CAHPF - Evolution Mining: A Busy Quarter With A Stronger H2 On Deck

2024-01-05 00:21:16 ET

Summary

- Evolution Mining's fiscal Q1 results showed a decline in gold production, but we should see better grades and much higher production in Q2 through Q4.

- The company acquired 80% of the Northparkes Mine, adding a lower-cost copper-gold asset to its portfolio, albeit at the expense of further share dilution.

- In this update, we'll dig into Evolution's fiscal Q1 results, recent developments, and whether it's worth paying up for the stock at current levels.

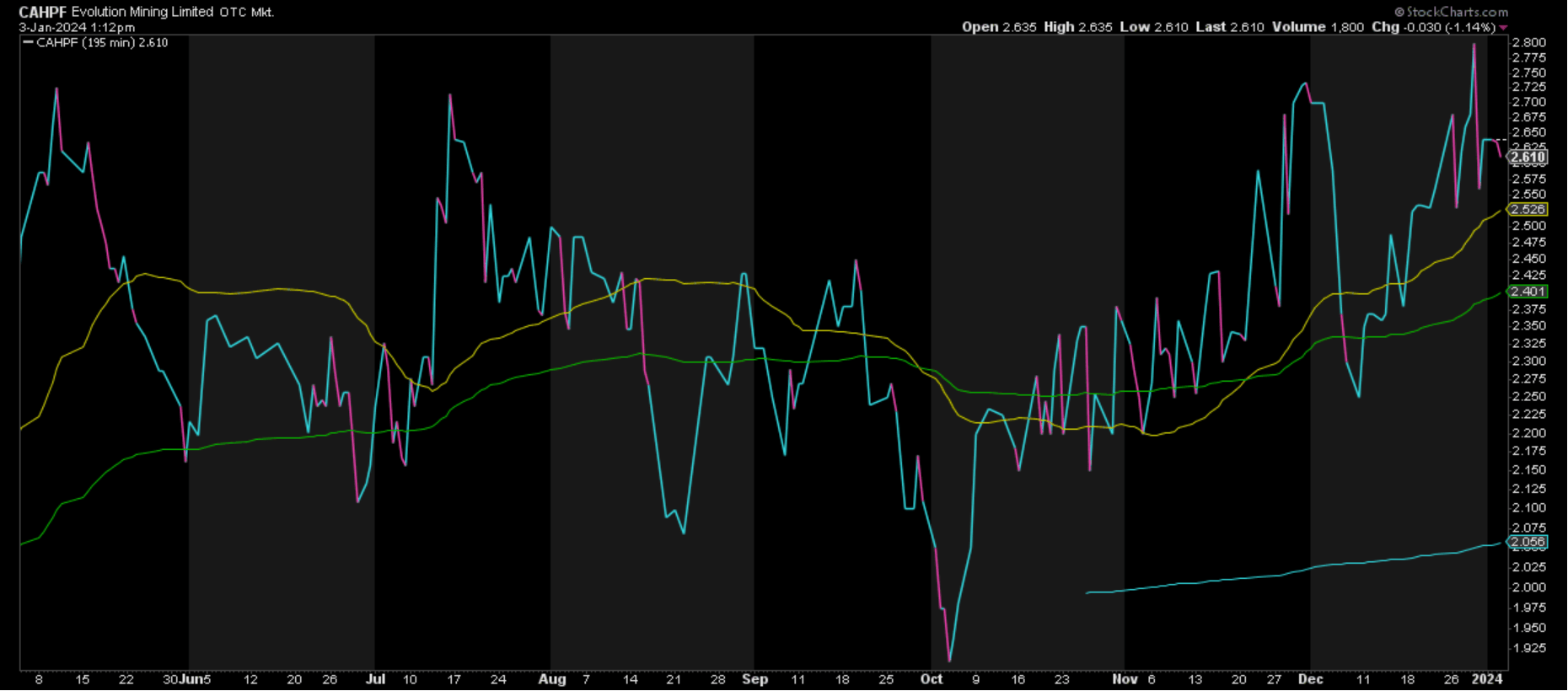

Just over four months ago, I wrote on Evolution Mining (CAHPF), noting that with the stock continuing to trade at a premium valuation relative to its peers, I expected any rallies above US$2.75 to provide an opportunity to book some profits. Since breaching this level in November and again in December, the stock has run into stiff resistance in what was a busy fiscal Q1 for the company following a major acquisition (80% of Northparkes) and a concurrent equity raise (~US$340 million). On a positive note, we should see a much better H2 following softer results in fiscal Q1, with better grades from Red Lake, additional contribution from Northparkes, and a further ramp-up in production from Cowal with the paste plant commissioning. In this update we'll dig into Evolution's fiscal Q1 results, recent developments, and whether it's worth paying up for the stock at current levels.

{kind=link}

All figures are in United States dollars unless otherwise noted at a 0.65 AUD/USD exchange rate.

Q3 Production & Sales

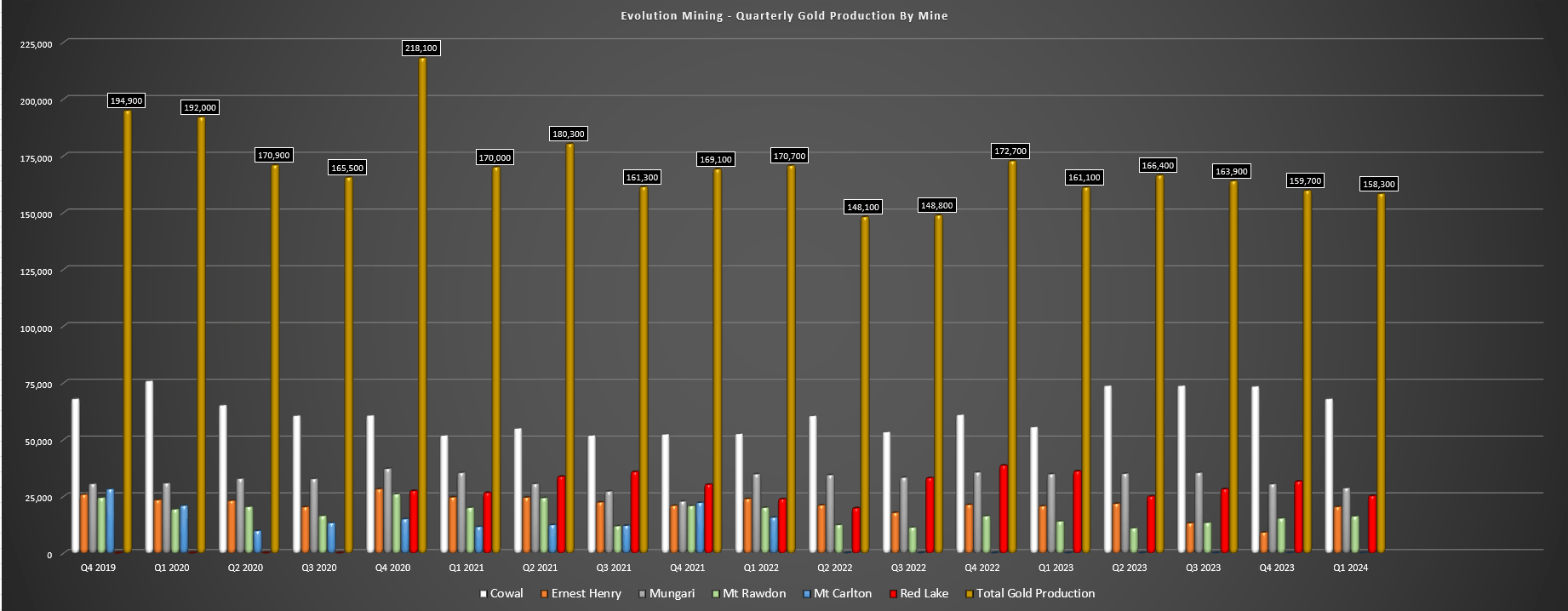

Evolution Mining ("Evolution") released its fiscal Q1 2024 results in November, reporting quarterly production of ~158,300 ounces of gold, a 2% decline from the year-ago period. The lower production can be attributed to a much softer quarter at Red Lake (-30% year-over-year), and lower production at Mungari (-17% year-over-year), offset by a better quarter at Mt Rawdon (+15% year-over-year), roughly flat production at Ernest Henry, and a significant increase in production at Cowal (+22% year-over-year) with increasing contribution from Cowal Underground. Meanwhile, although production is tracking at barely 20% of its FY2024 initial guidance midpoint (770,000 ounces), this was expected to be the softest quarter of the year due to the progressive ramp-up at Ernest Henry following the weather event that took operations offline for nearly two months in H1 2023 and planned shutdowns across the portfolio. Unfortunately, production was further impacted by ore passes at Cochenour (Red Lake) and mining restrictions related to seismicity in September.

Evolution Mining Quarterly Gold Production by Mine - Company Filings, Author's Chart

{kind=link}

Digging into the operations a little closer, Red Lake saw the most significant decline even if it did deliver into its guided range for the quarter, with production down 30% year-over-year to just ~25,200 ounces at all-in sustaining costs of A$2,552/oz. The lower production was related to fewer tonnes mined at lower grades (~194,000 tonnes at 4.57 grams per tonne of gold) and a decline in throughput to ~186,000 tonnes at 4.7 grams per tonne of gold vs. ~209,000 tonnes at 5.82 grams per tonne of gold in the year-ago period. On a positive note, Evolution completed the workforce planning and headcount reduction will allow for $12 million in annual savings, the Cochenour ore pass constraints have since been resolved, and we should see better grades reaching the mill in H2.

Moving over to Cowal, Evolution had a much better quarter year-over-year with production of ~67,900 ounces at industry-leading costs of A$1,315/oz, a significant improvement from ~55,500 ounces in the year-ago period. The sharp increase in output was driven by ~128,000 tonnes mined at 2.51 grams per tonne of gold underground, in addition to higher open-pit grades of 0.84 grams per tonne of gold. This resulted in operating cash flow of A$112.5 million in the quarter and with first paste delivered underground we should see a much better remainder of the year as the company targets full-year production of ~320,000 ounces (implying quarterly production of 84,000 ounces on average from fiscal Q2 to fiscal Q4 2024).

{kind=link}

As for Ernest Henry, the mine is back on track after a tough H2 2023 (extreme rainfall event in mid-March 2023), with production of ~20,400 ounces of gold and ~13,600 tonnes of copper at [-] A$2,275/oz all-in sustaining costs after by-product credits. This was a meaningful improvement from the year-ago period with the help of higher copper prices, and this showed up in the financial results with operating cash flow of A$110.6 million, up nearly 10% year-over-year. Finally, Evolution noted that it saw a quarterly record for development at the asset of 3,114 meters, and it mined ~1.64 million tonnes in the quarter, up from ~856,000 tonnes during the ramp-up period in fiscal Q4 2023. Since fiscal Q1, we've seen further strength in the copper price, suggesting another solid quarter for costs at Ernest Henry, and this will benefit its larger copper contribution (Northparkes 80%), which we'll dig into later.

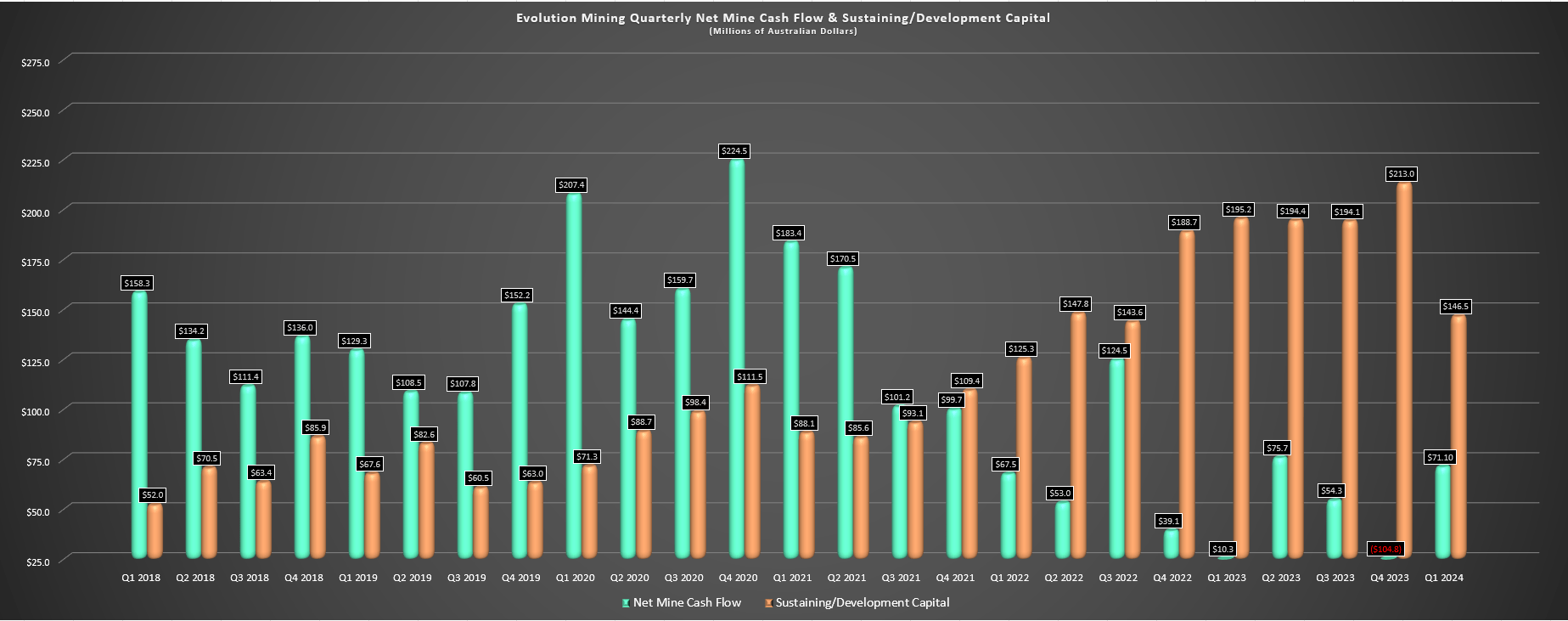

As for the fourth of Evolution's largest operations, its Mungari Mine saw lower production of ~28,700 ounces with a slower ramp-up than expected at the Paradigm Pit, which is expected to lift grades once full mining rates are reached. On a positive note, Evolution is making progress on its expansion plans (Mungari 4.2) with GR Engineering Services selected to complete its plant expansion to 4.2 million tonnes per annum, ultimately increasing production to ~200,000 ounces per annum from FY2027 to FY2032. Meanwhile, Evolution's financial performance improved with a higher realized gold price of A$2,907/oz, resulting in operating cash flow of $280.4 million, net mine cash flow of A$71.1 million, and net group cash flow of A$32.4 million, up from A$206.3 million, A$10.3 million, and [-] A$174.3 million in the year-ago period, respectively. That said, the company remains much more leveraged than its peers with nearly US$1.5 billion in net debt following the recently closed Northparkes acquisition.

Evolution Mining - Net Mine Cash Flow & Sustaining/Development Capex - Company Filings, Author's Chart

{kind=link}

Costs & Margins

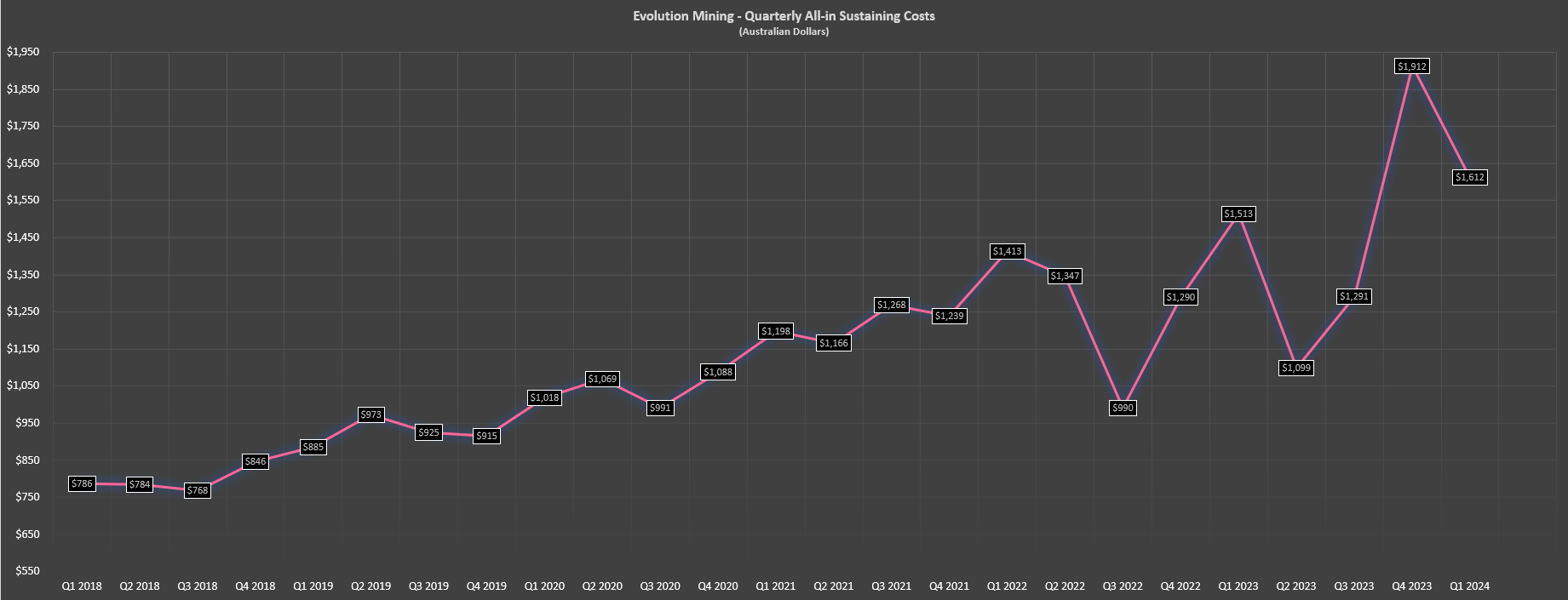

Looking at costs and margins, Evolution's all-in sustaining costs [AISC] dipped from A$1,912/oz in fiscal Q4 2023 (Ernest Henry impact), but were still up over 8% year-over-year to A$1,612/oz, and at industry-leading levels. The good news is that while sustaining capital is tracking below guidance (~17% of FY2024 guidance of A$210 million at midpoint), this will be more than made up for by higher production, and AISC margins still came in at a very respectable figure of A$1,295/oz or ~45%. Meanwhile, lower costs at Northparkes will help to pull down costs in H2 2024, suggesting that Evolution should have no issue delivering into its cost guidance of A$1,370/oz. Finally, while the labor situation hasn't improved much in prolific regions and there continues to be skill shortages, Evolution has the benefit of the gold price at its back, with the metal hovering above A$3,000/oz to start the year, suggesting better margins on a sequential basis (fiscal Q2 2024 vs. fiscal Q1 2024) and as the year progresses if this strength persists.

Evolution Mining Quarterly AISC - Company Filings, Author's Chart

{kind=link}

Recent Developments

While it was a relatively quiet Q4 for the rest of the sector outside of two smaller acquisitions by Calibre Mining ( CXBMF ) and Dundee Precious Metals ( DPMLF ), Evolution has remained busy on the M&A front with the acquisition of 80% of the Northparkes Mine in New South Wales, Australia. This marks the fourth acquisition in roughly four years for Evolution, beginning with the acquisition of the Red Lake Complex, the acquisition of Battle North, the acquisition of the remainder of Ernest Henry, and now a deal for a second copper asset in Northparkes. As for the acquisition price, Evolution paid a very reasonable price of ~$400 million up front with a contingent payment of up to $75 million, with the deal funded by ~8% share dilution at a share price of ~US$2.50, and a ~$130 million 5-year Term Debt Facility.

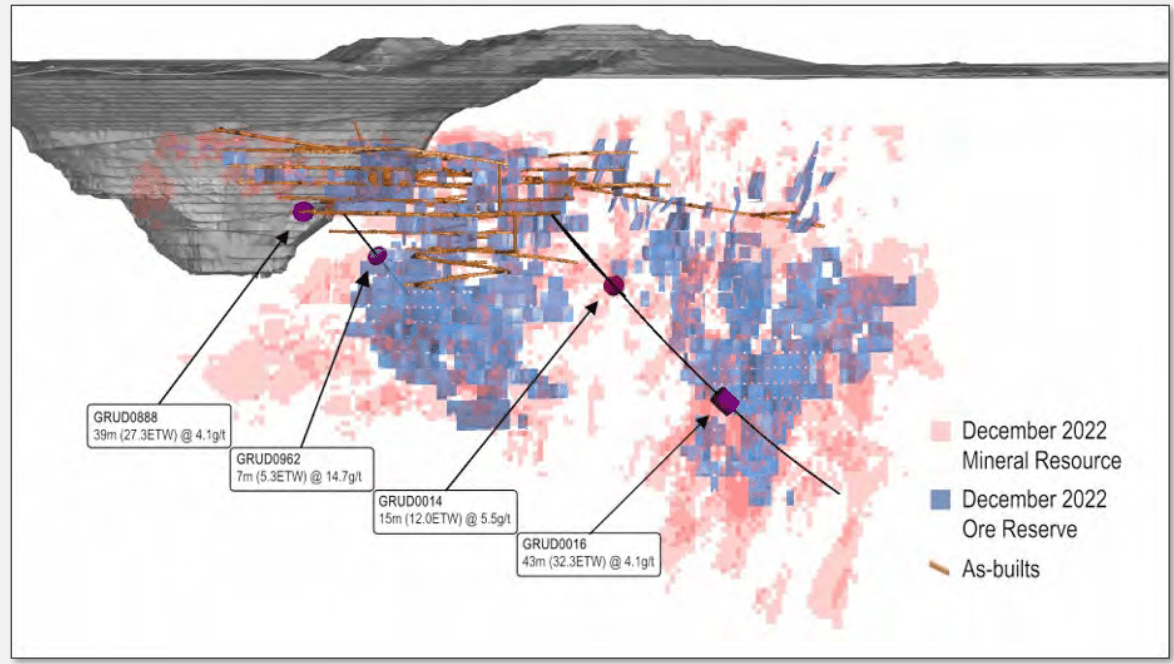

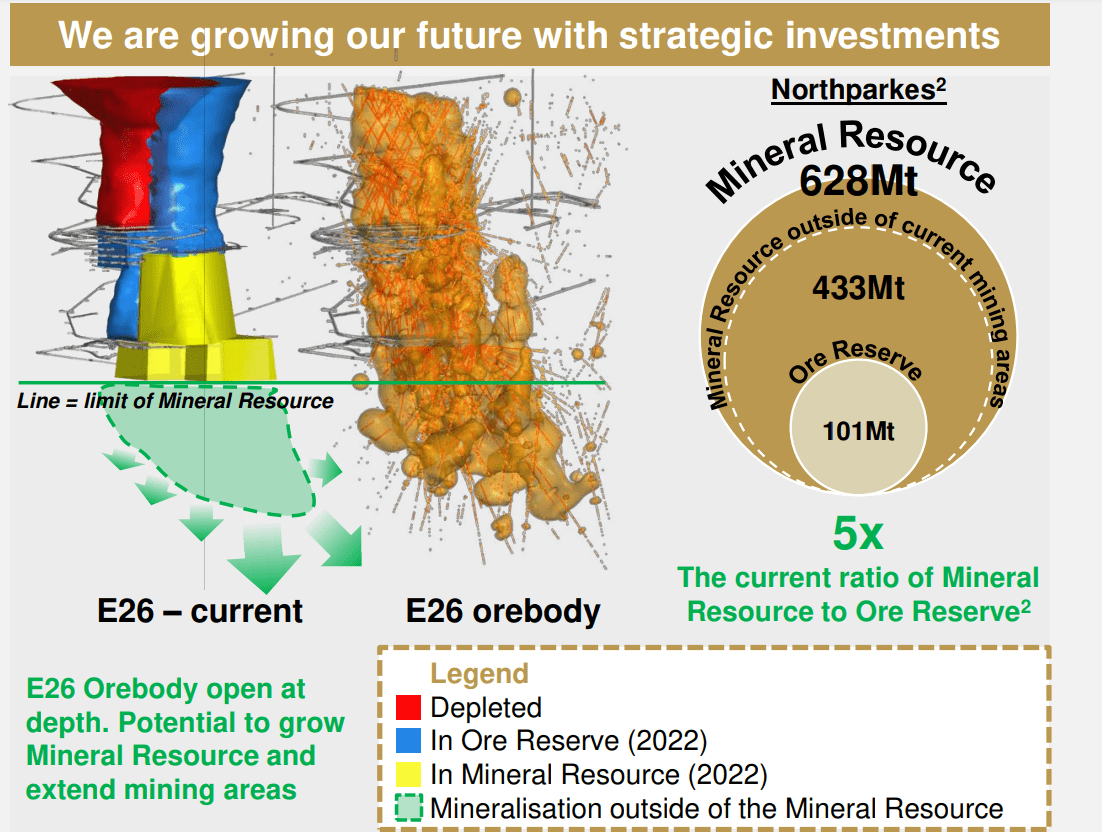

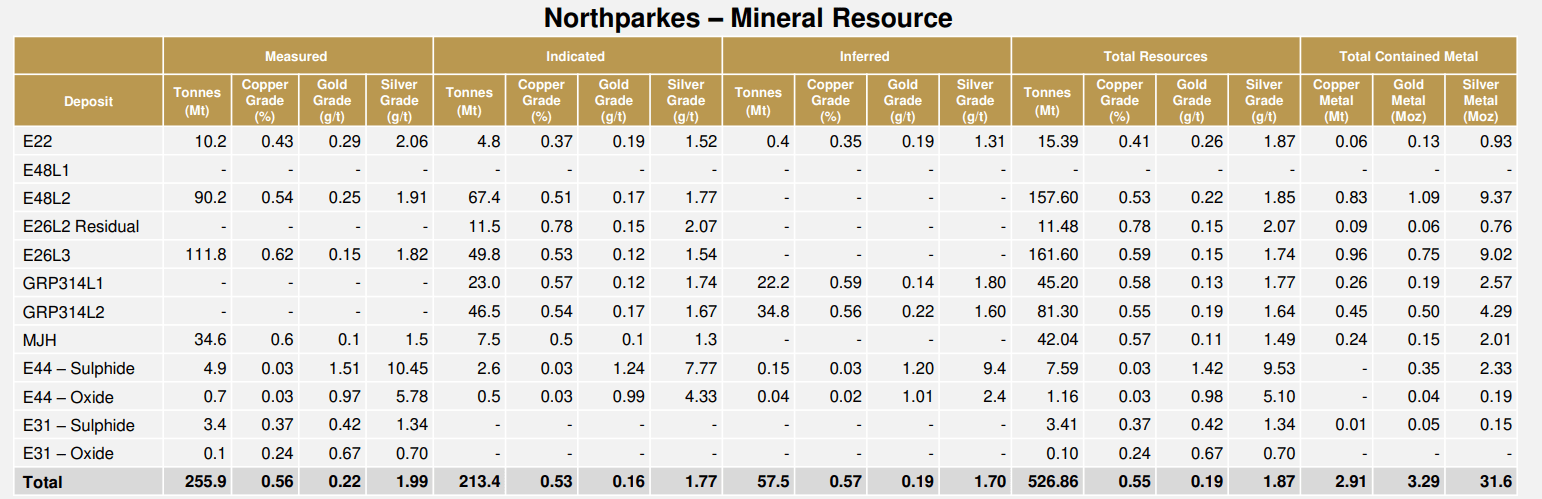

Digging into the asset, Northparkes is a large fully automated copper-gold mine previously operated by China Molybdenum that produced ~6.0 million tonnes of ore from underground last year, with record mill production of ~7.6 million tonnes. The mine is a block-caving operation with ore processed through a conventional floatation plant and Rio Tinto (RIO) previously operated it from 2000 to 2013 and the mine has been operating since 1993. Notably, the current mine life is estimated at ~30 years and the operation has a ~101 million tonne reserve base at 0.53% copper and 0.27 grams per tonne of gold, but the reserve makes up just a fraction of the much larger ~527 million tonne resource at similar grades (0.55% copper/0.19 grams per tonne of gold) or ~2.91 million tonnes of copper, ~3.3 million ounces of gold, and ~32 million ounces of silver.

Northparkes Mineral Resource/Reserves & Exploration Upside - Company Presentation

{kind=link}

{kind=link}

Unfortunately, the mine has a significant stream on the asset that was sold in 2020 comprising 54% of payable gold and 80% of payable silver for 10% of spot gold and silver prices until the delivery of 630,000 ounces of gold and 9 million ounces of silver (drops to 27%/40% of payable gold and silver, respectively thereafter). This certainly impacts the profitability of the asset vs. the full benefit of these by-products, but is still a very profitable asset because of its higher-grade open pits, sub-level caving and primarily block-caving (same mining method employed by Cadia), allowing for much lower operating costs and ability to mine relatively low-grade assets. For those unfamiliar, block caving is a highly productive bulk underground mining method that benefits from gravity and rock stress to extract ore through desired draw funnel shaped points by mining underneath the deposit by creating a void, with the unsupported area above then fracturing and caving on its own.

{kind=link}

As for the production profile and how this will benefit Evolution's overall production, FY2024 output is estimated at ~25,000 tonnes of copper and ~38,000 ounces of gold (80% basis), with the bulk of ore coming from the E26 Block Cave over the planned mine life which began production in 2022. However, high-grade open pits are also contributing to current production (E31 and E31N), and the asset is permitted for up to 8.5 million tonnes per annum, suggesting the potential to further increase production longer-term. Overall, this asset may not have a significant impact on the company's gold production (~5% growth vs. guidance of ~770,000 ounces) but will significantly increase copper production, with total copper production increasing by 50% to ~75,000 tonnes. Meanwhile, it should contribute to slightly lower all-in sustaining costs on a consolidated basis.

Overall, the deal is solid given the price paid and the fact that Evolution has added another lower-cost and Tier-1 jurisdiction asset with a long mine life to its portfolio. In fact, the company's average mine life has nearly tripled over the past decade from ~7 years to ~18 years with the addition of Northparkes, giving it a much stronger and longer-life portfolio than when it started with shorter-life and less robust assets at Cracow, Pajingo, Edna May, and Mt Rawdon. That said, these acquisitions and significant upgrade to the portfolio have come at a cost, with production per share and gold-equivalent production per share down meaningfully from 2012 levels as share dilution has outpaced production growth. In Evolution's defense, the portfolio is much stronger and longer-life, but the share count continues to creep higher (now ~2.0 billion shares) which has significantly reduced the benefits on a per share basis.

Evolution Mining - Gold Production Per Share, 2024 Gold-Equivalent Production Per Share & Reserve Life - Company Filings, Company Website, Author's Chart

{kind=link}

Valuation

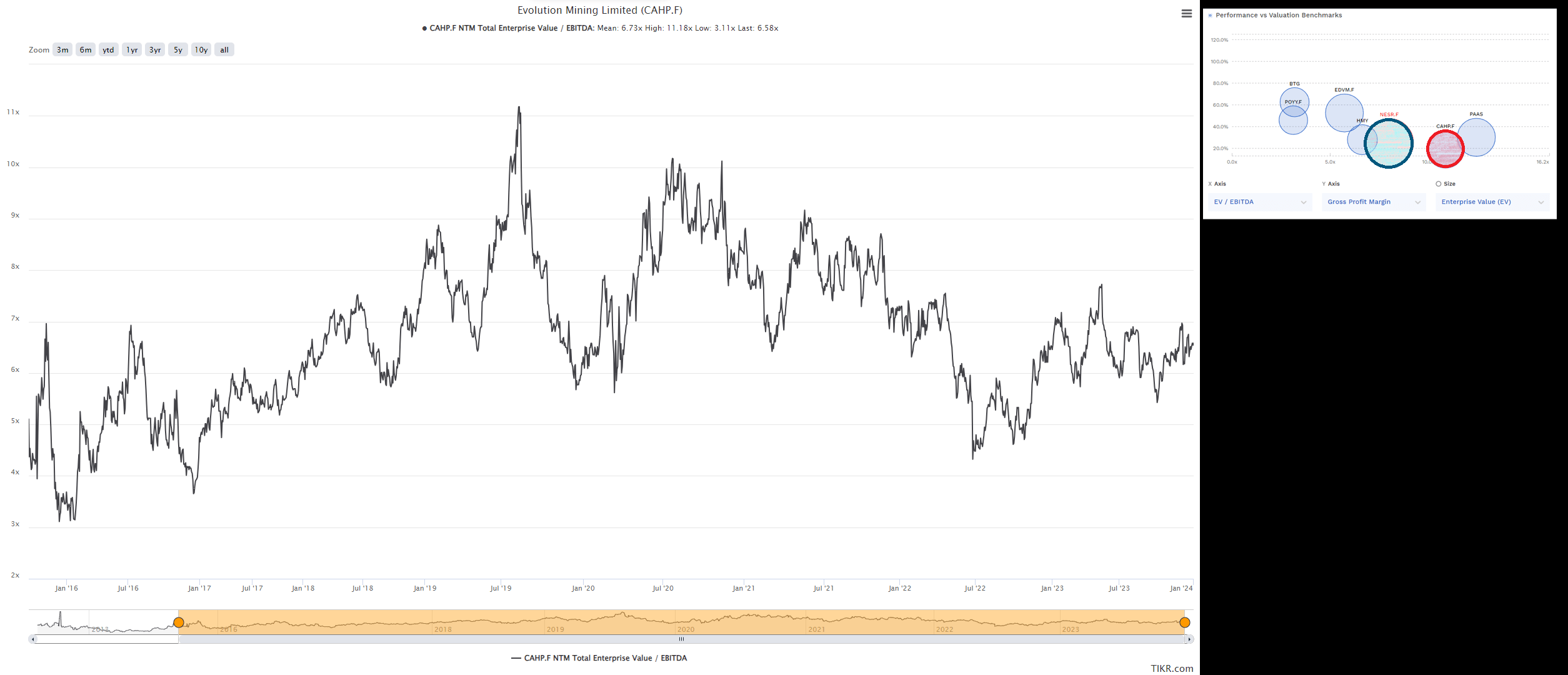

Based on ~2.0 billion shares outstanding and a share price of US$2.61, Evolution trades at a market cap of ~$5.2 billion and an enterprise value of ~$6.7 billion. This makes Evolution one of the highest capitalization names in the mid-tier producer space (500,000 to 1.0 million gold-equivalent ounces), and one of the more expensive names based on an estimated net asset value of ~$4.6 billion, with Evolution trading at a P/NAV multiple of ~1.13. It is worth noting that Evolution deserves a premium multiple given that it operates out of solely Tier-1 ranked jurisdictions (Australia, Canada) and the company has a very diversified portfolio vs. single-asset producers like Lundin Gold ( LUGDF ). Still, even using a generous multiple of 1.30x P/NAV and 8.0x forward EV/EBITDA, I don't see much upside in the stock from current levels, with the stock's fair value coming in closer to US$2.85.

Evolution Mining - Forward EV/EBITDA Multiple, Margins, Enterprise Value & EV/EBITDA Multiple - TIKR, FinBox

{kind=link}

Although Evolution may have ~10% upside from current levels, I am looking for a minimum 30% discount to fair value for Tier-1 jurisdiction producers to justify starting new positions. And if we apply this to Evolution's estimated fair value of US$2.85, the stock would need to decline below US$2.00 to become more interesting from a valuation standpoint. Hence, while the stock has certainly enjoyed a strong rally since I highlighted the stock as a Buy just over a year ago at US$1.20, the relative value setup is much less attractive today, meaning that I continue to favor other miners that have room for a meaningful re-rating vs. Evolution which has already traded above my previous conservative fair value estimate of US$2.00 - US$2.20 (September 2022).

{kind=link}

Summary

Evolution had a slow start to the year which was expected, but we should see progressively higher production as the year progresses with higher grades in H2 at Mungari and Red Lake and higher underground contribution from Cowal. Meanwhile, Northparkes gives Evolution a sixth operation to contribute to its H2 2024 results, setting up an even stronger 2025 on deck with a full year of contribution from this copper-gold mine. Although this is certainly a positive development and it was purchased at the right price, Evolution remains quite leveraged relative to peers, less attractively valued after its significant outperformance, the company has struggled with growing production per share with it growing mostly through M&A. To summarize, while I would consider Evolution Mining from a swing-trading standpoint below US$2.00, I continue to see more attractive bets elsewhere in the sector from a relative value standpoint.

For further details see:

Evolution Mining: A Busy Quarter With A Stronger H2 On Deck