EVGGF - Evolution AB: An Unknown Gem Dominating The Live Casino Solutions Market

2023-10-17 13:00:46 ET

Summary

- Evolution AB is a company with strong financials, including negative net debt, high return on capital, and impressive revenue and free cash flow growth.

- The company operates in the live casino solutions market, providing games and services to major gaming operators worldwide.

- Evolution has a dominant competitive position, with a strong focus on innovation, differentiation, and customer satisfaction. It holds 80% of the live software market share.

How much would you be willing to pay for a company with the following characteristics?

- Negative net debt.

- Return on capital of 29.20%.

- A revenue CAGR of 49.40% from 2018 to 2023E.

- A free cash flow CAGR of 72.60% from 2018 to 2023E.

- A free cash flow margin of 57.60%.

- A dividend per share that went from $0.27 to $2.63 in 5 years.

Your answer is probably "a lot", but I have good news: there is no need to overpay this company since the current market cap/NTM free cash flow is only 18.55x. The company in question is Evolution AB ( EVVTY ).

Typically, if something is relatively cheap compared to its potential I focus on the downsides in order to justify its low valuation. Most of the time there is at least one major problem that justifies an undervaluation by the market, but in this case I could not find anything to dilute my interest. In all fairness, I think there are two factors that affect Evolution's underestimation the most:

- The first is that few people know about this company and you can also see this from the followers on Seeking Alpha. It is based in Sweden and is not yet listed on major U.S. exchanges. Also, not all brokers allow the purchase of its shares.

- The second is that Evolution AB is a sin stock since it has a major role in the gambling market. Just as with companies that sell tobacco, not all investors are willing to have a company that offers harmful products.

These two factors, combined with a time of pessimism in the markets, made it possible that Evolution could be traded at multiples that were significantly very low relative to its characteristics and potential.

Business model

After this brief intro, let's now talk about the most important thing: how does Evolution make so much money? After all, even Visa ( V ) struggles to achieve a free cash flow margin of 57%.

{kind=link}

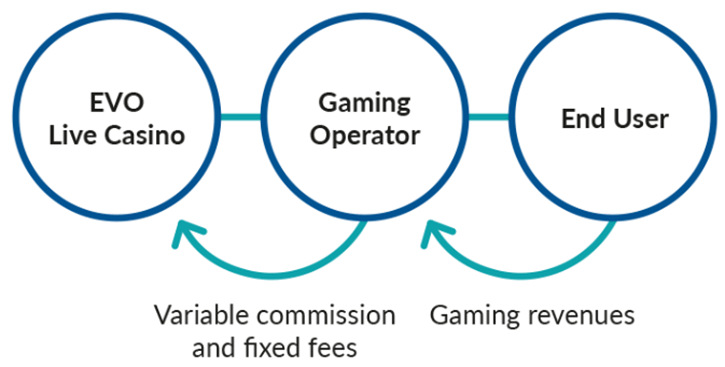

Evolution develops, produces, markets and licenses fully integrated Live Casino solutions to major gaming operators worldwide. These gaming operators subsequently market the products to their end users. Evolution's customers include the world's most popular gaming platforms, such as PokerStars, William Hill, and Sisal. In addition, customers also include some land-based casinos.

{kind=link}

Simply put, Evolution is in charge of creating the casino games in which gamblers will participate, but its earnings depend indirectly on them. In fact, most of its revenue comes mainly from the commissions imposed on gaming operators' earnings. In particular, Evolution does not treat its customers equally; in fact, those with low bargaining power pay commissions of up to 20 percent. To these, set-up fees are also added.

To date, this business model has proven very successful for three reasons:

- The first is that Evolution is in no way exposed to the losses of its customers. Once the contract is signed -which is usually three years- each month the gaming operators must pay the commission based on their earnings. So, in the event of operator losses, Evolution would not suffer any damages. Moreover, even if an operator went bankrupt, there would not be many problems given the heterogeneity of its customers.

- The second reason this business model works so well is its scalability. Once a game appreciated by bettors is created, gaming operators will flock to grab the license. Since some games allow hundreds of users to participate at the same time, there will be hundreds of bets each round. In a traditional casino this would not be possible since the people who can bet at the same time are limited. More people playing means more money for the gaming operator and consequently more money for Evolution.

- The third reason is that Evolution has the ability to treat its customers differently given its strong bargaining power. Contracts are customized, which means that the same game is priced differently depending on the customer who intends to get the license. Operators have no choice but to accept Evolution's terms since its games are the most popular worldwide. Taking a concrete example, try to imagine what would happen to a gaming operator who has not purchased a license for Crazy Time : it would limit the sign-up of new users.

In summary, the first point leads to steady revenues, while the second and third leads to rapid growth with high margins.

Over the past few years, management has done an excellent job and has positioned Evolution for long-term prosperity. As I will show later, the online gambling market is growing rapidly and there is fierce competition to grab new users. In any case, what surprises me most is that Evolution is not negatively affected by the competition, quite the contrary.

While PokerStars battles with William Hill and hundreds of other gaming operators, Evolution gives them all the tools to compete. Basically, operators clash on the battlefield and Evolution sells them weapons: the wider the war, the more Evolution will get richer.

Evolution's competitive position reminds me a lot of that of ASML ( ASML ), a well-known Dutch company that produces the world's most advanced lithography machines. While Intel ( INTC ), TSMC ( TSM ) and all the other major semiconductor companies compete for more market share, they all buy ASML's lithography machines to prevail among themselves. In other words, as in the gold rush, it was not the miners who got rich but those who sold shovels and picks.

Competitive advantage

At first glance it may seem that Evolution's competitive advantage is rather fragile; after all, it only takes a camera, some ideas, and a good presenter to create a new game that would appeal to bettors. Certainly, we are not talking about a company that produces machinery that is impossible to reproduce like ASML; however, I think its competitive advantage is much more important than one might think. In particular, I believe Evolution's position is dominant not only toward competitors but also toward customers themselves.

Land-based casinos

Although some land-based casinos are Evolution customers, a large part of them are not, so they should be considered direct competitors. After all, if a bettor plays in the casino he is in fact taking away possible income from the online operators and thus from Evolution.

European Online Gambling Key Figures 2022 Edition : European Gaming and Betting Association (EGBA).

As we can see from this picture , although online casinos have achieved strong growth boosted in part by continued lockdowns, land-based casinos still remain at the top in terms of total revenue. In the next few years, it is unlikely that the hierarchy will flip; however, I am hopeful from a long-term perspective. Land-based casinos have existed for centuries, while online casinos have only spread in the last 10 to 15 years and have already gained a strong following. In fact, the latter are expected to experience a higher growth rate in the coming years.

In my opinion, there are three main advantages that online casinos possess over land-based casinos:

- The first is to scale the business better and have higher profit margins. If hundreds if not thousands of people can play continuously and at the same time, the house will make much more money. In land-based casinos, the playing times are much longer and there are technical limitations.

- The second is that the online casino has fewer costs to support than the physical casino. There is less staff, there is not a huge structure to maintain, and it is possible to place offices in strategic locations where the cost of living is lower. For example, Evolution operates mainly in Malta and Cyprus.

- The third advantage is that Evolution, because it has a lighter cost structure, can afford to offer games at a much higher RTP than land-based casinos.

On this last point I think it is worth dwelling as it represents a crucial aspect.

For those who do not know, RTP stands for Return to Player, and it indicates how much a bettor expects to earn in a given casino game. Obviously, the house always wins, so the RTP will always be less than 100%. In the case of land-based casinos RTP is between 70% and 90%, which means that out of $100 played the average bettor will get back between $70-$90. In the case of Evolution the situation is quite different.

mrq.com

These are some of the games offered by Evolution and their RTP is extremely high: no physical casino can guarantee such an RTP given the costs it has to bear. This means that the average bettor is more likely to lose less playing Lightning Blackjack than Blackjack at a land-based casino. But there is more.

As already anticipated, the house always wins in the long run, however, the way it does it is totally different in the games offered by Evolution: in fact, the mechanism is much more devious. If in traditional casinos the bettor starts losing money already from the first rounds since the RTP is lower, in the case of Lightning Blackjack this process is longer and more complex. The bettor before losing will believe that he is in control of the situation and sometimes may even win small amounts. Either way, the outcome in the long run is always the same, and the resulting frustration of defeat is greater. It is highly improbable that a bettor will stop playing after pocketing a small win: the temptation to continue is too strong.

This mechanism generates much more addiction toward that particular game, and the bettor will be more enticed to play it again. So, a high RTP generates less revenue in the first few rounds of play, but causes much more addiction in the bettor. It is a diabolical mechanism, and combined with the ease of access to online casinos, it is Evolution's greatest strength.

Finally, I would like to clarify that I do not believe that land-based casinos have no future, but that online casinos are on the rise. Playing Blackjack from your smartphone does not compare to the same feeling as sitting at a real table. Land-based casinos will never be completely replaced, but I would not be surprised if their attendance declines in the coming decades.

Competition from similar companies

In addition to land-based casinos, Evolution must also compete with companies with a similar business model. The industry in which it operates provides huge profit margins, and as a result more and more companies are enticed to invest in it. Anyway, at least for the time being, its dominance is overwhelming.

Evolution holds 80 percent of the live software market share and for the 12th consecutive year won the live casino supplier of the year award at EGR. The remaining 20 percent is divided mainly among Microgaming, Playtech ( PYTCF ), ITG and other smaller companies.

The latter are all good companies , but they fail to compete in terms of innovation and efficiency. In fact, it has been about a decade since their importance has been downsized. Yet, it is curious to note that they were the pioneers of the online casino having all been established about a decade before Evolution. So, what led to such a rapid ascent by the Swedish company? In my opinion, there are two factors to consider: differentiation and constant acquisitions.

Differentiation

Unlike its competitors, Evolution's live casino games are not created to make the bettor lose as much money as possible in a short time, but to entertain him or her for as long as possible. In fact, many of its games have a high RTP and are customized to the smallest detail in order to intrigue the user. The presenters are intentionally very welcoming and have conversations directly with the bettor.

No doubt there are people who lose a lot of money, but the primary goal remains to keep the user unknowingly attached to his or her smartphone. If the bettor loses almost everything right away, he or she will have a negative memory and may never participate in that live show again; whereas if the losses are minimal and occur between laughs, the defeat is less bitter.

To best make the point, I attach CPO Todd Haushalter's comment on one of the world's most entertaining games, Crazy Time :

The goal was to make a game that is so entertaining that people would enjoy just watching it as they would a game show on television. To achieve this, we knew we needed lots of variety and to make the players the contestants on the show. The variety comes in the form of copious bonus rounds that bring the players into different side games, all of which are distinctively different and entertaining in their own right. We know this game will appeal to slot players and we wanted to really entertain them, and to do that we packed each game round with lots of action, also making it longer than a typical slot-round. We feel players get great entertainment value with each bet in this game.

This is some of the best work Evolution has ever done and I honestly believe it is the most fun casino game ever made. It highlights a paradigm shift for Evolution: this game will appeal to audiences far and wide, from slot players to sports bettors and everyone in between. There is truly nothing like it.

Crazy Time was released in 2020, and 3 years later it has spread rapidly even among those who were not used to gambling: the management's goal has been met in full. Personally, I recently played it to see how much truth there was in these words, and indeed the addictiveness of this game is disarming. It seemed to me that the disappointment of losing money was offset by the entertainment generated by the presenters and the bettors themselves commenting in the lobby.

In general, Evolution's live shows are objectively the best around, and the numerous prizes won are proof of that. As we shall see, the financial results are also on its side. Finally, I would like to conclude this paragraph with a more in-depth look at CPO Todd Haushalter.

Overall, I believe that all of Evolution's management is top notch, but it is probably Todd Haushalter's creative streak that has set this company apart from the competition. His vision toward live casinos has always been very forward-looking, and for that reason I think he is Evolution's value-add, and therefore the worst enemy for the competition. Regarding the future of live casinos, this was his answer that impressed me the most:

It is going to be highly entertaining games that are almost like TV shows that you can gamble along with at home. We think of Netflix, YouTube and video games as our competition, so we are bringing games that are equally entertaining.

Basically, companies like Playtech and ITG technically are not even to be considered as competitors, as their degree of entertainment is not comparable. These are strong words, but they denote an outsized personality. If his vision were to be realized, Evolution's growth would still be in its earliest days, and competition is an incentive to improve faster.

My view on competition is that it's good to have competition. It makes you run faster.

Acquisitions and willingness to expand

The second factor that has helped Evolution's growth has been the continuous acquisitions made in recent years. By acquiring its competitors, management is incorporating all the most innovative technologies within the company to dominate the market. Major acquisitions as of 2020 include Big Time Gaming , DigiWheel , NetEnt , and Nolimit City .

Most acquisitions feature a mixed payment structure between cash and issuance of new shares, but to date dilution is not an issue.

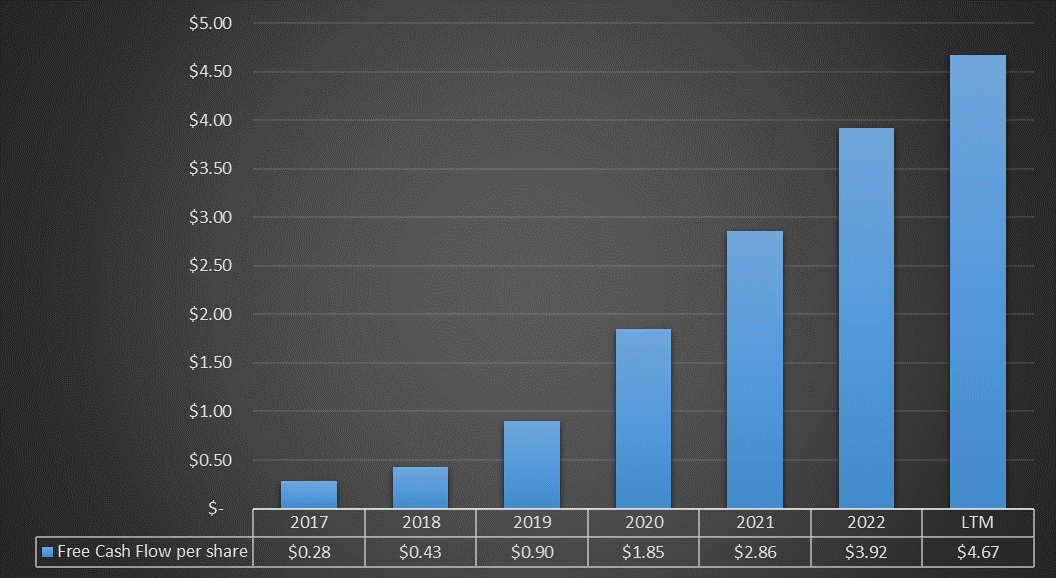

Chart based on Seeking Alpha data

{kind=link}

From 2017 to the present, free cash flow per share has increased significantly every single year, a sign that the acquisitions made are paying off. After all, each acquisition has been targeted to grow Evolution's ecosystem.

Continued acquisitions, combined with the innovative games being released each year, are increasingly crushing the competition.

As the leading innovator in the industry of online casino, together with a record number of new products released every year, we will continue to relentlessly increase the gap to our competitors. Evolution has a great speed forward, and I can promise you that we will continue to push boundaries as paranoid as ever and also for the coming period.

With a behemoth growing so rapidly and prone to buying up its rivals, it will be increasingly difficult for new entrants to compete.

Favorable position toward customers

So far I have emphasized aspects related to competitive advantage toward direct competitors; in this section I will instead discuss the relationship with customers.

As already anticipated, Evolution generally earns a commission between 10%-20% on gaming operators' earnings. So, not everyone pays equally and this is because Evolution's bargaining power ensures price discrimination. In my opinion, the reasons why a gaming operator decides to pay even a higher-than-average commission stem mainly from two aspects:

- The first is that if it wants to attract more bettors it must necessarily be licensed for the most popular games of the day. Under current market conditions, Evolution is the company that provides the most entertaining live shows. Therefore, especially if we are talking about a small game operator, it is almost mandatory to pay a higher commission in order to increase in popularity.

- The second is that Evolution is synonymous with safety. Consider that this company operates in an industry where scams are commonplace, and there are multiple security measures that must be taken to ensure that the live show is not rigged. It is not easy in this market to gain trust. Think about what could happen to a gaming operator if it became known that the live shows it offers are rigged: at best it would close down the next day. There is a lot of responsibility on the managers of these companies, and relying on Evolution is a safe solution.

Safety and potential earnings from the trendiest live shows of the moment are the reasons for a gaming operator to rely on Evolution, beyond whether the commission is 10 percent or 20 percent. When a company has bargaining power it is visible especially in the financial results, as the profit margins are high. In fact, this is the case with Evolution.

Financial results and future prospects

So far we have seen mainly the qualitative aspects of Evolution, now I will highlight the quantitative ones. As discussed, the competitive advantage of this company is significant; in fact, its financial results are very positive.

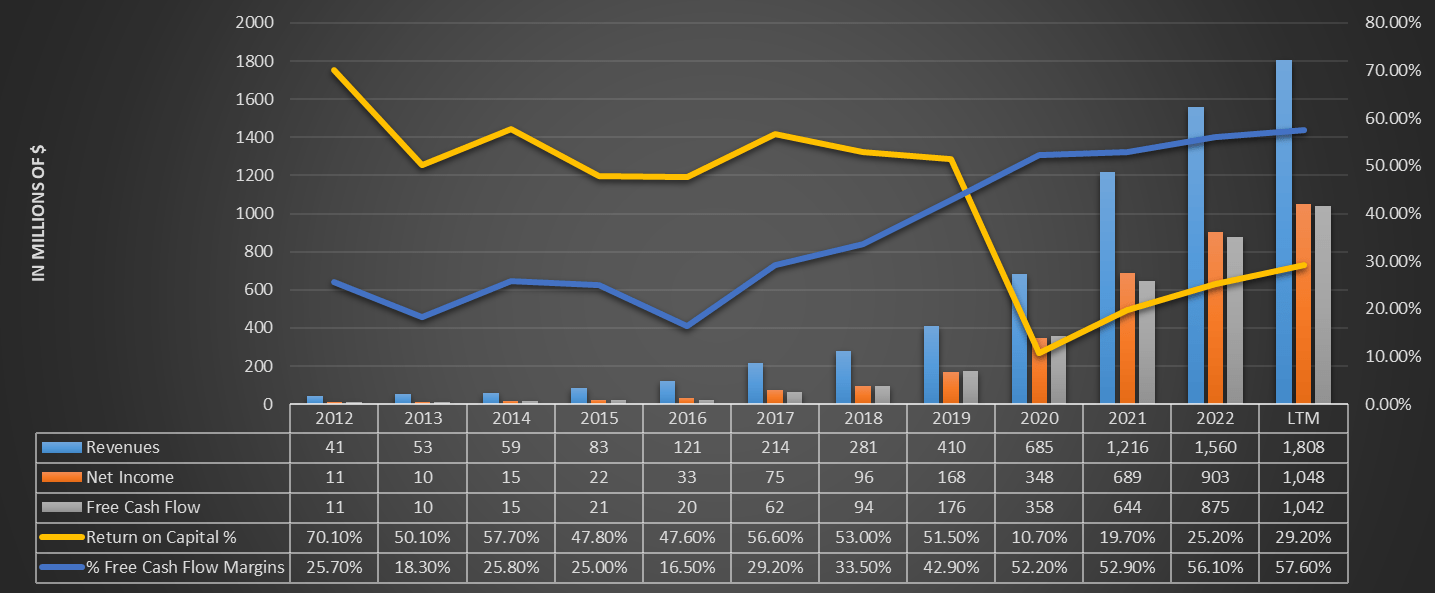

Chart based on Seeking Alpha data

{kind=link}

Since 2012, revenue growth has been sensational and today revenues total $1.80 billion. What is most surprising, however, is the free cash flow margin: 57.60% and constantly improving due to the scalability of the business. Earning $57.60 in free cash flow for every $100 in revenue is something few in the world can achieve. This explains how the company constantly makes acquisitions: it always has a large amount of cash on hand. In addition, the return on capital well above 25% and the absence of debt should not be overlooked.

Overall, we are talking about a company that from a financial point of view is objectively very solid. Personally, it reflects all my investment criteria:

- High return on capital and high profit margins.

- Growing revenues and free cash flow.

- Negative net debt.

- Significant competitive advantage.

Anyway, these considerations are based on Evolution's past; let us now see what the future prospects are.

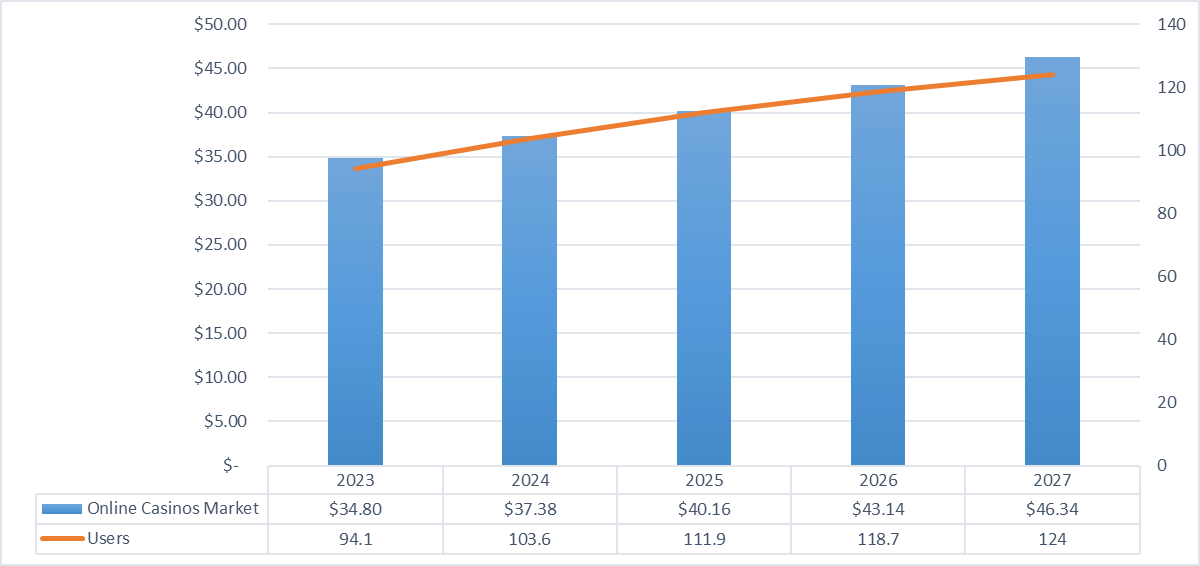

{kind=link}

Revenues in the online casino market are expected to reach $34.80 billion in 2023 and grow at a CAGR of 7.42% through 2027. At that point, revenues in this market would amount to $46.34 billion and users would be 30 million more than in 2023.

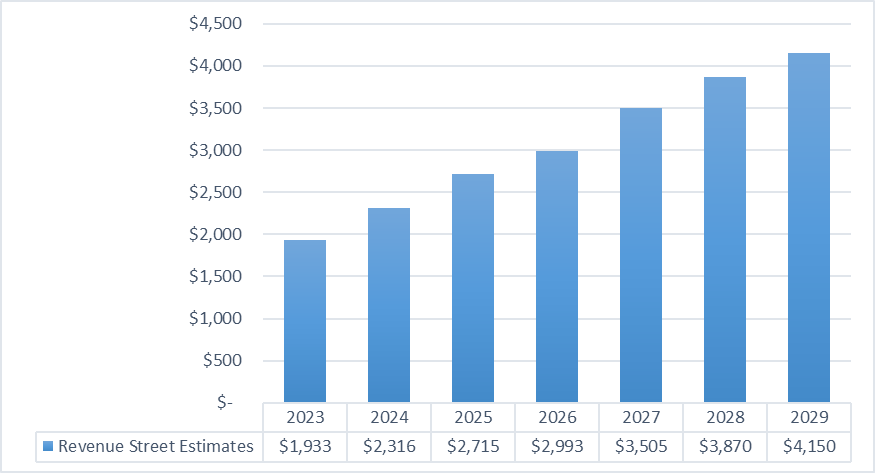

{kind=link}

Narrowing the field to Evolution alone, street estimates on revenues predict a CAGR of 16 percent, more than double the reference market. If these estimates turn out to be correct, Evolution in the coming years would continue to gain an increasingly large market share, just as it has over the past decade.

Personally, I consider this scenario realistic, however, it is reasonable to expect that growth may gradually slow down. After all, 2018-2023 revenues have grown at a CAGR of 49% and this is not sustainable over the long term.

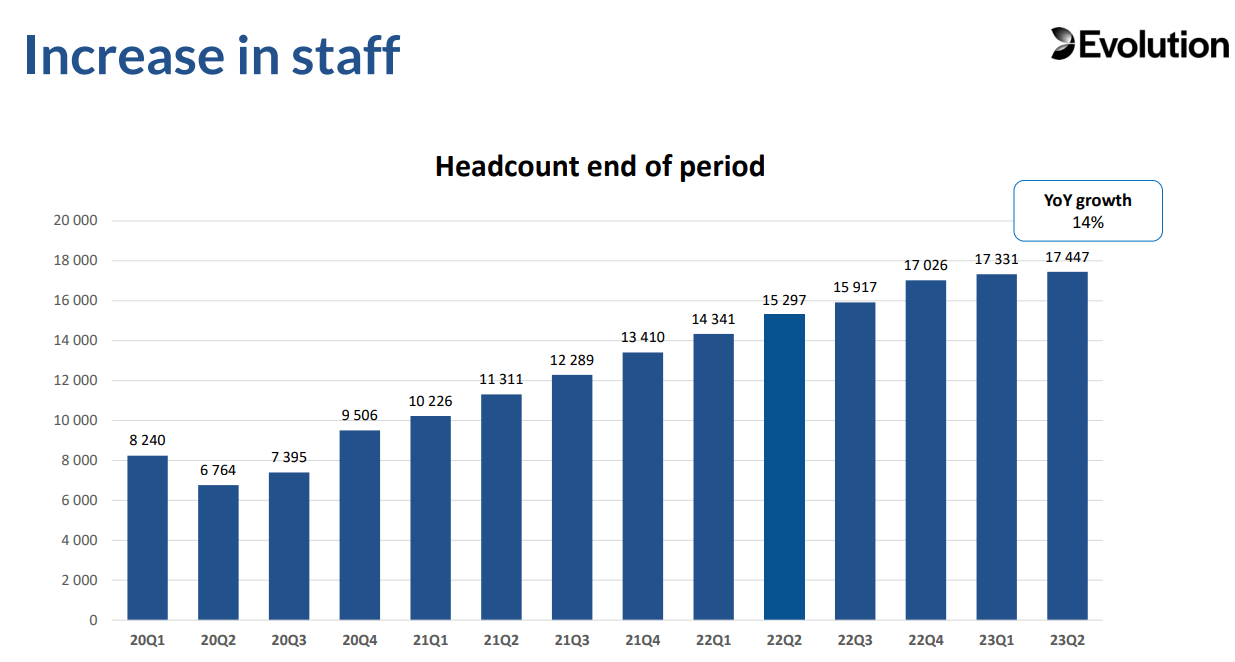

Finally, Evolution is already laying the foundation for a new cycle of prosperity and there is no shortage of new hires.

{kind=link}

While major tech companies have laid off thousands of employees, Evolution is increasing staff quarter after quarter.

Valuation

To consider Evolution a simple growth company is reductive because it has several characteristics that make it value at the same time:

- The first is the issuance of sustainable and growing dividends just like the leading U.S. consumer staples. Also, as innovative as it is, its business model remains quite traditional and predictable.

- The second is that Evolution is trading below its fair value.

Let us look at these two aspects in detail.

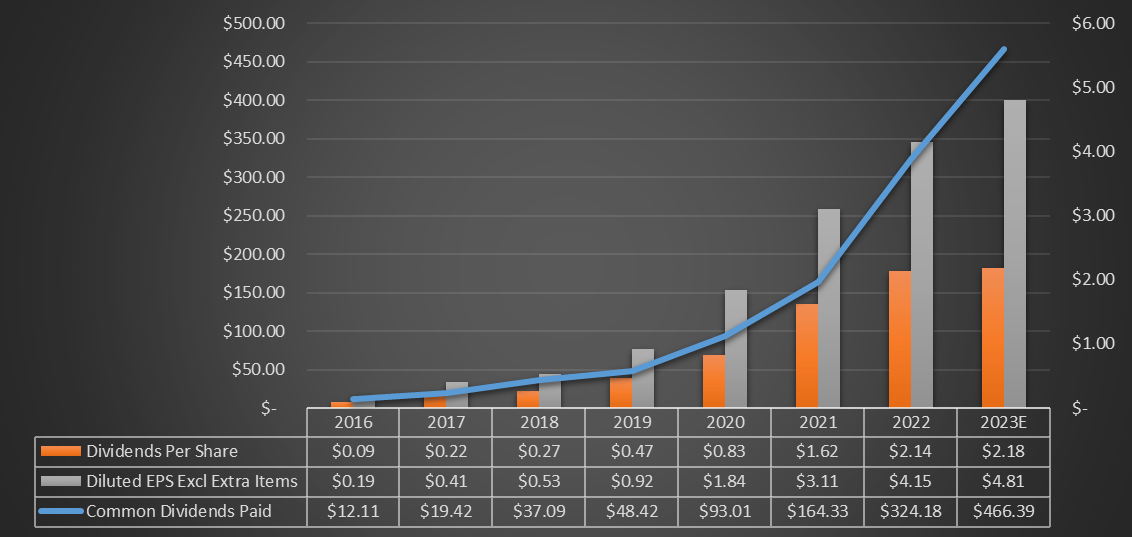

Dividend analysis

Evolution is very focused on dividends, in fact the Board has adopted a dividend policy under which the company will distribute a minimum dividend equal to 50 percent of net income each year. This means that if earnings growth continues to be impressive, the dividend issued will increase significantly.

Chart based on Seeking Alpha data

{kind=link}

Evolution's strong growth has virtually skyrocketed the dividend in recent years: it has nearly tripled in about three years. If the growth estimates seen above turn out to be correct, Evolution's shareholders in a few years could earn a rather high dividend yield.

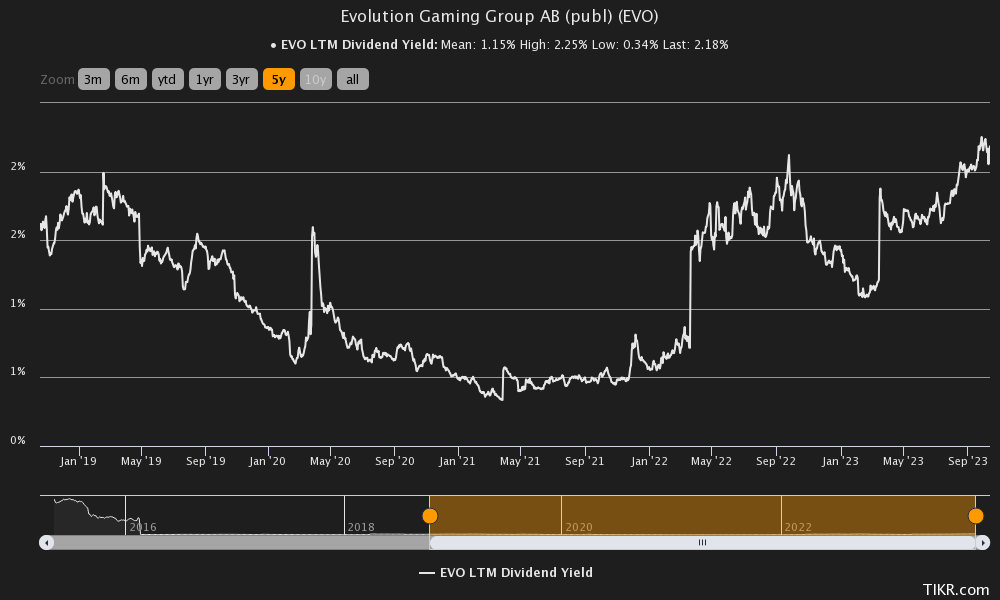

{kind=link}

For those who bought this company 5 years ago, today the yield on cost would already be 16.74% since the dividend CAGR was 85.95%. Certainly dividends will slow their growth in the future, but if we considered a CAGR of 15% for the next 5 years, it would mean a yield on cost of 4.50% before double taxation. This seems like a reasonable scenario.

{kind=link}

Finally, based on the current dividend yield, today seems to be one of the best times to buy this company. Only on two previous occasions this ratio has exceeded 2% in the past 5 years.

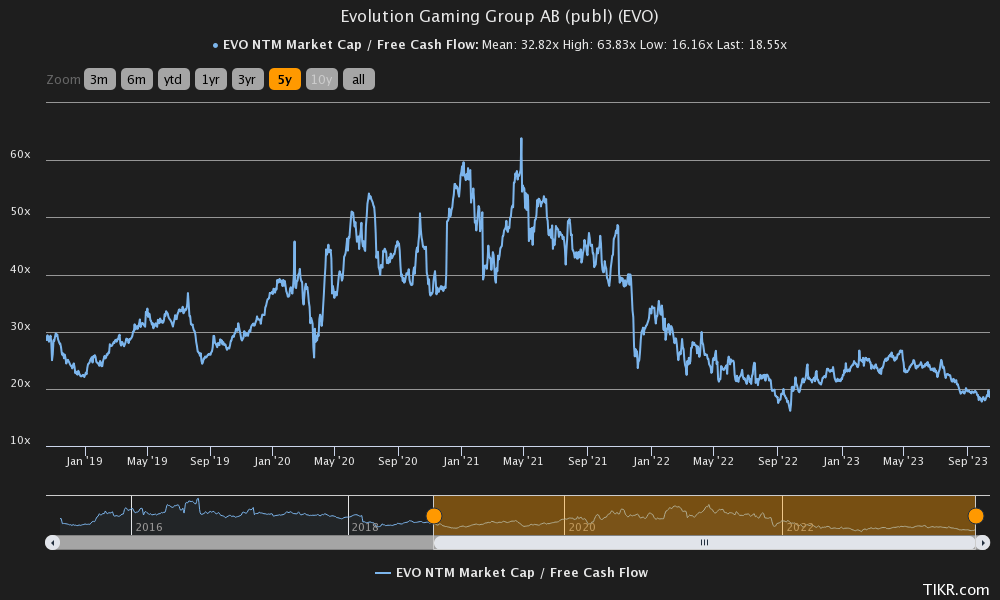

Multiples and fair value

As well as the dividend yield, the other valuation multiples also signal an undervaluation.

{kind=link}

The current NTM Market Cap/ Free Cash Flow is only 18.55x, too little for a company with such growth potential and such a competitive advantage. What's more, the average of the last 5 years is almost double the current figure. From this perspective Evolution seems undervalued, but by how much? To understand this we need a discounted cash flow model. To make the fair value more conservative, I wanted to divide the model into three scenarios each with its respective weight:

- Best-case scenario, where street estimates of free cash flow 2023-2027 will be discounted in full. Its weight is 40%.

- Normal-case scenario, where street estimates discount a 10% deterioration. Its weight will be 40%.

- Worst-case scenario, where street estimates discount a worsening of 30%. Its weight will be 20%.

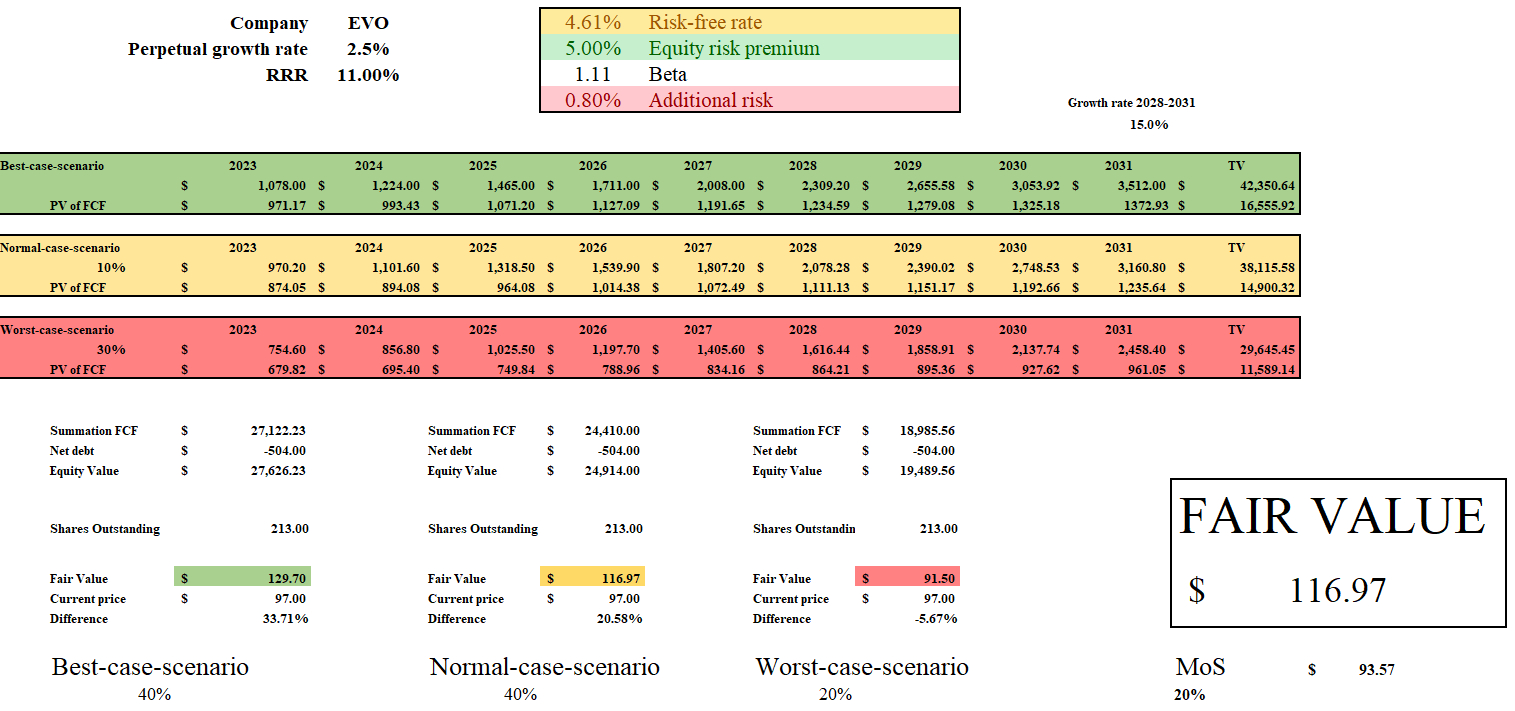

In addition, this model has the following inputs:

- Discount rate of 11% calculated through the CAPM formula. The values to calculate the latter can be seen in the picture below.

- 2028-2031 growth rate of 15%; perpetual growth rate of 2.50%.

{kind=link}

Based on these assumptions, Evolution's fair value is $116.97 per share, so at the current price it looks undervalued. Also, interestingly, the current $97 per share is close to the fair value obtained in the worst-case scenario, which is $91.50 per share. As a reminder, the worst-case scenario discounts growth prospects reduced by 30 percent from current estimates; in other words, Evolution is trading almost as if it is discounting this dire scenario.

Overall, by buying the company now, I think there is a good chance to get at least an 11 percent return per year.

Risks

Although Evolution objectively appears to be a solid and interesting company, it still has a number of risks. No investment is without them, and for this company I have identified mainly three.

- Being a sin stock, the first undoubtedly concerns regulatory risk. Only 40 percent of revenues come from regulated markets, and we do not know how regulations regarding gambling will evolve in the future. There could be restrictions such as, for example, a maximum amount you can play, or a maximum number of times you can participate in Evolution live shows. After all, we know how harmful gambling is, and no government would wish for it to spread. In any case, banning betting would only fuel the organized underworld, so it is unlikely that there will be any drastic change in the future. This is a very similar situation to the tobacco market.

- The second risk concerns competition. Previously, we have seen how in just a few years Evolution has downsized its rivals, but in the future this could change. After all, Evolution's competitive advantage is not about technology that is too advanced to be replicated, but about the know-how and inventiveness of its employees. If important figures such as Todd Haushalter left the company, it would be quite a problem. It is unlikely to happen, but there is no certainty.

- The third risk is always about competition, particularly the inability to innovate due to a stringent dividend policy. As noted earlier, 50 percent of profits must be distributed to shareholders, which means that the company gives up half of its available funds each time. That 50 percent could have been invested since Evolution's high return on capital, instead it is given away to meet the short-term needs of shareholders. As far as I am concerned, I prefer a young, high-growth company to reinvest everything in the business in order to increase the gap with the competition, but the Board is not of the same mind. So far the high payout ratio has not affected growth but in the future it might.

Conclusion

Evolution is a young, fast-growing company with some of the highest profit margins in the world. The outlook for growth in the online casino market is positive, and according to street estimates Evolution will continue to increase its market share. Its competitive advantage has been achieved through a different approach than its competitors, which denotes personality and foresight from management.

Since its fair value is $117 per share, at the current price Evolution is in my opinion a buy. For such a company, I would have been willing to pay a premium, but at the current price there is even a discount. It is not a given that Evolution will remain at $97 per share for much longer, which is why I have recently invested in it. If the price continues to fall, I am ready to increase the position.

Editor's Note : This article was submitted as part of Seeking Alpha's Best Value Idea investment competition , which runs through October 25. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Evolution AB: An Unknown Gem Dominating The Live Casino Solutions Market