QQQ - Equity CEFs: Top Picks For 2023

Summary

- 2022 was a year to forget, while most believe 2023 will begin with the same issues that took the equity and bond markets well into bear market territory last year.

- That is, a hawkish Federal Reserve that doesn't want to let up on strangling inflation into submission while draining market liquidity.

- Then there's the ongoing conflicts between Russia and Ukraine and China and Taiwan, each of which could have profound global economic ramifications, not to mention, global peace.

- With that backdrop, most market pundits believe the first quarter to first half of the year will favor fixed income products over stocks, and when you can earn almost 5% in riskless assets out a year, that's probably a safe bet in this market environment.

- But rarely does the market do what consensus predicts, and the biggest variable hanging out there is what exactly are Jerome Powell and the Federal Reserve thinking and what will they do next?

Note: All prices are as of 12/30/2022 and may have changed since this article was first released to subscribers of CEFs: Income + Opportunity on January 2nd, 2023.

I always like to start the Top Picks edition with a review of last year's picks, but since it was an extremely difficult year with the S&P 500 (SPY), $382.43 current market price , down -18.2% with the NASDAQ-100 ( QQQ ), $266.28 current market price , closing the year down a stunning -32.5% , I thought I should first begin with what I wrote on January 2nd of last year:

2021 was supposed to be the year the Federal Reserve finally got to reverse its ultra-low rates and massive market stimulus after COVID-19 and finally take charge over its balance sheet.

But the virus had the last word and so now it looks like 2022 will be the year of 'normalization' for the Fed. And what does 'normalization' mean? 'Normalization' can mean reducing the amount of stimulus, i.e. tapering, or it can mean replacing securities as they mature or it can mean letting securities mature without replacing. And of course, it also means raising interest rates to more 'normalized' levels.

So in this case, the Fed is starting from almost a maximum support and liquidity position that begins with tapering and it ends with rate hikes. The problem is, we don't know how far that goes.

Generally speaking, it will go on until either the economy or the markets say it's enough, but in either case, that's usually not market friendly.

And, boy, did that turn out to be the truth. Throw in Russia's invasion of Ukraine in February, which further put the screws to the Federal Reserve as inflation spiked, and you had all the ingredients of a bear market.

But not even the most bearish of prognosticators could have predicted the fall of some growth and technology sectors by -75% even while some value sectors, like energy, were able to rise by over +50% last year.

Such was the year in 2022, which seemed to be a flip-flop of 2020, when it was growth and technology that were the market leaders while commodities tanked.

So what will 2023 bring? I believe there are just too many unknowns and too many potential "black swan" events that could occur during the year that anyone trying to make a prediction of what the markets will do will have better luck getting answers by dusting off the Ouija board.

My personal feeling is that after such a difficult year and with so much heavy tax-loss and redemption selling in December, we should get some sort of a January effect rally to start the year.

But the problem for the markets going forward is that the Federal Reserve is probably not going to back down from their hawkish position to get to their 2% inflation target even if it means a mild recession, so it appears that no matter what the economy does, they're not going to change their tune.

And if that's the case, and most market bulls believe they WILL change their tune sooner rather than later, then you're essentially relying on positive market sentiment to take the markets higher even while fighting the Fed. And, that's a battle that investors will probably lose, even if we do get short-term oversold lifts in the market like we did in 2022.

But I still have to give my Top Picks for 2023, and before I do that, let me briefly go over my top picks from last year.

Top 2022 Overall Pick

My top overall pick for 2022 was the Eaton Vance Tax-Managed Buy-Write Strategy Fund ( EXD ), $9.19 year-end market price, $9.06 NAV, +1.4% market price premium, 9.2% current market yield, and EXD did indeed outperform its benchmark S&P 500 (SP500) during 2022, falling -17.8% for the year when you add back distributions.

EXD is one of the more defensive option-income closed-end funds ("CEFs") you can own, but like many of the option-income CEFs from Eaton Vance, they tend to offset that defensiveness by overweighting the mega-cap technology names in their S&P 500 all-stock portfolio which clearly underperformed in 2022.

Nonetheless, EXD has some things going for it, especially if the NASDAQ-100 has a better year in 2023. First, EXD's distributions are essentially tax-free due to the build-up of losses the fund had during its early years when it was a municipal bond fund while writing options.

That strategy didn't work very well, but ironically, EXD's 9.2% current market yield is essentially still non-taxable since the vast majority of the monthly distributions are made up of return-of-capital, which is non-dividend 1099 income in the year received, though you would need to reduce your cost basis by the return-of-capital amount, thus deferring the tax until you sell the position.

I'll let you figure out what a 9.2% current yield paid monthly might translate to on a tax-equivalent basis, but when you throw in EXD's option-write strategy which sells S&P 500 and NASDAQ-100 options against 96% of EXD's portfolio value, that's a super-defensive strategy that brings in a lot of option premium in case 2023 turns out to be another dud.

Finally, EXD is due to merge into its much larger sister fund, the Eaton Vance Tax-Managed Buy-Write Opportunities Fund ( ETV ), $12.28 year-end market price, sometime in the 1st or 2nd quarter of 2023, but don't worry, you won't lose that Return of Capital tax deferral as most of ETV's distributions are now Return of Capital too.

Note: For more information on Return of Capital, here's a popular article I wrote back in early 2011, CEFs and Return-Of-Capital: Is It As Bad As It Sounds? that helps explain how option-income funds can offer tax-advantaged return-of-capital in their distributions even while growing their NAVs

And here is a more recent PDF from Eaton Vance that explains how Return of Capital is considered more of a tax-concept rather than an economic one . In other words, don't take the phrase 'Return of Capital' literally:

Finally, virtually every CEF in this bear market has a lower NAV today than it did at the beginning of 2022, and some much lower, so if you own a taxable account, you might as well make lemonade out of lemons and own funds that can at least designate a good portion of the fund's distributions as Return of Capital.

Which is why virtually all of my Top Picks for 2023 are option-income funds which give you won't find any leveraged pure equity CEFs in my Top Picks for 2023, which are much more dangerous in bear markets than

And this is why you will hear me continue to endorse the Eaton Vance option-income CEFs for 2023 over-and-over again. Heck, that's why you see 'tax-advantaged' in many of the Eaton Vance equity CEF fund names.

Top 2022 Aggressive Pick

In 2022, I tried to go conservative with my aggressive fund pick and selected the Virtus Artificial Intelligence & Technology Opportunities Fund ( AIO ) , $16.19 year-end market price, $19.11 NAV, -15.3% discount, 11.1% current market yield , and though the fund's value stock exposure helped support AIO's NAV during most of the year, it was the small-cap technology and innovation portion of AIO's portfolio, which was mostly in the fund's 44% convertible security exposure of the portfolio, that suffered the biggest losses.

This is where the bear market really saw the most dramatic price declines in stock prices of up to 75% or more. And these declines in the disrupters and innovation small-cap technology space actually started in early 2021.

That said, AIO's diversified portfolio meant that AIO's NAV, down -21.9% in 2022, held up far better in 2022 than the vast majority of growth and technology focused CEFs and ETFs, and much better than the NASDAQ-100 ( QQQ ) , down -32.5% , or say the ARK Innovation ETF ( ARKK ) , $31.24 year-end market price , down -67.8% in 2022, despite ARKK and AIO owning many of the same small-cap technology disrupter and innovation stocks:

Y Charts

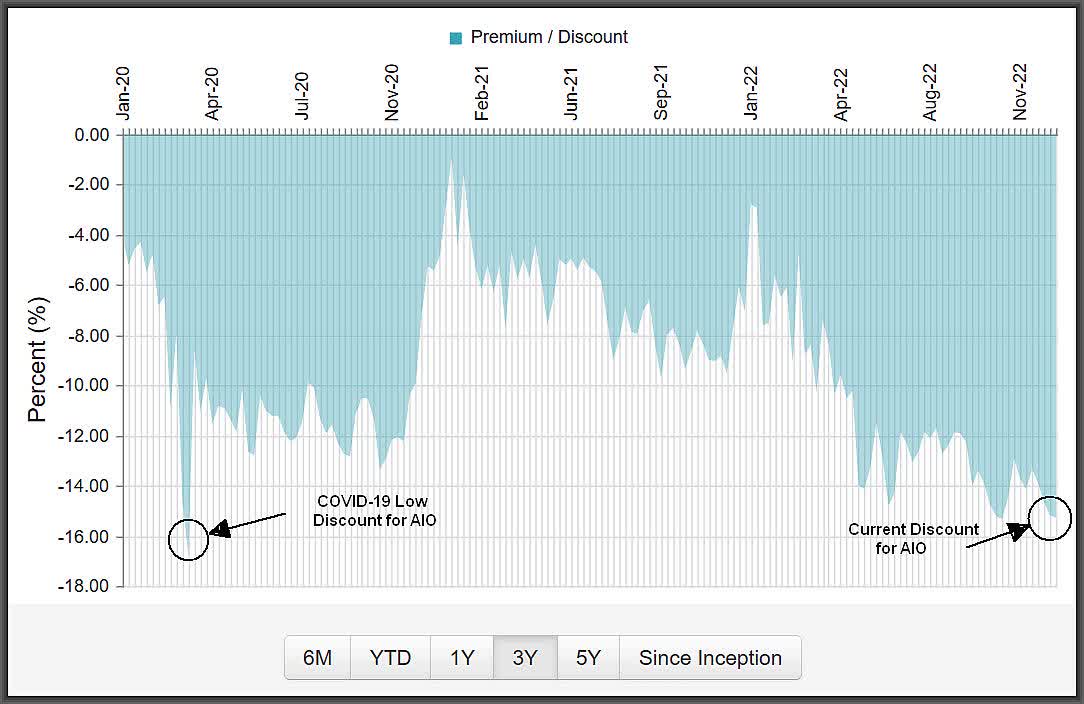

So should AIO have fallen to a -15.3% discount, the widest since the COVID-19 bear market in March of 2020? Absolutely not, but such is the market we are in currently and like many equity CEFs last year, there was significant added pressure on AIO's market price due to tax-loss selling, particularly near year end.

Here is a 3-year Premium/Discount graph of AIO from the worst of the COVID-19 days:

{kind=link}

What's remarkable about AIO is that even after going public in late 2019 at $20 per share both at MKT price and NAV price, AIO's NAV is still at a very high $19.11 today.

And that's after paying out $4.60 in capital gain distributions ( $1.15 in 2020 and $3.45 in 2021), as well as monthly distributions of another $4.60 along the way, i.e. $1.30 in 2020, $1.50 in 2021 and $1.80 in 2022, after raising AIO's distribution twice since inception from $0.1083/share to $0.15/share today.

That's a total of $9.20 in total distributions that AIO has made over the past 3-years during one of the worst periods for small cap technology and growth stocks in history, which actually started well before 2022 rolled around, and yet AIO's NAV has only depreciated from $20 to $19.11 .

That is, frankly, phenomenal and even if the technology sector continues to struggle into 2023 and a distribution cut is necessary after 2-raises, the portfolio managers of AIO have already shown their prowess in being able to maneuver through and survive anything a bear market can throw at them.

I would have made AIO my top pick again in the aggressive CEF fund category for 2023 but there's actually another fund I will discuss below that could see even better returns if the small-cap growth and technology sectors rebound next year.

Top 2022 Value Pick

I struggled with making a value pick last year and as it turns out, the Gabelli Dividend & Income fund ( GDV ) , $20.61 year-end market price, was NOT a good pick and was, by far, the biggest disappointment in what was generally, a fairly good year for value sector equity CEFs.

Unfortunately, the portfolio managers of GDV underweighted energy, which you had to overweight if you hoped to have positive performance from your fund in 2022.

Instead, GDV's largest sector exposure was in financials, healthcare, food & beverage and computer software and services, in that order as shown below.

As a result, GDV's NAV was down -14.6% in 2022 and like most equity CEFs, saw even worse market price performance, down -18.8% , as GDV's discount widened to -14.4% market price discount.

What also hurt GDV was the use of leverage, which is inherent in most of the Gabelli (GAMCO) stock based CEFs, making them some of the most volatile equity CEFs you can buy.

Most leveraged equity CEFs include some fixed-income exposure in their portfolios, usually up to 33%, to help bring down the volatility that leverage brings as well as to provide income. But not the Gabelli funds. Most of the Gabelli CEFs are pure stock based, thus making the use of leverage even greater in a bull market but not in a bear market, especially if your portfolio is not positioned in the right sectors.

Top 2022 Rebound Pick

My top Rebound Pick for 2022 was the Voya Asia Pacific High Dividend Equity Income fund ( IAE ) , $6.13 year-end market price, and for all of the turmoil coming out of China last year regarding COVID lockdowns, potential stock de-listings and expectations of a real estate collapse, IAE held up very well, only down -10.4% at NAV.

Compare that to most emerging market CEFs, which were down as much as 30% in 2022, and IAE solidly outperformed due partly to utilizing a defensive option-write strategy on most of its individual stock holdings as well as having a diversified geographic country exposure that included both emerging markets and developed markets in SE Asia.

{kind=link}

But again, like most CEFs, IAE's market price suffered worse than its NAV and closed the year down -13.8% , while seeing its discount end the year at a relatively wide -14.0% .

Still, IAE was a welcome surprise in a bear market year and at only $83 million in total assets, I'm still of the mind that Voya may end up liquidating IAE at some point, like they did with two other small equity CEFs in early 2021, the Voya Natural Resources Equity Income Fund ( IRR ) and the Voya International High Dividend & Equity Income Fund ( IID ) .

I wrote about this in this article, Equity CEFs: Will IAE Be The Next Voya Fund To Liquidate , back in April of 2021, and though it obviously hasn't happened yet, if it does, you would see an immediate windfall jump in IAE's market price to reflect the liquidation value of IAE's current NAV.

Top 2022 Specialty Pick

My specialty pick for 2022 was the Cushing NexGen Infrastructure Income Fund ( NXG ) , $38.30 current market price. NXG was my fund to take advantage of any energy and energy MLP recovery in 2022 without being fully exposed to the sectors.

Note: Cushing changed the ticker symbol from SZC to NXG on November 1st

From that standpoint, NXG performed very well, only down -1.9% at total return NAV for the year. But in hindsight, it would have been better to have selected a pure energy or pure energy MLP fund, as those sectors completely outperformed the markets.

Still, NXG should not have fallen to a -22.3% market price discount with that kind of NAV performance, and I stand by my pick, even though NXG fell -7.2% for the year. Still, that was significantly better than the broader markets.

In review, here is how my 2022 Top Picks performed at total return market price compared to the S&P 500 in which a green background shows outperformance while a red background underperformed.

| Fund |

| 12/31/2021 Price |

| 12/30/2022 Price |

| Total Distributions |

| Total Market Price Return |

| EXD |

| $12.07 |

| $9.19 |

| $0.8496 |

| -17.8% |

| AIO |

| $24.79 |

| $16.19 |

| $1.8000 |

| -27.4% |

| GDV |

| $27.00 |

| $20.61 |

| $1.3200 |

| -18.8% |

| IAE |

| $8.11 |

| $6.13 |

| $0.8600 |

| -13.8% |

| NXG |

| $44.00 |

| $38.27 |

| $2.5584 |

| -7.2% |

| SPY |

| $474.96 |

| $382.43 |

| $6.3207 |

| -18.2% |

Note: Most returns you see quoted for the S&P 500 do NOT include dividends. However, for purposes of true comparison, I include all dividends and distributions for all funds, including SPY.

Overall, not a disaster, and up until the final week of the year, EXD was down only -13.0% but fell another -5% during the last week to more closely reflect the current valuation of ETV, the fund it will be merging into sometime in the first half of 2023.

Also, Virtus doesn't give a benchmark for AIO, probably due to AIO's unique income and growth strategy that includes convertible securities, equities and even high-yield bonds, so considering AIO's technology and growth lean in the convertibles and stock portion of the portfolio, AIO's benchmark should be closer to something more aggressive, like say the Russell 1000 Growth ETF ( IWF ) , which was down -29.3% last year.

With that, let's move on to my 2023 Top Picks.

Top 2023 Overall Pick

My top overall pick for 2023 is the Eaton Vance Tax-Managed Global Buy/Write Opportunities Fund ( ETW ) , $7.76 year-end market price , $8.38 year-end NAV, -7.4% market price discount, 9% current market yield .

ETW is one of Eaton Vance's more defensive option-income CEFs, selling index options against a very high 96% of the fund's all large-cap global stock portfolio.

If you go to pages 7-8 of the PDF below, you'll see the rolling options on the S&P 500 and NASDAQ-100 primarily but because ETW is a global stock fund, there are also written options on the Dow Jones Euro Stoxx 50 Index and the Nikkei 225 Index.

Because of Eaton Vance's size and number of option-income funds they manage, they are the only fund family that is able to write rolling options that expire every few days to a week out such that when one option expires, another is put on roughly a month out.

What this means is that the Eaton Vance option-income funds are much less susceptible to poor timing than the monthly option expirations that most fund families utilize. This is something that is not widely recognized but is a major advantage to the Eaton Vance option funds.

I believe option-income funds will see a significant edge in 2023 over leveraged funds not only because of the uncertainty of what the new year will bring but also due to the cost of leverage, which keeps going up along with short-term rates.

Option-income funds perform best in up and down markets in which no clear trend is seen. Though it's hard to predict whether funds that have a high exposure to the growth and technology sectors will see a rebound in their equity holdings this year or if funds that focus in value sectors like financials, healthcare and energy will see continued outperformance, but with option-income CEFs, at least the strategy can compensate to a degree if the portfolio holdings are overweight in the wrong sectors.

This is what happened to many of the Eaton Vance option-income CEFs in 2022. They had been overweight the mega-cap NASDAQ-100 ( QQQ ) technology names for years and what worked in years past did not work in 2022 when the QQQ's were down -32.5% with many component stocks in the index down much more than that.

But because of the written option strategy of the Eaton Vance equity CEFs, their NAV losses were largely mitigated even while having a large exposure to growth and technology stocks.

I believe that if 2023 turns out to be a positive year for stocks, then growth and technology stocks will probably offer the best upside simply because of how far they fell last year.

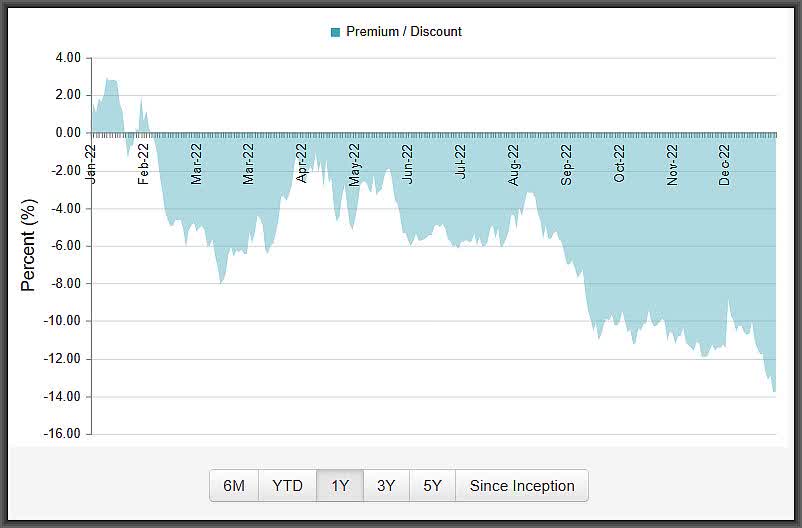

But it certainly will not be without bumps along the way. So, from that perspective, I believe the option-income CEFs from Eaton Vance should perform much better in 2023 and ETW with its global stock portfolio, a high option-write percentage and now at the widest discount since COVID-19, offers one of the best risk/rewards among all CEFs.

Top 2023 Aggressive Pick

My top aggressive pick for 2023 is the BlackRock Innovation & Growth fund ( BIGZ ) , $6.81 year-end market price, $8.82 year-end NAV, -22.8% discount, 12.3% current market yield.

Though BIGZ had one of the worst NAV performances of all equity CEFs in 2022 year, down -41.3% , the fund has also fallen to a -22.8% discount after starting last year at about a -10% discount.

That, in and of itself, is a strong incentive for some kind of an improvement now that 2022

Owning BIGZ right now would be sort of like owning the ARKK Innovation fund ( ARKK ) , $31.24 year-end market price , at a further -22.8% drop in price, or at about $24 a share.

Once you look past the rout in market prices of the stocks and sectors BIGZ invests in, which are mostly small-cap technology and innovation stocks you've probably never heard of, you realize there's a lot of bad news already built into BIGZ's price.

The other positive with BIGZ is that the huge discount means a current buyer would receive a 12.3% current market yield paid monthly, while the fund only has to cover a reasonable 9.5% NAV yield.

It's clearly been a rough ride for BIGZ since its inception at $20 in March of 2021, but this is one of those risk/reward ideas in which clearly, the reward outstrips the risk.

Top 2023 Value Pick

Voya finally found a year in which its value sector strategy worked for most all of its equity CEFs. And one Voya fund, the Voya Global Advantage And Premium Opportunity fund ( IGA ) , $8.70 year-end market price, $9.96 year-end NAV, -12.7% discount, 9.1% current market yield , had a fantastic year with its NAV down only -1.6% .

I believe IGA's outperformance continues in 2023, and thus I will make IGA my top 2023 value fund pick. IGA includes a diversified value sector exposure with roughly 70% of its global stock portfolio in either financials, health care, industrials, consumer staples or energy stocks.

{kind=link}

Combine that with a fairly low 37.5% option-write strategy on individual stock holdings (Latest Top 10 holdings shown below), and a wide -12.7% market price discount, and IGA should be a safe bet no matter how the markets perform in 2023.

Voya Investments

Top 2023 Rebound Pick

Pretty much any pick could be a rebound pick after last year but my top rebound pick for 2023 is going to be the Tekla Healthcare Investors fund ( HQH ) , $18.00 year-end market price , $20.88 year-end NAV , -13.8% market price discount , 8.7% current market yield .

Let's face it, when you combine the experience and research capabilities of Tekla and its portfolio managers in the biotechnology and healthcare sectors, eventually the market is going to recognize that.

I'm not sure why HQH has fallen to such a wide discount when its NAV was down only -7.0% in 2022, but I'm pretty sure it has to do with what has caused a lot of equity CEFs to lose valuation, distribution cuts and tax-loss selling.

{kind=link}

With HQH's market price down -17.1% in 2022, thus resulting in the widening discount of -13.8% , I believe this represents one of the best entry points in HQH's history going back to 1987 when it was founded by the San Francisco Bay Area firm of Hambrecht & Quist.

I remember Hambrecht & Quist very well from my days with Morgan Stanley in San Francisco, and they were a major player in helping underwrite many technology and biotechnology companies at the time. And this is why you still see HQ in the ticker symbols for Tekla's ( HQH ) and Tekla's Life Sciences fund ( HQL ) .

HQH uses a slight bit of leverage on its mostly all-stock portfolio, but not enough to get it into too much trouble. Here is HQH's top 10 holdings, which you would probably find among any biotech fund:

Tekla Capital

From a sector allocation perspective, HQH is 53.4% in biotechnology stocks, 20.3% in pharmaceuticals and 8% in healthcare providers & services.

But what it really comes down to for HQH is valuation and portfolio management and since the biotech industry is driven more by medical breakthroughs, FDA drug approvals, mergers and buy-outs, and not necessarily by economic or Federal Reserve decisions or influences, HQH should be somewhat insulated from the markets in general, just in case we end up in another down year.

And as long as COVID or other global diseases continue to be a threat to humanity, there's a good chance that HQH and really, all of the Tekla funds, will be part of that first line of defense against future pandemics, and hopefully make some money along the way.

Top 2023 Specialty Pick

Many of you who have followed me over the years know that I was a big bear on the PIMCO Global StocksPLUS & Income Fund ( PGP ) , $6.93 year-end market price , $6.91 year-end NAV, +0.3% market price premium, 12.0% current market yield , when it was at 60% to 100% market price premiums and north of $20 market prices.

Well, today, after writing multiple articles in years past on why PGP would have to dramatically cut its distribution and see a significant price fall, PGP is now at $6.93 and only a slight +0.3% premium.

After cutting its distribution four times since 2016 and some -62% from its inception high of $0.1834/share per month to a current $0.069/share per month, I believe it's time to take a chance on PGP at par valuation instead of a 100% market price premium.

Understand, it was never about PGP's aggressive income and appreciation strategy, which combines a highly leveraged multi-sector bond fund that takes some of that income and establishes a very large E-mini long option on the S&P 500 ( SPX ) .

The problem I had with PGP going back to 2013 was that it was always about PIMCO maintaining PGP's original 2005 inception distribution for way too long even as PGP's NAV yield rose to over 20% . That was way too high and I argued that even with PGP's uber aggressive strategy, the fund could not reasonably be expected to cover that NAV yield.

And yet, for years, shareholders of PGP thought the fund could do no wrong even as it rose to 60% and even 100% market price premiums, while I argued the monthly distributions were unsustainable.

For example, here was an article from April of 2019, Equity CEFs: You Should Be Listening To Me , when PGP cut its distribution a third time from $0.122/share to $0.0939/share and which includes links to as far back as 2013 when I first started writing on PGP.

PGP is not unlike a lot of the multi-sector bond funds from PIMCO which specialize in highly leveraged portfolios of high-yield corporate bonds, investment grade corporate bonds, government mortgage-backed securities, other government and sovereign bonds, etc.

The difference is that PGP also ventures into S&P 500 options, hence the StocksPLUS in its name. This adds a very aggressive component to PGP's strategy in an already very aggressive leveraged fixed-income portfolio. So if the fund's strategy is hitting on all cylinders, PGP can have incredible NAV market price and NAV upside.

But unfortunately, in 2022 both bonds and stocks suffered their worst combined sell-off in history and as a result, PGP's NAV fell -27.0% . But I'm betting that at least one of PGP's strategies, either bonds or stocks, will turn it around in 2023 and will outperform. And if both bonds and stocks do well, look out!

Conclusion

With many equity CEFs finishing the year close to their 52-week market price lows and near their lowest valuations since COVID-19, this is about as good a time to invest in these funds as I've seen in years.

But not all equity CEFs are going to be attractive. Except for oil and energy focused funds, almost all CEFs lost NAV last year, some significantly, so it makes sense to focus on funds that can at least take advantage of the NAV loss and can include a higher percentage of Return of Capital in their distributions.

Note: Intended for taxable accounts that can take advantage of Return of Capital.

With that in mind, I've tried to include mostly option-income funds in my 2023 top pick selections since they generally can offer a higher Return of Capital in their distributions without necessarily including destructive Return of Capital . This is in contrast to leveraged-income CEFs in which any Return of Capital in their distributions is usually going to be of the destructive kind.

The only heavily leveraged-income CEF among my 2023 picks is PGP, but remember, PGP is mostly in fixed-income securities. Leveraged-income equity CEFs can generally offer greater appreciation potential than option-income CEFs, though leveraged-income equity (not necessarily bond) CEFs will need an up year in stocks.

And there are no guarantees that we will see an up-stock market in 2023.

For further details see:

Equity CEFs: Top Picks For 2023