MCG - Everyman Media Group: Cheap U.K. Listed Cinema Chain With Superior Growth Potential

- Everyman Media Group, a UK-based cinema chain, trades at a similar valuation to its UK and US counterparts despite historically delivering better growth and having far better growth prospects.

- The company trades at 1.35x EV/sales, ~5.5x EV/OCF and ~8x EV/EBITDA while peers trade on 2.1x FY22 EV/Sales, ~14.2x EV/OCF and ~7.4x EV/EBITDA.

- Everyman has a superior product offering which drives strong customer loyalty and higher Food and Beverage (F&B) spend per head (SPH) that continues to accelerate - now double IPO SPH.

- For a lot of Cinema chains COVID has proved to be a disaster but for Everyman, it has provided an inflection point to recommence expansion while others falter.

- This opportunity exists because Everyman trades on AIM and suffers from low liquidity, now cinema is operating without restrictions Everyman will be able to show its worth through FY22&23 and earn its deserved re-price.

Note: For US investors who wish to trade Everyman Media Group, they must do so directly on the London Stock Exchange - there is no US ticker for Everyman

I have covered Everyman Media Group plc (LSE: EMAN) extensively in the past. It remains the largest holding in my high-conviction portfolio and whilst the share price has slowly dragged lower in 2022, I have become more convinced about the market's undervaluation and under-appreciation of the company.

Admittedly, on the face of it, the cinema industry doesn't appear to be an attractive sector to park your money. Prior to the pandemic even though box office performance remained resolute, concerns regarding the rise of streaming services were increasing. The pandemic accelerated this shift dramatically as cinemas were forced into prolonged closures while the likes of Netflix became major beneficiaries of the stay-at-home economy. Now cinemas are facing a new challenge; the increased risk of stagflation and the ramifications this could have for the consumer discretionary industry. However even considering this, box office performance has been strong in both the UK and US through the start of 2022.

Everyman Cinema in Kings Cross London (Everymancinema.com)

Despite these headwinds, there is a small UK cinema operator that delivered its record revenues in H2 2021 and maintains a healthy balance sheet. Everyman is attractive because, despite the challenges the industry is facing, the company is now benefiting from the niche it has carved out within the market since its inception. Whilst other Cinema chains like Cineworld ( OTCPK:CNNWF ) falter amid a significant debt load, Everyman is expanding - set to open four new venues in 2022 and expected to deliver 26% revenue growth in 2022 compared to 2019 (pre-COVID)

This opportunity exists because Everyman trades on the Alternative Investment Market ((AIM)), the sub-market of the London Stock Exchange for small-cap companies. Whilst some equities consistently receive steady volume flows on AIM, Everyman suffers from extremely low liquidity which means trading is incredibly inefficient. This isn't helped by the fact that Everyman's operations have been incredibly disrupted over the last two years, making it a lot harder to break down the figures and understand how the company is performing on a no-restriction basis without relying on forecasts. Whilst Everyman isn't up-listing to the main market anytime soon, I do believe the share will attract more liquidity as we move out of the pandemic. Everyman now has a clean slate ahead to show its worth and deliver better growth and numbers than its peers and it has already started to do this. When Everyman delivers the growth and profitability that I believe it can, the company will then start to see its deserved reprice.

In this deep dive write-up, I am going to discuss what separates Everyman from its competitors and how this has driven exceptional Food and Beverage (F&B) spend. I am also going to dig into the financials and show why, with consideration of growth prospects, Everyman is incredibly undervalued in comparison to peers.

Introducing Everyman's story and its edge

Everyman Media Group was founded in 2000 by Daniel Broch, who acquired the Everyman Cinema in Hampstead which dated back to 1933. From its small beginnings, Everyman expanded quickly acquiring Screen Cinemas in 2008 which brought the venue count to eight - Broch sold out his majority stake at this point. The business was then listed on AIM in 2013 and continued to roll out its offering across the UK. By 2019/20 the share price was nearing all-time highs of over 200p as the company had delivered consistent growth and turned profitable.

Then the pandemic hit, massively disrupting Everyman's growth journey and it soon felt like all the efforts Everyman had made over the previous seven years since listing had gone to waste. Roll forward to today and, while the market cap remains well below its 2019 peak, digging into the details and fundamentals it is very clear that Everyman is in a far better position than the market would think. It is easy to put Everyman in the same bracket as its peers and come to the conclusion that cinema has and will continue to suffer and therefore so will Everyman.

Yet that hasn't been and I don't think will be the case moving forward. Everyman has a clear-cut focus on customer service and curating the best possible experience for customers. This is achieved by:

- Exceptional unique interior and luxurious sofas - This is their specialty; Everyman replaces seats with couches and delivers food to your seat.

- An engaged and welcoming team - To achieve this Everyman had to build a strong team culture over a long period of time. Take a look at Taqweem R's recent Linkedin post for more.

- Enhanced menu options - Everyman constantly looks to improve and expand its menu, as shown through the introduction of the 'Spielburger' offering

Whilst the company isn't as well known as the likes of Cineworld due to its smaller venue count, Everyman has developed a reputation for its customer experience , making it difficult for larger peers to replicate that brand in the UK.

Over time this has led to Everyman becoming a brand consumers love, driving a steady increase in demand. All it takes is a quick 'Everyman Cinema' search on Twitter to find out how much a lot of customers enjoy the experience:

Or take a look at this tweet:

There is a clear trend here - Everyman is cultivating an all-around entertainment experience that entices consumers into venues in its own right. Former CEO Crispin Lilly previously discussed this edge and how Everyman is less reliant on market tailwinds when he talked to Piworld about the H1 2019 results :

We are not as dependent on the underlying success of films that fuel the market (compared to peers). We succeeded in flipping the equation from people buying a ticket to the cinema purely based on the film. The typical equation is usually I want to see that film, what time is it on and where is it showing. We have flipped that around to - I want to go out next week, I want to go to the Everyman again . Once we start to see that, people take chance on the type of films they want to see.

This beautifully sums up Everyman's edge. Indeed, I discovered Everyman as a result of my love for the experience and my belief that no one has yet been able to deliver that experience at the scale that Everyman has achieved.

Excelling on its KPI's and outperforming peers

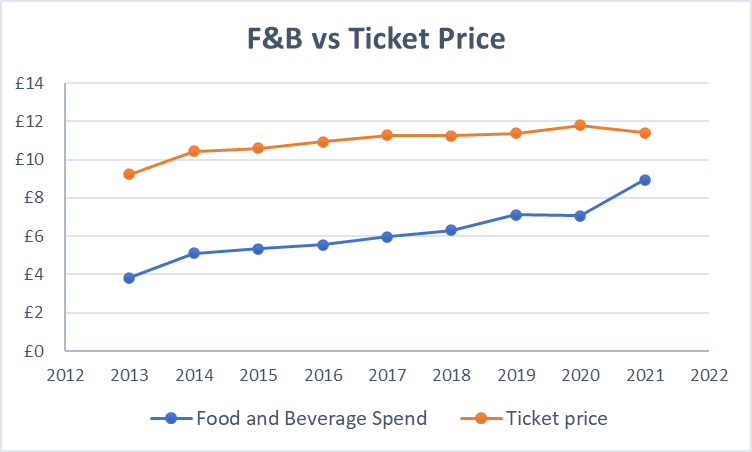

However, don't just take my word for it - Everyman's premium focus has allowed the company to charge higher prices driving Food and Beverage (F&B) spend higher. Below I have charted F&B spend per head against ticket price over time.

Compiled by author from Company Reports

{kind=link}

Everyman was operating 36 venues by the end of 2021, back in 2013 the venue count was just 10. Since 2013, Everyman has grown F&B spend per head by 234% while also expanding the number of venues by 260% . This allowed the company to deliver £64 million of revenue in 2019 compared to just £11.5 million in 2013.

The gap between the two Key Performance Indicators (KPIs) has consistently narrowed as F&B spend has grown, and that trend accelerated in 2021. This is where I believe Everyman has seen an inflection point as a result of the pandemic. The positive implication of higher F&B spend can be seen on the top line where despite Everyman achieving 97% of H2 2019 admissions in H2 2021, revenue increased 14.7% . As a quick comparison, Cineworld achieved just 63% of H2 2019 admissions in H2 2021.

The F&B spend is the higher margin component of sales (as many readers will know - F&B is the bread and butter of cinema margins). F&B made up 40.8% of Everyman's sales in 2021 and this has driven significantly improved financial performance. I expect these positive trends to continue as, in its final results for 2021 (delivered in March 2022), Everyman announced :

So far in 2022 admissions momentum has continued and we remain focused on delivering quality customer service throughout food, drink, staff and film.

Those customers who have returned to Everyman are clearly of higher value. A lot of sales in the industry are made up by a small percentage of consistent customers. Whilst Everyman doesn't give any specific data regarding this, we do know that in the US half of ticket sales come from just 11% of moviegoers . This figure is most likely similar to the UK.

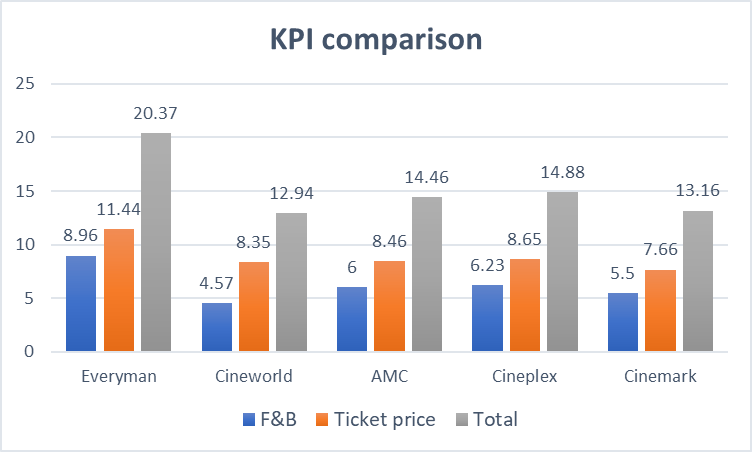

Whilst some may associate the disproportionate jump in F&B spend with pent-up demand, I believe more credit should be given to the influence of menu enhancements and customers going to Everyman to get the 'full experience'. As mentioned, customers are far more willing to indulge at Everyman as it's a premium experience. Below I have tabled a comparison of Everyman F&B and ticket spend against all publicly listed peers.

| Cinema Chain |

| F&B |

| Ticket Price |

| Spend Per Head |

| Everyman |

| £8.96 |

| £11.44 |

| £20.04 |

| Cineworld |

| £4.57 |

| £8.35 |

| £12.94 |

| AMC ( AMC ) |

| £6 |

| £8.46 |

| £14.46 |

| Cineplex ( OTCPK:CPXGF ) |

| £6.23 |

| £8.65 |

| £14.88 |

| Cinemark ( CNK ) |

| £5.50 |

| £7.66 |

| £13.16 |

For those who prefer a more visual form:

Compiled by author from company reports

{kind=link}

Everyman's unique market position and strong offering is clearly paying dividends as customer spend per visit is in a different ballpark.

Taking market share and developing new revenue pipelines

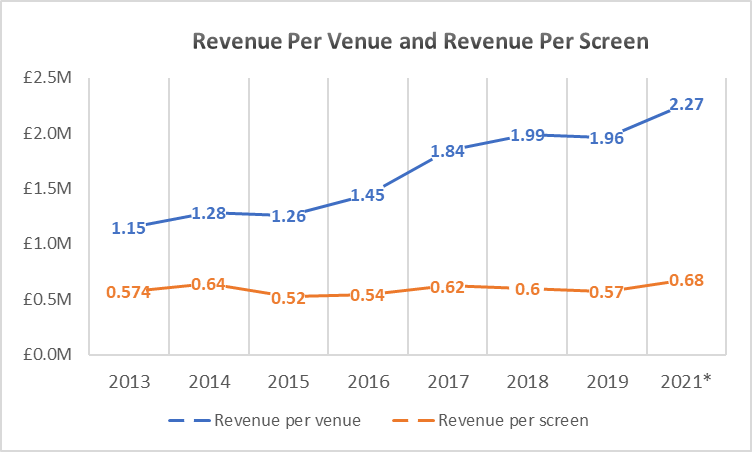

When Everyman was first listed in 2013, its market share was just 0.74%. At the time the board said it believes that there is 'significant growth potential for an independent cinema chain within the UK'. They were correct - fast forward to 2021 this share now stands at 4.5%. Below I have compiled Everyman's Revenue Per Venue ((RPV)) and Revenue Per Screen (RPS) from 2013-2019. *I have added H2 of 2021 and annualized it as that has been the only period since the onset of the pandemic that has been pretty much restriction free.

Calculated by author from Company Reports

{kind=link}

Note that these figures are calculated using the total number of venues at the end of a period, therefore many of the venues opened during a given year will not have a full year of revenue contribution.

Nonetheless, it shows a steady increase in RPV and a more consistent RPS. The reason RPS is fairly level reflects the multi-screen capacity of new cinema openings. Due to this, a lot of the newer screens are of smaller size with smaller capacity.

Despite this, there is still a strong breakout in FY21 where RPS hit a record £680k p.a., an increase of 19.2% YoY. Everyman halted its expansion with the onset of the pandemic, therefore the percentage increase in venues in 2021 wasn't very large (10%). This gave a large majority of venues a full half-year of revenue contribution.

This expansion has allowed Everyman to continually grow its market share:

| Year |

| Market Share |

| Growth% YoY |

| Venue Count |

| Growth% YoY |

| 2013 |

| 0.74% |

| N/A |

| 10 |

| N/A |

| 2014 |

| 0.9% |

| 21.6% |

| 11 |

| 10% |

| 2015 |

| 1.12% |

| 24.4% |

| 16 |

| 45% |

| 2016 |

| 1.64% |

| 46% |

| 20 |

| 25% |

| 2017 |

| 2.11% |

| 28% |

| 21 |

| 5% |

| 2018 |

| 2.53% |

| 20% |

| 26 |

| 23% |

| 2019 |

| 3.1% |

| 22% |

| 33 |

| 27% |

| 2021 |

| 4.5% |

| 45% |

| 36 |

| 9% |

I think the above table is useful as it allows us to see how much of Everyman's increase in market share is driven by the rollout of new venues and how much is organic demand growth. Market share growth (CAGR: 29.4%) has outstripped venue growth (CAGR: 20%) .

Due to the luxurious nature of Everyman's venues, the company has also been able to book additional income through venue hires. Moreover, the company has secured exclusive partnerships with other premium brands such as Jaguar and Green & Black's chocolate. Everyman groups together these revenues with its memberships (have varying price points, more detail can be found here ). In FY21 this revenue came to £3.5 million or 7.1%.

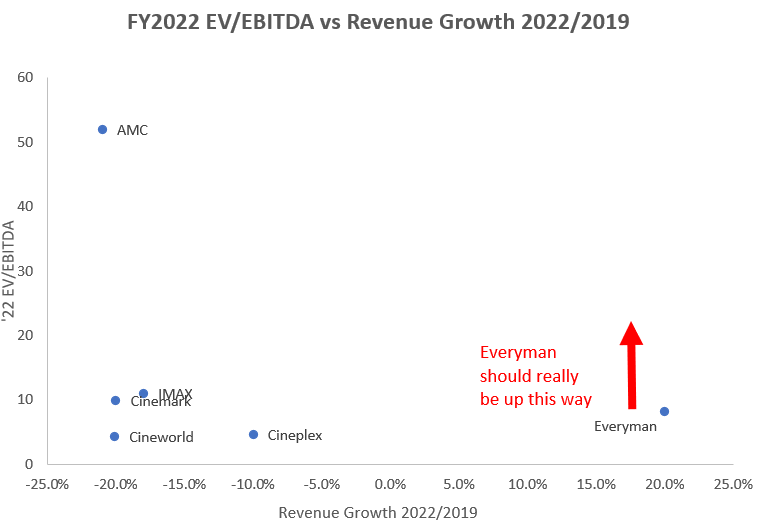

Financial analysis, profitability and comparison to competitors

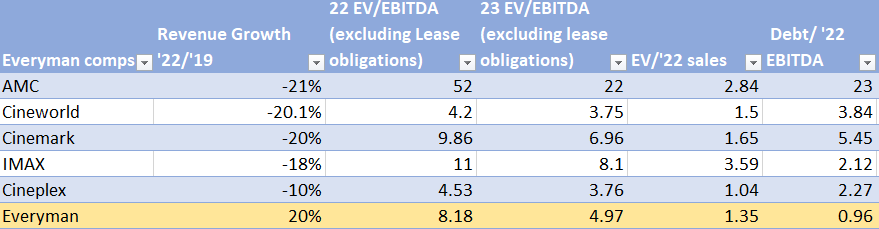

Canaccord Genuity expects Everyman to deliver £78.5 million in revenues for FY22 with EBITDA at £13 million. Due to the disruption of both 2020 and 2021, I am using FY22 metrics as the basis for comparison between competitors. Before drawing comparisons with other quoted chains it is important to understand the implication of capitalized leases and operating leases.

Capitalized leases are included in long-term debt and operating leases are not. Cineworld, Cinemark and Everyman (UK and Canadian listed companies) have a huge weighting towards capitalized leases while AMC, Cinemark and IMAX (US companies) have pretty much all their leases booked as operating leases. This massively affects the EV figure. Lease obligations are a normal course of business and while they are included as part of 'statutory accounts', they are not the key focus for companies and management when looking at debt. Everyman opened up its Final Results outlining its total debt figure as '£12.5M' (not the £91.65M that can be seen on the balance sheet of its statutory accounts which includes capitalized leases) while Cineworld in its summary for its preliminary results outlined its net debt (excluding lease liabilities).

Due to this I have removed leases from the debt figure in order to draw a fairer comparison between companies operating in different jurisdictions. Refinitiv daily time series EV value was used for the initial figure.

Calculated and compiled by author using Refinitiv figures and estimates

{kind=link}

As you can see from the comparisons, I find Everyman's current valuation to be hugely misplaced. Everyman is anticipated to grow revenues at 20% this year compared to FY19, while its competitors' revenues are all likely to shrink.

Turning to EV/EBITDA given Cineworld's extreme debt levels and precarious financial position, I do not believe the valuation difference to Everyman is anywhere near big enough. The administration risks for Cineworld have been heavily documented and rightly so, its debt load is extremely high (over $5 billion). At this point, Cineworld's EV is made up nearly wholly of debt and it has become a binary bet on whether it collapses or survives (I believe the former is far more likely). The market is still adjusting for this fact with the Cineworld share price down over 67% in the last 52 weeks. Everyman is growing EBITDA far faster than Cineworld in 2023.

Even drawing a comparison to Canadian-based Cineplex, which trades on the most reasonable valuation, I believe Everyman should command a far higher premium as it holds a far more deleveraged balance sheet and has substantially better growth potential. Everyman appears even more undervalued when you look past this year. In FY23 the company is expected to grow revenues to £105.7 million (+34%) and in FY24 revenues are expected to reach £131.9 million (+24%) . EBITDA is expected to be £21.7 million and £29.5 million respectively. This significantly lowers Everyman FY23 EV/EBITDA multiple. In contrast to Cineplex which is only expected to achieve £1.696 billion in revenue by the end of FY24. That would be an increase in revenues of just 1.8% from 2019 while Everyman is slated to more than double its revenues over the same period.

EBITDA is also only expected to be 5% better over the period to 2024 for Cineplex as well. Everyman should be earning a significantly higher multiple for the far higher growth it has delivered and is anticipated to deliver on both revenues and EBITDA.

Turning to IMAX ( IMAX ) and Cinemark, they are only expected to deliver revenue growth on 2019 by the end of 2024 . This slower growth and slower recovery is unsurprising and reflects competitors' scale. This should mean that the smaller, more versatile and faster-growing Everyman deserves a far higher multiple.

compiled by author using Refinitiv figures and estimates

{kind=link}

The issue for Everyman is that this is just one sell-side forecast - which is the only coverage the company has received. Whenever box office figures are discussed, Everyman is never included in that discussion. Morgan Stanley recently upgraded Cinemark to overweight on its optimism for box office, notes like these will draw discussion and comparison to the larger peers - but Everyman won't be discussed as a small-cap AIM listed equity.

There is clearly a stark belief from the market (though in this case this 'market' is just a few retail traders) that Everyman will not get near achieving these forecasts. When In fact I believe that FY22 top-line consensus is conservative, here's why:

- Everyman is opening four new venues through the year, Edinburgh has opened (April) and three more are to come. The Borough Yards venue was opened in December, and will make full contribution to 2022 numbers.

- If H2 2021 revenues were annualized, the figure would be £82 million , early box office (Q1 UK and Ireland) and with a strong film slate in H2 (which is historically the stronger half year) give me the belief that box office performance in 2022 will be similar to that of second half of 2021.

Considering the above I believe at the upper end of expectations Everyman could hit £84 million in revenues which would provide a boost to both EBITDA and pre-tax profit and make the valuation look even more lucrative.

Cash flow

Now to compare cash flows: note I have once again annualized H2 2021 cash flows to provide a fair comparison between UK and US businesses that experienced differentiated levels of disruption in the first half of 2021. I have also excluded lease obligations from the EV figure for Cineworld, Everyman and Cineplex.

| Total OCF H2 '21 (annualized) |

| EV/OCF '22 |

| IMAX |

| $46.2M |

| 25.15x |

| Cineworld |

| $540M - double check |

| 10.5x |

| AMC |

| -$67.4M |

| N/A |

| Cineplex |

| CAD158M (USD $122.94M) |

| 9.8x |

| Cinemark |

| $378M |

| 11.4x |

| Everyman |

| £20M ($24M) |

| 5.5x |

When comparing cash flows, Everyman's valuation looks even more ludicrous. The heavy debt load of nearly all of its competitors is massively weighing down on their balance sheets and Everyman remains the stark outlier.

Drawing comparison to high-quality hospitality

Considering the large differences between Everyman and its peers in terms of size and debt levels, investors may want to draw comparison to perceived more 'high quality' hospitality businesses. Below I have compiled a mix of hospitality stocks.

| '22 EV/EBITDA |

| '22 - '24 Revenue CAGR |

| '22 - '24 EBITDA CAGR |

| Choice Hotels ( CHH ) |

| 15.25 |

| 2.85% |

| 7.6% |

| Texas Roadhouse ( TXRH ) |

| 10.8 |

| 9.47% |

| 13.63% |

| Red Rock Resorts ( RRR ) |

| 9.1 |

| 4.08% |

| 2.12% |

| Hilton Worldwide ( HLT ) |

| 15.82 |

| 12.95% |

| 15.77% |

| Membership Collective Group ( MCG ) |

| 16.3 |

| 28.5% |

| 54% |

| Hyatt Hotels ( H ) |

| 13.33 |

| 9.38% |

| 19.18% |

| Everyman |

| 8.18 |

| 29.72% |

| 51.5% |

The majority of hospitality falls into the 10-15 EV/EBITDA range, with all of them expected to put in lower growth than Everyman over the coming years. Red Rock Resorts is the only other company with a sub 10x ratio and they're quite clearly expected to grow both revenue and EBITDA at a far slower pace than peers. It is clear that in the hospitality sector the market is awarding higher valuations to the likes of Hyatt and Hilton for higher growth.

I believe the most suitable comparison comes between Membership Collective Group ( MCG ) and Everyman where it's clear a significant premium has been applied to MCG for its far superior expected growth moving forward. MCG is also similar in terms of its premium offering and focus. MCG owns Soho House - a private members club. The company also has a more 'speculative' nature as it only IPO'd very recently (2021) and does not have as much of a sustained operating history as well-known brands such as Hilton.

Everyman trades at half the price of MCG which has delivered consistent negative operating cash flow (OCF) bar Q2 of last year where the company delivered just $10 million in OCF. On the whole in 2021 MCG delivered negative $127 million in OCF, while Everyman delivered positive $9.1 million for the Full Year. To me, as a base case, Everyman should have the same EV/EBITDA multiple (excluding its lease debt as I have) as MCG and that would mean at least double the current share price .

Why does this opportunity exist?

Considering all the discussion about Everyman excelling on all its KPIs, experiencing accelerating demand for its offering while also trading at similar forward valuations to heavily indebted peers that have far weaker growth prospects - it begs the question, why does this opportunity exist right now?

It is because the market is inefficient. This is particularly true for the small/micro-cap space and that's why there can be such great opportunities in this market. This is even more true for AIM and Everyman. AIM is very much a mixed bag in terms of liquidity, some companies can experience steady streams of volume from retail investor bases. While others experience very little liquidity. Frustratingly Everyman falls in the latter camp. Everyman, and a lot of AIM, experiences very little institutional interest. No institutions trade EMAN, though many hold quite large positions:

Everyman Investor Relations

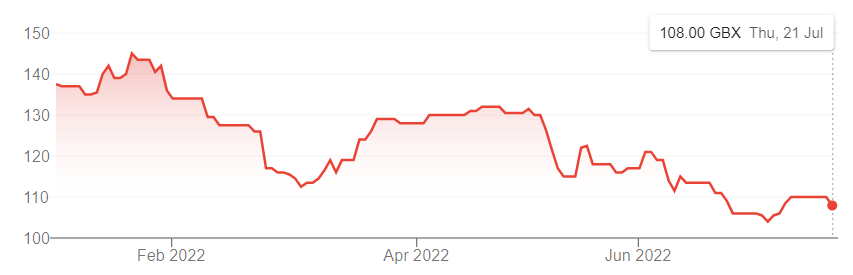

Since the turn of the year just 4.4 million shares have changed hands, which represents 9.6% of the free float. Combine this with the fact there is little to no sell-side coverage on Everyman, the company gets very little attention. To understand the inefficiency let's compare the share price performance to a consumer discretionary ETF - the XLY (NYSE: XLY )

Now let's take a look at Everyman's share price Year To Date (YTD)

{kind=link}

The XLY is down 27% YTD and Everyman is down 21% YTD. Whilst a difference, it is quite subtle. However, the inefficiency can be seen in the manner of Everyman's decline this year. From the 3rd of January to the 27th of January, Everyman was up 3% - the XLY was down 17%. In all fairness, Everyman did deliver a positive trading update on the 21st, however there wasn't a particularly large reaction to it. Yet when the market began its descent in January pulling pretty much all equities down as everyone and everything was affected by the broader market, Everyman was level. This to me highlights the incredible inefficiency of this thinly traded company.

That is exactly why I believe it trades at the price it does today - inefficiency and simply not enough understanding from the market of the opportunity and the finer details of how impressive Everyman's performance has actually been. Whilst Everyman is thinly traded, it isn't too difficult to build a relatively large position over time - in fact ask CEO Alex Scrimgeour. Scrimgeour was appointed CEO of the company at the start of 2021 and over time has steadily accumulated a significant position in the open market.

| Shares purchased |

| Price paid per share |

| Date of notification |

| Cost of purchase |

| 119,355 |

| 150 |

| 08/04/2021 |

| £179,000 |

| 45,128 (Scrimgeour's Wife) |

| 155 |

| 01/06/2021 |

| £69,750 |

| 32,300 |

| 139 |

| 23/07/2021 |

| £44,897 |

| 44,191 |

| 130 |

| 28/09/2021 |

| £57,448 |

| 10,000 |

| 113 |

| 17/06/2021 |

| £11,300 |

| 250,974 |

| £362,395 |

Considering that Scrimgeour was paid around £300,000 in total remuneration (excluding share based payments) for 2021. These buys are very significant and are well over his annual salary base of £244,000 - he clearly believes the shares are undervalued and he is putting his money where his mouth is.

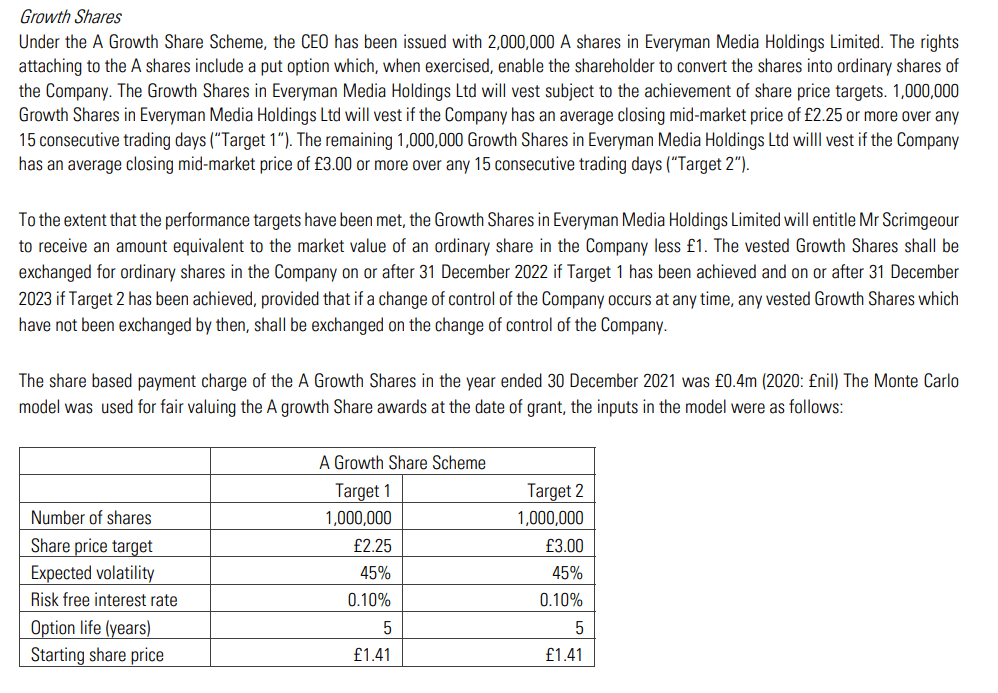

He is also incredibly well incentivized to achieve large share price upside through his 'growth shares':

{kind=link}

Catalyst for the reprice

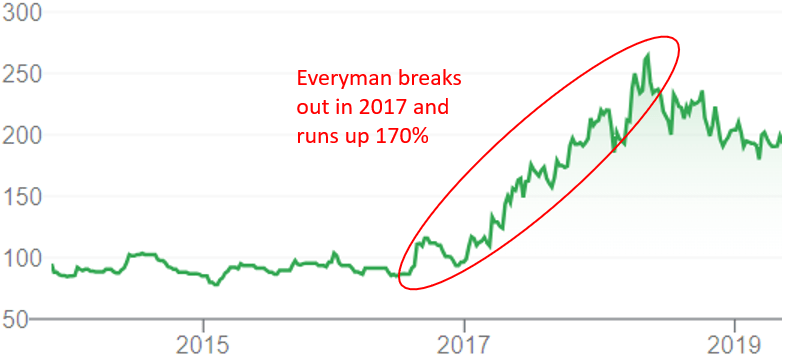

Considering the lack of liquidity, how Everyman actually realizes upside needs to be considered. Looking back at the share price action, the firm traded between a channel from 2013 to 2016, before breaking out higher on FY16 (released early 2017) results and continued in an uptrend till mid-2018:

{kind=link}

Now reflecting back on a lot of the figures I have discussed in this article, it is clear that this rise was initiated by the outsized growth reported in FY16 where revenue per venue expanded after a dip in 2015, and market share grew 46%. This trend then continued with even more explosive top line growth in 2017. 2016 was also the point where Everyman turned profitable for the first time, net income then increased significantly in 2017.

I believe through 2022 and 2023 the company can achieve a similar rise and even run higher. This is because the H2 21 results were not just a 'flash in the pan' and Everyman will continue to receive strong demand for its offering despite the headwinds in the market. I believe F&B spend will prove to be enduring, massively boosting the top line figures moving forward. Due to the distinct lack of coverage and massively disrupted figures, a lot of the gains made in H2 2021 have largely been ignored. If Everyman shows these are enduring gains and reports strong figures while larger counterparts like Cineworld continue to struggle - which is what the forecasts show and what I fully expect to happen - then a reprice will come.

Risks

The primary risks that face Everyman are the same risks that the majority of cinemas are facing across the world and these are centered around the macro environment and the effects this could have on consumer discretionary spend. However, as mentioned, Box Office figures show that the industry has performed well so far this year and there is plenty to be optimistic about regarding the film slate in the second half of the year. And sometimes a cinema ticket can be a cheaper night out than drinks and dinner and may substitute for more expensive entertainment during an economic downturn. Historically, Cinema admissions remained strong during the depression of the 1930s.

There is also the issue of lack of liquidity. The board hasn't made large efforts to address this issue. The investor relations page, while it does contain all the necessary up-to-date information and disclosures, is outdated. A lot of press relations is outsourced to Alma PR. I believe new CEO Alex Scrimgeour will make more of an effort to address this, particularly after acquiring a large stake in the open market - it is more than in his interests.

Conclusion

So bringing it all together:

- Everyman has steadily built up a strong presence and reputation in the UK driven by the continued roll out of its unique offering.

- Everyman's investment into its venues and menu enhancements have helped to drive incredible Food and Beverage spend per head growth which puts it in a different ballpark in terms of customer spend to all its listed competitors.

- Despite the fact Everyman is experiencing superior demand for its offering, is currently and is going to deliver strong revenue growth (even with more conservative estimations), the company still trades at moderate valuation to its peers despite the heavy debt levels of many competitors.

- When compared to other hospitality businesses in industries with lower debt Everyman becomes even cheaper on both an EV/EBITDA basis and in terms of the operating cash flow it produces. I see a lot of similarities to another hospitality business MCG which currently trades at double the valuation of Everyman and I believe, as a base case, Everyman should earn a similar valuation which would be double the current share price.

- A mixture of KPI outperformance and continued expansion has driven record-ever revenues in H2 2021 for Everyman, with the roll out of four new venues this year that is set to improve.

- Low liquidity and limited coverage mean that many have overlooked this clear opportunity.

- Between 2017 and 2018, the Everyman share price more than doubled following two years of excellent trading results, I expect a similar reprice on the back of a strong 2022 and 2023.

Considering the above points, I believe Everyman should start to earn its deserved reprice as soon as its strong H2 2021 performance is seen to be enduring into 2022 and beyond. At this point I think those results largely went overlooked and ignored, however as the underlying trends become clearer, Everyman Media Group is undoubtedly one of the strongest small cap buys in the market.

For further details see:

Everyman Media Group: Cheap U.K. Listed Cinema Chain With Superior Growth Potential