EVKIF - Evonik: The Reversal Could Be Significant 'Buy'

2023-12-11 13:17:10 ET

Summary

- Evonik Industries' position is currently volatile and uncertain, but I'm not worried.

- The company's 3Q23 results were above expectations, with positive cash generation and a confirmed adjusted EBITDA that can cover the current dividend.

- Evonik is undergoing a strategic realignment of its portfolio and investing in future technologies, which could lead to long-term growth opportunities.

Dear readers/followers,

I've been putting money to work in Evonik Industries AG ( EVKIY ) for some time. The company represents a significant investment both in my private and commercial portfolio and like BASF, the current position of the company is one of volatility and near-term uncertainty.

One might ask themselves if I am worried about the trends that have sent this company down more than 10% in around 8 months - and the answer to that would be no, not really. I know going into these investments that volatility is a core theme, and the holding period for them is often several years. This does not bother me - it would bother me if I bought at some sort of high valuation point, but that is not what I did - I bought the company relatively cheaply.

Evonik is a relatively new position I've been establishing over the past few months, as the company has been troughing between €17-19/share for the native - and even lower at times.

In my original article, I presented the solid fundamentals for this company, and what I expected these fundamentals to do over the next few years.

Let's look at what I expect, in this updated article compared to my last piece , for the company to do.

Evonik Industries - An updated upside based on 3Q23

The upside and expectations for Evonik for 2023 have changed. Meaning, that what was once a relatively decent development for 2023E, has turned into a pretty sharp EPS drop. This has caused the company's share price to decline quite a bit. However, we did not buy at over €30/share, as some investors did, but have an average buy-in cost basis of below €20/share. This means that I believe I bought the company close to the right price.

There's no question that this company is cyclical. However, being cyclical also means that it will cycle up once again - and the question of timing here is the significant one.

Evonik currently manages a yield of almost 7% - though I would be careful expecting this, given that the current adjusted EPS is actually not expected to cover the 2023E dividend (Source: S&P Global). Evonik does not have a history of what the company does in this situation, but I will say that the company has not cut the dividend for almost 10 years - only increased or held it. However, it has never been below earnings, if only momentarily. So we'll have to see.

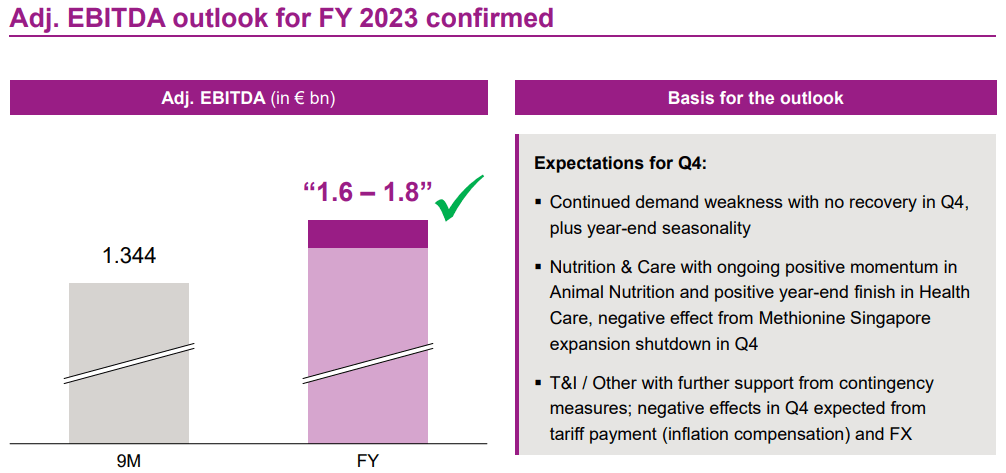

All that being said, the 3Q23 results were substantially above 2Q levels. The company's positive mix managed to offset what was otherwise a very weak market and deliver adjusted EBITDA of just south of half a billion euros on a quarterly basis. Cash generation picked up - FCF was also inching closer to that half-billion, and the company now expects a full-year cash conversion of 40% for 2023E.

The company also confirmed an adjusted EBITDA of €1.6-€1.8B, which by itself would be enough to cover the current dividend.

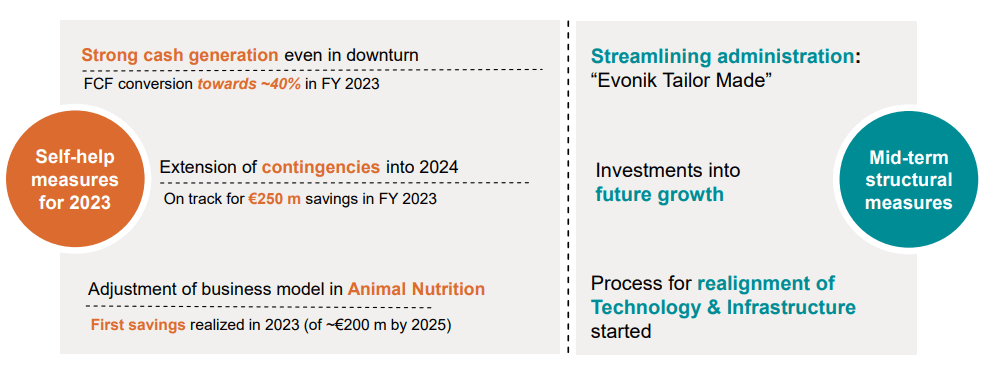

However, the company is currently in the midst of a strategic realignment of its portfolio. This is not news, that's what has been going on for some time, but it seems that the company is doubling down on this focus to address the current downturn.

{kind=link}

All of these contingency measures are in fact on track for the year, with 70% delivered after a 9M basis, and fixed costs clearly below 2022 and in fact, overcompensating to overall inflationary levels.

What I mean by this is that Evonik has managed to offset inflation on the fixed costs side. And this continues with a clearly declining trend into 4Q, from areas like personnel, services and travel, logistics and maintenance - the company is "cutting the fat", as it were - and it's a good thing.

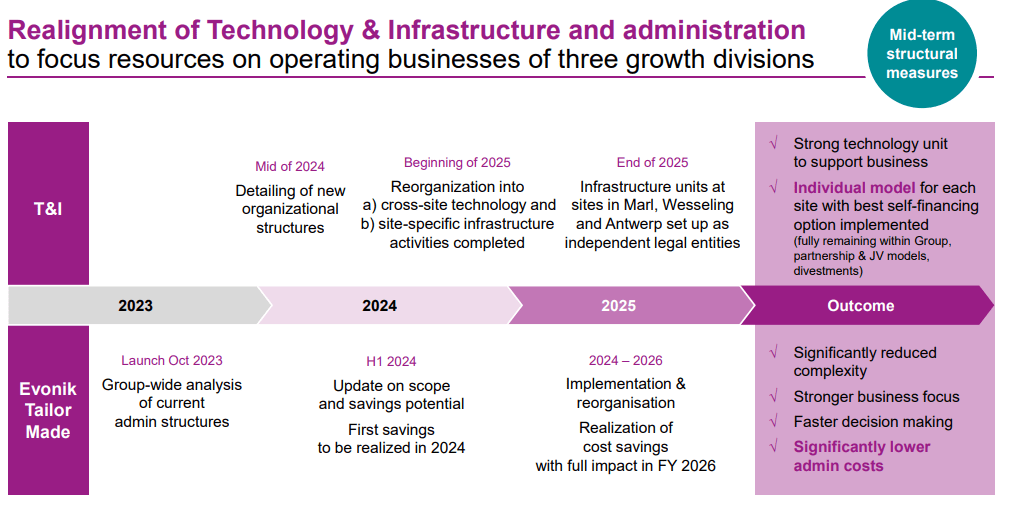

Here is the current plan the company is executing on.

{kind=link}

At the same time, Evonik is investing in future technologies. We're talking about things like SEPURAN membranes for gas separation, and green membranes where the company has the 1000th biogas plant focusing on this. We're also talking mid to double-digit investments in the millions of euros in a plant in Austria, completion in 1h25. Evonik is also moving to start up the first world-scale biosurfactant plant on time in 2024-2025. The company will take the fight to legacy surfactant technologies, and the first samples are expected in 4Q23.

Also, Evonik is moving deeper into its JV in China for gut health and animal nutrition products, entering the market early next year. So there are plenty of things happening in China.

All of these positive and interesting developments can't really disguise operational weakness in the current results. We're seeing declining overall sales, declining adjusted EBITDA, somewhat higher FCF due to very strict working capital, and not as bad an adjusted EPS level as I expected. if the company manages to score a decent adjusted quarterly EPS, the dividend should, on the basis of this, not be in danger - and this EPS is already impaired by almost 35% by planned divestments of Superabsorber.

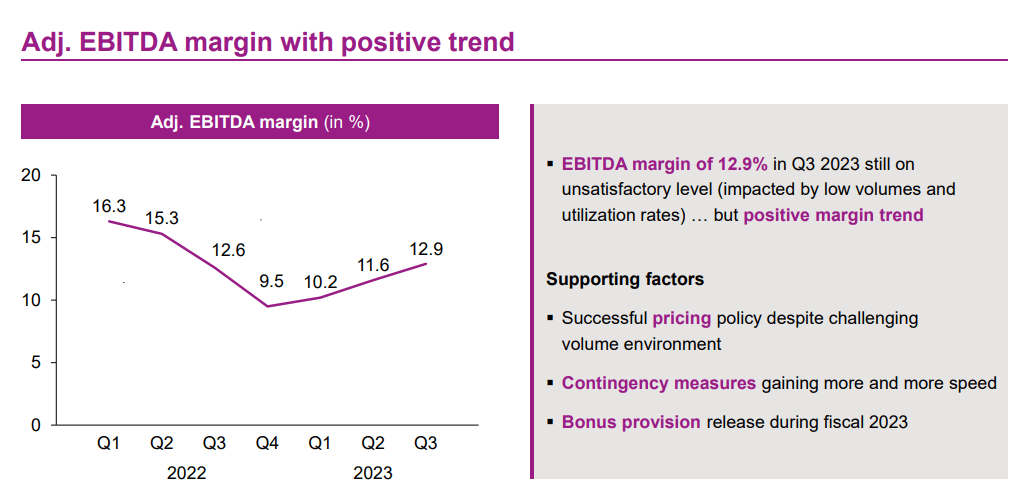

It's however fair to say that margins have turned around from trough levels.

{kind=link}

From a segment-specific view and expectation, the company saw significant demand weakness in core areas like Specialty additives with declines due to weak customer demands and inventory destocking. These are exactly the same trends we've seen across the world in basic materials. They are neither strange nor are they unexpected - and they're also not expected to be solved overnight. Nutrition & Care had decent flat development, a sequential EBITDA increase, good volume development, and lower variable costs - but there's a negative impact coming in 4Q due to plant maintenance. Smart materials also went down YoY, but again - sequential trend improvement.

Evonik IR (Evonik IR)

In the company's performance materials, there were certain product groups still seeing advantages from contract pricing levels, but once these turn around, EBITDA will turn even lower. This segment is perhaps the worst on the basis of weakened demand, weakened pricing, low downstream demand, and poor margins for the time being.

The focus here should be on overall forecasts. The company is candid about the volatility and the uncertainty of the market.

{kind=link}

What I would like to focus on is the fact that this is the worst market environment in over 10 years, and the company is still managing to generate this sort of adjusted EBITDA and overall upside. Also, the company has very solid fundamentals. Maturities are well-laddered, BBB+ and Baa2 stable confirmed, despite the profit warning back in July, and the company has gone ahead and refinanced its bonds early, with no current maturities until at least about a year.

As of the 3Q, the company has over half a billion euros worth of cash and equivalents on its balance sheet, with a €1.75B syndicated revolver. Cash is a non-issue for Evonik going through this environment.

Let's look at the risks and upsides.

Risks & Upside

The real risk for Evonik here is a continued longer downturn, which would, as I see it, put further pressure on the valuation here. Couple this with the realistic potential for a dividend cut (a part of me sees this as justified here), and investors might not see the upside in the near term they expect from Evonik that they expect at the current rate. There are substantially safer options for investment out there today. The risk is for a downturn related to the cycle - not due to fundamentals, those are solid.

At least, that is the main risk that I see for Evonik personally.

The upside for Evonik is holding it through the cycle and enjoying the fruits of the company's labor as an investor when it comes out the other side. Because, as I see it, those fruits are going to be sweet indeed. We're talking well into 20-25% annualized at the right sort of expectations.

Let me show you in valuation.

Valuation

So, first off, I'm not changing my PT, even though I considered doing so given the degree of near-term weakness. The reason I am not changing it and still am saying €27.5, is because this PT already included a substantial lack of visibility and overall weakness in the near term. This was always a longer-term play, and it certainly still is.

Even just normalized, the company has a 15-16% annualized RoR from this price - and we need to remember, that Evonik has a 10-year history of beating estimates more than 40% of the time with a 10% margin of error. (Source: FactSet)

If the market starts taking into consideration the company's rate of growth, the company's fundamentals of BBB+, and very low debt of less than 24% of LT/debt to cap, much like other German stalwarts, then I believe the RoR we see here could be 140-150% inclusive of dividends for the next 2-3 years. Of course, this requires a premium due to growth. Somewhere in between that 15-45% annualized lies the 20-25% annualized that I consider likely for this company.

I believe that once the cyclical tendencies are clarified, that's where this company is likely to trade - but what we need to see, just like with my investment in HeidelbergCement when I sold at the upcycle, is for this investment to really materialize expected upside - likely come next year, as well as 2025E.

This is a 2-year play, and nothing I can see at this time changes this.

At any time when you bought at around €20 or thereabouts, you'd have done fine with Evonik. Take note of where the company is currently trading, and you'll see that you're still very much in the game in terms of pricing.

As I mentioned about comps we do compare to, we have peers like Linde plc ( LIN ), L'Air Liquide S.A. ( OTCPK:AIQUY ), BASF SE ( OTCQX:BASFY ) ( OTCQX:BFFAF ), Ecolab Inc. ( ECL ), Sika AG ( OTCPK:SXYAY ) ( OTCPK:SKFOF ), Corteva, Inc. ( CTVA ), and Dow Inc. ( DOW ). I own many of these myself, but Evonik is better-valued and more appealing than all of the ones I just mentioned. I believe many of these companies are worth your consideration - that's why you can expect an update on some of them, like Sika AG as well in the near term.

However, Evonik remains a major play for me at this time - and my thesis for the company is as follows.

Thesis

- I've been adding more of Evonik Industries over the past few months, building my position slowly.

- I view Evonik as a substantially undervalued, quality enabler of renewables and ESG-based technology, which puts it on a trajectory for growth for the next decade and more. The yield is another big advantage here.

- I use both common share investments, and I've also written PUTs, taking advantage of the weakness in the share price.

- My PT for the company remains at a conservative €27.5/share given the lack of visibility for some of the divestments and trends in 2023. I could impair it slightly, but I take a longer stance for Evonik, and that longer stance implies all "upside" to me.

- However, the company is a "BUY" here.

Remember, I'm all about:

- Buying undervalued - even if that undervaluation is slight and not mind-numbingly massive - companies at a discount, allowing them to normalize over time and harvesting capital gains and dividends in the meantime.

- If the company goes well beyond normalization and goes into overvaluation, I harvest gains and rotate my position into other undervalued stocks, repeating #1.

- If the company doesn't go into overvaluation but hovers within a fair value, or goes back down to undervaluation, I buy more as time allows.

- I reinvest proceeds from dividends, savings from work, or other cash inflows as specified in #1.

Here are my criteria and how the company fulfills them (italicized).

- This company is overall qualitative.

- This company is fundamentally safe/conservative & well-run.

- This company pays a well-covered dividend.

- This company is currently cheap.

- This company has a realistic upside that is high enough, based on earnings growth or multiple expansions/reversions.

Evonik fulfills every single one of my investment criteria here.

Editor's Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

For further details see:

Evonik: The Reversal Could Be Significant, 'Buy'