition, the rising stock market prices for the mega-cap technology plays had a positive impact on option premiums, allowing the fund to make some money that way. Thus, there are some reasons to believe that the period covered by this report was a much better period overall than what the fund experienced back in 2022.

During the six-month period, the Eaton Vance Enhanced Equity Income Fund II received $3,980,049 in dividends from the assets in its portfolio. This was the fund's only income during the period, so its total investment income in the reporting period is the same figure. This was not sufficient to cover the fund's expenses, leaving it with a net investment loss of $844,620. Obviously, that was not enough money for the fund to pay any distribution, but it still distributed $36,147,657 to its investors. At first glance, this is likely to be quite concerning as the fund is unable to cover its expenses, let alone its distributions, out of investment income.

However, there are other ways through which the fund can obtain the money that it needs to cover the distribution. For example, it receives a premium whenever it sells an option. These premiums are not considered to be investment income for tax purposes (they are either a return of capital or a capital gain, depending on the circumstances) but obviously still represent money coming into the fund. In addition, the fund might have been able to take advantage of the strength in the market and sell some securities for capital gains.

Fortunately, it did have considerable success in this endeavor during the period. The fund reported net realized gains of $56,398,444 and had another $129,969,535 net unrealized gains. Overall, its net assets increased by $153,193,625 after accounting for all inflows and outflows during the period. While this was not sufficient to make up for the losses that it suffered in 2022, it was enough to cover the distributions that the fund paid out with a substantial amount of money left over. Overall, there should not be any real reason to worry about the fund's distribution at this time, although it may have problems should the current bear market continue for another year or so.

Valuation

As of September 28, 2023 (the most recent date for which data is available as of the time of writing), the Eaton Vance Enhanced Equity Income Fund II has a net asset value of $17.84, but the shares only trade for $17.27 each. This gives the fund's shares a 3.20% discount on net asset value at the current price. That is not nearly as attractive as the 4.34% discount that the shares have had on average over the past month. However, it is still a discount, so it is not a horrible price to pay.

Conclusion

In conclusion, the Eaton Vance Enhanced Equity Income Fund II is an income-focused closed-end fund that does not require its investors to sacrifice their equity exposure to obtain income. The fund's strategy should actually outperform for a while, as it seems unlikely that we will experience anything resembling a raging bull market in the near future.

The fact that the fund's distribution appears sustainable, and its shares are trading at a discount adds to its appeal. The only real problem with Eaton Vance Enhanced Equity Income Fund II is that it is not particularly diversified across sectors, so you will need to ensure that the rest of your portfolio is appropriately structured to allow you to achieve the diversification that you should have.

For further details see:

EOS: Some Attractive Characteristics, Limited Diversity