HQL - Equity CEFs: What's Going On With Tekla's HQH And HQL?

Summary

- The iShares Biotechnology ETF (IBB) is down -12.9% year-to-date but the Tekla biotech equity CEFs are down even more despite NAVs that are holding up extremely well.

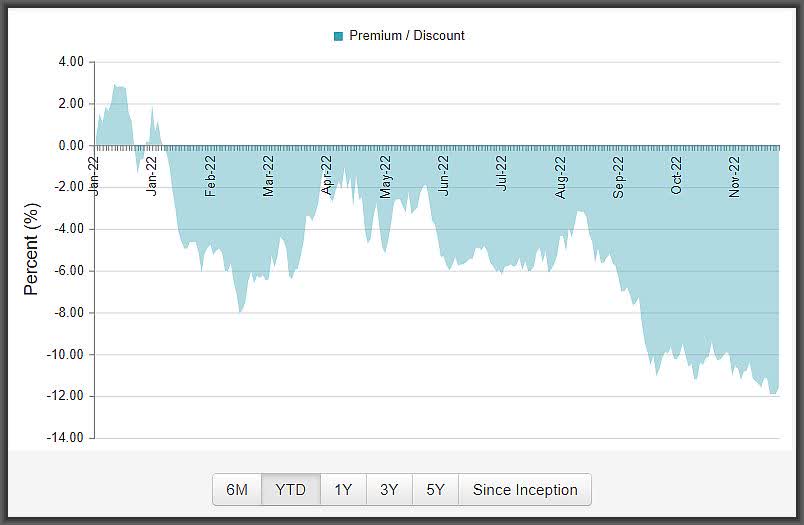

- The result is that the Tekla biotech CEFs (HQH) and (HQL) keep dropping to lower-and-lower valuations with HQH now at a -11.6% discount and HQL at a -12.0% discount.

- Why is this happening? Frankly, I'm not sure. The funds don't use leverage and they invest in many of the same biotech stocks as IBB and the SPDR Biotech ETF (XBI).

- Could it be a declining distribution each quarter? Each fund pays 2% of NAV each quarter so, in a bear market, the funds have seen drops each quarter this year. HQH, for example, has gone from $0.48/share in March to $0.44 in June, $0.40 in September and $0.39 just last week.

- But that shouldn't be a reason to sell, and in fact, is a reason to buy since the distribution will never be a burden to the NAV. I believe this is an excellent opportunity to own these funds at double digit discounts as I see no reason why these funds should be penalized for their NAV outperformance.

Note: This article appeared to subscribers of Equity CEFs: Income + Opportunity last week on Nov. 29 and is an example of real-time ideas presented in the service.

The Tekla Healthcare Investors fund ( HQH ) , $18.62 current market price , and the Tekla Life Sciences Investors fund ( HQL ) , $14.63 current market price , have been far outperforming their benchmarks at total return NAV, with HQH down only -5.5% YTD and HQL -7.9% (see below).

So why are their market prices underperforming by this much resulting in a ramp down valuation this year? If someone can come up with a better reason than a declining distribution each quarter of this year, I'd like to hear it.

Here is HQH's YTD Premium/Discount chart:

{kind=link}

CEF Connect

At 2% of NAV each quarter, both funds will be paying out an 8% annual distribution, which is very reasonable considering the funds do not generate enough income to cover the NAV yield from their portfolio even with the convertible preferreds.

You're essentially betting that the portfolio will be able to generate roughly 2% appreciation each quarter, which is very reasonable in a bull market but certainly more difficult in a bear market. But because the distribution will adjust each quarter based on the prevailing NAV, the 2% should never be a burden to the NAV, unlike many CEFs that keep their high distributions even as the NAV deteriorates.

That's a major positive for the funds even though we've seen the distributions adjust downward each quarter this year. So even though HQH's distribution is now $0.39/share , its lowest since 2013, a current investor can still receive a windfall 8.4% current market yield based on the discount. And if the funds see an increase to NAV in 2023, their distributions will rise too.

I don't quite understand the negativity in HQH and HQL, particularly if it's entirely based on a declining distribution. The Tekla portfolio managers have done an outstanding job in putting together a portfolio of biotech stocks and biotech convertible preferreds ( 7.8% of HQH's total portfolio) that are dramatically outperforming their benchmark ETFs, the iShares Biotechnology fund ( IBB ) , $132.89 current market price and the SPDR S&P 500 Biotechnology fund ( XBI ) , $79.65 current market price, funds that barely even offer a yield.

Here are HQH's top 10 holdings as of 9/20/2022:

Tekla Capital

I'm not going to get into the portfolio holdings but Tekla, particularly HQH, tends to stick with the larger and more established biotechnology and pharmaceutical companies, while HQL focuses more on the biotech and life sciences side.

That is reflected in their sector breakdowns in which HQL has the higher biotechnology exposure at 72.3% while HQH has the larger pharmaceutical exposure at 20.3% (below):

HQL

Tekla

HQH

Tekla

Clearly however, Tekla, which used to be the old Hambrecht & Quist (hence the HQ in the ticker symbols), has immense experience in the biotechnology and pharma sectors. Hambrecht & Quist was a major investment banker in the San Francisco Bay Area for technology and biotechnology firms and I remember them well during my years at Smith Barney and Morgan Stanley in San Francisco.

Though the markets may struggle a bit from now until year-end with mounting concerns over earnings and a looming recession, that really shouldn't impact the biotech space like it would other sectors.

I'm going to start a position in HQH here with a limit $18.55 buy price. HQH has the more conservative portfolio compared to HQL and is the larger of the two funds at about $1 billion in total assets.

YCharts

YCharts

For further details see:

Equity CEFs: What's Going On With Tekla's HQH And HQL?