ESLOF - EssilorLuxottica: Path To Maintaining Dominance

2023-11-22 08:02:38 ET

Summary

- EssilorLuxottica is a vertically integrated eyecare business with a diverse portfolio of leading brands and high barriers to entry. The business is the premier offering in the industry.

- EL's financial performance has been strong, with M&A-supported growth and high margins generating incrementally improving cash flows.

- The eyecare industry will further experience tailwinds as Western populations continue to age and economic development drives eyecare services in emerging markets.

- EL's business model, global reach, and focus on innovation position it well for long-term success despite potential risks.

Investment thesis

Our current investment thesis is:

- EL is a highly-quality business, with substantial scale in the eyewear/eyecare industry. It is vertically integrated, increasing exposure and shared expertise, while operating a range of leading brands to win customers.

- The business has built high barriers to entry and continues to do so through strategic acquisitions and partnerships, allowing the business to maximize its return from this industry.

- We expect the eyecare industry to continue its healthy growth trajectory, as the need for care continues to rise through economic development and an aging population.

- The business performs well relative to its peers while trading at an attractive valuation and yield. From this position, the business should generate healthy returns long term.

Company description

EssilorLuxottica (ESLOY) is a leading global player in the eyewear industry, formed through the merger of Essilor and Luxottica in 2018. The company's mission is to improve lives by improving sight, providing innovative lenses and frames to consumers worldwide, in many cases with a focus on fashionable products. With headquarters in Charenton-le-Pont, France, and Milan, Italy, EssilorLuxottica has a diverse portfolio of iconic eyewear brands and a strong presence in both the prescription and sunglasses markets.

Share price

EL's share price has made steady gains over the last decade, although has clearly lagged behind the S&P 500. This is despite an impressive period for the business, with strong financial and commercial results.

Financial analysis

{kind=link}

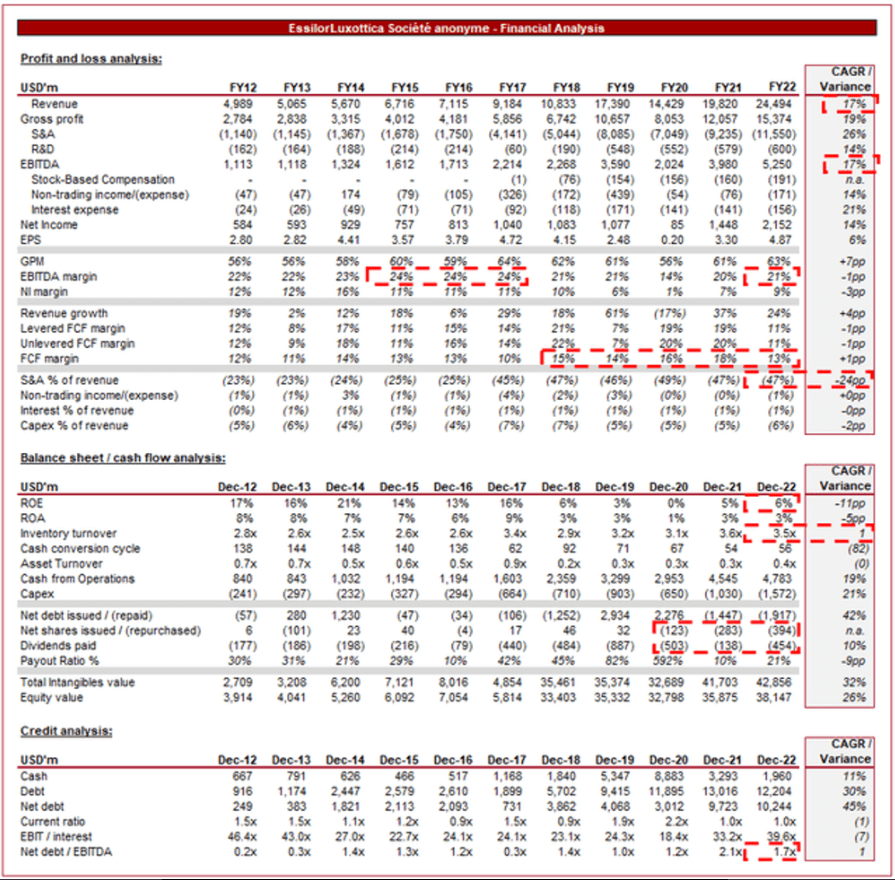

Presented above is EL's financial performance for the last decade.

Revenue & Commercial Factors

EL's revenue has grown at an impressive rate of 17% in the last 10 years, with only 2 fiscal years of growth below 10% (excl. the pandemic-impacted year). This is a result of both strong underlying organic growth, as well as inorganic acquisitions, including the combination of Essilor and Luxottica.

Business Model

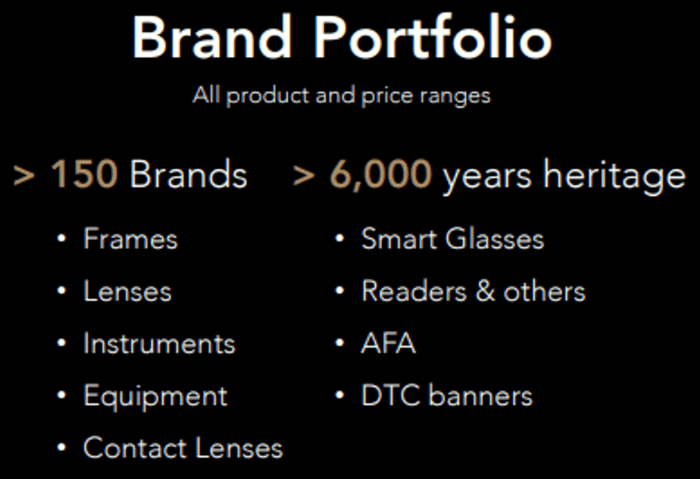

EL is a truly unique business in the industry, with unrivaled scale and reach in the industry. The business owns over 150 brands across the eyewear spectrum, with several leading brands such as Ray-Ban. The diversity of brands across segments and price points allows the business to capture a large amount of the market while reducing its exposure to any single market. For example, during an economic downturn, fashion brands may weaken but lenses will remain resilient.

{kind=link}

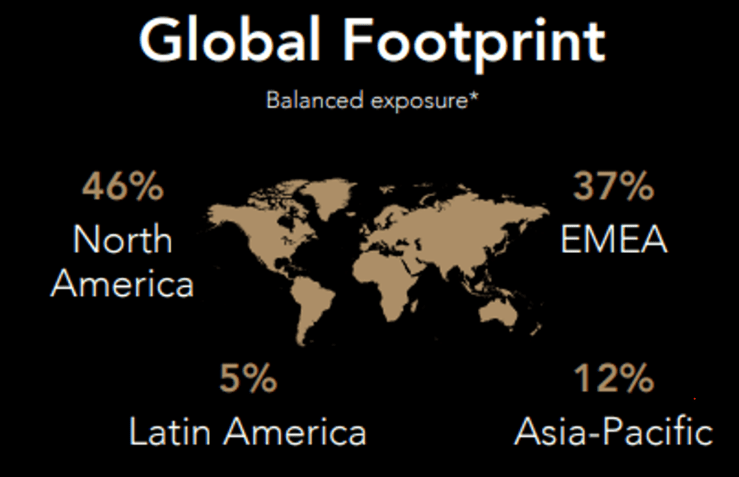

The business generates revenue globally, with a strong diversification across key geographies. This reduces reliance on any signal market, compounding the diversification benefits of its product range.

{kind=link}

For these reasons, we consider EL's customer profile to be high-quality, smoothing its revenue curve.

EL's business model encompasses a vertically integrated approach, combining the expertise of Essilor in lens technology and Luxottica in frame design and retail. The company operates through two main segments: Lenses & Optical Instruments and Equipment & Retail.

The company takes a broad approach, serving opticians, eye care professionals, and consumers through an extensive network of retail stores and online channels.

This vertical approach allows the business to maximize the value obtained from the industry. With deep expertise in eyewear, the business can:

- Share competencies between brands

- Minimize production costs between brands

- Cross-sell between service lines (Frames + prescriptions, for example)

- Minimize value leakage from the production-to-retail chain.

The business continues to focus on its Optical segment, with strong global partnerships with optometrists, innovation in optical equipment, and an increasing portfolio of retailers. This industry is highly valuable as it underpins strong demand in the fashion segments (directing consumers to the purchase of glasses) while having highly attractive economics and sustainable demand with population growth.

{kind=link}

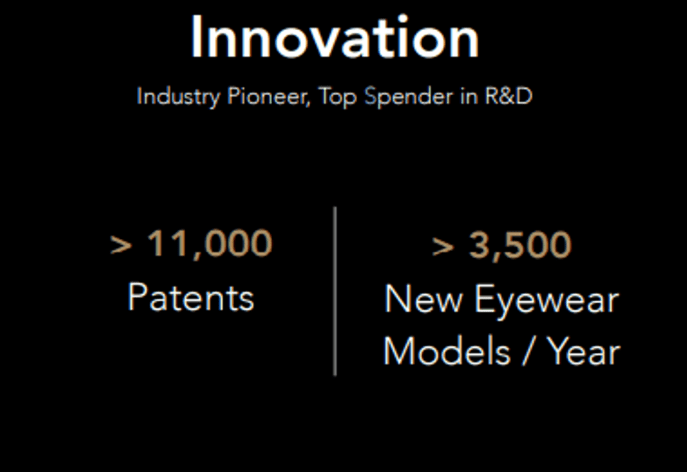

Underpinning the company's strong business model is quality innovation. The business has consistently spent c.3% of revenue on R&D, seeking to remain at the forefront of eyewear technology and production. Technological advancements in eyecare, such as advanced lenses, coatings, and frame materials, have improved the comfort and functionality of prescription glasses. New technologies, like blue-light-filtering lenses, offer additional benefits for consumers working extensively on digital devices.

{kind=link}

In conjunction with organic development, EL has acquired businesses as a means of developing its areas of weakness and exploiting opportunities. Most recently, the business acquired GrandVision for c.$7bn , a global leader in optical retailing (more than 7200 stores worldwide), and delivers high-quality and affordable eye care to customers around the world. With the eyewear industry still dominated by store footfall (given eye tests need to be conducted in person), this move looks to be a shrewd attempt at further widening its grasp on the industry. EL's M&A track record has generally been positive and we expect a continuation of this over time as opportunities present themselves.

{kind=link}

As well as acquisitions, the business utilizes its expertise to agree value accretive partnerships and minority investments. Several global brands have reach but lack the manufacturing expertise to produce an economically viable eyewear offering (Burberry ( BURBY ), Ralph Lauren ( RL ), Armani, Tiffany ( LVMHF ), Versace ( CPRI ), etc.). EL is able to provide just this. Further, the business has partnerships to further develop its technical capabilities, such as with Nikon (Research into optical equipment).

Competitive Positioning

Essilor's competitive advantage revolves around these key factors of a quality brand portfolio, global reach, deep expertise, and vertical integration. These factors have allowed the business to develop a dominant position in the market while building significant barriers to entry and yielding quality economics.

Eyewear Industry

EssilorLuxottica faces competition from various players, including:

Safilo Group S.p.A. ( SAFLF ), Johnson & Johnson Vision ( JNJ ), HOYA Corporation ( HOCPY ), and Cooper Companies, Inc ( COO ).

Having established the quality of the business, we can lean into the key driving force of our thesis.

As the global population continues to grow, the demand for vision correction and support products, such as prescription glasses, is likely to increase. Additionally, as the population ages, the prevalence of age-related vision problems, such as presbyopia (difficulty focusing on close objects), will gradually increase. These two factors will drive higher demand for eyeglasses and other vision aids, presenting an upward growth trajectory for eyecare businesses.

Underpinning this is the potential for a general rise in demand for eye care across age cohorts. The rapid pace of modern life, increased screen time, and exposure to blue light from electronic devices have contributed to a rise in vision-related issues, including myopia (nearsightedness) and digital eye strain. As awareness of these problems grows, more people seek regular eye examinations and prescription glasses to address their visual needs. This trend can result in sustained demand for eyecare products and services.

The rise of e-commerce and DTC sales has disrupted the traditional eyewear industry. Online platforms offer convenience and competitive pricing, attracting consumers who prefer to shop from the comfort of their homes. This is an easy process for consumers as they are able to provide their prescriptions online or order just frames to try them on. With a diverse array of retailer brands, such as Sunglass Hut, EL is positioned well to transition.

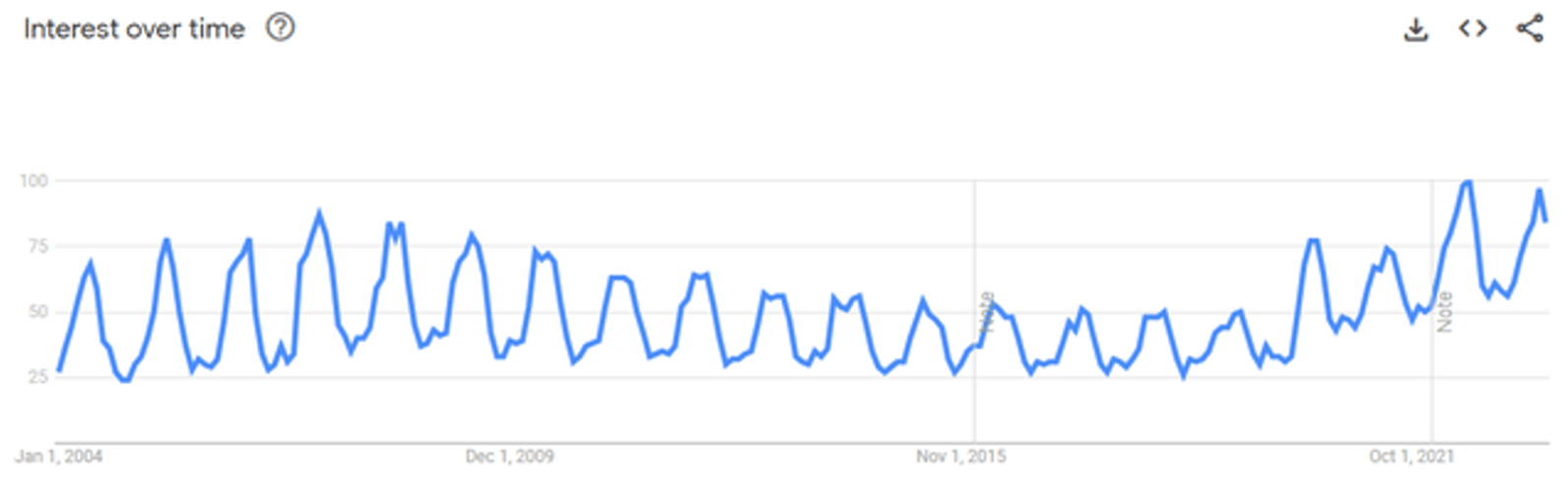

Marketing capabilities are a critical competency required in the fashion industry. The industry has high competition among brands, although if one was to own several of these brands, as EL does, it is essentially competing with itself. As the following graph illustrates, the interest in the Ray-Ban brand has been revitalized in recent years, suggesting the ability to drive improvement.

{kind=link}

Opportunities

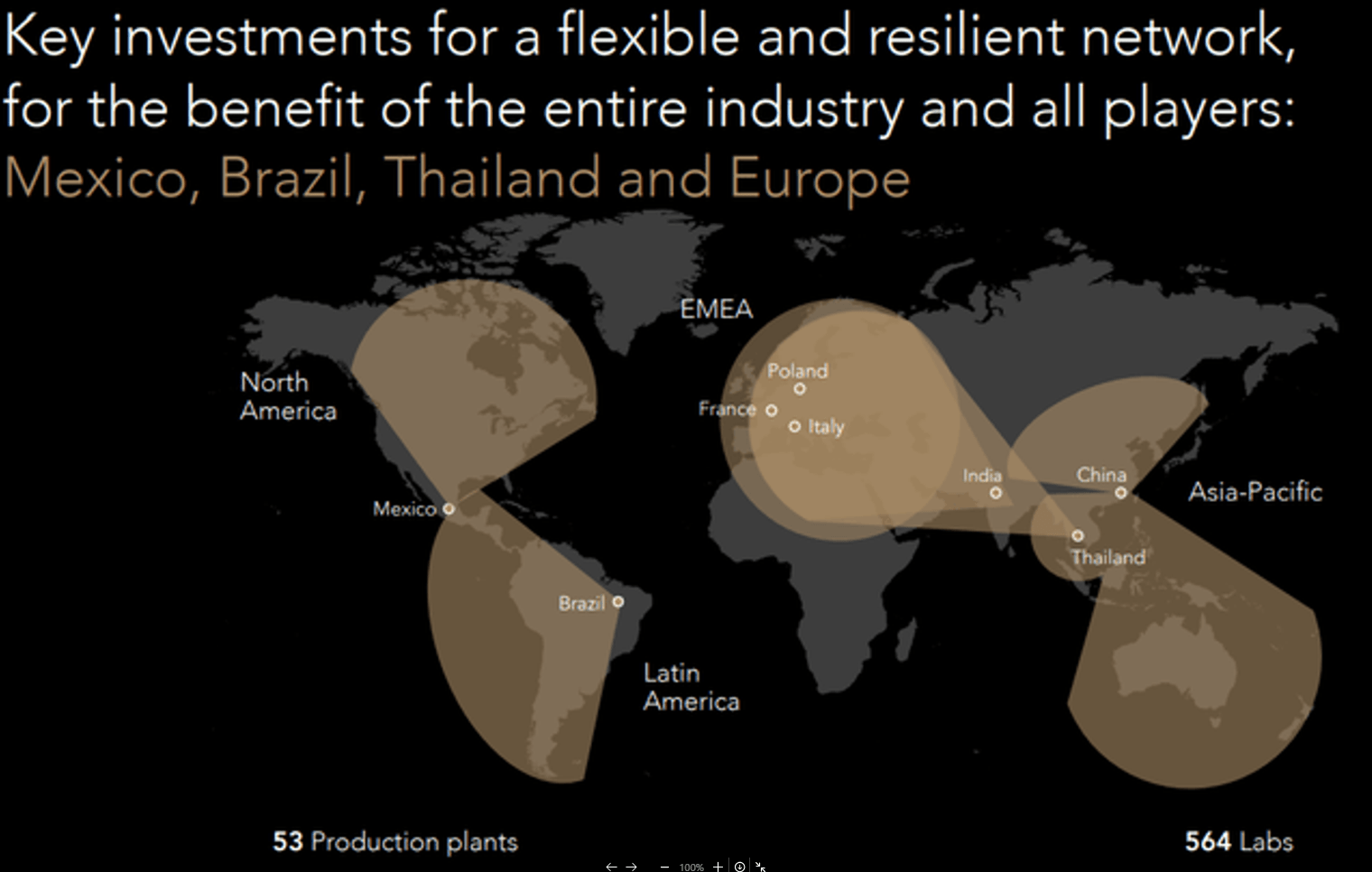

The growth of the global middle class, especially in emerging markets, has increased the affordability of prescription glasses for a larger segment of the population. As these markets continue to develop and income levels rise, more individuals will have access to vision correction products. EL has acknowledged this, focusing its efforts on key geographies such as Brazil.

{kind=link}

Notable threats

Counterfeit eyewear products in the market continue to impact brand reputation and revenue. Given the simplistic nature of eyewear, fashion brands can be easily replicated, both branded (counterfeit) and replica designs (copycats).

There is an inherent risk that technological development will yield prescription eyewear for vision improvement obsolete. We are already seeing consumers in the West (in particular) having laser eye surgery (LASIK), contributing to a reduced need for eyewear.

Economic & External Consideration

The eyecare industry has demonstrated resilience to economic downturns, as the need for vision correction remains essential for many people regardless of the economic environment. In times of economic uncertainty, individuals may prioritize healthcare-related expenses, including eyecare, which can help stabilize EL revenues.

This is reflected in the company's 9m'23 results, with top-line revenue growth of +7.2%. This has been driven by all segments of the company, with:

- North America remaining resilient.

- EMEA performing well, primarily due to Professional Solutions and optical retail.

- Varilux XR and Stellest developing well globally.

- Ray-Ban Meta launched to much success and market recognition, creating the foundation for a new generation of Smart Glasses.

There appears to be very little that can displace this company's trajectory.

Margins

EL has highly attractive margins, with an EBITDA-M of 21% and a NIM of 9%. Margins have traded flat over the historical period, although the business sits slightly below its peak level in FY17.

Margin movement has been materially impacted by acquisition, contributing to a change in product mix. Further, the business has faced inflationary pressures from input costs and supply chain issues, although we expect these to subside over the coming quarters.

Balance sheet & cash flows

EL's inventory turnover has gradually improved over the period, reaching 2.5x in FY22. This has allowed the business to further improve cash flows, with a strong current yield.

This has allowed the business to primarily utilize cash for its capital allocation strategy, reducing the need for debt. The company currently has a ND/EBITDA ratio of 1.7x, leaving sufficient scope for raising debt if required to conduct further M&A.

Distributions have come in the form of dividends and buybacks, with a reasonably good yield given the quality of the business.

Outlook

{kind=link}

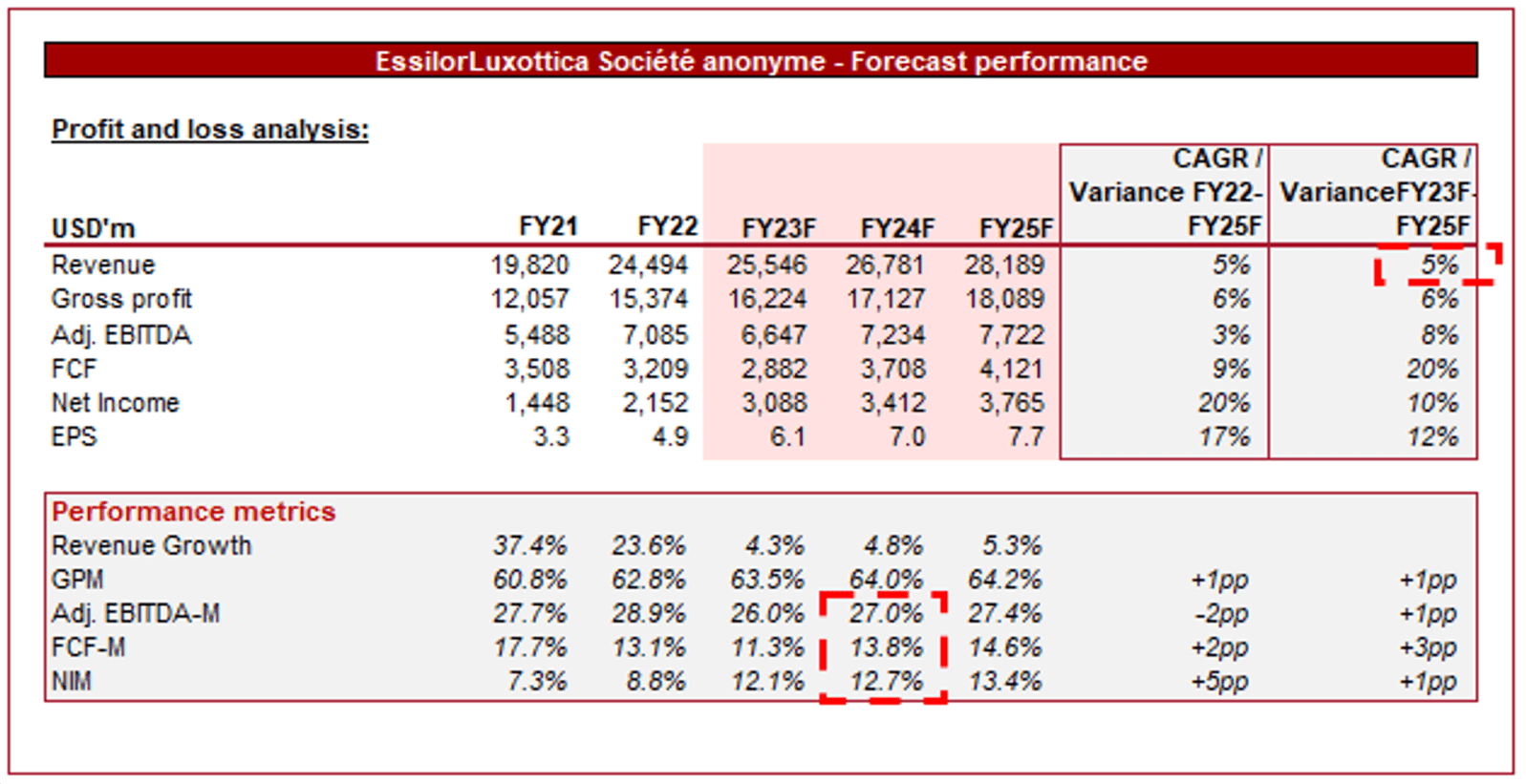

Presented above is Wall Street's consensus view on the coming 5 years.

Analysts are forecasting healthy organic growth in the coming years, with a 5% rate into FY25. This looks to be driven by emerging markets and e-commerce, offset by soft growth in Western markets.

{kind=link}

Margins are expected to remain flat in the coming years, likely in part from the impact of acquiring GrandVision. We see scope for improvement in the coming years, although a flat forecast is reasonable.

Industry analysis

{kind=link}

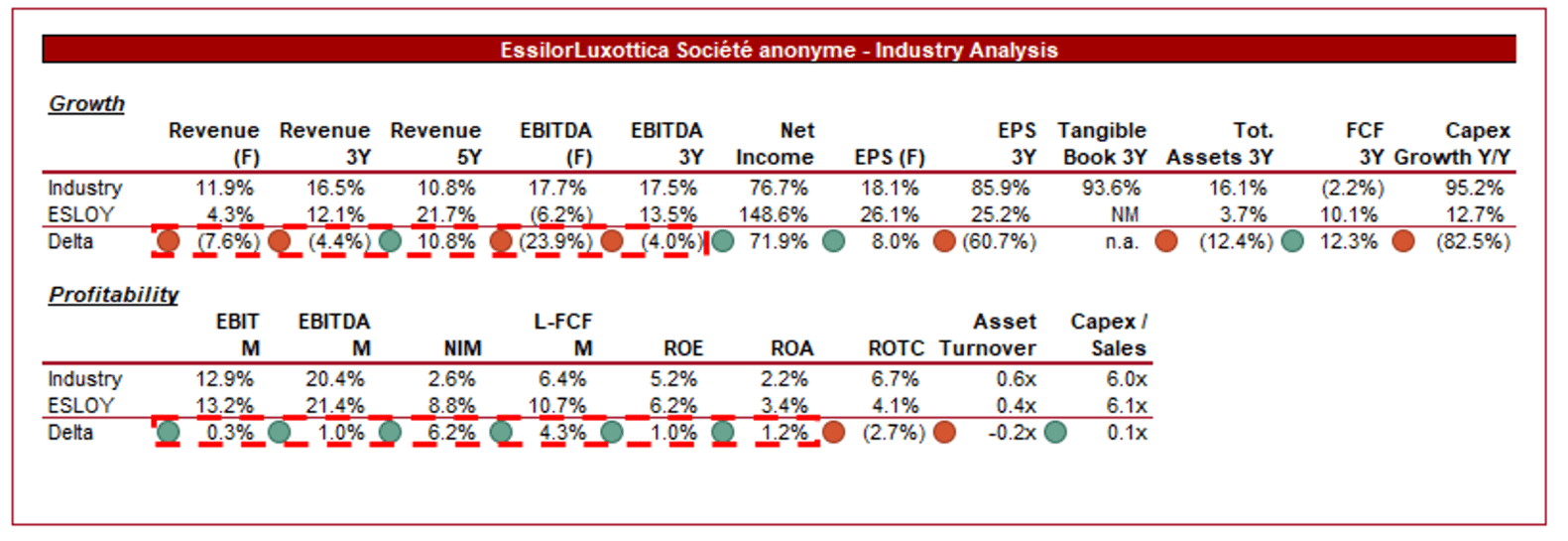

Presented above is a comparison of EL's growth and profitability to the average of its industry, as defined by Seeking Alpha.

EL performs well in our view. The business is generally growing at a superior level, although conceding that this is muddied by acquisitions. Margins are comfortably higher, particularly in cash flows, with a higher ROE.

The key difference between EL and this particular peer group is its size. EL is double the size of the nearest peer and over 50% the size of the combination of all other businesses. For this reason, there is a degree of incomparability, both in financial metrics and valuation. Small businesses with similar growth and margins will generally be valued higher due to greater scope for margin improvement and commercial development to drive growth.

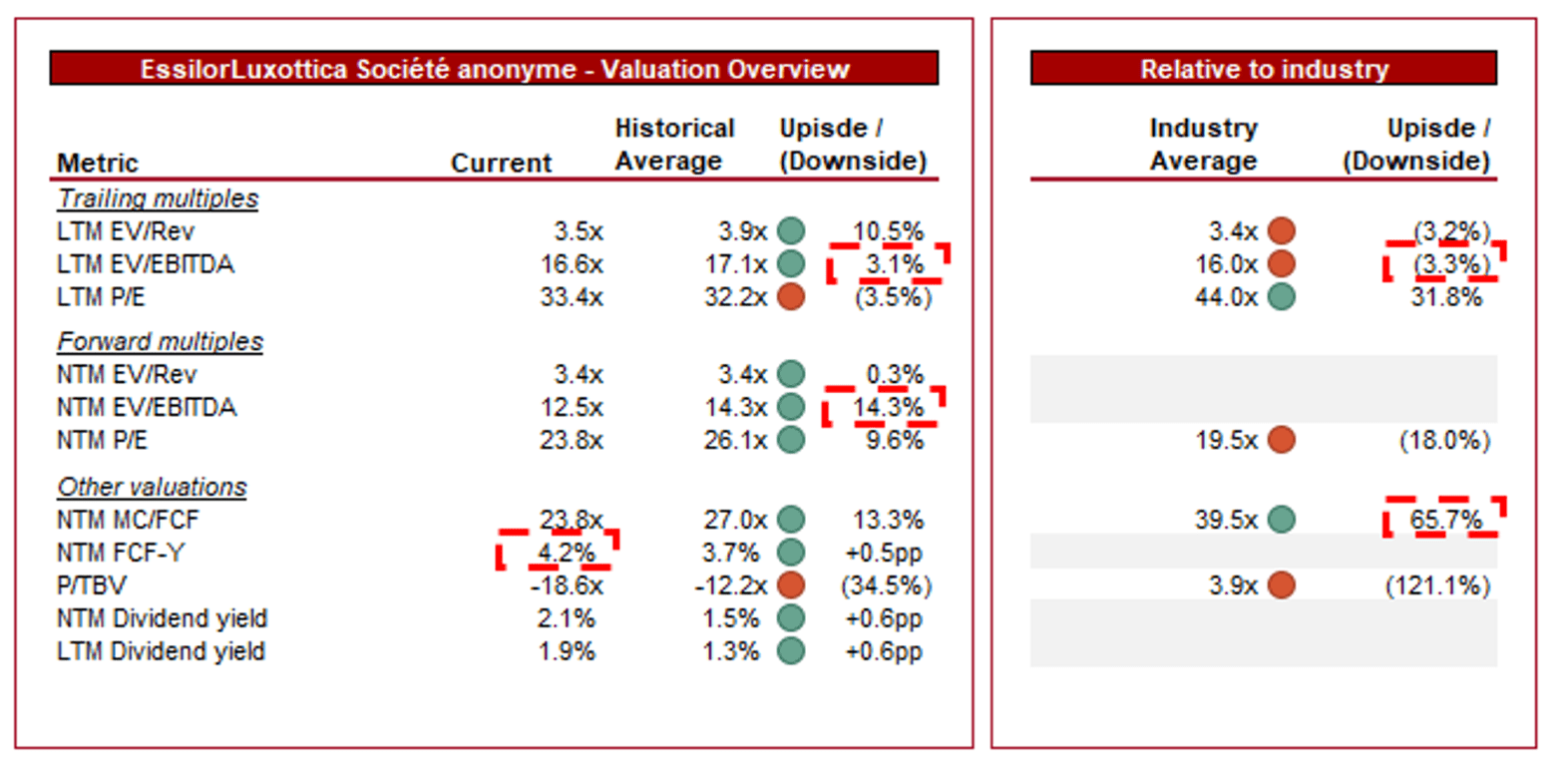

Valuation

{kind=link}

EL is currently trading at 17x LTM EBITDA and 13x NTM EBITDA. This is a discount to its historical average and also to the industry average.

Our view is that a small premium is justifiable, owing to the company's increased scale, margin rigidity, and further expansion in the industry. Confirming this assessment to us is EL's return, which is higher on a FCF-Y basis (+0.5ppt) and on a dividend basis (+0.6ppt).

As previously mentioned, a comparison to its industry peers is unhelpful due to the disparity in size. If we consider businesses with a market cap of >$19bn, EL has similar margins while being the cheapest.

Based on this, we believe there is upside available with owning EL, although not necessarily a large amount. This said, given the economic uncertainty, the risk-adjusted return, and potential for market outperformance makes this a shrewd choice.

Key risks with our thesis

The risks to our current thesis are:

- Ease of counterfeit/replica products (as previously explained).

- Technological development rendering eyewear less valuable (as previously explained).

- FX. With EL generating earnings globally, the business facing significant FX, especially as it relies more heavily on countries in Asia and LatAm. This has the potential to impact reported financial results.

Final thoughts

EL is a fantastic long-term business. The company has a highly defensible market position, a broad range of high-quality brands, deep integration into the market through vertical integration, and a commercially attractive industry which we expect to grow well in the coming years.

EL is not a cheap company but businesses like this rarely are. Given its strong performance relative to peers and its valuation compared to historical levels, we are comfortable assigning a soft buy rating.

For further details see:

EssilorLuxottica: Path To Maintaining Dominance