EVGGF - Evolution AB: Still A Strong Buy Looks Like A Bargain

2023-12-27 11:26:26 ET

Summary

- EVO surged 20% since my recent article, but I still believe it is a Strong Buy.

- I believe that in a conservative case, it is undervalued by 24%, and in an optimistic case, by 47%.

- The bad news from last quarter was the struggle to keep up with demand, which is the best kind of bad news.

- The company bought back almost 1 million shares only in December.

The thesis is still in place

Back in October, I published an article delving into Evo's ( EVVTY ) business, attempting to understand what makes this amazingly profitable business tick. I rated it a strong buy. Since then, there has been a market rally, and the stock surged by 20%. Additionally, Evo reported Q3 earnings. The thesis is still intact, and I believe Evo is massively undervalued.

I wanted to create an updated article because I believe my last one is outdated for investors who want to stay informed about the company. The 20% surge has altered the company's valuation, and there have been earnings, new buybacks in December, and the launch of the 'Crazy Time' in the US.

Q3

The Q3 results were released two weeks after my last article, on October 26th. So, the top-line growth for Evo was at 19.6%, which is a good number by itself but would be higher if the management kept up the investment pace into new studios and personnel. The CEO noted that demand was high, and they weren't keeping up with the pace.

That is a measure of the phenomenal traction our games have. However, it also means we are not expanding our studios at the right pace. We have faced delays, and in some cases not executed fully, in several of our planned studio projects for this year but even more importantly we need to increase the pace of recruitment both in existing studios as well as to support new studios. We are working hard to get back on track in our existing locations and we will continue to invest in our network of studios and add new locations.

I take three main points out of this event. The first is that demand is high, and that is always a good sign, especially in a tougher economic environment. The high demand that the company struggles to catch up to is the best kind of bad news.

The second important point I take from it is that management is willing to admit its mistakes openly and to note straightforwardly what happened. I appreciated this integrity.

The third point I worry about is whether management is willing to give up growth for better margins. Nevertheless, the CEO noted the ramp-up in investment in studios and personnel to catch up with demand.

Another piece of good news I see is that, apart from the fast-growing markets—Latin America and Asia, both experiencing up to 30% growth rates—growth in more mature markets, such as Europe, was also solid at 10% YoY. This indicates that the investment in new games, over 100 in 2023, is attracting customers. Regarding market share in those areas, the CEO was asked in the earnings call about market share expansion but did not give a clear answer. Also, it is challenging when competitors are private.

Growth in North America was 9%, but that's before the anticipated 'Crazy Time' December launch , the most popular Evo game worldwide has been released, and in my view, this could be a great catalyst to boost growth in the market. This is crucial, considering North America is a huge market, and Evo needs to leverage every opportunity it presents.

North America is a region that we expect to develop over many years as more US states regulate.

The RNG segment continues to deteriorate, and I start to wonder if this section is worth the R&D expenses on new games—24 new games in Q3. In the RNG world, Evo does not have an edge or a moat because barriers to scale are low, in contrast to the live games segment. However, it is important to note that the RNG segment is profitable.

Important Numbers

EBITDA margins topped 70%, which is outstanding. The management guidance is between 68% to 70%, with 70% more likely moving forward. Based on the 63% EBIT margin, Evo has a 27% ROCE, as opposed to a WACC of around 9%. This is another important figure, as high ROCE numbers are one of the main factors, besides revenue growth, for long-term company success. A recent study by Michael Mauboussin indicated that a high spread between ROIC and the WACC of a business is a common trait among winners.

Because of the low capital expenditure investments into studios, the free cash flow margin was 70%, I repeat, 70%. These are amazing numbers. However, I will not base my valuation upon these numbers, as both the tax rate, which will more than double next year, and also the ramp-up in investing into studios and personnel will probably erode margins.

From the balance sheet perspective, the cash pile grew to more than $800 million, and the company bought back almost 1 million shares only in December, reducing the share count by around 0.5%. This is in addition to the already high dividend payout ratio the company maintains. These buybacks are also an indication that management might believe the company is undervalued.

Ali Gunduz, who has a great newsletter mainly about Evo, introduced the possibility of a goodwill write-down:

The generous purchase considerations of the RNG studios created massive amounts of goodwill in Evolution’s balance sheet. By last quarter, that goodwill amounted to over 2.2 billion euros, an amount that is greater than all FCF that Evolution has earned in the last 3 years.

So, at the risk of repeating myself, Evolution - a growing and profitable company that is trading at around less than 18 times LTM earnings at the time of this writing - is holding a plug asset that is valued by acquisitions made at 46 times earnings and actually makes up the declining segment of the company. I think it is not unreasonable to expect a goodwill write-down at some point.

In such a case, both earnings per share and shareholders' equity might be reduced, impacting the EPS numbers that analysts forecast and investors closely track. This could pose a setback to the stellar growth Evo is achieving. However, in my view, the potential impact of such a case is insignificant due to the future robust cash flows that Evo is expected to generate. In my perspective, that's where the majority of the business value comes from.

So Far

So far, so good. In my view, the long-term thesis is intact. The numbers are at their highs, demand is strong, and the management has plans on how to capitalize on it, ensuring robust growth. I appreciate the management's integrity, and such a situation fosters trust, which is crucial where money is involved. Besides the elevated evaluation that increased the risk of purchases, the long-term compounding traits of Evo are further strengthened by the higher demand.

Valuation

If we assume a 55% Free Cash Flow margin to compensate for the tax rate expansion and the ramp-up in investments, we get a 4.2% FCF yield, which, in my view, is a pretty reasonable price—perhaps even a cheap price for a company with a top-line growth of 20%. Additionally, 23 times earnings multiple for up to 20% earnings growth gives us a PEG ratio of around 1, which is low for a high ROCE company. This is also Peter Lynch's favorite valuation multiple.

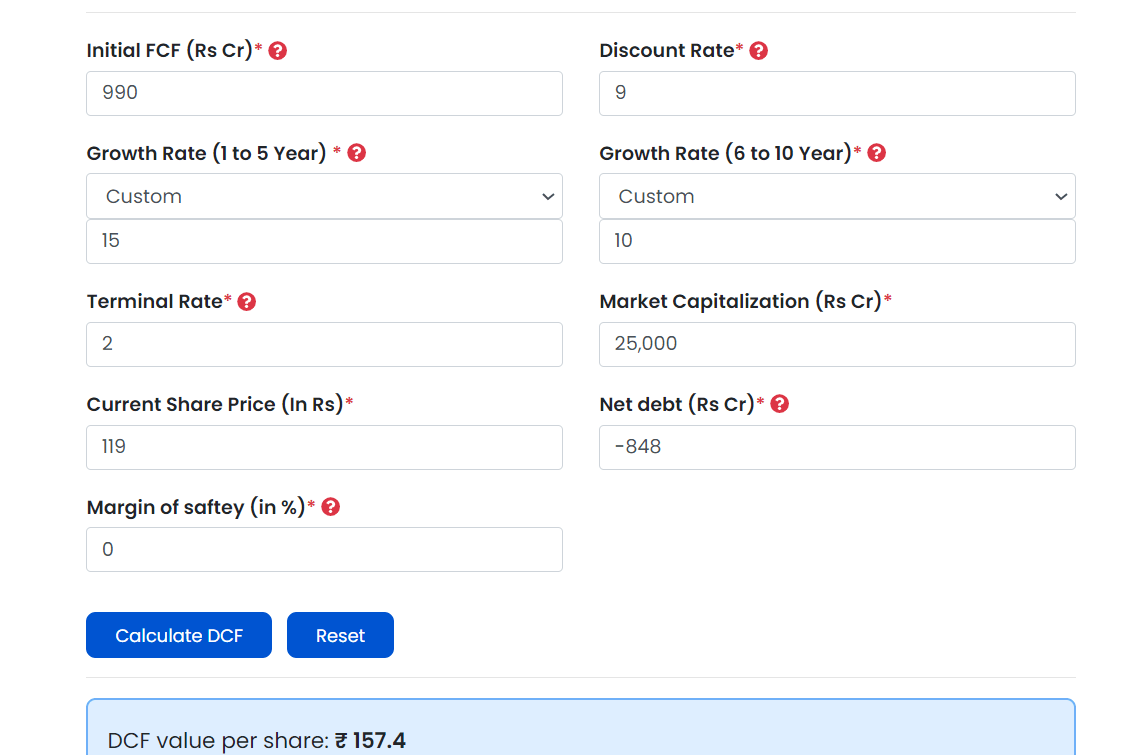

In terms of the Discounted Cash Flow, I'll be conservative. Assuming a 50% FCF margin, with full-year top-line estimates of $1.9 billion, we get just under $1 billion in FCF. The terminal growth is set at 2%, and the WACC is 9%. I'll be more conservative with the growth rates, assuming a 15% FCF growth in the first 5 years and a 10% growth for the 5 after. With such conservative assumptions, we get an undervalued stock by 24%.

WACC (author)

{kind=link}

DCF (finology)

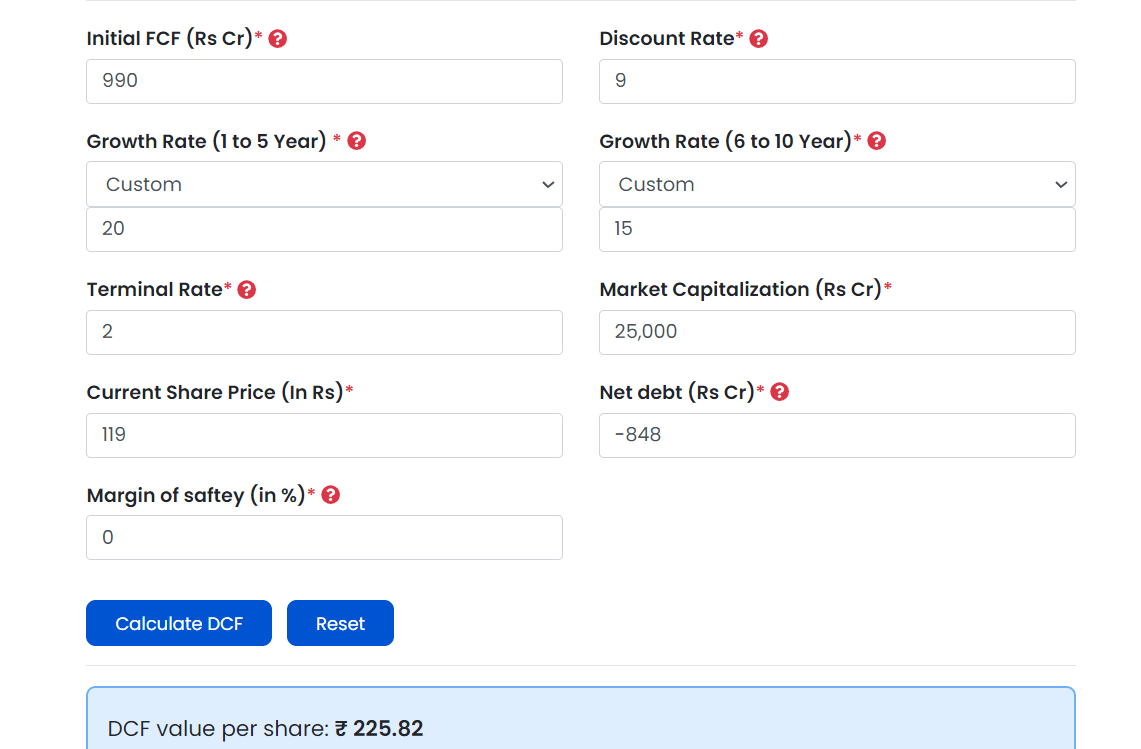

Now, let's input more optimistic assumptions. Assuming the same 50% margin but with a 20% growth rate for the first 5 years and then 15% for the 5 after, we get an undervalued stock by 47%.

{kind=link}

DCF (finology)

In my view, this is an outstanding valuation for a high ROCE growing business.

As opposed to the valuation in my last article (the intrinsic value was $142, based on very conservative estimates), I believe my free cash flow numbers are more accurate today, considering the included tax rate increase and capex surge. Additionally, my WACC is now more precise. Of course, the price has surged by 20%, making it riskier today than it was two months ago.

Also, in my view, a good valuation metric is the difference from the mean. Evo's multiple is low compared to its 5- and 3-year means, suggesting a potential for multiple expansion on top of earnings growth. This is a metric I like to use, and the combination of returning to the mean plus a robust discounted cash flow analysis provides a potentially accurate assessment.

Conclusions and Risks

Evo has lagged behind the S&P year-to-date, with only a 22% return compared to the S&P's 24%. This makes the opportunity looking forward more favorable, as I believe sectors that underperformed will likely perform better in the near term due to lower prices and the potential QE from the Fed in 2024.

The management noted currency risks as a major concern. This risk could meaningfully affect FCF looking forward; however, Evo does not have much control over such cases.

Another risk is rising competition, of course. Such margins attract a lot of competition, but those margins are not new, and it seems like Evo is achieving success in handling such competitors.

Yet another risk I see is the struggle to catch up with demand. This aspect could hurt the real growth Evo can achieve.

I will primarily monitor the thesis through the growth rates in mature markets and stay informed about any news regarding new regulations. If growth falls below the 15% threshold, then I will become concerned. Looking ahead, I am pleased with the management's commitment not to sacrifice growth for margins, and I anticipate that supply will catch up with demand, given the plans in place for new studios.

Regarding the risk/reward case, I still think Evo is an outstanding business and a potential multi-bagger long term. The potential for multiple expansion with organic business growth is a huge driver for value creation.

Therefore, I maintain my rating of STRONG BUY.

What is your view about Evo?

For further details see:

Evolution AB: Still A Strong Buy, Looks Like A Bargain