AIQ - Equity CEFs/ETFs: Top Picks For 2024 - Part II

2024-01-05 11:01:47 ET

Summary

- In Part I of my Top Picks For 2024, I explained why we saw such extreme valuation losses in most equity CEFs in 2023 and what that could-mean for 2024.

- In my opinion, liquidity was the over-riding factor for why so few stocks, think Magnificent 7, received the lion's share of buy-interest while most everything else suffered, including equity CEFs.

- But just because the Federal Reserve will continue its Quantitative Tapering doesn't mean that other Fed programs won't increase liquidity in other places.

- The regional banks, for example, have been a primary beneficiary of such liquidity and combined with an expectation of rate cuts next year, the markets rallied to end 2023 at essentially all-time highs.

- The riddle now is how to balance all of that in for next year and come out with picks that can outperform in 2024.

Part I here .

I should first say that, except for a very few number of funds in the CEF universe, the vast majority of equity CEFs could not keep up with the major market indexes, like the S&P 500 ( SPY ) , $475.31 closing market price , last year at market price.

And though most equity CEFs wouldn't necessarily use the S&P 500 as their benchmark, it's still the one index most equity asset managers compare their performance to.

And in 2023, my picks had a mixed performance though only the Eaton Vance Tax-Managed Global Buy/Write Opportunities fu nd ( ETW ) saw a significant underperformance in market price compared to its NAV price performance.

And considering only eight funds out of more than 100 equity CEFs I follow were able to outperform the S&P 500 and well over half were either negative on the year or showed only single-digit gains, my 2023 picks turned out OK after all, at least for CEFs:

| Ticker |

| MKT 2023 |

| NAV 2023 |

| Disc/Prem |

| MKT Yield |

| MKT Performance |

| NAV Performance |

| ETW |

| $7.77 |

| $9.03 |

| -14.1% |

| 9.0% |

| +9.2% |

| +16.3% |

| BIGZ |

| $7.33 |

| $9.10 |

| -18.8% |

| 7.2% |

| +18.9% |

| +11.1% |

| IDE |

| $10.18 |

| $11.85 |

| -14.1% |

| 9.0% |

| +21.0% |

| +16.4% |

| HQH |

| $16.57 |

| $19.64 |

| -16.4% |

| 9.3% |

| +1.0% |

| +1.7% |

| PGP |

| $7.50 |

| $7.38 |

| +0.7% |

| 11.3% |

| +20.2% |

| +18.8% |

Still, the only positive spin you can say about most of the equity CEF underperformances in 2023 is that if you go back to 2022's bear market when most equity CEFs outperformed the S&P 500, the overall performance difference over the past two years was much more balanced.

So the question then becomes, what will 2024 bring? A continuation of the bull market that really got going in November of 2023 or will some hiccup like a recession or a resurgence in inflation or the elections have more of an influence than we're plugging in right now?

All we can say for sure is that everyone is relying on the Federal Reserve to pivot from a tightening bias of monetary policy to a loosening bias and thus, everyone is expecting the bull market to continue well into 2024.

If only it were that simple.

Top CEF Picks For 2024

My first pick will follow what I did i n 2021 wh en I picked the same fund, in this case the Eaton Vance Enhanced Equity Income fund ( EOI ) , $16.58 closing market price , as a top pick in consecutive years.

That's because even though EOI's NAV performed well the first year, which was the COVID-19 year, I didn't think EOI appreciated as much as it should have at market price in 2020 .

And that turned out to be the right call when in 2021 , EOI went on to gain +32.0% at total return market price, beating the S&P 500, which rose + 28.6%, comparatively.

So I'm going to see if, once again, I was just 1-year too early and select the Aberdeen Healthcare Investors fund ( HQH ) , $16.57 closing market price , as a Top Pick for 2024 after making it a top pick for 2023.

Now large-cap biotech stocks, which is HQH's bread and butter, did not have a great 2023, to say the least, rising from negative for most of the year to a slight gain of 4.5% with the rally into year-end (see below).

Y-Charts

And though HQH's NAV pretty much followed a sector index ETF like the iShares Biotechnology ETF ( IBB ) , $135.85 closing market price , HQH's market price discount has dropped from a -12.9% discount at the beginning of 2023 to a -16.4% discount today.

That's a lot of negative news built into HQH and with M&A activity already picking up in the biotech space, I believe the risk/reward leans heavily toward reward at this point.

HQH uses virtually no leverage or options to augment its income or appreciation potential, so the fund's quarterly distributions are mostly dependent on portfolio appreciation from its holdings. Thus, HQH's distribution can vary quarter-to-quarter but a current buyer of HQH at $16.57 would receive a generous 9.3% current yield, which with the fund's discount, would mean a significant windfall over HQH's 7.8% NAV yield.

If you want to learn a little more about HQH, here is the fund's Fact Sheet (hit link) as of 9/30/2023.

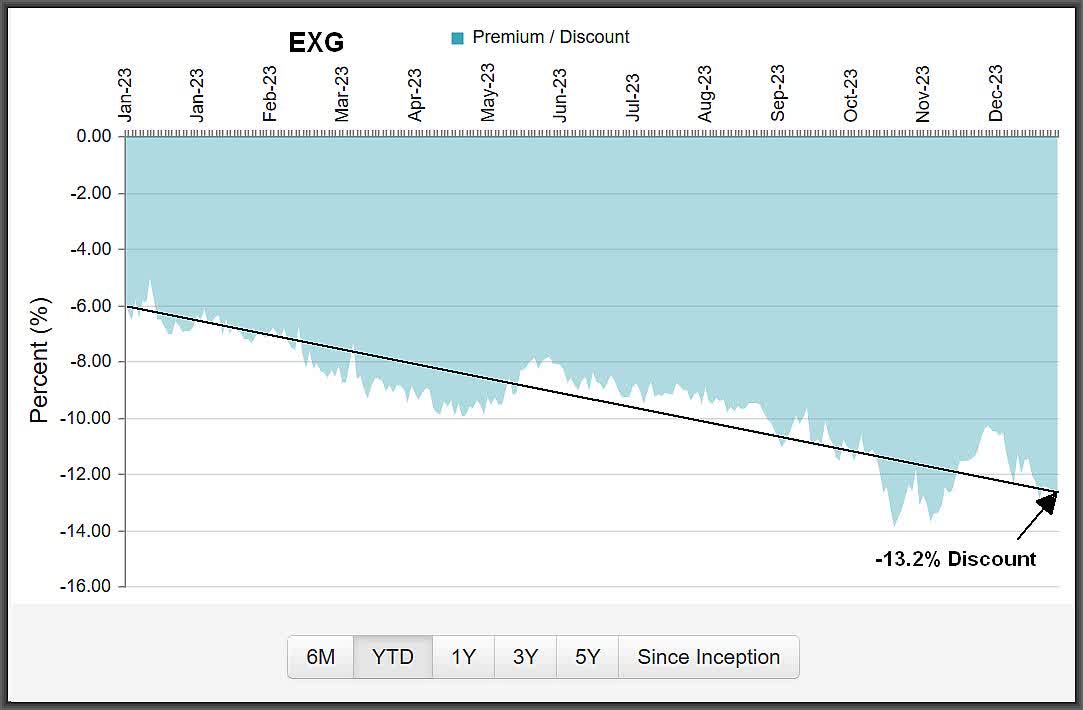

My second pick for 2024 is another equity CEF that saw its NAV performance far outdistance its MKT price performance. But I believe that once 2023 is finally in the rear-view mirror, institutional investors that abandoned equity CEFs from some fund sponsors will come back to the funds that have good liquidity, had superior NAV performance and should get a bump up at market price to start the new year.

And I believe no fund represents that opportunity better than the Eaton Vance Tax-Managed Global Diversified Equity Income fund ( EXG ) , $7.72 closing market price .

EXG is a very large equity CEF at $2.7 billion in assets, so what may have hurt the fund in 2023 as financial institutions bailed to raise cash or reduce debt should help the fund in 2024 since any institutional investor looking for good opportunities in smaller cap securities that invest in large cap stocks would first need to see liquidity and then excellent value. EXG offers both.

For a global large cap all stock fund that sells (writes) index options against roughly 50% of its portfolio value, EXG combines an easy-to-follow portfolio of global stocks while offering some defensiveness with its option-write strategy.

That combination helped EXG to a solid +19.1% total return NAV performance in 2023 but, as I pointed out earlier, EXG's market price performance was only up +11.0% .

That resulted in a Premium/Discount chart that looked like this in 2023:

{kind=link}

CEF Connect

At a $7.72 closing market price, EXG offers a current buyer a generous + 8.6% market yield paid monthly, which is well over its very reasonable and attainable +7.5% NAV yield.

In fact, with an NAV up +19.1% in 2023, you can see that this is well over twice EXG's +7.5% NAV yield, which means there is room to bump up EXG's monthly distribution if Eaton Vance wanted to.

The other nice feature of EXG's distributions is that they include a large percentage of Return of Capital (ROC) , which is non-taxable in the year received, though you would need to reduce your cost basis by the ROC amount.

And before you say that ROC is just handing you back your investment principal, keep in mind that as long as EXG's NAV is growing, then it's NOT destructive Return of Capital .

In other words, EXG's NAV started 2023 at $8.02/share and finished 2023 at $8.89/share , so clearly, even after distributions, EXG's NAV was growing and increased an impressive +10.8%.

So for taxable accounts, that 96% ROC in EXG's distributions in 2023 (EXG has an October fiscal year), means that if a shareholder realized an +8.5% annualized distribution yield, then it was virtually all non-taxable.

Here is EXG's Fact Sheet , which includes Top 10 holdings, expense ratio, etc. as of the third quarter of 2023:

In conclusion, despite the Eaton Vance equity CEFs seeing some of the worst valuation declines of all fund sponsors in 2023, ETW in the first table above being a good example, I believe that institutional shareholders will come back first to these funds in 2024 due to their size, liquidity and confidence of what Eaton Vance (now owned by Morgan Stanley ) brings to the table.

And if that happens, I believe institutions will gravitate first to the best NAV performers, then to the best valued funds and then to the most liquid funds. And that would mean EXG should be at near the top of their list.

Top ETF Picks For 2024

My last top funds for 2024 are all ETFs and I'm going to roll the dice on a couple of them.

I firmly believe you want to stay with the largest and most popular index and sector ETFs and not get caught up in all of the newer ETFs that offer newfangled strategies to offer higher yields but overall, have been very poor performers.

But there are plenty of ETFs that are directly correlated with the most popular index and sector ETFs from BlackRock's iShares and State Street's SPDRs , and frankly, they have been tough to beat in performance. The bonus is that they are generally lower priced than the indexes but can move well in excess of their underlying index.

For example, think the S&P 500 ( SPY ) had a good year up +26.4% ? Well, the ProShares Ultra 2X S&P 500 ETF ( SSO ) , $65.07 closing market price , which is directly tied to the S&P 500, was up +46.8%.

Now there weren't many stocks, funds and certainly CEFs that could beat the S&P 500 in 2023, so if that trend continues, and I think it will with the major market index ETFs, then doesn't it make sense to look at ETFs that can parlay that outperformance?

Of course, it works both ways and if the major market index ETFs and sector ETFs go down, you will see an accelerated downside in these funds too.

I should say that these first two picks are going to need a continued bull market environment in 2024 and particularly in their sectors, represented by energy and biotechnology.

Both energy and biotech were serious underperformers last year and the strategy of these picks is to leverage up any rebound or rotation to these sectors that we could see, beginning in January.

The first ETF is the ProShares Ultra +2X Oil & Gas ETF ( DIG ) , $36.74 closing market price. This is a geared (leveraged) fund that will go up (or down) twice whatever the SPDR Energy Select ETF ( XLE ) , $83.84 closing market price , performance is each day.

DIG also includes 23 of the top oil and energy company stocks which you can see below starting with Exxon Mobil ( XOM ) , $99.98 closing market price :

{kind=link}

Global X

The swap positions in the yellow highlighted boxes essentially act as the leverage to achieve the +2X daily performance of XLE. Now because DIG has to pay for this leverage, since it's like borrowed money, there will be some price decay over time.

What this means is that these funds are not necessarily for long-term hold periods though that doesn't mean you would have to sell them right away if there was a spike up in oil prices due to some global event.

You could also sell (write) call options on DIG into strength, which would more than offset the price decay if you wanted to hold onto the fund. You would just have to pick a strike price you're comfortable with (typically higher than the current price) and an expiration date in which the longer you go out, the more the time premium you take in.

So why is this an advantage over say, just buying long call options on XLE? As I've explained in past articles, you want to be a seller of options, NOT a buyer.

Here are a couple articles that explain how selling options put you in a much better position to make money than buying options:

Equity ETFs: Good Market To Write Options In - Part I

Equity ETFs: Good Market To Write Options In - Part II

So for example, if you bought two call contracts on XLE, $83.84 closing market price , out to a March 15, 2024, expiration at a slightly out-of-the-money $84 strike price, that would cost you $3.80 per contract or $760 ( $3.80 X 100 shares per contract X 2 contracts).

Or you could buy 200 shares of DIG at $36.74 for a total cost of $7,348 . Either way, you are controlling roughly the same value since 2 contracts of XLE is the equivalent of 200 shares at $83.84 or $16,768 . And since DIG moves 2X that of XLE, you're controlling roughly $14,696 with DIG.

Next, let's assume some price targets on XLE out to March 15th of 2024. Let's say XLE goes nowhere over the next roughly 10 weeks and is still around that $84 strike price or just under.

If you were long two call contracts on XLE, you're out of luck and your $760 is essentially gone. But if you held onto 200 shares of DIG instead, you may have seen a little erosion of your $36.74 basis, but not much if XLE goes nowhere over the next 10 weeks. So instead of losing $760 on long Call options at expiration, you have only a slight loss on DIG.

Now let's assume XLE goes to $89 , or a + 6% increase from $83.84 at expiration . If you're long a March 15th Call XLE $84 strike price, your option is only worth $5/contract ( $89 current price - $84 strike price). Thus, you made only $240 , $1,000 ($5 X 100 X 2) - $760 . Does that sound like it was worth it considering you could lose everything if XLE did nothing?

But if you owned 200 shares of DIG when XLE went up +6% to $89 , you would be up roughly +12% from $36.74 to roughly $41.15 . So your 200 shares has gone from $7,348 to $8,230 for an unrealized profit of $882 . Plus, your shares wouldn't expire if XLE went nowhere instead.

So we've looked at two scenarios for XLE to determine which enhanced performance strategy would give you the best bang for your buck if you thought the oil and gas sector was due for a bounce. One scenario was if XLE goes nowhere from its current price and the other scenario is if XLE goes up +6% from its current $83.84 price to say roughly $89.00 . In both of these scenarios, DIG would be the better investment.

Now lets consider what happens if XLE falls from its $83.84 current price. Well, the call buyer would certainly lose the entire $760 investment in the 2 long contracts. But if you owned 200 shares of DIG instead, XLE would have to drop over -5.0% to $79.50 for DIG to drop an equivalent $760 loss down to a roughly $33.00 price from a current $36.74 .

In fact, you would only be worse off in this scenario if XLE dropped below $79.50 , since the call option owner cannot lose any more than the $ 760 investment. But of course, the loss in DIG would be unrealized and at that point, you might want to consider adding to your position.

And if you wanted to add shares, you have a couple alternatives. You could simply buy more shares of DIG and average down in price in a continued weak oil and gas market or you could do what I did a couple months ago and sell Put options on DIG at a strike price (in my case, $33.00 ) you would be comfortable adding shares at.

Again, selling an option (in this case a put) brings in premium to you while it obligates you to buy DIG at a price lower than the current price, IF DIG drops below the strike price before expiration.

This is a strategy many new funds utilize, especially technology funds, so that they don't deploy all of their raised assets immediately in a strong market environment. They may buy half of a stock position they want to own immediately and then sell puts at a much lower strike price that they would feel comfortable buying the other half out into the future.

This way, if the market falls and their lower strike price is reached by expiration, they have averaged down on their full position. And if that lower price is not reached by expiration, well at least they get to keep the option premium and wait for another pullback. In fact, they get to keep the option premium no matter what.

Why You Should Consider Option-Writing On Leveraged ETFs Instead Of Simply Buying Leveraged CEFs

If you have been a long-time follower of my articles, you have probably already surmised by now that I am underemphasizing CEFs for income in 2024 while overemphasizing ETFs for appreciation and utilizing written options as an income alternative.

Really what it comes down to is that I want my funds to perform in lock step with their NAVs and not have to worry about picking a fund that goes up at NAV as expected but not getting any reciprocal performance in MKT price. That's what happened with many CEFs in 2023 and I just can't take that risk anymore.

I'm also convinced that the reason for this was that institutional investors were net sellers of CEFs in 2023, either due to less risky income alternatives (think fixed-income) or in the case of financial institutions like banks which may have needed to raise cash or reduce debt, less liquid positions like CEFs are generally the first to be sold.

And if that's the case, then CEF shareholders are now mostly represented by smaller, retail investors who often have different motivations about what they buy and sell than I do.

Will institutions come back in 2024? I don't know but I do believe we've seen the worst of the heavy institutional selling and I'm cautiously optimistic that if institutional money returns in 2024, it will likely follow the undervalued CEFs I still own.

But in the meantime, I'm not waiting around and I believe the best opportunities in a continued bull market lie with these geared ETFs from ProShares and Direxion that are directly tied to the performance of the major market index and sector ETFs.

Geared ETFs are not really that much different than leveraged CEFs. The big difference is that leveraged CEFs can lag in their market moves (which can be good or bad for shareholders) whereas geared ETFs will immediately reflect any change in net asset value.

The other consideration is that ETFs can have options whereas CEFs do not. In other words, leveraged ETFs can offer even greater upside than leveraged CEFs but they can also utilize the same income and defensive strategies as option-income CEFs.

So can you really get the best of both worlds with geared ETFs? It may be more work, but I believe so.

For Good Or For Worse, Options Are Becoming More Ubiquitous In Our Markets

The use of long options by investors to generate enhanced returns has grown exponentially in recent years and is a good example of how more and more investors are willing to speculate on short-term moves of the markets.

The rise of Zero Day To Expiration or ODTE options is another sure sign of this and is already affecting the daily moves of the major market indices. That's how big it has become and you can either ignore what's going on or take advantage of it.

The great thing about options is that they don't have to be speculative and can actually be quite conservative. And this is the difference between buying long options and selling covered options. Though most investors want to roll the dice and speculate using long Puts and Calls, the vast majority of them are going to lose money over time so you might as well be on the other side of that trade.

You won't win every time, but when you are selling (writing) options on positions you own, like on DIG or any of the major market ETFs, that's really just the opposite of speculative.

I feel so confident that this strategy will excel again in 2024, that I'm willing to make another one of my Top Picks for 2024 a geared ETF, also fro m ProShares .

The Proshares Ultra +2X NASDAQ Biotechnology ETF ( BIB ) , $57.15 current market price , is structured much like DIG and will have similar risks and rewards.

Only with BIB, you're hoping for an outperforming year in biotechnology after a long hibernation since the peak in August of 2021 when vaccinations for COVID-19 were peaking too.

I'm not going to go into great detail on BIB since it's simply a bet on a biotech recovery next year with even more mergers & acquisition activity. BIB's portfolio is structured like DIG's (see below), only BIB has many more individual positions in biotech companies, 262 in fact, than DIG's 23 positions in the large-cap oil & energy companies.

{kind=link}

Global X

So clearly, BIB holds many more small cap stocks that are more likely candidates for mergers and acquisitions.

What may also help the biotechnology sector in 2024 is more effective weight-loss drugs coming to market now that Ozempic has been adopted as an effective appetite suppressor and has helped power Novo-Nordisk ( NVO ) , $103.45 closing market price , to an all-time high.

Other growth areas for biotechnology include gene mapping and gene editing via CRISPR for helping genetic disorders. And one more reason could simply be the fast money crowd getting out of over-priced technology stocks and looking for other places for growth.

And biotech is a likely candidate for growth speculators since one drug breakthrough can make a company's stock skyrocket like Nvidia ( NVDA ) , $495.22 closing market price , did in May of last year.

You can think of BIB as a turbo-charged Aberdeen Healthcare Investors fund ( HQH ) , which owns many of the same large cap biotechnology names but at an attractive discount valuation and a high yield.

We just need 2024 to be a good year for biotechnology finally.

My last ETF pick is a nod to the growing influence and adoption that Artificial Intelligence is having on our economy and our society. There are a number of ETFs that now focus in AI though their portfolios, and thus performances, can be quite different.

In years past, I have included CEFs like the Virtus Artificial Intelligence & Technology Opportunities fund ( AIO ) , $17.40 closing market price , and even ETFs like the First Trust Cloud Computing ETF ( SKYY ) , $87.67 closing market price , which tends to have a lot of portfolio overlap with AI funds.

Both funds have been in my Equity CEF/ETF Portfolio Guide since 2020 and though SKYY gained + 52.2% in 2023, AIO was much more ho-hum with its performance, up +19.3% .

Y-Charts

The point is that artificial intelligence can mean anything from innovative small-cap stocks to well established large-cap technology and even industrial companies that are early adopters of artificial intelligence.

Thus, my last Top Pick for 2024 is the GlobalX Artificial Intelligence & Technology ETF ( AIQ ) , $31.18 closing market price , which is going to be more large cap stock focused simply because I believe institutions will still want to stick with large cap technology over small cap, even if small cap presents better opportunities.

AIQ though, doesn't have Nvidia as a top 10 holding, but rather Intel ( INTC ) , $50.25 closing market price , occupies its top spot.

But with 86 total holdings, there's enough diversification in AIQ to include many smaller and mid-cap stocks to the portfolio.

AIQ is one of Global X's larger funds at $900 million in assets managed and though that would still make it a small-cap security itself, defined as less than $2 billion in assets, that won't hurt an ETF like it could a CEF since ETF's will always trade near NAV. Thus, a portfolio of mostly large cap stocks in a small-cap ETF is an important feature here

AIQ returned +55.4% in 2023 but like everything in technology, timing is everything and if you go back two years, all three of these funds are still negative though AIQ has held up the best:

Y-Charts

Clearly though, we're looking at an extended market right now in large cap technology stocks and many believe the Nasdaq-100 ( QQQ ) , $409.52 closing market price, is due for a sub-par year in 2024.

So yes, the timing may not be perfect, but if you believe that artificial intelligence is still in its early stages of adoption, then you should still have exposure to this up-and-coming sector. And since I don't really own AIO anymore, AIQ is my ETF alternative.

Conclusion

I apologize for this being rather long, but when you're talking about a significant change in strategy from what I have been doing for over the last decade, you really want to explain yourself.

Frankly, the motivation to overweight equity ETFs and underweight equity CEFs is directly tied to the rise in interest rates which began in March of 2022, and which has caused a tectonic plate shifting in asset class re-distributions, including fixed-income.

Equity CEFs may get a bounce here in January but I still believe you will be better off over the course of a year in ETFs, particularly the major market ETFs, which I am already overloaded.

This may not be ground-breaking advice, but this is what worked in 2023 and I have no reason to believe it will change much in 2024. But this does not mean that all ETFs tied to the major market indexes performed well in 2023. We know that many of the option-income ETFs were serious laggards despite yields of up to +12% .

And this is why I'm also recommending that you utilize your own option write strategy on ETFs, whether it be on the major market indexes like SPY, QQQ, the Russell 2000 Small Cap Index ( IWM ) , $200.71 closing market price , or on ETFs that are sector specific like DIG, BIB and even AIQ.

This means you're going to have to be more hands on to make money in 2024 but if you have 40% of your assets in yield-oriented fixed-income investments like I do, then this only has to apply to the other 60% .

See? You can already relax and enjoy the new year!

For further details see:

Equity CEFs/ETFs: Top Picks For 2024 - Part II