ERH - ERH: A Decent Discount Opens Up For Utility And High Yield Exposure

2023-08-06 06:45:41 ET

Summary

- ERH is a closed-end fund that invests in utility and high-yield bonds and offers investors a monthly distribution based on a managed policy.

- The fund's discount has widened, making it a more attractive option for investors.

- ERH's distribution policy varies monthly but is predictable, and it rewards shareholders when things are going well.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Allspring Utilities and High Income Fund ( ERH ) takes a fairly odd approach to invest in, exactly as its name would suggest, utility and high-yield bonds. While a somewhat odd approach when initially thinking about it, this isn't the only closed-end fund that takes this approach. At the end of the day, these two types of investments can actually pair well together as income generators.

The last time we gave ERH a look was when the fund was at a shallow discount. Since then, the fund's discount has expanded to a more attractive level where the fund could be considered. Along with the more attractive discount, shares are under pressure as well as utilities are performing poorly in 2023. Utilities performing poorly have a lot to do with NextEra Energy (NextEra Energy, Inc. (NEE)), and we'll discuss that below.

ERH Performance Since Prior Update (Seeking Alpha)

Taking these two points into consideration, ERH is a more tempting fund today than it was last November.

The Basics

- 1-Year Z-score: -1.06

- Discount: -8.59%

- Distribution Yield: 8.16%

- Expense Ratio: 0.98%

- Leverage: 21.8%

- Managed Assets: $103.76 million

- Structure: Perpetual

ERH's investment objective is "a high level of current income and moderate capital growth, with an emphasis on providing tax-advantaged dividend income."

To achieve this objective, the fund will simply invest "approximately 70% of its total assets to a sleeve that places a focus on common, preferred and convertible preferred stocks of utility companies and approximately 30% of its total assets to a sleeve of U.S. dollar-denominated below investment grade (high yield) debt."

The fund's expense ratio is fairly low when compared to its peers. However, the fund is leveraged, and even if it is fairly modestly leveraged, that will still add borrowing costs. Those borrowing costs have also been rising quite materially as the Fed has been bumping up interest rates. The total expense ratio comes to 2.19% as of February 28th, 2023 . That's up from the 1.25% at the end of the fund's last fiscal year, 2022.

Another consideration for investors before diving into this fund is the small size. That can often result in fairly low daily trading volume and can make entering or exiting the fund with large positions difficult. The average daily trading volume comes to around 14k.

Performance - Attractive Discount

General discount widening, weaker performance and overall caution on adding leveraged instruments seem to be what is impacting ERH. The latest discount puts it well below the last decade's average. However, it was mostly overpriced through 2020 and through most of 2022. So that's likely skewing some of the average higher, but this still represents an attractive entry level for investors that would have been waiting on the sidelines to add.

Ycharts

When comparing to peers, we can take a look at Virtus Total Return Fund (Virtus Total Return Fund Inc. (ZTR)) and Franklin Universal Trust (Franklin Universal Trust (FT)). While these fund's names don't make it as glaringly obvious what they invest in, they actually invest similarly. ERH is a roughly 70/30 split between utilities and high-yield bond exposure.

ZTR takes a similar approach at 60/40, with equity utility-like positions being the largest exposure and then fixed income. However, their portfolio leans into some industrial and energy exposure on the equity side. Additionally, the fund's fixed income is spread across the credit rating spectrum and not targeting just high yield.

FT takes an approach of 60/40, but the fixed income sleeve is the largest portion of the fund, with utility equity positions being the smaller side of the pie. The credit quality of the fixed-income is predominantly high yield.

Armed with the general idea of how these funds differ, we can see that ERH has been the dominant fund in terms of total NAV return. However, the total share price return has been lacking.

Ycharts

Interestingly though, all three of these funds are showing some decent discounts. What caused this divergence between the returns is that ERH was trading at a narrower discount when this time frame started, and then that discount widened out. ZTR appeared to have followed a somewhat similar trajectory in terms of discount/premiums, whereas FT has generally maintained a deep discount for an extended period of time.

Ycharts

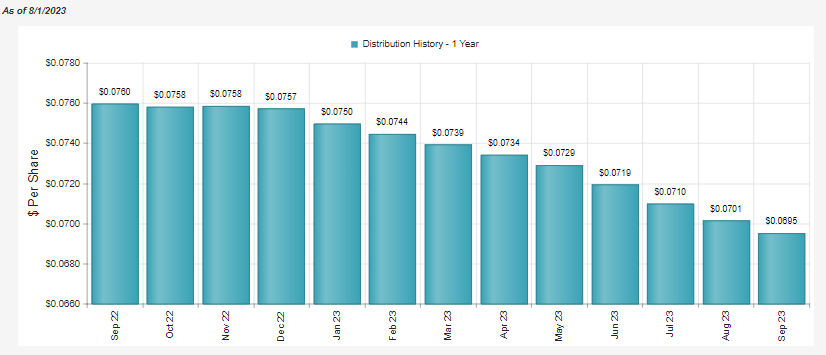

Distribution - Managed 7% Plan Adjusted Monthly

One area that investors may find ERH less appealing is the distribution policy. It leaves it predictable but variable each month. The fund pays a 7% rate based on the average NAV of the previous 12 months. As NAV goes lower, so does the distribution and vice versa. This allows for a reduced distribution when the fund is performing poorly but also rewards shareholders when it's doing better.

This isn't necessarily a bad policy, but some investors don't like the fact that it changes monthly. We've also been in an extended period of downturn for this fund, so the trend of the payout has also been going in the same direction. This could be adding to some of the pressure in widening out the fund's discount.

{kind=link}

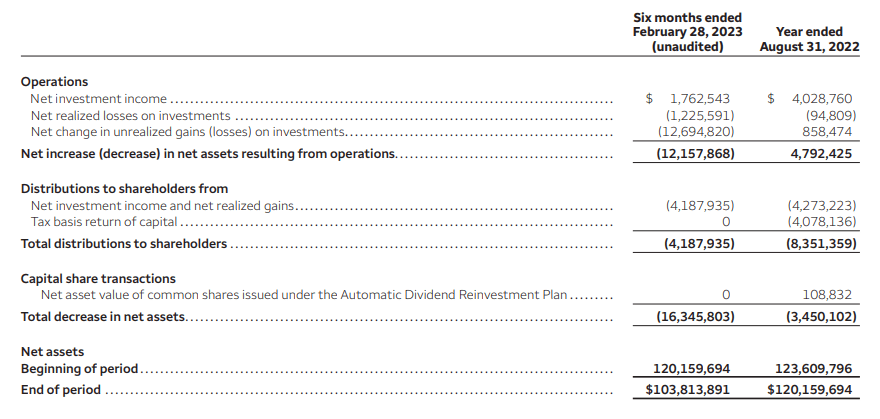

The fund's net investment income decreased in the last six months relative to the prior fiscal year. On a per-share basis, it was $0.43 for the entirety of fiscal 2022 and came in at $0.19 for the last six-month report.

{kind=link}

This was primarily driven by the higher interest rates bumping up the borrowing costs. Interest expenses last year for the same reporting period came in at $109,977. This rose to $670,173 this year. That offset the increase in total investment income, which went to $2.971 million from $2.721 million. Professional fees and shareholder report expenses also rose modestly.

We can also see that the fund performed poorly during this reporting period due to the sizeable unrealized losses experienced as well as the realized losses the fund also took.

For tax purposes, the fund's classifications in the last two years were quite different. Ordinary income was fairly consistent, but long-term capital gains and return of capital characterizations were materially different. Ordinary income should be a fairly regular classification thanks to the fund's fixed-income approach. It's when equities get involved that can cause some volatility - not only in the underlying asset itself but for tax purposes as well. This is one reason why it can be difficult to invest in CEFs for tax-sensitive investors. You never quite know what taxes might be from year to year for some funds.

{kind=link}

ERH's Portfolio

In terms of portfolio turnover, the fund can be fairly active. However, in recent years they've slowed down their pace of buying and selling. The last report showed a turnover of 10% for a six-month period. Fiscal 2022 saw a 23% turnover, with 2021 at 34% and 2020 at 68%. However, in years 2019 and 2018, we saw turnover come in at an elevated 131% and 109%, respectively. In late 2021 , this fund was sold off by Wells Fargo and rebranded to Allspring. However, no investment policy or objectives changed at that time.

Despite having a sizeable sleeve of fixed income, they don't provide a duration or average maturity for their fund. However, we can see that they hold quite a number of different positions at 262. This is often one of the strategies when investing in below-investment-grade securities, which is to own many of them in case/when a few default. The data being shared here is from the end of March 31st, 2023, as that's the period reflecting the latest fact sheet being available.

ERH Fund Characteristics (Allspring)

Despite not providing an average maturity, the fund does break down ranges of maturities where we can see that 3 to 5 years is the highest allocation, followed by 1 to 3-year maturities. This can be fairly consistent with high-yield bond exposure keeping lower relative maturities when compared to higher-rated debt. Investors want their money back faster generally when debt instruments are lower rated because then there is less time for a negative event to take place and seeing the issuer default. With shorter maturities, there is generally going to be a lower duration that goes along with it.

ERH Fixed-Income Maturity Schedule Breakdown (Allspring)

When looking at the fund's allocation of sector exposure, the largest is going to be to utilities, which comprise the overwhelming majority of the fund's equity allocation. The fixed-income sleeve takes a more diverse approach by investing across smaller allocations to many different sectors.

ERH Sector Allocation (Allspring)

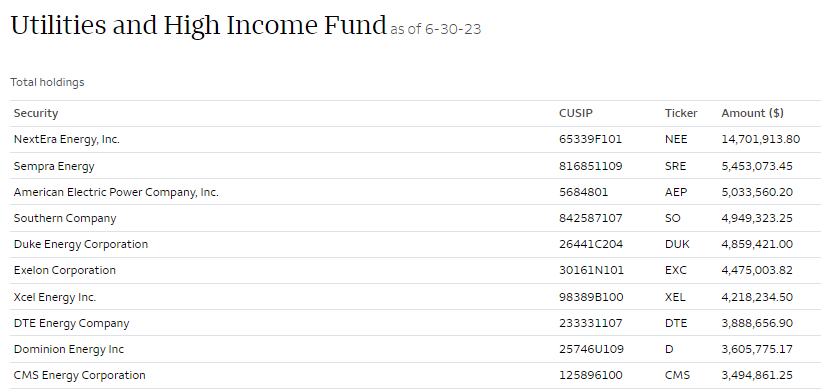

In looking at the total holdings, we get a more updated holding list as of June 30th, 2023.

{kind=link}

Here we can see NEE is the largest position by a meaningful weight. This is fairly typical for utility and infrastructure funds. In fact, the Utilities Select Sector SPDR ETF (XLU), which is often the gauge for the utility sector, owns a 15.11% weighting itself.

That's worked out well over the long term, as NEE has been a strong performer. It's actually probably one of the reasons that NEE has become such a dominant position in the utility and infrastructure space overall.

Ycharts

However, when we take a look at the shorter term, specifically on a YTD basis, having one position command such a high allocation can be bad news when things aren't going well. NEE isn't the worst performer, as Dominion Energy (D) takes that crown. In terms of allocation weighting, though, NEE being the second worst performer at a position that is four times its allocation, is going to have a much more detrimental impact. Thus, one of the leading factors of why utilities are performing so poorly themselves. Although admittedly, the whole sector isn't necessarily looking like their on fire, with higher interest rates causing downward pressure.

Ycharts

It's similar to the same reason why the S&P 500 or Nasdaq appear to be performing so well this year. A huge concentration in the magnificent 7 that have put up amazing results really has dragged up the whole 'market' barometer.

In the case of utilities, it's just simply the reverse. An overconcentration in NEE that's performed poorly has really wiped away what could be seen as decent relative results from Southern Company (SO), DTE Energy (DTE), Exelon Corp. (EXC) and Sempra (SRE). While these positions are specific to ERH's top ten holdings as reflected as of the end of June, these also mirror closely with XLU's top holdings.

XLU Top Ten Holdings (Seeking Alpha)

Conclusion

ERH is at a better valuation relative to where it was when we last took a look at the fund. Widening discounts, weaker performance and some aversion to leveraged instruments are likely some of the factors at play. The constant reduction in the distribution could also be another factor, albeit a factor that is predictable based on the managed distribution policy that resets monthly based on a 7% average NAV rate. Aside from just being cheaper than when we last looked at the fund, it's also cheaper relative to its longer-term history, which also makes it a more appealing option at this time to consider.

For further details see:

ERH: A Decent Discount Opens Up For Utility And High Yield Exposure