ESAB - ESAB Corporation: Upside Exists Despite Recent Bottom Line Weakness

Summary

- ESAB Corporation has had a lumpy operating history, but the overall picture for the business in recent years has been positive.

- This year, the firm has faced some pressure on its bottom line, but sales do continue to climb nicely.

- Add in how shares are priced, and the company looks to be a decent play with some upside potential to offer.

Although the economy has long since made the transition from being industrialized to being data-centered, the fact of the matter is that we utilize industrial activities more than we ever have before. The large structures that we build, the equipment that we use, and so much more that makes the economy function, all require some degree of construction. One company dedicated to helping this process play out is ESAB Corporation ( ESAB ). Over the past few years, the financial trajectory of the company has been a bit mixed. Having said that, the overall trend is mostly positive. This year, the firm has faced some pressure on its bottom line. But on the whole, the company seems to be a rather solid operator in its space. Given these factors, and after considering how shares are priced today, I believe that the company is likely to see its stock outperform the broader market. Because of this, I've decided to rate the enterprise a soft ‘buy’ for now.

A niche industrial provider

According to the management team at ESAB Corporation, the company formulates, develops, produces, and supplies consumable products and equipment for use in the cutting, joining, and automated welding activities that are required to make the modern world exist. It also is involved in the production and sale of gas control equipment. To truly understand the company though, it would be best to dig into its individual operations. For instance, during the 2021 fiscal year, welding consumables accounted for roughly 69% of the firm's sales. Examples here include electrodes, nozzles, shields, and tips.

The company's equipment, meanwhile, accounts for roughly 31% of sales. Specific examples here include portable welding machines, large customized automated cutting and welding machines, and more. Also included in its business activities are the software and various digital solutions that they deploy in order to help its customers increase their own productivity, remotely monitor their welding operations, and to digitize their necessary documentation. It's also worth noting that, while the company is a US firm, only about 41.4% of all of its revenue comes from the Americas, while 36.8% of its profits come from the same region. By comparison, the rest of its sales and profits come from a combination of the EMEA (Europe, Middle East, and Africa) regions, and the Asia Pacific region.

One important note to make is that there is some litigation risk with this particular firm. You see, not long ago, the business was actually part of a larger enterprise called Colfax, with the remaining entity called Enovis Corporation ( ENOV ). It was split off and, during that process, ESAB Corporation received some subsidiaries that carry future asbestos-related liabilities with regard to pending and future unasserted claims. Truly, this creates a potentially massive liability for the company. As of the end of its 2021 fiscal year, for instance, the business had 14,559 unresolved asbestos claims. The average cost of resolved claims during that year came out to $8,421. Assuming that these unresolved claims are the only ones that ever arise and that the aforementioned average cost continues to hold, that would translate turn around $122.6 million in potential expenses. Having said that, in 2021 alone, the company reported 4,393 claims as having been filed. That's a similar number to what it saw in each of the prior two years. This means that it is an ongoing issue for investors to pay attention to. As of the end of the third quarter of 2022, the total asbestos liabilities on the company's books came out to $271.6 million. However, this was offset to some degree by a similar amount, about $240.1 million, of asbestos insurance assets.

{kind=link}

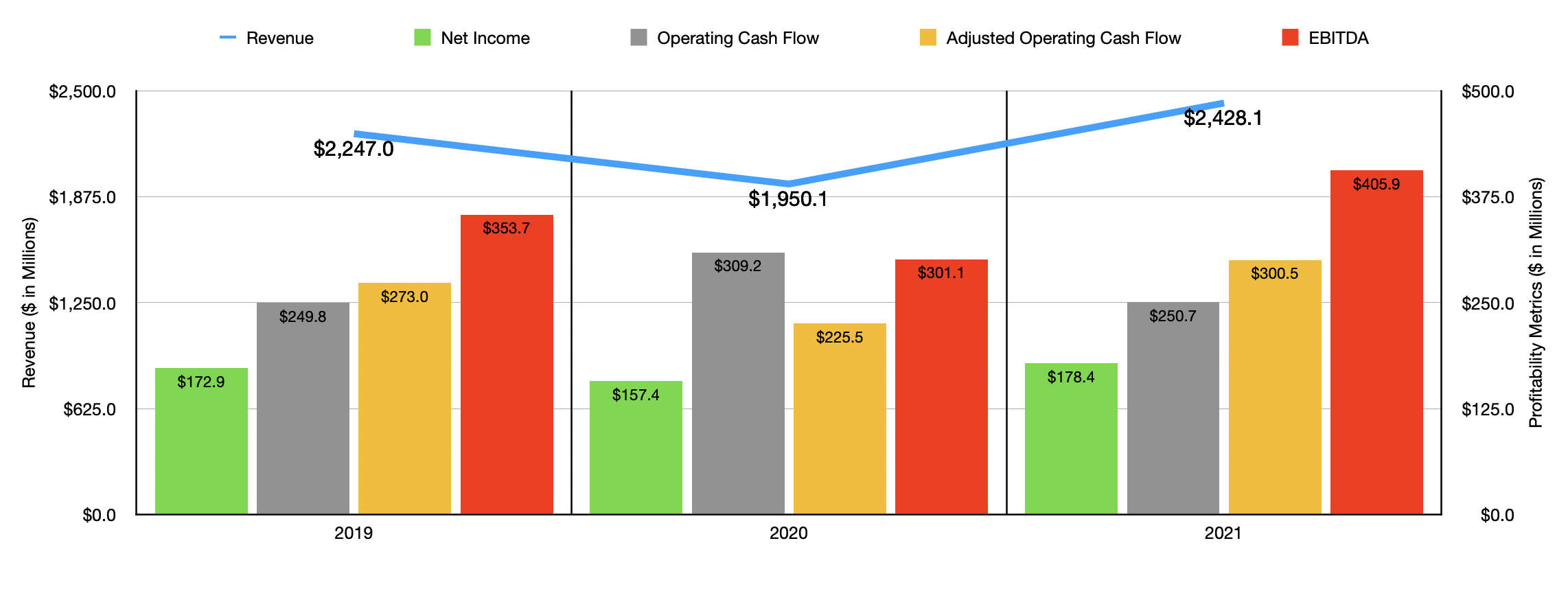

Over the past three years, the financial picture of the company has been somewhat mixed. In 2019, for instance, the firm generated a revenue of $2.25 billion. This dropped to $1.95 billion in 2020 before rebounding to $2.43 billion in 2021. On the bottom line, the picture has been similarly volatile. Net income, for instance, dropped from $172.9 million in 2019 to $157.4 million in 2020. In 2021, this number shot up to $178.4 million. That same kind of volatility can be seen by looking at other profitability metrics as well. Operating cash flow, for instance, has ranged between $249.8 million and $309.2 million over the past three years. If we adjust for changes in working capital, the range was between $273 million and $300.5 million. And finally, when it comes to EBITDA, the firm reported a drop from $353.7 million in 2019 to $301.1 million in 2020 before experiencing a rebound to $405.9 million in 2021.

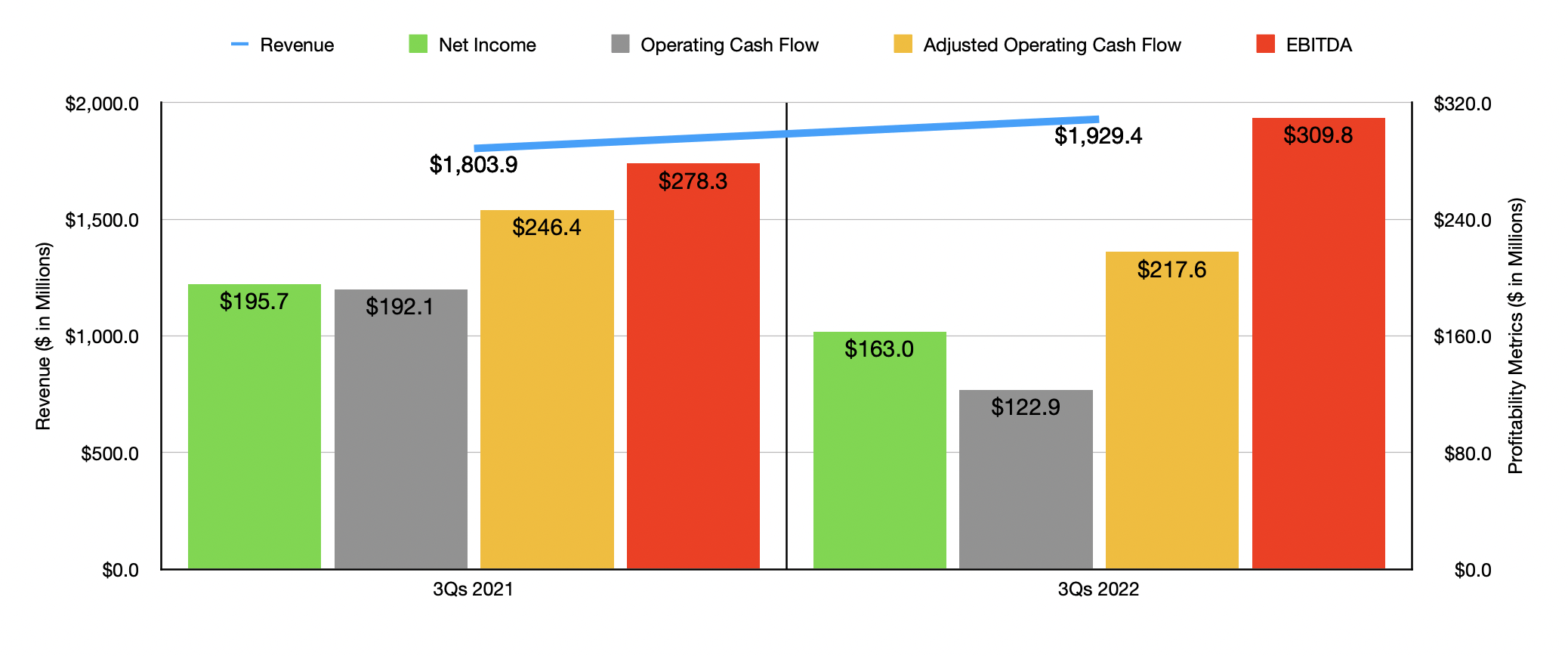

Similar volatility was also experienced throughout 2022. For the first nine months of the year, sales of $1.93 billion beat out the $1.80 billion reported one year earlier. Interestingly, sales growth would have been larger had it not been for a $74.2 million impact associated with foreign currency fluctuations. Actual organic growth from the firm's existing businesses totaled $199.7 million. Although I already mentioned the asbestos exposure, it is also important to note that the company has some exposure to Russia as well. In the first nine months of 2022, this amounted to revenue of $72.7 million.

{kind=link}

Net income, meanwhile, actually took a hit, dropping from $195.7 million to $163 million. Part of this pain came from a decrease in the company's gross profit margin from 34.7% to 34.3%. Although this may not seem like a significant disparity, it alone impacted profits to the tune of $7.7 million on a pretax basis. A rise in restructuring and other related charges, as well as higher income tax expense, both negatively impacted the business as well. This brought other profitability metrics down with it. Operating cash flow, as an example, dropped from $192.1 million to $122.9 million. Even if we adjust for changes in working capital, the metric dropped from $246.4 million to $217.6 million. In fact, the only profitability metric that improved during this time was EBITDA. Based on the data provided, it rose from $278.3 million to $309.8 million.

For 2022 in its entirety, management said that total core sales should rise by between 5% and 7%. The company defines ‘core’ as excluding results from Russia. Actual organic revenue from its core operations should grow an even more impressive 11% to 14%. The difference between the two is mostly associated with pain from foreign currency fluctuations. The company said that core adjusted earnings per share should be between $4 and $4.10. At the midpoint, that would translate to net income of $151.9 million. The company is also forecasting core EBITDA of between $405 million and $415 million. No guidance was given when it came to other profitability metrics. But if we annualize the adjusted operating cash flow figure, we should anticipate a reading of $268.7 million.

One thing that makes the company difficult to value is the fact that management made, subsequent to its third-quarter earnings release, an acquisition of a firm called Ohio Medical. That cost the business $127 million but brings with it an additional cash tax benefit with a net present value of $15 million. Overall sales from that entity should be around $45 million annually, with EBITDA margins in excess of 20%. Using the 20% member to be conservative, that should increase EBITDA for the company by roughly $9 million. The credit facility that ESAB Corporation has recently had a weighted average interest rate of 3.82%. Shipping this out and factoring in a 21% tax rate would imply a cash benefit to the company each year of $3.3 million. Both the net income figure and the operating cash flow figure I mentioned above include this in the equation. The EBITDA figure does not. With that factored in, EBITDA at the midpoint should be roughly $419 million.

{kind=link}

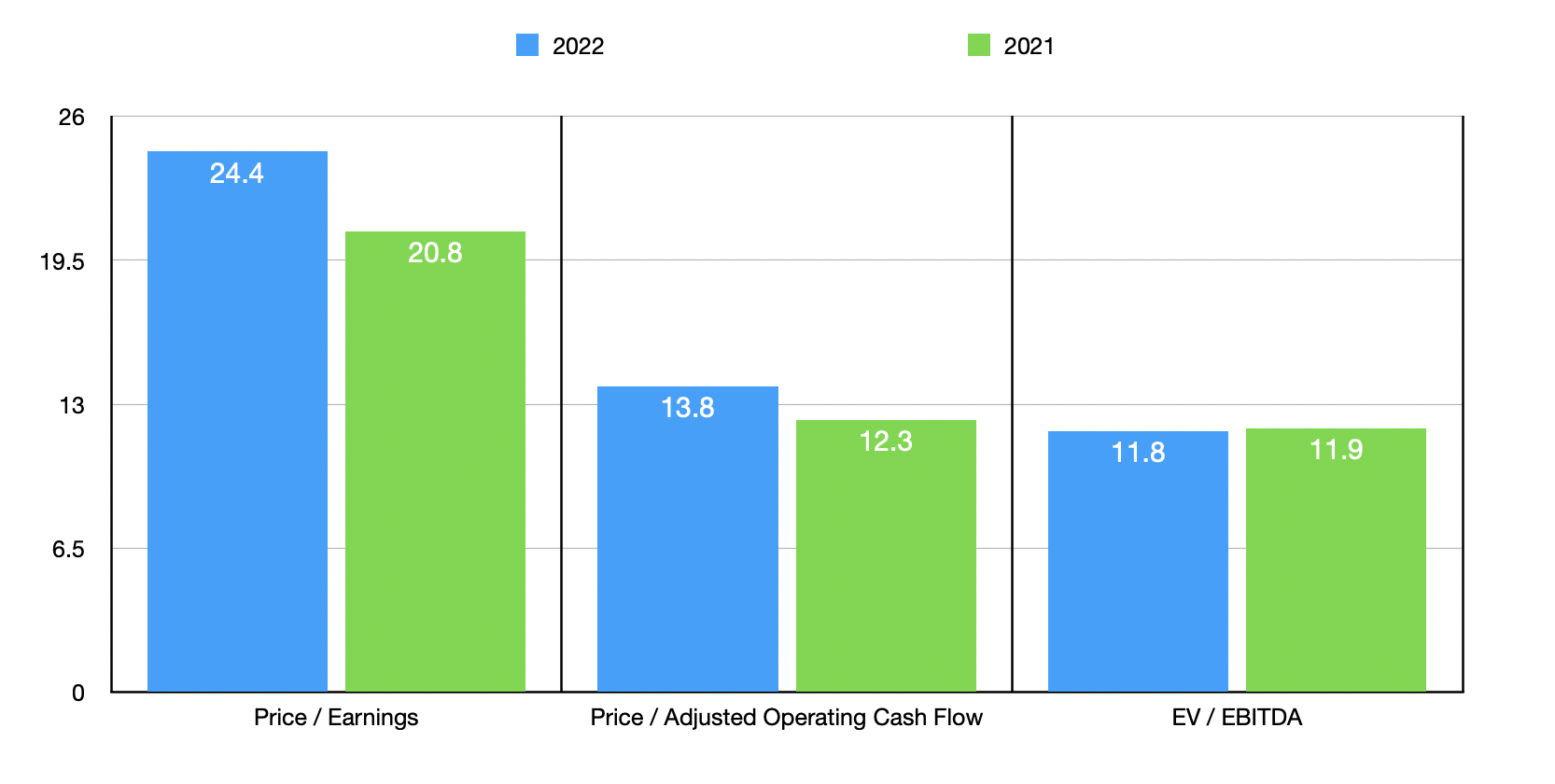

Based on these figures, ESAB Corporation is trading at a price-to-earnings multiple of 24.4. The price to adjusted operating cash flow multiples should be 13.8, while the EV to EBITDA multiple should come in at 11.8. Two of these three metrics are more expensive than if we were to use the data from 2021. You can see this in the chart above. As part of my analysis, I also compared the company to five similar businesses. On a price-to-earnings basis, these companies ranged from a low of 6.2 to a high of 103.5. In this case, two of the five firms were cheaper than our prospect. Using the price to operating cash flow approach, the range would be from 6.2 to 41.5. Meanwhile, using the EV to EBITDA approach, the range would be from 3.9 to 32.4. In both of these cases, only one of the five firms was cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| ESAB Corporation |

| 24.4 |

| 13.8 |

| 11.8 |

| John Bean Technologies ( JBT ) |

| 29.2 |

| 26.7 |

| 19.6 |

| Gates Industrial Corporation ( GTES ) |

| 20.0 |

| 21.2 |

| 11.2 |

| Albany International ( AIN ) |

| 34.1 |

| 26.5 |

| 16.3 |

| SPX Technologies ( SPXC ) |

| 103.5 |

| 41.5 |

| 32.4 |

| Mueller Industries ( MLI ) |

| 6.2 |

| 6.2 |

| 3.9 |

Takeaway

Based on the data available, I would make the case that ESAB Corporation is an interesting business, and it will likely do well for itself in the future. The firm does have some risks that many other businesses do not face. But these are not necessarily insurmountable problems. In general, I don't like the volatility that we have experienced and I don't like the recent margin pressure the company is contending with. But shares are cheap and cash flows are robust. Given these factors, I feel a soft ‘buy’ rating for the company is okay for now.

For further details see:

ESAB Corporation: Upside Exists Despite Recent Bottom Line Weakness