EVKIY - Evonik: A Slow Q1 But There Are Underlying Signs Of Improvement

2023-05-10 13:22:01 ET

Summary

- Evonik is a relatively new position I've been establishing over the past few months, as the company has been troughing between €17-19/share for the native.

- The company reported 1Q23 results as I am writing this article - and there are things to take into consideration here.

- Every solid presented fundamental from my previous article stands - but I am updating my thesis with a current set of expectations.

Dear readers/followers,

I've been investing in Evonik ( EVKIY ) for a number of months now, establishing a very solid position and base at a cost of around €17.9/share for the entirety of my position. I've been following the company for an extensive period of time, but never really gone in, because, with this sort of admitted cyclicality, I do want nearly 20% potential upside - and that's conservative.

For the past few months, we've seen exactly that, and that's why I've been pushing money to work. I'm now at a decent 2.8% exposure with a YoC of close to 6% which I consider well-covered.

The company very recently - meaning May 9 - published its 1Q23 results. In this article, I'm putting Evonik in the context of those results and giving you my take of where I believe things are going.

Evonik Industries - 1Q23 looks slow but is actually indicating a ramp-up

If you look at the headlines, you might be mistaken into thinking that Evonik is seeing a slowdown that might continue for some time to come. While I believe 2023E will certainly come in lower than 2022A, this does not mean that the company is unattractive.

While it's true that the company's overall margins and profitability indicators at best put the company at an average rating, the combination of value and growth potential coupled with improvements in fundamentals and with strategic advancements in accordance with its overall strategy tells me that this company is about to go places.

What do I mean by this?

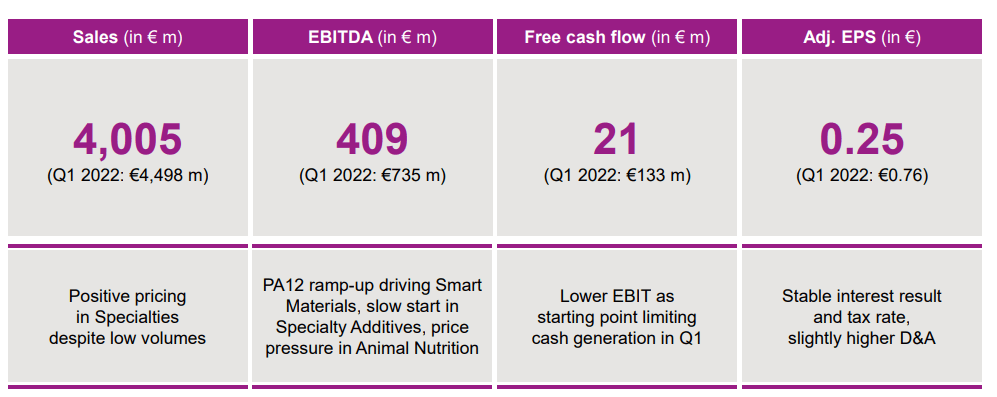

I mean that 1Q23 FCF proxy EBITDA was south of €410, which is less than we might have expected despite positive pricing deltas in specialties and other segments. However, as with other commodities businesses, volumes were actually down, and a combination of pricing pressure, slow starts to key segments, and other negatives, means 1Q23 really doesn't look all that fantastic.

At least not on the surface.

{kind=link}

Doesn't look too great on a YoY basis either, and it looks even worse if we start looking more granularly into the segments. EBITDA margins in Additives fell by 33% aside from the double-digit EBITDA decline, Nutrition dropped 66% in terms of margin at the same time, and smart materials dropped 23%. Granted, these are very high overall comp levels - and they don't really represent fairly comparative levels for the long term. It hides, in a way, the strong pricing the company has managed to push through.

However, in the end, 1Q23 was really a trough quarter in terms of demand, and in terms of margins. Input materials were a real culprit here. Spreads and margins for input commodities like Butadiene and various plasticizers were put under significant pressure - but as the market normalizes and adjusts to these spreads, we're likely to see higher contracted prices for the company's products and commodities.

These results, I argue, are "Hiding" what is really going on under the surface in Evonik. And to understand and to follow that you really have to understand the various trends the companies work in.

Evonik smart materials plants are showing record production, with strong pricing trends that slowly offset the rising variable costs dragging things down. Health care/nutrition is always seeing a slow 1Q typically, and every single company in the sector of Animal Nutrition is reporting the same sort of feed price problem - that includes meat producers. It's a macro thing, and that's not something that Evonik is going to be able to change.

So what makes me positive about the company, when everything here seems to be pointing in the wrong, not right direction?

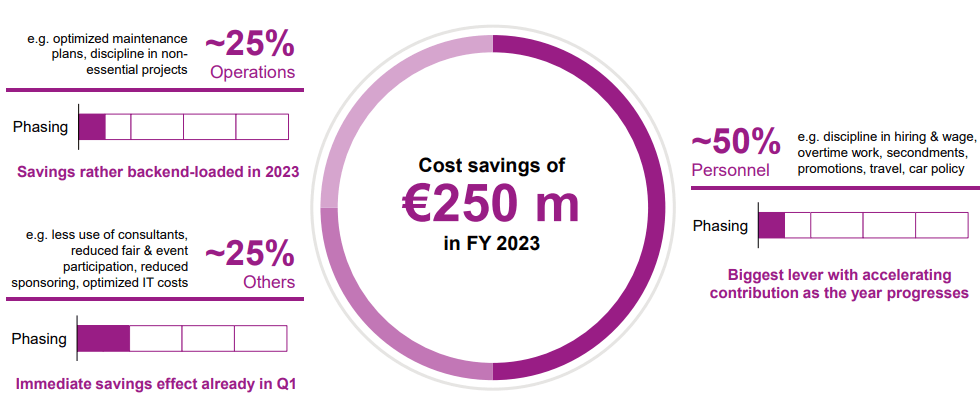

Digging deeper into the monthly numbers, we see sequential improvements on a month-to-month basis. January was trough - and every month since January 2023, we've seen volumes ramping up, order books filling up, improved cost absorption, and pricing deltas picking up with company asset utilization. This is not even mentioning raw materials going down in price, as well as the company-specific contingencies and savings really picking up steam.

{kind=link}

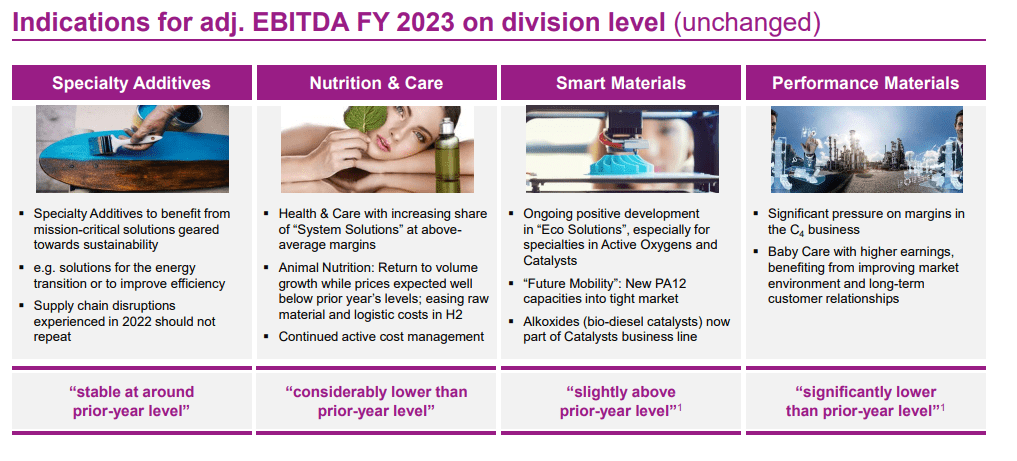

As mentioned, the company's 2022 results were high. 2023 results are doubtful and not likely to be as high. We saw almost €2.5B in 2022 in EBITDA on an adjusted basis. For 2023, I would say we can expect €2.1B, but we probably can't expect more than that given the relatively weak 1Q trends. The company's pick-up and acceleration going into 2Q and 2H will probably save things from being significant in terms of declines, but it won't cause a beat. Animal nutrition is a segment I continue to expect to stay down. Feed costs, based on my research and following the industry, are likely to remain high - so gains will likely come from other segments, including additives and smart materials, as well as from company-wide improvements and contingencies. If we do get massively falling materials and input prices in 2H, as some expect, it's likely that we're going to see additional support for growth and outperformance in the latter half of the year, but that's about it.

The company has provided an FCF outlook and guidance. While cash conversion is expected to be higher, with the improved earnings situation, the positive outlook requires higher CapEx discipline and positive contribution from net working capital, as the company optimizes its flow.

Current segment outlook gives us a confirmation of this expectation for the full year. Performance materials and Nutrition are likely to remain lower, with the rest of the segments and other trends bringing about stabilization.

{kind=link}

What Evonik in the end needs is a normalization in feedstock and input pricing. Without this, these segments will continue to remain compressed - but the same is true for most other companies in the segments or related segments.

On the positive side, financial debt remains extremely manageable, and the company's current EBITDA brings us to a level just north of 2x - again, extremely good both historically and in context.

We do need to account for some higher pension discount rates, but this is only a small change. This company remains a very solid chemical and materials business. Its dividend yield, at 6%, is at the top 95th percentile in its industry, and it's well-covered even in this year. At a payout of €1.17/share, the adjusted EPS that FactSet is forecasting with a double-digit drop at €1.66 is less than 80% EPS payout on an adjusted basis.

Evonik remains BBB+ rated, at nearly $10B, and at the forefront of its field with a debt/cap of less than 27%.

It also happens to trade, at this time, at less than 10x P/E, which is where we move into the updated valuation thesis.

Evonik Valuation - Not as cheap as €17, but still great

The company may not still be trading around €17/share, which would be an amazing price both for the short and long term - but at below €20/share, it still yields 6% and comes with a significant upside potential in my view, even taking into account a muted growth rate due to some of these near-term pressures.

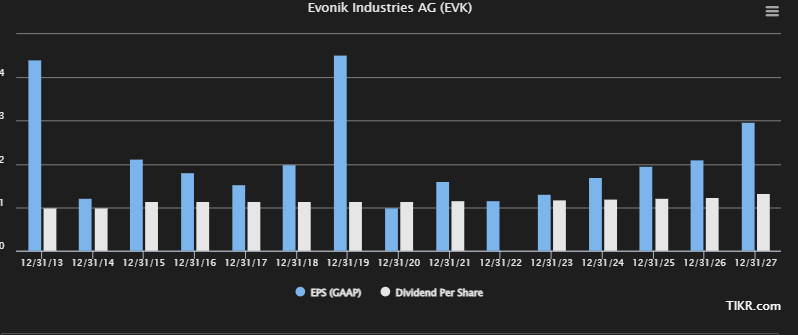

Let's move to GAAP - in terms of GAAP, and not adjusted, EPS is actually expected to increase on a very steady level here - and the payout ratio is expected to improve. Remember, Evonik has always been a very solid dividend payer, and lower EPS has not caused it to pause that shareholder return. I think it is unlikely to do so in the future.

TIKR.com Evonik (TIKR.com/S&P Global)

{kind=link}

My key objective when investing in a stock is participating in the value and earnings growth over time, both through increasing dividends, and also growth in those earnings leading to capital appreciation. While the company is currently in the midst of mixed pressures, I believe near-term results will prove that the company is coming out of this on the right side - with growth. Going forward, I expect we'll see sequential improvements, leading to share price growth and higher returns.

The company's history is an exercise in paying attention to valuation, and that's what we'll do here. What Evonik has done is change the nature of how it operates in terms of products and ambitions. And while this has been a chaotic journey, it's rapidly reaching its end, allowing the company to focus on growth as opposed to transformation.

At any time when you bought at around €20 or thereabouts, you'd have done fine with Evonik. Take note of where the company is currently trading, and you'll see that you're still very much in the game in terms of pricing.

As I mentioned about comps we do compare to, we have peers like Linde ( LIN ), L'Air Liquide ( AIQUY ), BASF ( BASFY ) ( BFFAF ), Ecolab ( ECL ), Sika AG ( SXYAY ) ( SKFOF ), Corteva ( CTVA ), and Dow ( DOW ). I own many of these myself, but Evonik is better-valued and more appealing than all of the ones I just mentioned.

It doesn't have worse fundamentals or a worse credit rating, not materially. It doesn't have worse sales. It's not substantially less efficient - often better in fact, but there's a high "transformation" discount. I obviously do not agree with this substantial transformation discount.

Remember that Evonik is RAG-owned - it has a majority shareholder, so their interests will take precedence. However, RAG has a very aligned set of interests with typical shareholders, which you can see when looking at the company's shareholder return history.

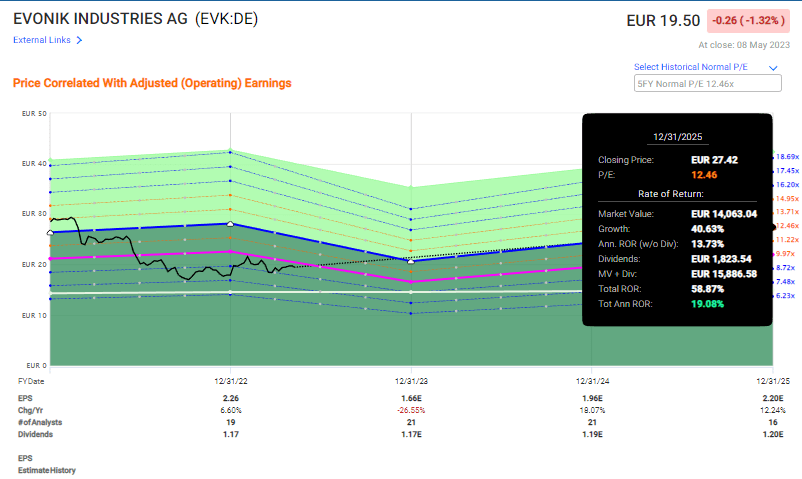

Not much has changed in terms of analyst valuation. They still consider Evonik to be about 20% undervalued to a conservative PT of €24, though that share price range goes from €15 up to €31/share. Regardless though, you're well-served here. The combination of safe yield and attractive upside gives us a potential RoR of nearly 60% in less than 3 years here - and that's to a conservative 12.5x P/E.

Evonik Upside (F.A.S.T. Graphs)

{kind=link}

So, I say that there's plenty of upside here, and based on that, here is my thesis for Evonik.

Thesis

- I've been adding more of Evonik Industries over the past few months, building my position slowly.

- I view Evonik as a substantially undervalued, quality enabler of renewables and ESG-based technology, which puts it on a trajectory for growth for the next decade and more. The yield is another big advantage here.

- I use both common share investments, and I've also written PUTs, taking advantage of the weakness in the share price.

- My PT for the company remains at a conservative €27.5/share given the lack of visibility for some of the divestment and trends in 2023. I could impair it slightly, but I take a longer stance for Evonik, and that longer stance implies all "upside" to me.

- However, the company is a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansion/reversion.

Evonik fulfills every single one of my investment criteria here.

For further details see:

Evonik: A Slow Q1, But There Are Underlying Signs Of Improvement