EVG - EVV: Larger Discount Presents A Better Opportunity

2023-08-14 17:22:01 ET

Summary

- EVV is a more compelling fixed-income closed-end fund to invest in due to improved distribution coverage and a wider discount.

- The fund utilizes leverage and has a multi-sector bond fund approach, with a focus on senior loans and non-investment grade bonds to help give it a "limited duration."

- The fund's discount is trading well below its historical average, which is the primary factor behind me being less cautious than around a year ago.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Around a year ago , we gave Eaton Vance Limited Duration Income Fund ( EVV ) a lo ok. The distribution coverage was weak, and the discount on the fund was shallow and uncompelling. Today, coverage has improved while they changed their managed distribution policy to come much closer to what they are actually earning.

This distribution adjustment is probably what caused some of the valuation to deflate to a larger discount. Either way, today, EVV looks like a more compelling fixed-income closed-end fund to invest in without as much caution as warranted as a year ago. The slowing pace of rising interest rates and the likelihood of nearing the end of this rate hiking cycle could mean less of a headwind going forward as well, at least in the interest rate department.

The Basics

- 1-Year Z-score: -0.76

- Discount: -9.78%

- Distribution Yield: 9.75%

- Expense Ratio: 1.29%

- Leverage: 30.3%

- Managed Assets: $2 billion

- Structure: Perpetual

EVV's investment objective "is to provide a high level of current income. The Fund may, as a secondary objective, also seek capital appreciation to the extent consistent with its primary goal of high current income."

To achieve this, they take a multi-sector bond fund approach. They are invested in a diverse asset mix of credit instruments, though the largest contributors are senior loans and non-investment grade bonds. That's what can primarily make them hit their "limited duration" target of between zero and five years. The latest fact sheet shows a leverage-adjusted duration of 3.3 years.

Leverage Discussion

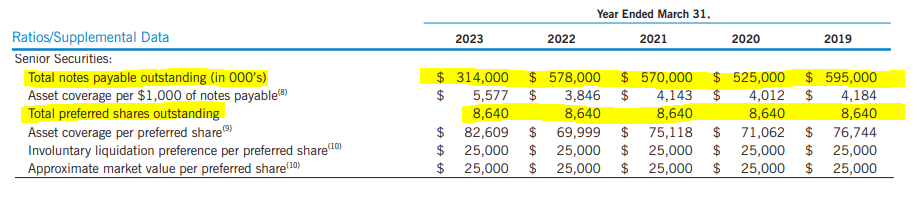

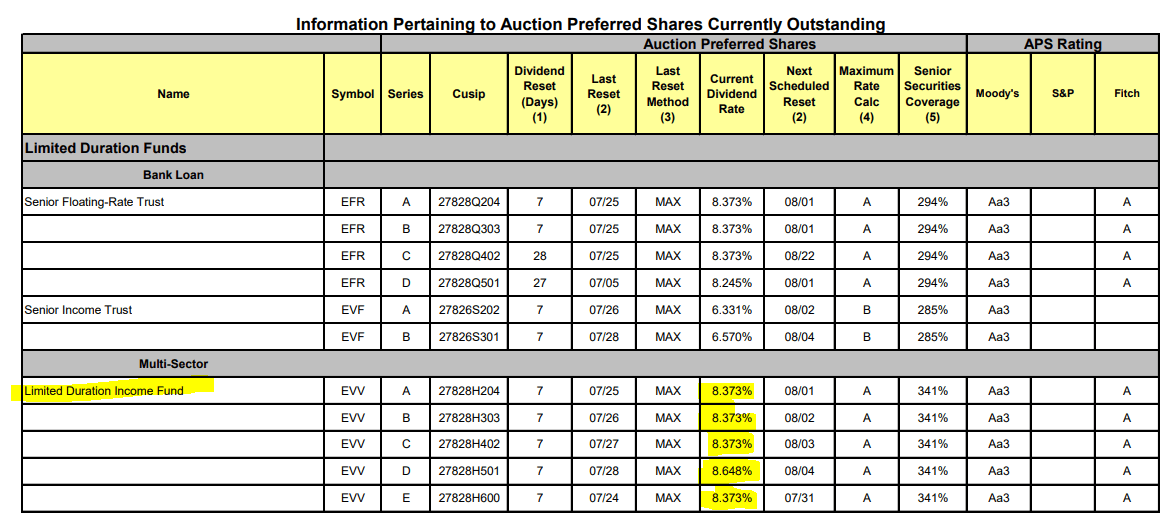

Similar to other leveraged funds, EVV is having to deal with higher interest rates driving up their costs to borrow. They utilize borrowings between auction preferred shares and a credit facility. Eaton Vance had started to redeem their APS since the 2008 auction failures. EVV has " redeemed/repurchased 73% of its APS."

That being said, they haven't redeemed any in years and instead have taken to adjusting their credit facility when the need arises. This is a more flexible form of borrowing that can be easier to adjust as needed. Hence this is the fairly standard operating procedure for these types of leveraged CEFs.

{kind=link}

The APS is costing them well over 8% as of the latest update, making it a very expensive form of financing.

{kind=link}

This is important to consider because that has been pushing up the total expense ratio of the fund. As of their last annual report, total expenses came to 2.72%, up from 1.77%. Fortunately, with so much floating rate exposure for the fund, it has been a natural hedge against these rising rates. The fund has still seen its net investment income rise as yields rise in the underlying portfolio.

In addition to the floating rate exposure in the fund's underlying portfolio, the fund has also implemented futures contracts where they short various U.S. Treasury and Euro bonds and notes to hedge against rising interest rates as well. With these efforts, the fund became less interest-rate sensitive and was able to offset the rising costs of leverage. The fund now produces higher NII and has realized capital gains related to these futures contracts.

Discount Presents A Potential Opportunity

As mentioned, the last time we touched on EVV, the fund's discount was fairly shallow at around 3%. Fast forward to around a year later, and we have a more compelling opportunity to initiate a position. The fund's discount is trading well below its historical average since inception.

Ycharts

In looking at the fund's historical performance against its blended benchmark, the fund has often produced a higher upside over the longer term. In the more short-term one-year period, the fund had struggled, but this is likely due to the leverage impact on the fund.

EVV Historical Performance Relative to Benchmark (Eaton Vance)

{kind=link}

The blended index is; "33.33% Morningstar LSTA US Leveraged Loan IndexSM, 33.34% ICE BofA U.S. Mortgage-Backed Securities IndexSM, and 33.33% ICE BofA Single-B U.S. High Yield Index (the Blended Index)." This helps represent the dynamic allocation of EVV.

Distribution Changes To Managed Plan

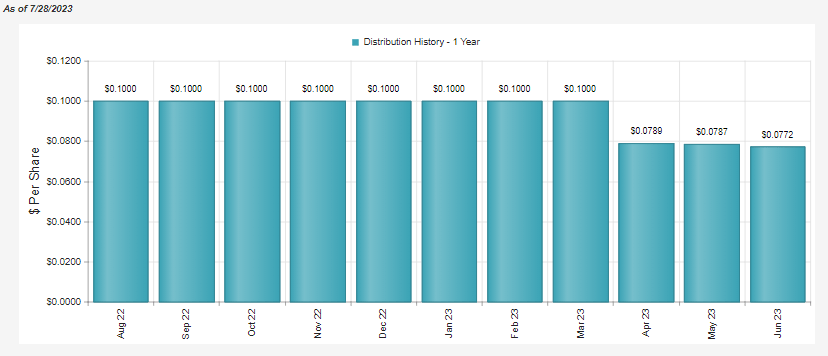

When they made changes to the Eaton Vance Short Duration Diversified Income Fund ( EVG ) earlier this year, they also changed up EVV's managed distribution plan. Similar to EVG, there was no note saying exactly what the new plan is exactly.

However, based on the monthly changes in the payout, we can clearly confirm that it is a monthly adjusted plan. With a bit of an assumption based on the changing amounts, we can also take a guess that it is close to a 9% managed plan. The $0.0772 worked out to an 8.88% distribution rate, but July isn't reflected on CEFConnect yet, which was a small bump to $0.078.

{kind=link}

The $0.078 annualized works out to $0.936, which just happens to be exactly 9% of the $10.40 NAV on the last day of June. This is also consistent with the previous month's payouts in each of the respective prior closing month NAV amounts equaling ~9%.

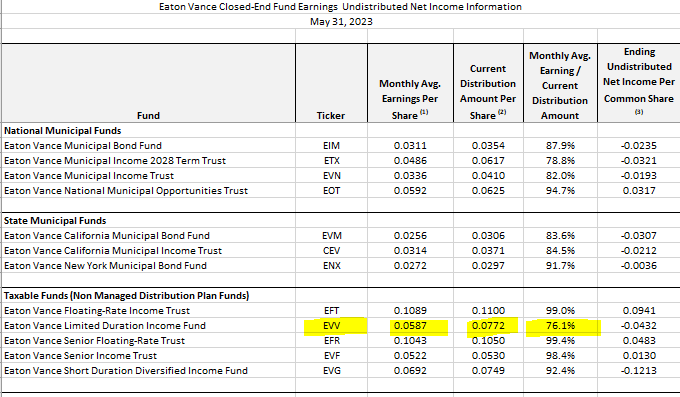

Distribution cuts are never fun, but with the reduction in the payout and a growing NII per share, the fund's coverage has improved quite materially. Nearly a year ago, for the month ended July 31, 2022, distribution coverage came to 54.8% with average monthly earnings per share of $0.0548.

EVV Latest UNII Report (Eaton Vance (highlights from author))

{kind=link}

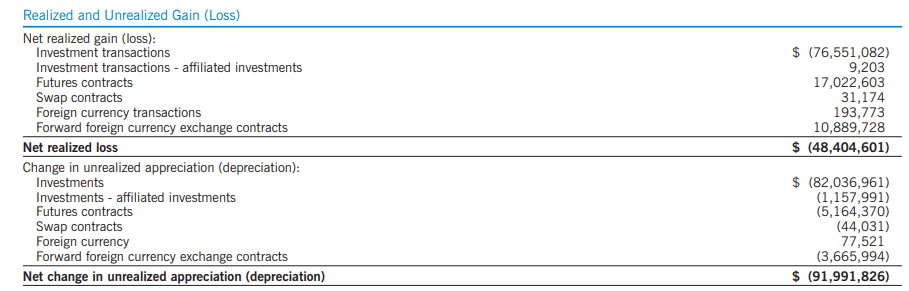

To help provide coverage for the distribution, the fund can also realize gains in its portfolio. That's not usually a source that can be as consistent for a fixed-income fund; however, with their derivatives, they've helped significantly in the last year. It helped offset a portion of the realized losses in the underlying portfolio. Though it clearly wasn't enough to offset all the losses in the fund.

The largest contributors to offsetting the losses came from the futures contracts, but also forward foreign currency exchange contracts also provided some hedges against losses.

{kind=link}

Given the fixed-income focus of the fund, it's natural to see most of the distribution being characterized as ordinary income. However, for EVV, since they were paying out well beyond what their portfolio could support, we also see significant distributions identified as return of capital.

{kind=link}

EVV's Portfolio

Portfolio turnover in the last year exploded to a 201% rate. This was above 137% in fiscal 2022, which was also well above the 2021 turnover rate of 57%. So clearly, we have seen a lot of changes in the underlying portfolio take place in the last fiscal year. At the same time, the actual portfolio mix hasn't changed dramatically.

Senior loans make up the largest allocation of the fund, which was at 35.8% a year ago. High-yield bonds or non-investment grade bonds also made up the second largest allocation when it was at 25.7% previously. Finally, U.S. Government/ Agency MBS also made up the third largest and most material allocation for the fund at 23.5%. The other allocations don't represent a meaningful weighting for the fund.

EVV Asset Breakdown (Eaton Vance)

Senior loans offer floating rate exposure for the fund and help limit the fund's duration. High-yield loans also tend to have lower relative durations because they often have shorter relative maturities than their investment-grade counterparts.

The agency MBS comes with mostly fixed rates. However, with how the rest of the portfolio is positioned combined with the hedging, the duration still stays limited. Not all of the positions are allocated to fixed rates either; some are based on floating rates when looking through their holding list. The Agency MBS and other U.S. Government exposure also help shift the credit quality of the portfolio higher.

EVV Portfolio Credit Quality (Eaton Vance)

The fund overall is fairly junky, but this added diversification can help mitigate the downside too. Besides hedging through various derivative contracts and having a material portion of its portfolio in AAA quality, the portfolio also limits risk by spreading it out across a number of holdings. In this case, the fund lists the number of holdings at 1298.

At this number of holdings, you get some negative with the diversification. You aren't necessarily going to see any wild outperformance, but conversely, you also shouldn't see any massive losses mount relative to their blended benchmark either.

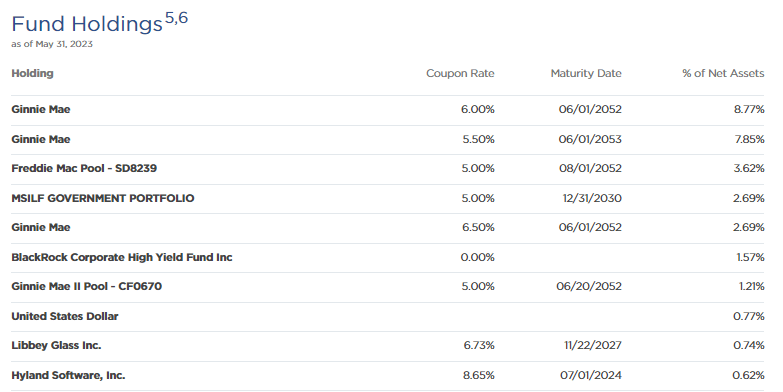

The largest holdings in the fund are agency MBS related or the Morgan Stanley Institutional Liquidity Fund ( MUIXX ) at 2.69%, which is just short-term treasury cash-equivalent type securities as it's a money market fund. While the top holdings of the fund comprise a fairly large weighting, they can contain hundreds or even thousands of pooled loans.

{kind=link}

Conclusion

EVV looks like a more interesting fund than it had been in the past due to its discount widening. However, this discount widening could have been at least partially triggered by the result of a change in its distribution policy. It now pays out a lower managed distribution rate that changes monthly. CEF investors tend to like level distributions, so a monthly changing payout could be a negative for some.

Admittedly, last year the discount had widened out to similar levels where they currently are now before this adjustment even took place. In this case, the discount has been more persistent than in the prior cases; the fund narrowed the discount quite sharply.

EVV Discount History (CEFConnect)

While I don't suspect that will be the case this time, I still believe that the current discount represents a much more attractive level to consider investing in this limited-duration multi-sector bond fund.

For further details see:

EVV: Larger Discount Presents A Better Opportunity