VLO - Even Valero's Finances Are Vulnerable

2024-01-17 08:09:12 ET

Summary

- Refineries are facing challenges due to the decline in crack spreads.

- Refiners continue to operate near 100%, a good sign for higher cracks with spring and summer approaching.

- In the near future, Valero's renewable business will likely provide more stable returns.

For refineries, crack spreads mean everything. In recent months, the Gulf Coast 2-1-1 fell into the mid-20s, down from the mid-30s. Companies such as Valero ( VLO ) rely heavily on those spreads for results. During the last conference call, management closed with this remark :

"[W]hile there are broader factors that may drive volatility markets, we remain focused on things we can control. This includes operating our assets efficiently in a safe, reliable and environmentally responsible manner, maintaining capital discipline by adhering to a minimum return threshold for growth projects and honoring our commitment to shareholder returns."

In our view, Valero's operations and business are at the very top of its industry. But like every business, it can't control everything. Mentioned above, crack spreads, the difference between raw material costs and product sale prices, determine the majority of the profits. We have written on Valero in the past , but our interest mostly lies within its conversations on renewable products, a business in which we heavily invest. With lower cracks, investors should expect lower quarter-over-quarter and maybe year-over-year results. How vulnerable are investors to that cycling shark? Let's set the drone to hover overhead and take a closer look.

The Company

Valero operates fourteen refineries , eight of which are in the Gulf Coast Region, and most of the capacity resides there also. Gulf Coast crack spreads become particularly important. Again, we view Valero as the best of the best in refinery operation.

The Quarter

Now, turning to a short summary of last quarter, the results include:

- Record 3rd quarter earnings at $7.49 compared with $7.14 in the prior year.

- Refining income fell from $3.8B to $3.4B year over year.

- Expenses increased modestly from $4.70 to $4.91 per barrel year over year.

- Capital expenses equaled approximately $400 million, inline.

- Shareholders return equaled $2.2B, of which $1.3B was used to purchase 13 million shares.

Guidance for the 4th quarter refining throughput was:

- Gulf Coast at 1.77 million to 1.82 million barrels per day.

- Mid-Continent at 445,000 to 465,000 barrels per day.

- West Coast at 245,000 to 265,000 barrels per day.

- North Atlantic at 470,000 to 490,000 barrels per day.

The company produced an excellent quarter. What about the next?

Fossil Fuel Refining

The closer look at the 3rd quarter results shows income dropped year over year more than the costs increased. From our own data set, crack spreads, shown in the next table, dropped significantly.

| Cracks GC 2-1-1 |

| July |

| Aug. |

| Sept. |

| Ave |

| 2022 |

| $44 |

| $38 |

| $36 |

| $40 |

| 2023 |

| $33 |

| $42 |

| $34 |

| $36 |

The Gulf Coast 2-1-1 spread averaged 10% lower in 2023. Reviewing the 4th quarter year over year shows further losses.

| Cracks GC 2-1-1 |

| Oct. |

| Nov. |

| Dec. |

| Ave |

| 2022 |

| $51 |

| $38 |

| $30 |

| $40 |

| 2023 |

| $24 |

| $20 |

| $20 |

| $21 |

On a year-over-year basis, the cracks dropped 48%; quarter over quarter, the drop equals 40%.

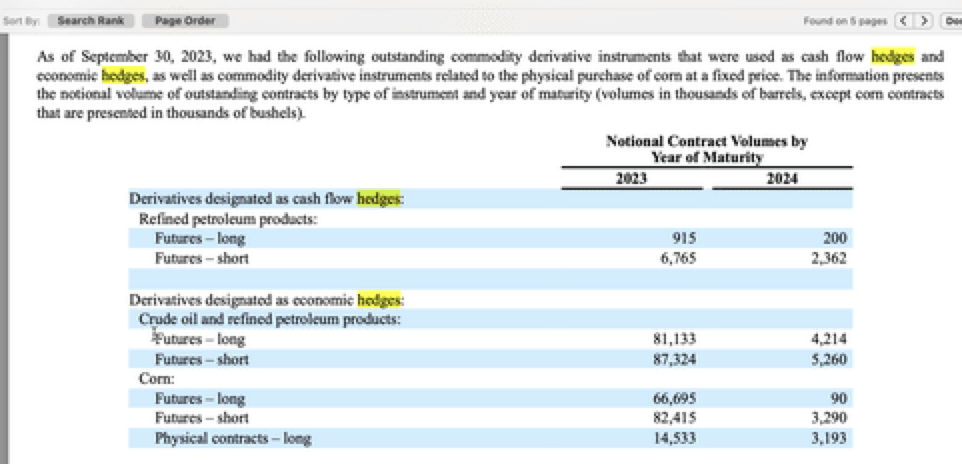

The company does hedge. From the last 10-Q , the next graphic shows that the company has approximately 100 million barrels in hedges.

{kind=link}

Note that the hedges roll off before the end of 2023 with very few thus far for 2024, approximately one-tenth. Investors might expect significantly lower profits in the 4th quarter. For next year, the cracks still remain precipitously low thus far also likely negatively affecting 1st quarter 2024.

Renewable Fuels Business

We are going to switch gears for a look at Valero's renewable business. Our view offers two perspectives on the business, one from Valero and one from Calumet Specialty Products ( CLMT ), the current leader in profitable renewables. First, a Valero management summary of the September quarter.

- DGD SAF project at Port Arthur remains on schedule for completion in 2025.

- The Arthur plant could at that point upgrade half of its 470M gallon per year capacity to SAF.

- RND generated $123M in income compared to $212 million last year.

- Volumes were almost a million gallons higher than a year ago.

- Lower margins produced lower income.

Management noted several important facts from the September quarter. RINs dropped sharply in the quarter, continuing into October. Operating expenses include $0.19 per gallon of non-cash types or 40% of the total cost. The big drop, in their view, was from anticipation of a couple of big start-ups that now were delayed, and Russia freezing out exports forcing more exporting from the U.S. Finishing up their comments, they add,

"The real margin loss there is really because as fat prices have since adjusted in the [spot] market but obviously, there's a lag of our fat prices that kind of carried on that have since started to catch up with this drop in credit prices."

Since the drop, the spot market has cleaned itself up, with fat prices falling. Management views California has the center of the market, but it is expanding its business into Canada (a big outlet without RIN exposure), Oregon, and Washington where price stability seems more real. And with being on the Gulf Coast, Valero believes it has significant advantages with access to a variety of feed stocks and markets. We aren't so sure about that comment. Summing Valero's position:

"So, there's no doubt that there's going to be a continued pressure on the RINs for both the D4 and D6, but our strategy has always been -- there's other markets that you can minimize the impact of that. And then with our platform, we're still the most advantaged from a cost and CI standpoint."

Let's now turn to Calumet for more detail. It started up its renewable operation in Great Falls last year and has been since working out startup operation and equipment issues. At its last call, management discussed the same issues with the sharp decline in D4 and D6 RINs.

"Most recently, we've seen this with over 60% of our products finding its way to Canada, which is fitting with our location less than 2 hours south of the Canadian border by truck. As we see reports of backups in the Panama Canal, extending supply chains in all industries , we are reminded how fortunate we are at Montana Renewables to be situated with direct rail access to critical markets .

"I think we're seeing well a steady margin theory applies to the industry as a whole, volatility can be driven by length of supply chain . In a declining feedstock price environment, margins in our industry will be higher for those with short supply chains. Over time, the industry's volatility should balance out, and we simply would expect those with shorter supply chains to be more steady."

Valero carries a relatively long supply chain and with it expect volatility.

On SAF premium, an important business for Valero moving forward, Bruce Fleming, Head of Calumet's MRL business, stated:

"The industry watchers seem to be centering on about $1 to $1.50 gallon premium to RD and that's substantially a European circumstance right now. But I think we could broadly suggest that it's going to be somewhere in North America. Anybody with an RD platform should be able to fish out about 15% or 20% of it as SAF."

Past discussions suggest that Calumet is expecting a dollar premium with SAF going forward. Investors with Valero can expect choppy results in the renewable business, but it does correct itself. This company's move into SAF offers an opportunity for significantly higher, more stable cash flows that are not subject to the highs and lows in the fossil fuel businesses.

Going Forward

The story seems cyclical and far from out of character. A recent article on OilPrice developed from GasBuddy data, forecasts weaker prices in early 2024 followed by significantly higher prices into summer. " So as long as that's the case , our view would be that when you get to the driving season next year, demand picks back up, you'll see cracks respond. " Remember, in total, the current operating percentage still remains sufficiently above 90% or near full capacity during a weaker usage period.

Valero is still, unlike others, seeing strong demand in diesel. Distillate/diesel inventories still remain significantly below 5-year averages, thus it continues to carry significantly higher premiums over gas.

Dividend

A last subject for income investors seems important, a discussion on dividends. The company is buying back a lot of stock, with last quarter alone equaling 13 million shares. Analysts dogged management a little on this issue and what it means for future dividends. They responded:

"And on the dividend, we maintain a dividend is competitive, growing and sustainable through the cycle. And we feel like we're in a reasonable range now. I wouldn't want to get into more specific on timing or potential dividend increases at this time."

The company has 340 million outstanding common shares and is purchasing its stock at a rate of 50 million plus shares a year. How many years can this continue? With most of the return of capital being share repurchasing, investors have to wonder when significant increases will occur.

Risk

Again, in our view, the primary risk is from significantly lower crack spreads in the near term with a significant decline in earnings. Economists are still debating about a recession, deep or shallow or non-existent. Although most of the public feels like a recession is already here, officially one isn't, and it isn't determined yet of its severity. Other risks not mentioned might also exist.

For further details see:

Even Valero's Finances Are Vulnerable