EVV - EVV: Limited Duration Income Portfolio With A Decent Discount

2024-01-18 03:57:00 ET

Summary

- Eaton Vance Limited Duration Income Fund provides exposure to debt instruments with a focus on floating rate exposure to limit duration.

- The fund has a wide discount and offers a diversified portfolio across many holdings and both investment-grade and below-investment-grade credit.

- The distribution is appealing and gets a boost thanks to the discount; however, coverage is weak and that should be considered.

Written by Nick Ackerman, co-produced by Stanford Chemist.

Eaton Vance Limited Duration Income Fund ( EVV ) provides investors exposure to debt instruments with a focus on incorporating floating rate exposure to limit the fund's duration. Duration is an interest rate sensitivity measure, and it tells us how much the fund's underlying portfolio should move based on changes in interest rates. Floating rate exposure is particularly attractive in a rising rate environment; however, it also isn't a bad idea when designing an all-weather portfolio always to have a diversified pool of assets.

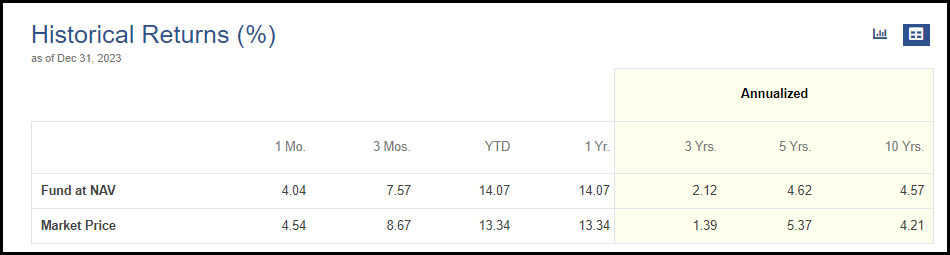

Since our last update, the fund's discount has widened a touch further. Overall, the total returns have been quite attractive anyway.

EVV Performance Since Prior Update (Seeking Alpha)

With a wide discount, this fund is still worth considering for investors looking for a diversified multi-sector debt portfolio. With over 1200 holdings, one is definitely diversified. Additionally, the fund is further diversified as an investor is getting exposure to both investment-grade and below-investment-grade instruments as well.

EVV Basics

- 1-Year Z-score: -0.24

- Discount: -10.03%

- Distribution Yield: 10.04%

- Expense Ratio: 1.22%

- Leverage: 39.3%

- Managed Assets: $2 billion

- Structure: Perpetual

EVV's investment objective "is to provide a high level of current income. The Fund may, as a secondary objective, also seek capital appreciation to the extent consistent with its primary goal of high current income."

To achieve this, they take a multi-sector bond fund approach. They are invested in a diverse asset mix of credit instruments, though the largest contributors are senior loans and non-investment grade bonds. That's what can primarily make them hit their "limited duration" target of between zero and five years.

The latest fact sheet shows a leverage-adjusted duration of 4.15 years. That's been extended a bit compared to the prior update of 3.3 years, but still comfortably in the range they target. With rates expected to come down, it wouldn't necessarily be a bad thing for the managers to start incorporating investments that take them to the longer end of their target range.

Since our last update, the fund's leverage ratio has also increased to nearly 40% from around 30%. This occurred as they took up the borrowings on their credit facility. This is based on a floating rate of SOFR plus a spread, with the fund's last semi-annual report showing an interest rate of 6.33%. Given the limited duration exposure via floating rate investments, this isn't so much of a problem for this fund as they are likely putting this capital to work and earning a positive spread.

The fund also incorporates preferred shares for leverage. While this is often a form of fixed-rate leverage for other funds, in this case, it is auction-preferred shares. That means they are paying a variable rate, and the rates here were substantial, coming in at over 8%.

{kind=link}

Still, being able to invest in floating rate securities on the lower quality of the credit spectrum likely still results in a positive spread. Given that, we saw net investment income rise in the latest report, reflecting this being the case. In total, the expense ratio for this fund was lifted to 3.06% from 2.72% at the end of fiscal 2023.

Discount Remains Appealing

Despite the floating rate exposure the fund carries, we still saw the fund take a meaningful hit in terms of share price and NAV going lower throughout 2022. However, similarly to most other fixed-income CEFs, 2023 provided a rebound to claw back most of those losses.

{kind=link}

At the same time, the fund's discount has widened over the last year as well. The fund is now trading just below its longer-term decade-long average. The fund was able to touch near parity with its NAV during 2021 and 2022 - though it was an admittedly volatile time, as we can see.

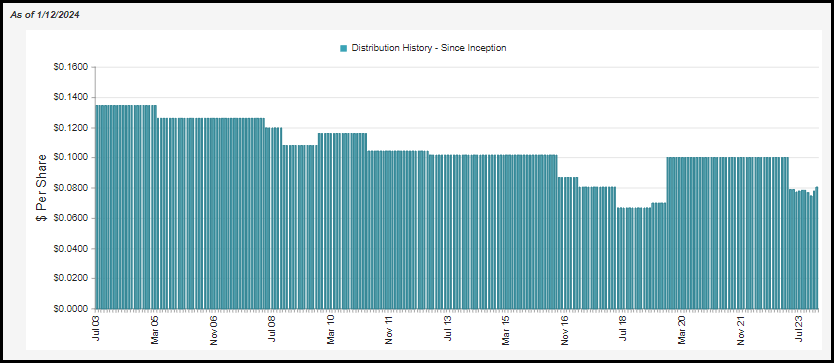

That was also prior to their distribution change, which saw a significant decline in the payout, and going to a variable rate due to monthly adjustments is also often less appealing to income investors in CEFs. So, I don't necessarily think that the current discount is a screaming buy, but it is certainly not the worst time to consider at this valuation.

Ycharts

Distribution Lacking Coverage

Despite the higher expense ratio that we highlighted above when factoring in the borrowing costs rising materially, the fund generated a higher NII ratio of 7.79% from 6.47%. Again, that further reinforces the fact that the higher borrowing rates have been more than offset by the fund's floating rate exposure benefiting from the higher rate environment.

That means when rates are cut, the fund will actually be at more of a disadvantage unless the managers can shift their portfolio further into higher-yielding fixed-rate debt instruments. However, the fund comes with an overall ceiling on the limit that they can incorporate if they want to stay within the duration range that they've stated.

Additionally, since the fund doesn't bother to pay out what it earns but instead has chosen a managed policy, they have been overpaying its distribution. The policy varies monthly, but it is based on a 9% NAV rate. This was a relatively newer policy put in place in early 2023.

{kind=link}

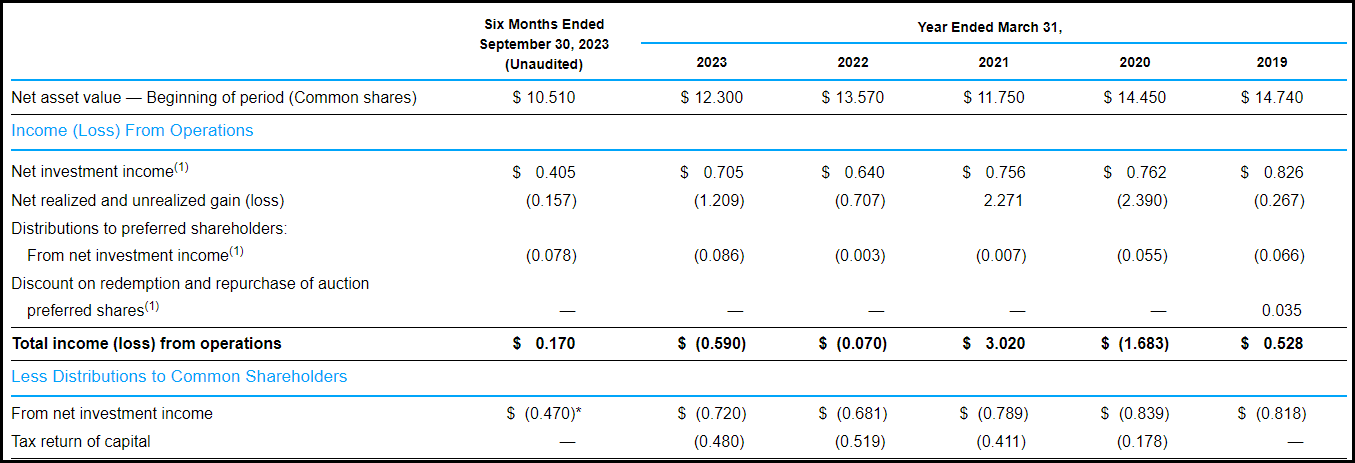

The lack of coverage is reflected below in that the fund earned $0.405 NII per share in the last semi-annual report but ended up paying out $0.47 in distributions.

{kind=link}

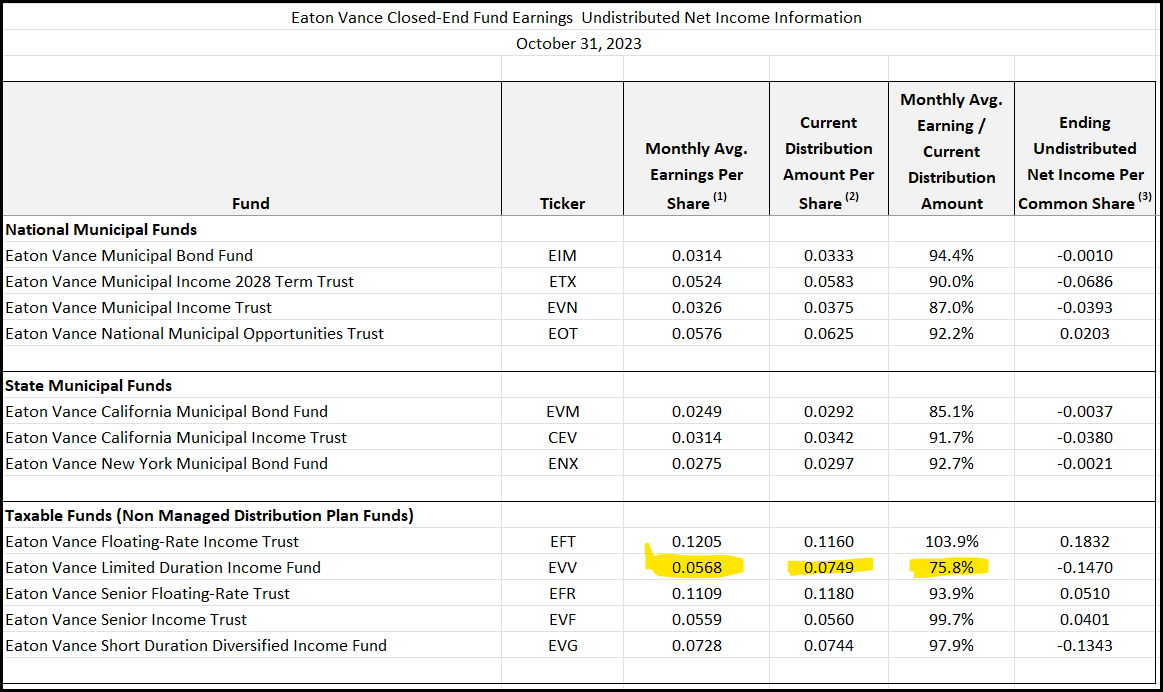

This is further reflected in the latest UNII report as of October 31, 2023. We see there that the fund's NII coverage ratio came to 75.8%. That's a tick lower than the 76.1% coverage ratio we saw in our previous update.

{kind=link}

What this means is that unless they can see underlying appreciation and gains in their portfolio, the NAV should generally trend lower over time. With rates being cut, we might be able to see some appreciation, but that could be short-lived for the next year or two before the trend would once again return to gradually going lower.

It's important to consider, though, that even with a declining NAV, that doesn't mean the fund isn't worthwhile to own. The fund can still produce positive total returns when factoring in the distributions overall.

Still, while the fund's distribution yield comes to around 10% and the NAV rate is roughly at 9%, this could be considered closer to 7.5% and 6.75%, respectively. Those rates would be based on what is actually being earned, and thanks to a significant discount, the difference is substantial.

As we highlighted in our previous update, this does mean return of capital distributions.

Given the fixed-income focus of the fund, it's natural to see most of the distribution being characterized as ordinary income. However, for EVV, since they were paying out well beyond what their portfolio could support, we also see significant distributions identified as return of capital.

{kind=link}

EVV's Portfolio

EVV's portfolio is able to have a lower effective duration, primarily thanks to its senior loan exposure. This is one of the main focuses of the fund, along with non-investment grade bonds and U.S. Government/Agency debt instruments. These three components make up the overwhelming majority of the entire portfolio.

EVV Portfolio Asset Mix (Eaton Vance)

This has tended to be the case, and it actually hasn't changed much since our prior update. Similarly, the credit quality the fund is exposed to in its underlying 1,203 total holdings has barely budged as well since our prior update. The portfolio remains slightly tilted toward below-investment-grade debt, but the higher quality of BBB and above still represents a meaningful allocation as well.

EVV Portfolio Credit Quality (Eaton Vance)

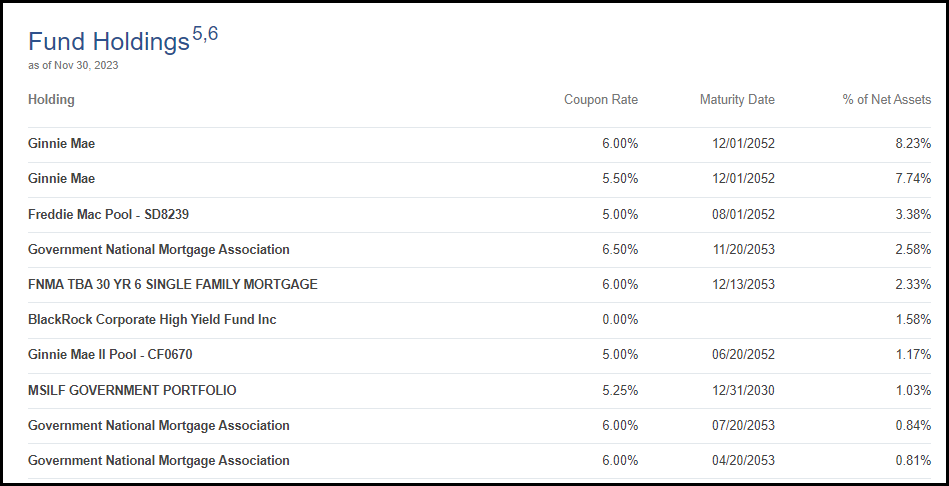

The high credit quality is primarily thanks to the U.S. government or U.S. Agency MBS. Government National Mortgage Association or Ginnie Mae represents the highest exposure in the top ten. These securities seemed to have slipped by a rating downgrade, unlike Freddie Mac and Fannie Mae when the U.S. was downgraded by Fitch earlier in 2023.

While these are showing fairly high concentrated positions in the top ten for the first few holdings, these are backed by hundreds or thousands of underlying mortgages. That takes their vast number of holdings and multiplies it even further in terms of underlying exposure.

{kind=link}

Perhaps what could be a bit surprising here is how little the broader composition of the portfolio has remained, given the fund's 109% turnover rate - which isn't even annualized. This also isn't really an anomaly. In FY 2023, the turnover rate came to 201%, and FY 2022 saw a turnover rate of 137%. That said, given a target duration range, it also makes sense that the overall composition hasn't changed drastically. If it were, that could push them outside the limited duration targets.

Conclusion

EVV is highly diversified and provides investors exposure to a target range of duration that is limited, as its name would suggest. They do this by investing with a material weight in floating-rate securities. However, they also incorporate fixed-rate bond exposure as well to make them a more multi-sector fixed-income fund overall. The fund's discount doesn't make it a screaming deal here, but it does represent a decent discount on an absolute basis. On a relative basis, the fund is trading near its longer-term average, which represents a level that seems like a fair valuation overall.

The fund's distribution rate is quite appealing, and thanks to the large discount, investors get a 'boost' relative to what the fund has to earn (the NAV rate) and what investors receive (the market rate.) That said, this is a policy based on a 9% NAV rate that is adjusted monthly.

They also aren't able to earn that amount, so they would require capital gains to cover a shortfall. What is more likely is that the NAV will generally trend lower over time outside of fairly short periods. One of those periods could be coming up if we get the rate cuts that are expected in the next year or two. Rates being cut should help boost the value of the underlying portfolio, which could see NAV rise during this period despite the shortfall in coverage.

For further details see:

EVV: Limited Duration Income Portfolio With A Decent Discount