IDU - Eversource Energy: A Stable Utility To Buy On Dips

2023-09-19 16:44:51 ET

Summary

- Eversource Energy is a large utility serving New England that possesses stable cash flows that are not heavily dependent on the strength of the American economy.

- The company's stock price has weakened due to rising interest rates driving lower appeal of utility stocks.

- Eversource Energy plans to invest $21.5 billion in infrastructure upgrades to increase its rate base and achieve 5-7% earnings per share growth.

- The company has a stronger balance sheet than many of its peers, although its net debt-to-equity ratio has been increasing.

- The 4.20% dividend yield appears to be sustainable and the company's stock appears fairly valued.

Eversource Energy ( ES ) is a regulated electric and natural gas utility that serves much of the New England region, including the heavily populated states of Connecticut and Massachusetts. The company also serves much of New Hampshire, but that state is not nearly as heavily populated:

Eversource Energy

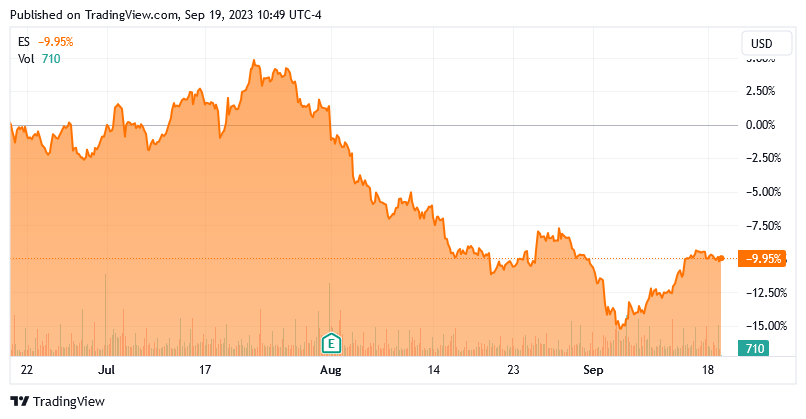

Thus, despite the fact that the company’s service territory is relatively small geographically, it is still one of the largest utilities in the United States in terms of customer count. However, this is not the most important thing about it. As I pointed out in my last article on the company, Eversource Energy enjoys very stable cash flows that have minimal correlation with the strength of the American economy or the American consumer. This could prove to be a real advantage for the company and its investors right now as there are numerous signs that the economy is weakening. Unfortunately, the company’s stock price is also weakening, as the company’s shares are down 9.95% over the past three months:

{kind=link}

There are a few reasons for this weakness, including the fact that utility stocks have been losing some of their appeal as rising rates make short-term bonds comparatively more attractive. Eversource Energy’s second-quarter earnings results were also not as they could have been, but they do still show our stability and growth thesis in full display. Fortunately, the company has a reasonable valuation right now, so it still could be worth considering for long-term investors despite the headwinds of rising interest rates.

About Eversource Energy And Second Quarter Commentary

As stated in the introduction, Eversource Energy is a regulated electric and natural gas utility that serves the New England states of Connecticut, Massachusetts, and New Hampshire. Despite its small geographic area, this is one of the heaviest-populated regions in the United States. As such, Eversource Energy has a surprisingly large customer base consisting of approximately 3.29 million electric, 890,000 natural gas, and 237,000 water utility customers. This makes the company one of the largest utilities in the United States.

However, as I have pointed out in numerous previous articles, the size of a utility does not change the fact that it will possess certain inherent characteristics. The most important of these is that the company will enjoy remarkably stable cash flows through any macroeconomic conditions. I pointed this out in my previous article on Eversource Energy:

The reason for this overall financial stability should be fairly obvious. Eversource Energy provides a product that is typically considered to be a necessity for our modern way of life. After all, nearly everybody has electric service to their homes as well as some sort of heating system in place. In fact, the presence of these things is required under habitability laws in just about every location in the United States. The overwhelming majority of people cannot possibly imagine life without these modern conveniences, and of course without the things that are powered by electricity. As such, most people will prioritize paying their electric bills ahead of any discretionary expenses during periods in which money gets tight.

We can see Eversource Energy’s overall financial stability reflected in its second-quarter results. Here are some of the relevant numbers from the most recent quarter compared to the second quarter of last year:

| Q2 2023 |

| Q2 2022 |

| Revenue |

| $2,629.3 |

| $2,572.6 |

| Operating Income |

| $594.0 |

| $510.5 |

| Net Income |

| $15.4 |

| $291.9 |

| Operating Cash Flow |

| $578.1 |

| $469.9 |

(all figures in millions of U.S. dollars.)

With the notable exception of net income, we can see that all important measures of financial performance showed year-over-year improvement. This is in line with the statement that the company should be very resistant to changes in economic performance. With that said, the year-over-year decline in net income may be concerning. However, this was due to a one-time impairment charge that does not really reflect the company’s operating performance. From the earnings press release :

As a result of Eversource concluding its Offshore Wind Strategic Review that included the sale of its interest in the undeveloped offshore lease area to Ørsted ( DNNGY ) and the advancement of the sale of its interest in the projects under development, Eversource has determined that the carrying value of its total offshore wind investment is impaired. Therefore, the results for the second quarter and first half of 2023 include an after-tax impairment charge of $331.0 million, or $0.95 per share, related to Eversource Energy’s offshore wind investment.

There have been a few media reports lately about recent offshore wind projects having their economics increasingly challenged. For example, Seeking Alpha ran this news report last week mentioning that rising material costs and interest rates have rendered it impossible for several offshore wind projects to earn an acceptable rate of return under their original power purchase agreements. This means that in order to get these projects to go further, the utilities and other companies that were planning to purchase the electricity produced by these offshore wind farms will have to pay much higher prices than they originally planned or budgeted for. This could prove problematic, especially for utilities, due to the strain on household budgets that may push electric costs beyond comfortable levels. Other companies factor the electric costs into their costs of production, so higher electric costs will push up the cost of the goods and services that they sell. If these power purchasers balk at the increased cost of purchasing electricity, then these projects may lose their economic viability and never get developed at all, which will result in losses for those companies that intend to build offshore wind farms. Thus, it is a bad situation all around and in hindsight, it may have been the best decision for Eversource Energy to just exit the scene and take the write-off.

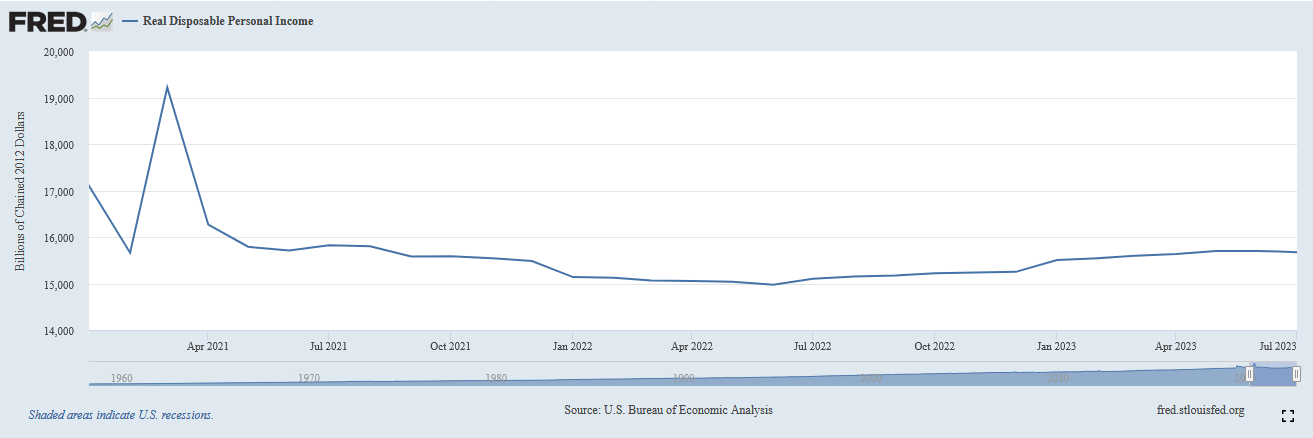

As just mentioned, rising electricity prices will put additional strain on an already struggling consumer. Regular readers of my articles and blog posts will already be well aware of this. After all, high inflation has reduced real disposable income for the average household since the start of 2021:

{kind=link}

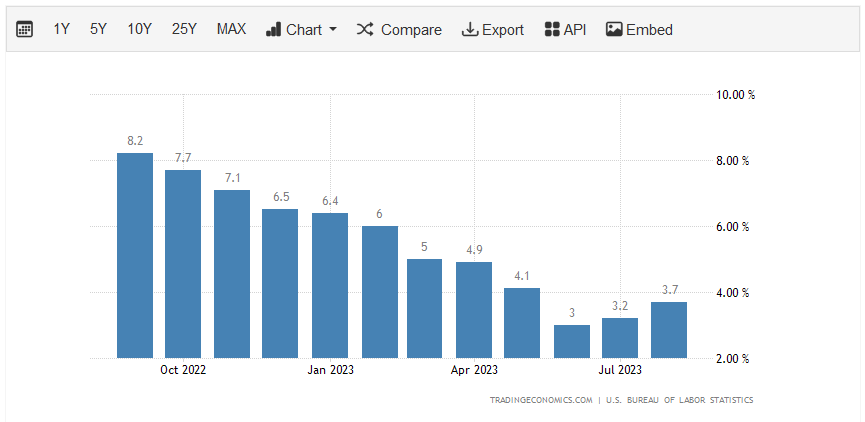

While there has been a slight uptick in the past few months, this may have evaporated now as inflation has once again started to trend up:

{kind=link}

In fact, we do see this above as the Federal Reserve reports that real disposable personal income declined slightly in July, corresponding to the uptick in the headline consumer price index growth rate. It is reasonable to assume that the same thing happened in August due to the even larger increase in the headline inflation rate.

The last thing consumers need right now is higher bills. However, as already mentioned, it does seem likely that they will cut back on other areas of spending before they cut back on paying the monthly bills that they receive from Eversource Energy. We can, in fact, see evidence supporting this conclusion in the company’s history. Here are its revenues over the past ten years along with the trailing twelve-month period:

{kind=link}

As we can see, the general trend is for growth and there have been very few interruptions to that trajectory despite the fact that there were a variety of economic climates over that climate. In fact, even the COVID-19 lockdowns that accompanied the pandemic had no real impact on the company’s revenues. We see a very similar situation when we look at the company’s operating cash flows over the same period:

{kind=link}

There is certainly a bit more variation here than there was in revenues but overall, the basic conclusion remains true. Eversource Energy should be in a much better position to handle a slowdown in consumer spending due to financially strained households reaching their limits than companies in many other industries. This makes it well worth considering for an investor who wants to reduce their exposure to the American consumer.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. After all, we like to see any company that we are invested in grow and prosper with the passage of time. Fortunately, Eversource Energy is well-positioned to accomplish this. The primary way in which this growth will be accomplished is by the company increasing the size of its rate base. I explained the concept of rate base in my last article on this company:

The rate base is the value of the company’s assets upon which regulators allow it to earn a certain rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the amount that it charges its customers in order to earn that specified rate of return.

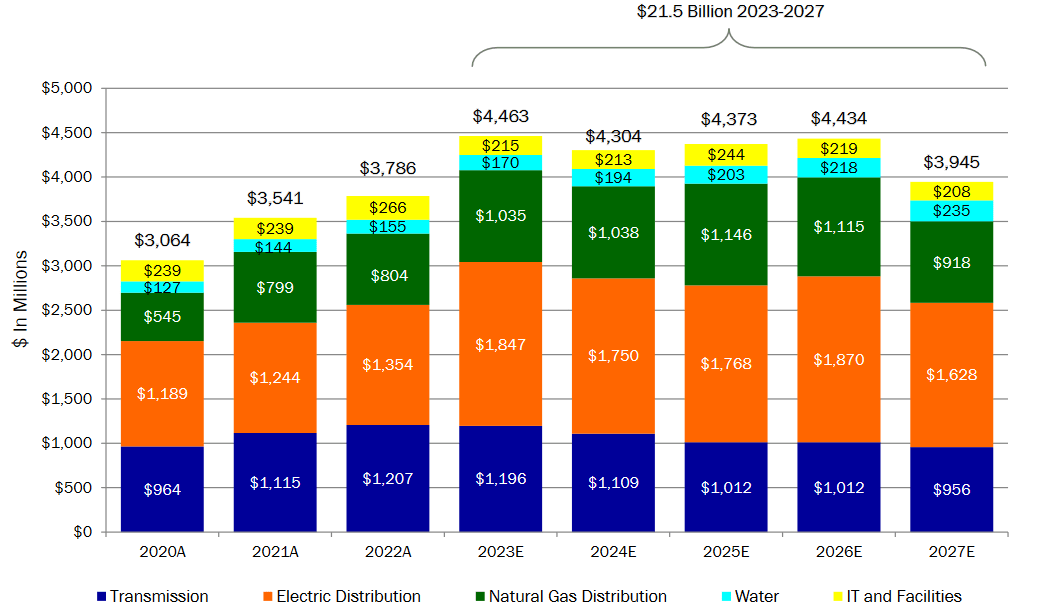

The usual way through which a company increases its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure network. Eversource Energy is planning to do exactly that over the next few years. In conjunction with its second-quarter earnings report, the company stated that it intends to invest $21.5 billion over the 2023 to 2027 period into activities and assets that will increase its rate base. The company’s earnings presentation included this helpful graphic detailing the amount that the company intends to spend in each year over the period:

{kind=link}

We can very quickly see that the amount that the company intends to spend each year over the 2023 to 2027 period is higher than the amounts that it actually spent on a yearly basis in 2022 or earlier years. This is not exactly surprising, as electric and natural gas utilities have been affected by the same inflation that all the rest of us have suffered. This pushes up the amount that the company has to spend in order to accomplish the same task. In addition, as the size of the rate base increases, the company has to spend a larger amount to hit the same percentage. Finally, the larger the rate base, the more depreciation the company will have to cover and overcome. Indeed, as we can see here, Eversource Energy’s depreciation & amortization expense has been increasing each year over the past decade:

{kind=link}

This is perhaps a flaw with the regulatory requirements that basically require a utility to constantly build out its infrastructure in order to grow its earnings, but it is what it is. Overall, we can see that the company is going to invest a considerable amount of money into upgrading its infrastructure over the next five years.

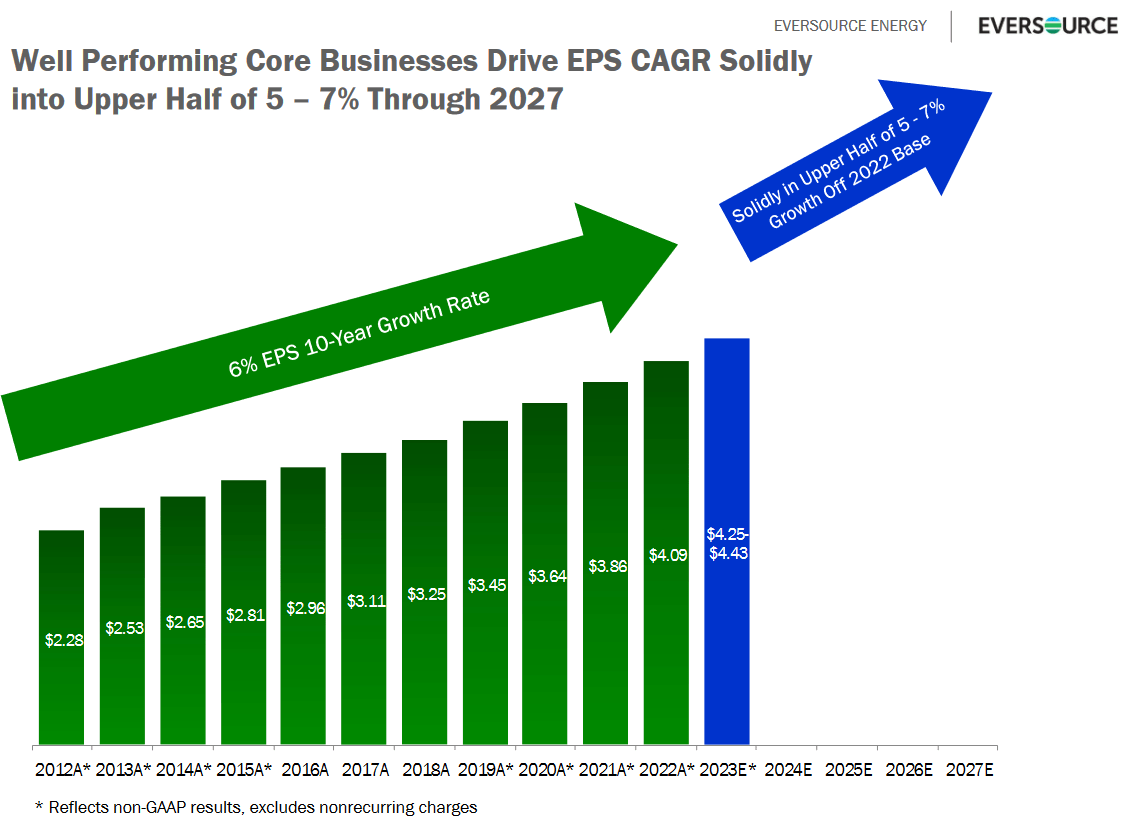

This can be expected to grow the company’s rate base at a 7.5% compound annual growth rate over the 2021 to 2027 period. This should allow the company to grow its earnings per share at a 5% to 7% rate over the period, which would represent a continuation of the company’s historical 6% compound annual growth rate with respect to its earnings per share:

{kind=link}

When we combine this with the company’s current 4.20% dividend yield, we can project a 9% to 11% average annual total return over the period. This is in line with most other electric and natural gas peers. While it is certainly not as high as the growth rate that we might expect from companies in the technology or biopharmaceutical spaces, it is an attractive return right now during this time of economic uncertainty considering the company’s overall financial stability.

Financial Considerations

It is always important to analyze the financial structure of a company before making an investment in it. I explained the reasons for this in my previous article on Eversource Energy:

It is always important that we analyze the way that a company finances itself before making an investment in it. This is because debt is a riskier way to finance an investment than equity because debt must be repaid at maturity. That is typically accomplished by issuing new debt and using the proceeds to repay the existing debt as very few companies have sufficient cash on hand to completely repay their cash as it matures. This process can cause a company’s interest expenses to increase following the rollover, depending on the prevailing interest rate in the market. As interest rates are currently at the highest levels that we have seen since the tail end of the Internet bubble in 2001, it is pretty much certain that any debt rollover today will increase a company’s interest costs. In addition to interest rate risk, a company must make regular payments on its debt if it is to remain solvent. As such, an event that causes a company’s cash flow to decrease could push it into financial distress if the company has too much debt. Although utilities like Eversource Energy usually have remarkably stable cash flows over time, there have been bankruptcies in the sector before so this is not a risk that we should ignore.

One ratio that can be used to analyze the financial structure of a company is the net debt-to-equity ratio. As of June 30, 2023, Eversource Energy had a net debt of $24.7799 billion compared to $15.7097 billion in shareholders’ equity. This gives the company a net debt-to-equity ratio of 1.58 today. This is a marked increase from the 1.50 ratio that the company had at the end of the first quarter, which is disappointing. It is somewhat understandable that this ratio would increase a bit though, as the first quarter usually results in an influx of cash from the company’s natural gas business that then drops off in the second and third quarters. This extra cash increases shareholders’ equity and decreases the net debt.

Here is how Eversource Energy compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Eversource Energy |

| 1.58 |

| DTE Energy ( DTE ) |

| 1.89 |

| Entergy Corporation ( ETR ) |

| 1.92 |

| FirstEnergy Corporation ( FE ) |

| 2.17 |

| Exelon Corporation ( EXC ) |

| 1.68 |

With the notable exception of Entergy Corporation, all of the company’s peers saw their net debt-to-equity ratios increase versus their levels at the end of the first quarter when we last discussed this company. This confirms the above statements that the increased cash inflow during the winter season combined with possibly lower capital investment (it is not enjoyable to work outdoors during the winter, after all) frequently causes net debt-to-equity ratios to be suppressed versus their summer levels.

The takeaway here is that it does not appear that Eversource Energy is overly reliant on debt to finance its operations, as it is less leveraged than its peers. This is a positive sign, especially since the company’s interest expenses have already started to increase due to debt rollovers. This should help reduce the risk that the company’s debt load could pose to its investors.

Dividend Analysis

One of the biggest reasons that investors purchase utility stocks like Eversource Energy is because of the very high dividend yields that these companies usually possess. Eversource Energy is certainly no exception to this, as its 4.20% dividend yield is substantially higher than the 1.47% yield of the S&P 500 Index (SP500). In fact, Eversource Energy’s dividend yield is quite a bit higher than the 2.61% yield of the U.S. Utility Sector ( IDU ).

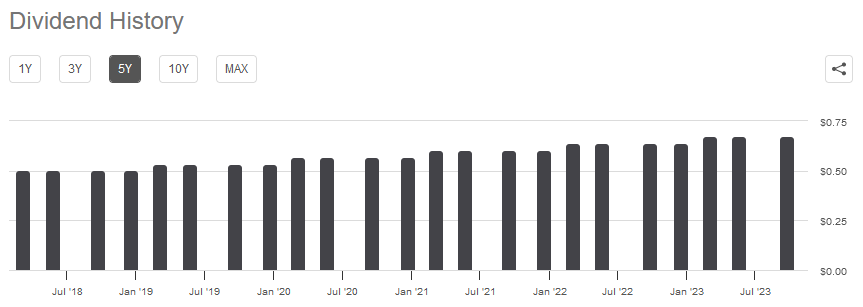

The company also has a long history of raising its dividend on a regular basis:

{kind=link}

The fact that the company increases its dividend is very important during inflationary periods, such as the one that we are in today because it helps offset the negative impact of inflation and helps ensure that the distribution can maintain its purchasing power over time. However, we still want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut that reduces our incomes and probably causes the stock price to decline.

The usual way that we examine a company’s ability to pay its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, Eversource Energy had a negative levered free cash flow of $1.8427 billion. Obviously, this is not enough to pay any dividends, but the company still paid out $891.1 million to its shareholders during the period. At first glance, this is likely to be concerning as the company is not generating sufficient cash internally to cover its dividends.

As I have pointed out in various previous articles, it is not unusual for utilities like Eversource Energy to finance their capital expenditures through the issuance of debt and equity. These companies will then pay their dividends out of operating cash flow. This is because of the incredibly high costs that are involved with constructing and maintaining a utility-grade infrastructure network over a wide geographic area. During the twelve-month period that ended on June 30, 2023, Eversource Energy reported an operating cash flow of $2.2068 billion. That was more than sufficient to cover the $891.1 million that the company paid out in dividends while still leaving a substantial amount of money left over that could be used for other purposes. Overall, this dividend is probably reasonably safe. We should not need to worry too much about it.

Valuation

According to Zacks Investment Research , Eversource Energy will grow its earnings per share at a 5.69% rate over the next three to five years. This is in line with the growth rate that we calculated based on the company’s rate base growth, so it seems pretty solid. This growth rate gives the stock a price-to-earnings growth ratio of 2.59 at the current price.

Here is how that compares to some of the company’s peers:

| Company |

| PEG Ratio |

| Eversource Energy |

| 2.59 |

| DTE Energy |

| 2.87 |

| Entergy Corporation |

| 2.58 |

| FirstEnergy Corporation |

| 2.26 |

| Exelon Corporation |

| 2.80 |

As we can see here, Eversource Energy appears to be the median valuation amongst these other fairly large utility companies. This is a sign that the company is definitely not overvalued right now. Indeed, it is at worst fairly valued. An argument in favor of it right now could be made when we consider that the company has the strongest balance sheet of this peer group but is only at the median valuation. It might make sense to pick up shares on any dips.

Conclusion

In conclusion, Eversource Energy is a fairly large utility serving most of the heavily populated regions of New England. The company enjoys remarkably stable cash flows over time, which could be a boon right now as we continue to see signs that the American consumer, which is the last bastion of strength in the economy, could be reaching the breaking point. Eversource Energy is somewhat better positioned to handle this than companies in many other sectors of the economy. The company is less reliant on leverage than its peers and its relative valuation is quite reasonable. Overall, it might be worth watching the company’s stock and buying in on any dips.

For further details see:

Eversource Energy: A Stable Utility To Buy On Dips