ESLOF - EssilorLuxottica: Long-Term Outperformance Put On Your Sunglasses And Buy

2023-07-10 04:22:53 ET

Summary

- I revisit EssilorLuxottica SA, noting its near-equal performance to the S&P 500 with a RoR of 9.93% versus 10.03%.

- Despite not outperforming the S&P 500, the company's near double-digit growth in less than four months is noteworthy.

- I believe EssilorLuxottica, a dominant player in the global eyewear market, has potential for further outperformance in the short and near term.

Dear readers/followers,

It's time for me to take a look at EssilorLuxottica SA ( ESLOF ) once again, after my last foray into the company back in March. The company hasn't outperformed the broader S&P 500 average entirely - with a RoR of 9.93% versus a S&P 500 of 10.03%, but it's very close.

Seeking Alpha ESLOF RoR (Seeking Alpha)

In this market, close to equal performance with a near-double-digit growth in less than 4 months is worth noting, as I see it. Especially considering that I believe the company to be capable of further degrees of outperformance in the short and near term.

For those of you who don't yet know EssilorLuxottica and what the company does, or what the upside is, this article will serve as a combined reminder, intro, and thesis for a potential investment into the company that's dominating the global eyewear market.

Let's get going.

EssilorLuxottica - Plenty to like about excellent eyewear

As I said in my previous article, this is probably one of the more interesting discretionary companies outside of the monolith which is LVMH ( LVMUY ). It started out as the name would suggest Essilor, a French eyewear company, and Luxottica, an Italian eyewear company.

The company has the distinction of generating revenues of over €14B, and it's most well-known for being the brand company for a variety of world-famous eyewear brands, both in glasses and sunglasses.

EssilorLuxottica IR (EssilorLuxottica IR)

This company, dear readers, is a market dominator. It owns some of the most storied and famous brands around, with 150 different names in its portfolio, which comes to a combined heritage of nearly six millennia, including products like:

- Frames

- Lenses

- Instruments/equipment

- Contact lenses

- Smart glasses

- Readers

- Banners

- AFA

The company has professional solutions in wholesale in over 150 nations, but also operates a strong DTC business, with a global footprint.

The company is very NA-heavy with a 46% share of the mix and another 37% in EU. That means the APAC and LATAM areas are extremely underpenetrated so far. The brands that are under the EssilorLuxottica banner, and you may not realize this, include:

- Essilor

- Luxottica

- Ray-Ban

- Oakley

- Target Optical

- Lenscrafters

- Chanel

- Crizal

- Persol

- Valentino

- Versace

- Varilux

- Bvlgari

- Alain Mikli

And many others. The brands include timeless favorites, such as the Ray-ban aviators, and a pair of sunglasses I myself own (with EssilorLuxottica's patented glasses, an amazing product). It's easy to invest in a company when the valuation and prospects are good, but when you also happen to love the product, which I do.

All of my glasses and eyewear are EssilorLuxottica. The company controls around 75% of the top-20 rated brands, with Ray-Bans obviously being among the most well-known and well-loved.

The company is a fully integrated operation, complete with 53 mass-production facilities around the planet delivering to 564 prescription and mounting facilities, with 57 global distribution centers to retailers. The company has already done the work that many other companies now need to do in diversifying and hardening its supply chain to ensure that no issues occur as a result of a trend like COVID-19. EssilorLuxottica was one of the least-impacted consumer discretionary businesses by COVID-19, and their operations, barring some logistical interruptions, continued functioning relatively unencumbered.

That does not mean the journey is done, however. The company is moving into the digital age with things like E-lens, near-vision, single-vision solutions and light management solutions, smart glasses, and other things.

This is an extremely tricky market the company is in. Very few new entrants even have close to a chance of success in eyewear. 80% of the market is represented by prescription, and more than 50% is served by independent ECPs. The company has solutions across all markets and all price segments, and the independent aforementioned ECPs serve as the backbone for the company's ambitions for further growth. However, the degree of demand for the company's products and solutions is very strong and remains at what I would consider a high level, given the overall prevalence of eyesight correction.

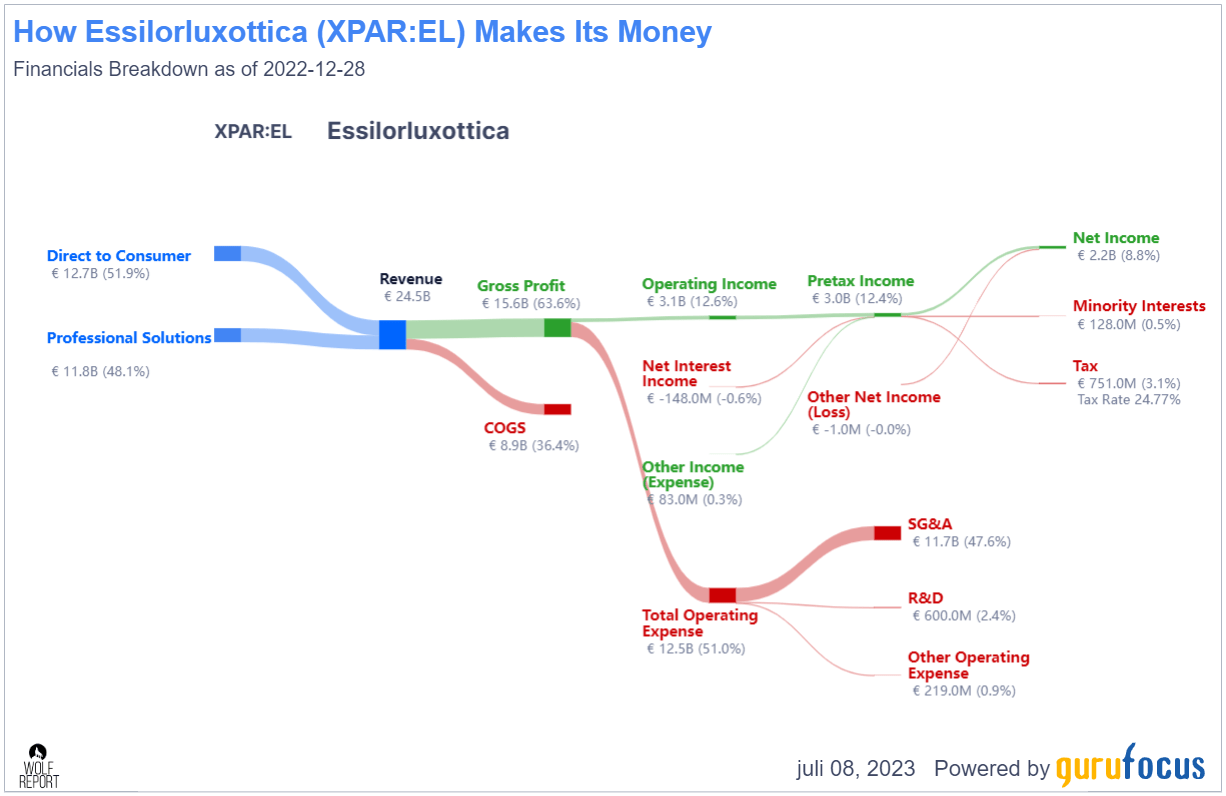

The company's native listing is actually in Paris, not Milan, under the EL ticker. The company scores one of the best fundamental safety scores in the entire discretionary segment barring LVMH and manages a near-64% gross margin, 12.6% operating margin, and almost 9% net margin. This is not as good as LVMH - but the problem here is that LVMH controls more of the marketing and distribution pipeline. What I mean is that COGS is not the problem for EssilorLuxottica, at only 36.4% of revenue, it's actually OpEx - and specifically SG&A, which consumes nearly 48% of the company's revenues. This is not surprising per se but is also perhaps the biggest challenge the company faces.

EssilorLuxottica Revenue/net (GuruFocus)

{kind=link}

Because aside from this, very few risk-specific headwinds for the company can even be argued to exist. The company is an inherently profitable business with plenty of cash on hand. Much like LVMH, it's a sort of "timeless buy" at the right price, and given the trends that the company has seen, I believe it once again offers value at the price it's being offered at.

FY22 wasn't as bad as some analysts, or the market trends may make it out to be relative to the company's valuation. Sales were up 14%, margin at nearly 17% operating level, up 70 bps, but with a heavy investment focus to strengthen the business model. To put it simply, my issue isn't how much the company sells, it's how much of that revenue turns into net profit. For a company with this sort of footprint and brand recognition, this should be a lot better.

As a quick comparison, LVMH's share of Opex is 10% less, managing the same COGS, with around an 8-9% lower SG&A. It's exactly these percentages that for LVMH result in a 17-18 net profit margin.

So that's where EssilorLuxottica has work to do. Now, I am in no way expecting the company to be able to beat LVMH or do the same thing. EL isn't LVMH. But I would like to see maybe 300-500 bps worth of improvement over the next 4-7 years or so - and that is part of what the company is investing for. Hopefully, this will be a development driven by DTC sales or improved margins, increasing prices, and maintaining a push-through on the margin side, mixed with new product families and products with higher profit margins than legacy lenses and glasses.

For the coming 2023, I don't see a whole lot of negative overall high-level trends for the company. Most of what could be considered overarching risk is maybe some softness in the Chinese market.

Aside from margins, the next big challenge to EL is the fact that it's one of the most premiumized companies I actually invest in next to LVMH. So let's move to valuation and see what we have going for us here.

EssilorLuxottica - the valuation is rich - but so is expected company EPS growth

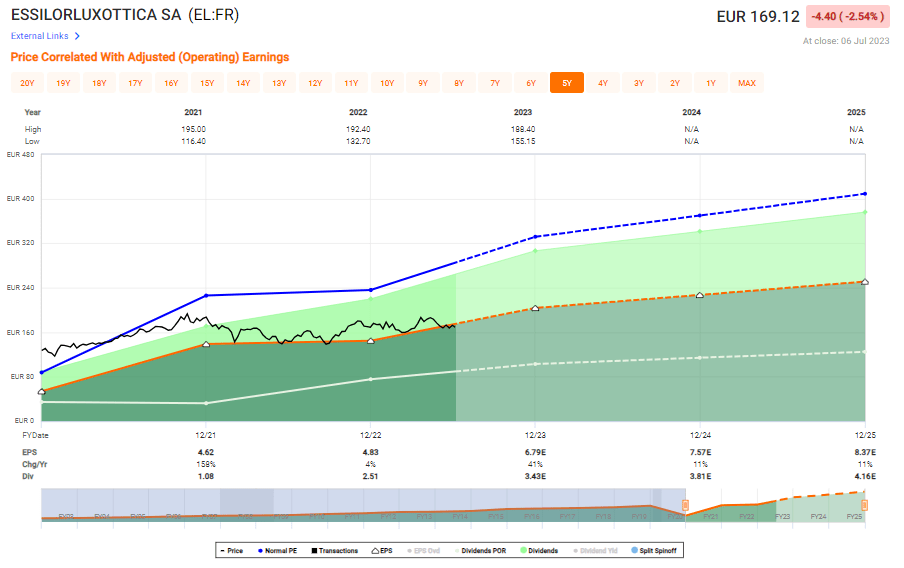

So, there is no putting into question that a 28-29x normalized long-term P/E ratio for the valuation is high. However, it also comes with the company expecting significant future growth as we see a China reversal along with new products and sales coming online.

This is the earnings "picture" we see for the company going forward.

EssilorLuxottica Upside (F.A.S.T graphs)

{kind=link}

And based on a 92% accuracy ratio for a 2-year basis with a 20% MoE, I consider the conviction for these forecasts to materialize relatively high. You just need to accept that the company demands a premium and only has a dividend of just south of 2% - which is still good for a company in this segment.

LMVH is without a doubt the superior investment, all things being equal. But the thing is, the valuation between these two companies is not equal. LVMH is a position where I don't see that we could buy it at an acceptable valuation. Meanwhile, EL is very buyable here.

I forecast EL to be around 30x P/E. The upside to a 30x P/E with these growth estimates in mind here is almost 20% per year, or 56% total RoR until the end of the 2025E Fiscal.

EssilorLuxottica Upside (F.A.S.T graphs)

{kind=link}

I consider this development to be fully realistic, and this is what I base my positive thesis on for EL. However, my current PT reflects an even lower, more conservative estimate where we barely see any upside despite this growth, and even at €175/share you don't see a loss of capital going forward.

I do not consider any longer that my current price target fully reflects the upside potential in the stock - so I am changing it. Based on expansion, sales, and new products, I now consider EL to be worth closer to €195/share. In my previous estimate, I was too conservative and too careful overall, which I regret.

S&P Global analysts are more in line with my new targets, with 19 analysts going from €155/share to €225/share, averaging out at €193/share with 12 out of 19 at a positive "BUY" or "Outperform" rating. This denotes almost a 15% undervaluation at the company's sub-€170/share price we're seeing here.

I believe the company is substantially undervalued to even only portions of its estimates materializing - and that is why I am buying more in the company here.

The following is my updated thesis for EssilorLuxottica.

Thesis

- EssilorLuxottica is a world-leading eyewear company - in fact, it's the world-leading eyewear company, with convincing longer-term upside due to incredibly strong fundamentals, strong growth trajectories, and strong recent overall performance. We want to keep an eye on costs here, but I do see the very real potential for continued growth and even outperformance in this investment.

- There was nothing in the most recent report suggesting a company downturn here, rather giving us the circumstances for a bounce back up in the 2023-2024 period, further suggesting an upside here.

- I'll continue to provide coverage for the company here, and I consider it a solid investment at anything below a €195/share conservative PT, compared to its current share price of €169/share.

- For me, therefore, this one is a "Buy" here, and the buy is even stronger than in my previous article where I had a lower overall price target.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

While EssilorLuxottica cannot be called "cheap", it still fulfills 4 out of 5 criteria for a positive, profitable investment at this time, which means I'm at a "Buy" rating here. I maintain this for the 2H23 period.

For further details see:

EssilorLuxottica: Long-Term Outperformance, Put On Your Sunglasses And Buy