EQNR - Equinor's Strong Q2 Earnings Show Its Long-Term Value

2023-07-26 15:02:53 ET

Summary

- Equinor ASA announced strong Q2 earnings with a double-digit dividend rate and a continued commitment to share repurchases.

- The company's cash flow was temporarily lower as a result of tax obligations, but it's continuing to generate strong free cash flow.

- The company has the ability to continue generating strong returns and growth, especially in renewable energy, making it a valuable investment.

Equinor ASA ( EQNR ) is Norway's state oil company, the company that defined the riches for a nation. The company is smaller than many other integrated oil producers, with a market capitalization of just under $100 billion. As we'll see throughout this article, despite some one-time expenses, the company can generate strong shareholder returns.

Equinor Q2 2023 Results

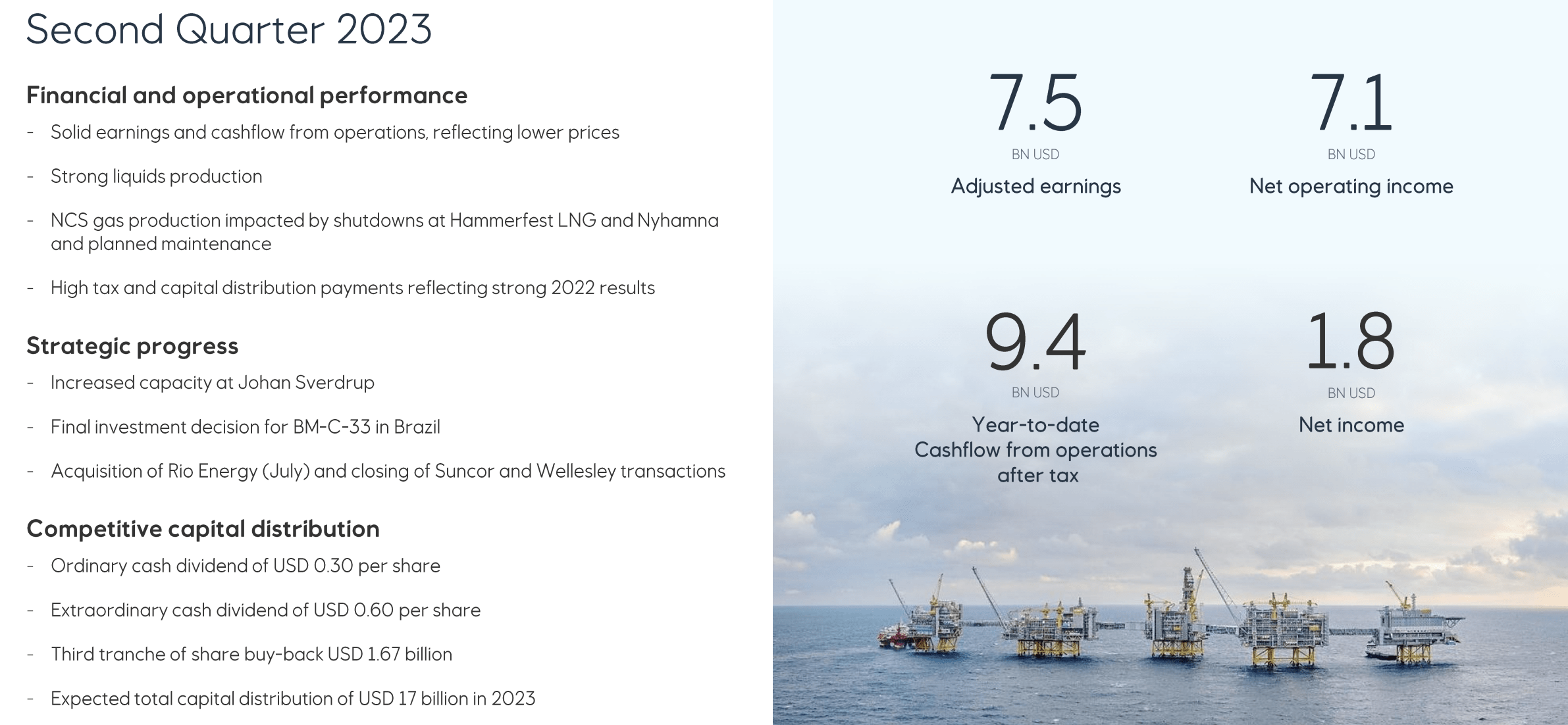

The company had strong results in Q2 2023 , showing its continued financial strength.

{kind=link}

The company generated strong earnings and cash flow as production remained high. It was partially impacted by maintenance shutdowns, but we expect that to be temporary. The company has continued to make final investment decisions and expand other large projects, to enable production to continue growing over time.

The company earned $7.5 billion in adjusted earnings for the quarter and $9.4 billion in YTD CFFO after tax. That gave the company $1.8 billion in net operating income. The company declared a total of $0.9 in dividends, or a double-digit annualized dividend yield as the company's earnings have continued to remain strong.

The company expects total capital distribution of $17 billion in 2023, with another almost $2 billion in share buybacks after those dividends. The company is continuing to generate massive cash flow and passing it directly to shareholders.

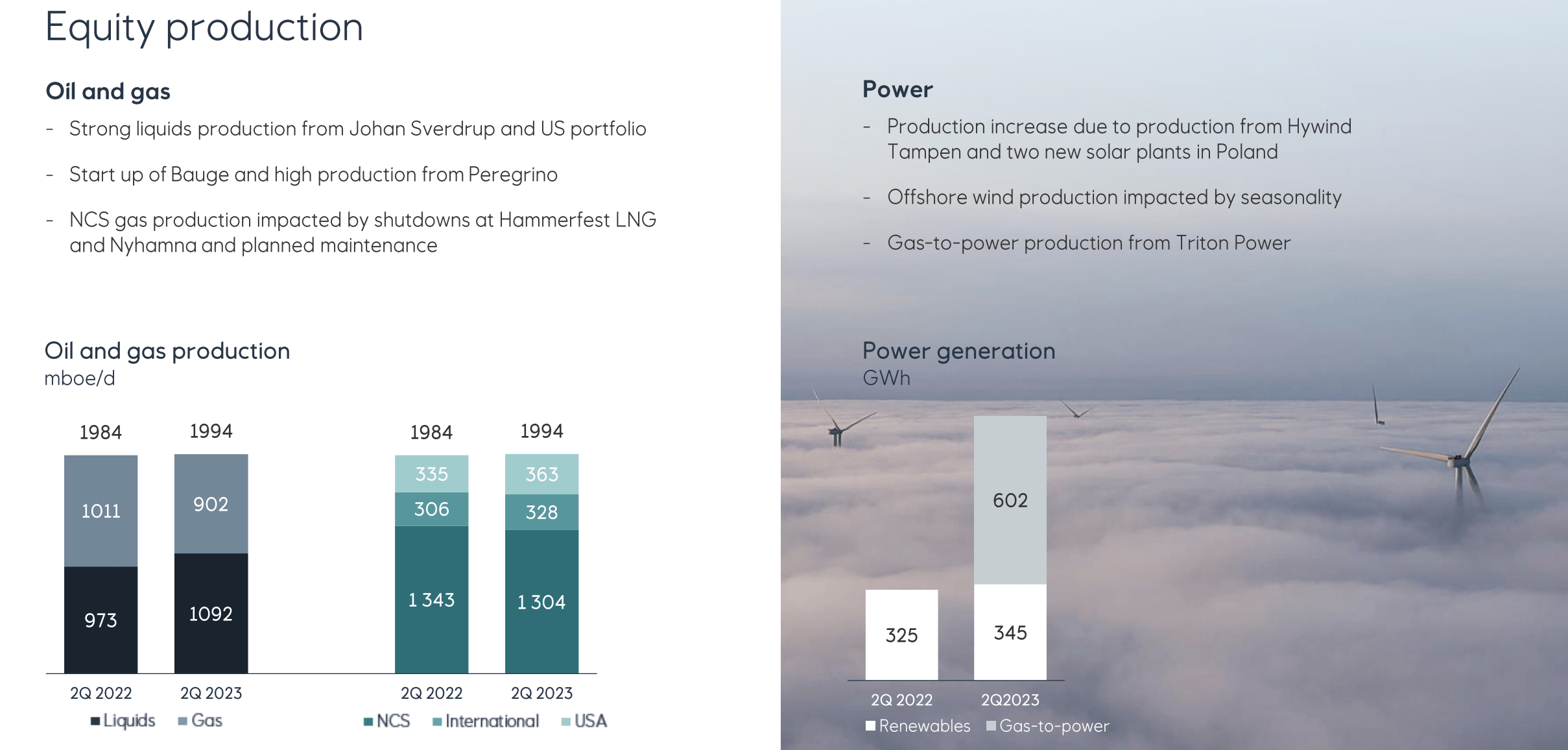

Equinor Equity Production

The company's core business has kept production high as the company has expanded into renewables as well.

{kind=link}

The company had strong liquids production of more than 1 million barrels / day. Total production counting the company's gas production was almost 2 million barrels a day as the country's gas remains in incredibly high demand from continental Europe. The company's gas is the most interesting replacement for Russian gas.

The company's Hammerfest LNG had a leak , but the company's managed to solve it and bring back production. The company's gas to power business remains strong, as the company promotes natural gas as a transition fuel. However, the real strength is the company's 345 GWh in renewable power, or $10s of millions in renewable power.

The company has 3.3 GW of renewable capacity, it's working to continue expanding.

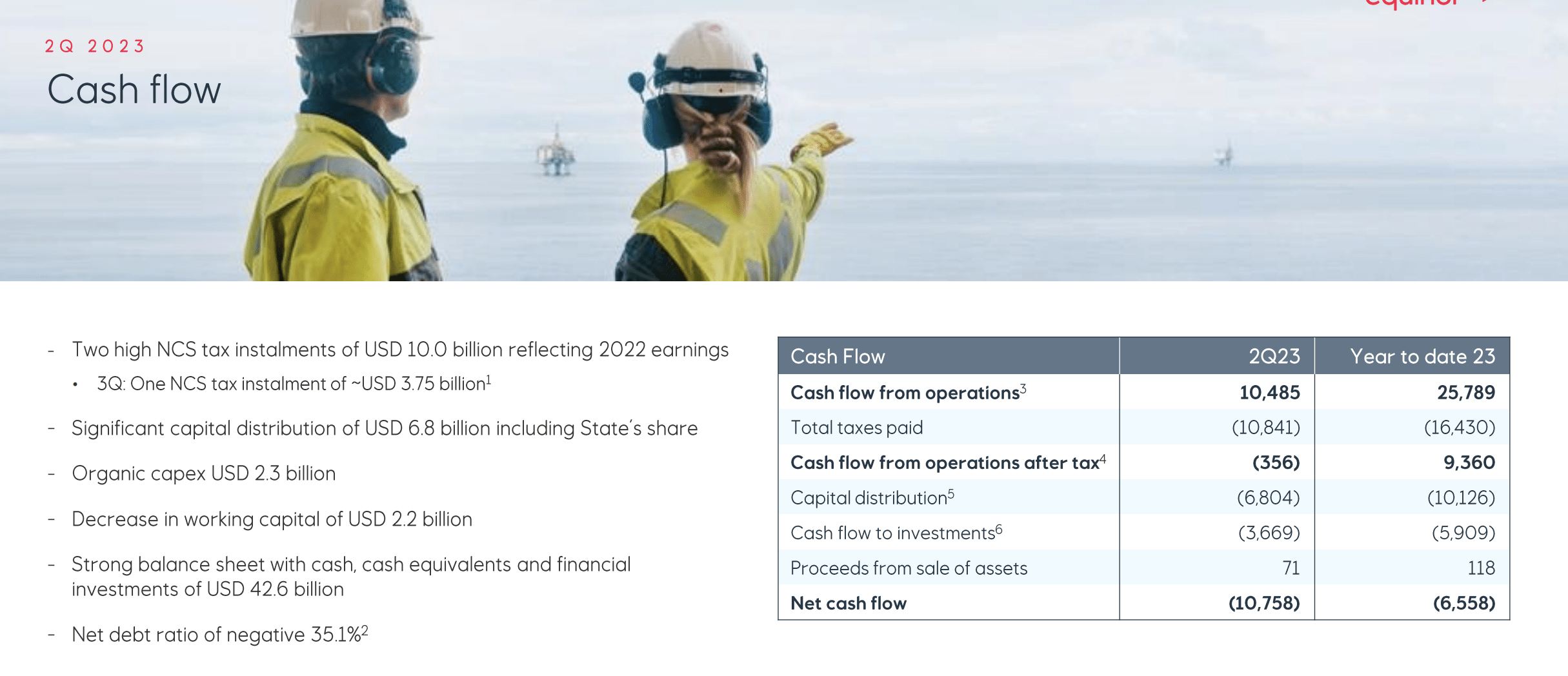

Equinor Cash Flow Costs

The company's cash flow was temporarily impacted by a massive tax bill.

{kind=link}

Norway charges a 78% marginal rate on the NCS (Norwegian Continental Shelf). That resulted in the company paying almost $11 billion in taxes during the quarter, paying off massive tax liability from 2022. The company expects a $3.75 billion tax liability in 3Q, which will enable its cash flow to be much higher in the next quarter.

The company spent $2.3 billion in organic capex for the quarter, and had -$11 billion in net cash flow for the quarter. The company has a massive negative net debt ratio though, with a strong balance sheet, so temporarily paying off tax liabilities is not at issue. The company can continue directing that cash heavy balance sheet to shareholders.

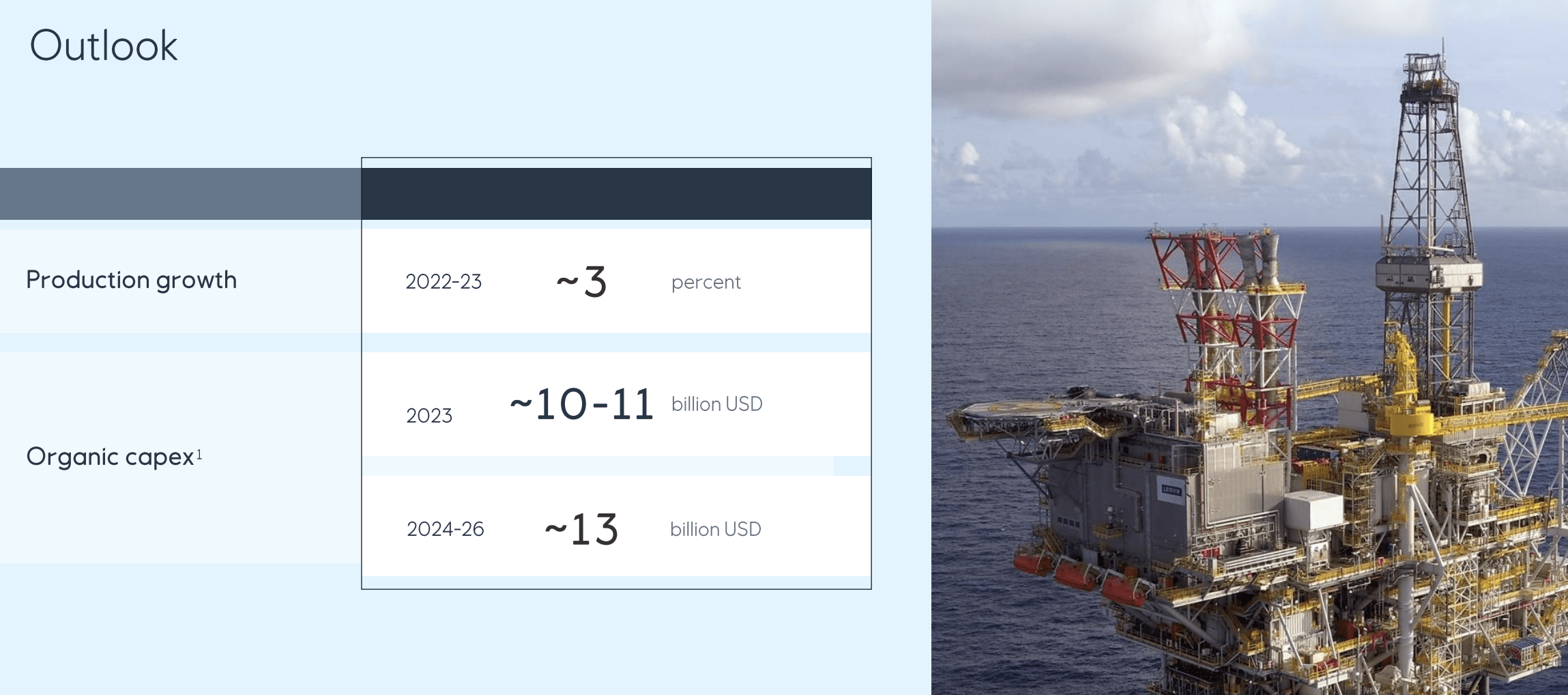

Equinor Outlook

The company's outlook shows continued strength in its portfolio.

{kind=link}

The company is planning to ramp up its capital expenditures from $2.75 billion / quarter currently to $3.25 billion / quarter in the 2024-2026. That's especially true as the company ramps up its renewable capital spending. That's a capital spending level the company can comfortably afford. It produces ~180 million barrels / quarter + its renewable business.

The company's capital spending is ~$12 / barrel, a relatively low level of capital spending for a company that's managing continued growth, and much lower than current prices.

Equinor Renewables

Norway continues to have massive electricity energy demand, as electric vehicles ("EVs") have hit a 90% share .

{kind=link}

The company is building the world's largest wind farm, and it's working to diversify heavily outside of its core Norway business. The company is building a leadership position in offshore wind and helping to give its earnings more of a utility like status. The company expects project base returns of 6%, not high, but a level it can comfortably deploy capital at.

The company is targeting 14 GW of installed capacity by 2030, a more than quadrupling of current levels, which will enable massive growth in reliable cash flows. Wind energy, especially in the company's region, is much more valuable than solar earnings.

Thesis Risk

The largest risk to our thesis is crude oil prices. Prices have seen some strength recently, pushing up towards $80 / barrel, and OPEC+ has been working to maintain that. There's thought of economic strength going into the 2H of the year, which could support prices even more. However, should demand drop dramatically, that could hurt long-term returns.

Conclusion

Equinor ASA has a portfolio in one of the most stable producing regions in the world. The company's portfolio is split between oil and natural gas, a drag somewhere like the United States, but in Europe, where Russian natural gas has been shut down, it's one of the strongest assets to have. The company has also been building up a strong renewable business for diversification.

The company has an incredibly strong net cash position. Despite immediate tax expenditures, the company is driving substantial shareholder returns as overall earnings remain well into the double-digits. We'd like to see the company aggressively repurchase shares and focus on long-term returns. Let us know your thoughts in the comments below.

For further details see:

Equinor's Strong Q2 Earnings Show Its Long-Term Value