EVV - EVV: Near-Term Share Price Declines Likely But Remains A Hold

2024-01-18 03:26:43 ET

Summary

- Eaton Vance Limited Duration Income Fund offers a high level of income with a current yield of 10.04%, which is higher than many other fixed-income funds.

- EVV's recent performance has been respectable, with shares up 10.60% since late October, outperforming the Bloomberg U.S. Aggregate Bond Index.

- The fund's portfolio includes a mix of bonds, debt securities, and leveraged loans, providing some protection against interest rate changes.

- The market is probably wrong about the extent to which the Fed will cut interest rates this year, but this fund should hold up better than peers in a correction.

- EVV has been failing to cover its distributions, but the valuation right now is very reasonable.

The Eaton Vance Limited Duration Income Fund ( EVV ) is a closed-end fund that may be helpful for those investors who are looking to earn a very high level of income from the assets in their portfolios. The fund does a fairly good job at this task, as its 10.04% current yield is very competitive with most other fixed-income funds today. Indeed, this yield is actually quite a bit higher than some of the most popular investment-grade and junk bond funds that currently trade in the market. This is not exactly surprising though, as the inverted yield curve has generally resulted in assets with a shorter duration having higher yields than long-duration assets. That is a direct result of the market's expectation that the Federal Reserve will shortly pivot and begin rapidly cutting interest rates. As we will discuss in this article, that scenario appears to be unlikely to actually play out and this fund should be able to perform reasonably well if the central bank does in fact keep interest rates higher for longer than the market currently expects.

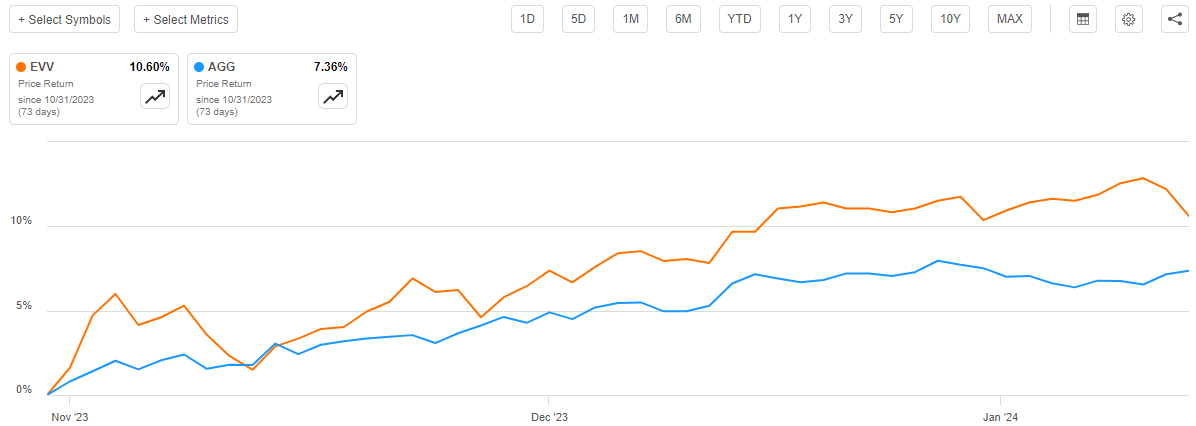

As regular readers may remember, we last discussed the Eaton Vance Limited Duration Income Fund back in late October. The fund's performance since that time has been quite respectable, as its shares are up 10.60% since the date that my previous article was published. That is quite a bit better than the Bloomberg U.S. Aggregate Bond Index ( AGG ) has managed to deliver over the same period:

{kind=link}

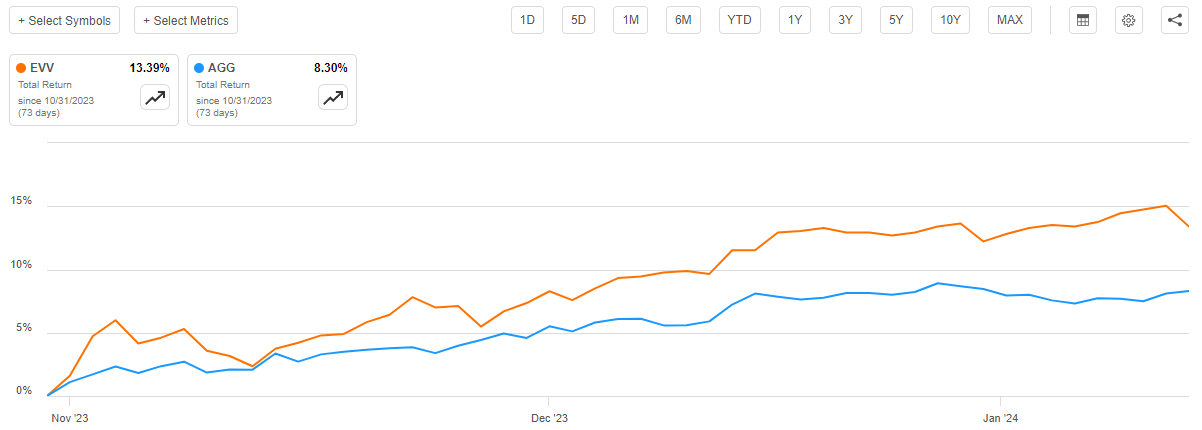

As is usually the case with closed-end funds, a simple look at the price action does not tell the whole story. This is because these funds typically pay out a significant proportion of their investment profits to the shareholders in the form of distributions. This tends to result in these funds having very high yields which means that investors in the fund typically do much better than the share price performance would indicate. As such, we need to incorporate the distributions paid by a fund into an analysis of its performance in order to see how investors actually did. When we do that, we see that investors in this fund increased their wealth by 13.39% over the past ten weeks or so. That is likewise much better than the Bloomberg U.S. Aggregate Bond Index managed to deliver:

{kind=link}

This is certainly going to appeal to most investors today. However, as regular readers are no doubt well aware, I have been warning about the risks inherent in bond funds right now as the market has probably gone too far in its attempts to front-run the Federal Reserve's pivot. That belief was reinforced by comments made by one of the members of the Federal Reserve's Board of Governors. His full speech is available at the link, but to put his comments succinctly, the market is wrong about the Federal Reserve's pivot and there is no reason to expect rate cuts within the next several months.

That scenario could lead this fund to give up some of its recent gains, and indeed we are already starting to see it. However, for reasons that we will see later in this article, this fund may be somewhat less affected by a failure by the Federal Reserve to start reducing rates in March as most of the other bond funds in the market. As such, I am not going to downgrade it at this time, but it is important that investors who are either long or considering this fund realize that it will probably underperform a pure senior loan fund over the next few months. It is probably a good idea that investors maintain some exposure to assets that may benefit from a rate cut in the unlikely event that something happens and forces a rate cut, and this fund looks like it might be one of the better ways to accomplish that.

About The Fund

According to the fund's website , the Eaton Vance Limited Duration Income Fund has the primary objective of providing its investors with a very high level of current income. Unfortunately, the website does not provide any information about the fund's strategy to achieve that objective. CEF Connect does provide a very basic description of the fund, though:

The Fund's investment objective is to provide a high level of current income. The Fund may, as a secondary objective, also seek capital appreciation to the extent consistent with its primary goal of high current income. Under normal market conditions, the Fund expects to maintain an average duration of no more than five years (including the effect of anticipated leverage).

It is very common for bond funds to state the provision of both current income and capital appreciation as primary and secondary objectives respectively. This is despite the fact that bonds do not provide any net capital gains over their lifetimes because investors receive the face value at maturity just as they paid the face value to obtain the bond in the first place. Although the description provided by CEF Connect does not actually state that this is a bond fund, the fund's asset allocation makes it immediately obvious. As we can see here, 97.84% of the fund's assets are invested in bonds or debt securities. The remainder of the fund's assets are invested in cash alongside very small allocations to other securities:

CEF Connect

It is important to note that not all of the 97.84% "bond" allocation shown above is invested in traditional fixed-rate bonds. CEF Connect has a tendency to classify any debt security that does not have a convertible feature as a "bond" even if it is not what people think of when they picture a bond. For example, collateralized loan obligations, senior leveraged loans, structured credit instruments, and similar things are classified as bonds even though these are not fixed-rate coupon-bearing instruments issued by a company or government. This fund does contain a few of these exotic instruments, as the fact sheet points out:

Fund Fact Sheet

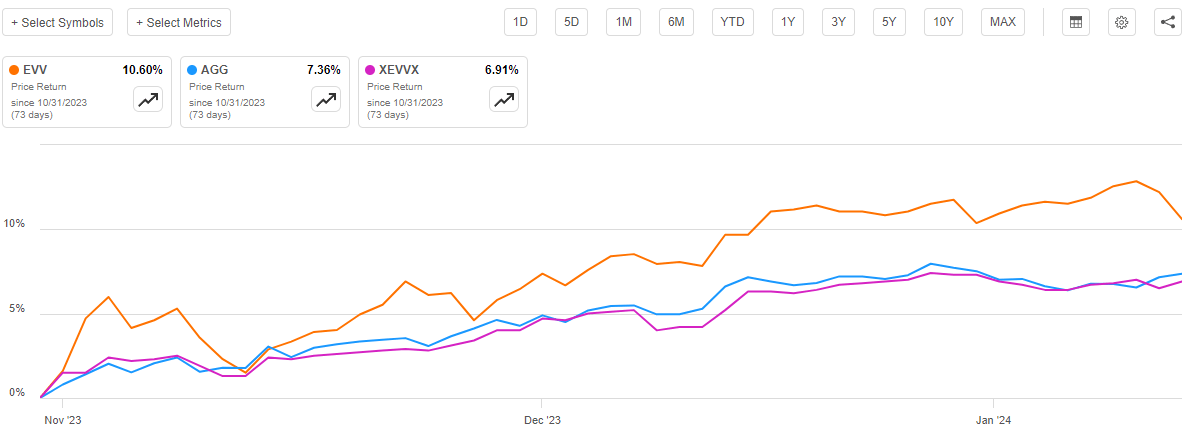

We immediately see that 34.50% of the fund's assets are invested in senior loans. These have very different characteristics from ordinary bonds due to the fact that their coupons pay a variable interest rate. As I explained in a previous article , this variable rate ensures that these securities will always have a competitive interest rate to other securities with similar characteristics so they do not experience the price fluctuations that other debt securities do when interest rates change. The presence of these securities is one of this fund's biggest advantages over other bond funds in the market today. This is because these assets should not be affected very much regardless of what the Federal Reserve actually does with respect to interest rates. As they account for over a third of the portfolio, the fund's net asset value should decline much less than it would if the fund were entirely invested in ordinary bonds. Of course, there is also a downside to this protection, as the fund's net asset value will not increase as much in a falling interest rate environment as it would if this fund were entirely invested in fixed-rate bonds. We can actually see this by looking at the fund's net asset value performance. As we can see here, the fund's net asset value is only up 6.91% since the last time that we discussed the fund:

{kind=link}

Thus, the fund's portfolio itself actually underperformed both its share price and the Bloomberg U.S. Aggregate Bond Index. This could poke a bit of a hole in the thesis, as the fact that the shares outperformed the underlying assets of the fund in anticipation of rate cuts could ultimately result in the shares declining when those rate cuts fail to materialize even if the portfolio itself holds up okay. We will take a look at this later in this article, as this situation strongly suggests that it will be critical not to purchase the shares of the fund unless they can be obtained at a discount on net asset value.

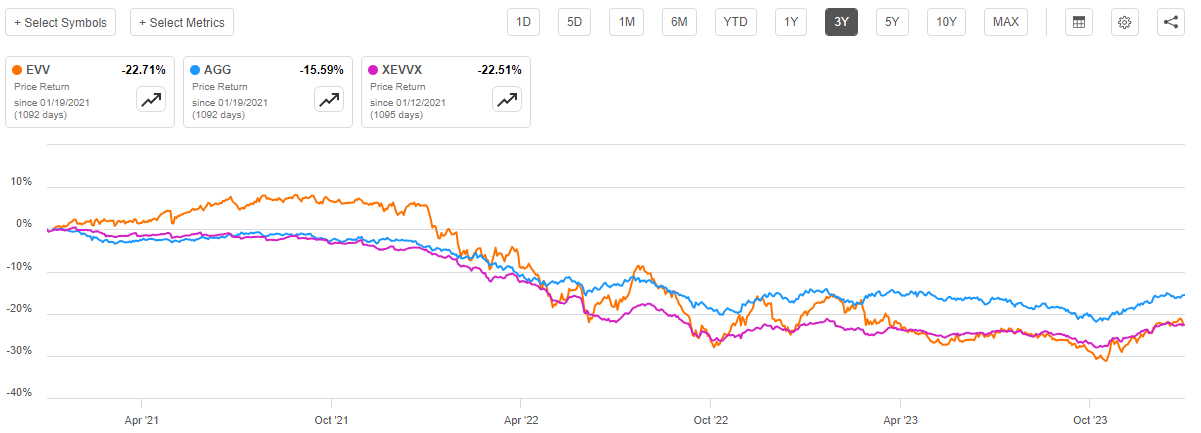

Another thing that this fund has going for it is that it specifically aims to have an average duration of less than five years. This is less than the 6.11-year duration of the Bloomberg U.S. Aggregate Bond Index so overall it means that the Eaton Vance Limited Duration Income Fund is attempting to have a lower average duration than the bond market overall. Duration is a measure of an asset's sensitivity to interest rates. Generally speaking, a bond with a short duration should decline less than one with a high duration when interest rates increase and vice versa. As such, we should expect that this fund will prove to be somewhat more stable than an ordinary bond fund when interest rates change. In practice, that is not exactly true, as we can see by looking at the fund's performance over the past three years:

{kind=link}

As we can see here, the shares of the Eaton Vance Limited Duration Income Fund (orange line) and its net asset value per share (purple line) were both more heavily impacted by the reversal of the Federal Reserve's longstanding loose monetary policy in 2022 than the Bloomberg U.S. Aggregate Bond Index. This fund did decline more than the index did during that event, although otherwise, it does not really appear that the fund's net asset value is more volatile than the index. The fund's shares most certainly are though, and this is something to keep in mind when purchasing this fund. That was mentioned earlier.

It is probable that the fund's leverage is responsible for its larger decline over the three-year period relative to the index. The incredibly low-interest rate environment that dominated most of the past twenty years or so, unfortunately, forced most bond funds to take on substantial amounts of leverage to deliver reasonable yields to investors. That same leverage then amplified the fund's losses in 2022 when the Federal Reserve began returning to a more historically normal federal funds level. If the fund did not have this leverage, it seems likely that it would have outperformed the aggregate bond index due to the lower interest-rate sensitivity of the assets in its portfolio. This, unfortunately, presents another risk to the thesis that this fund should hold up better than a typical bond fund if the Federal Reserve does fail to reduce rates to the degree that the market expects. However, this fund should still manage to hold up better than other leveraged bond closed-end funds in such an event.

Optimism About Interest Rates May Be Overblown

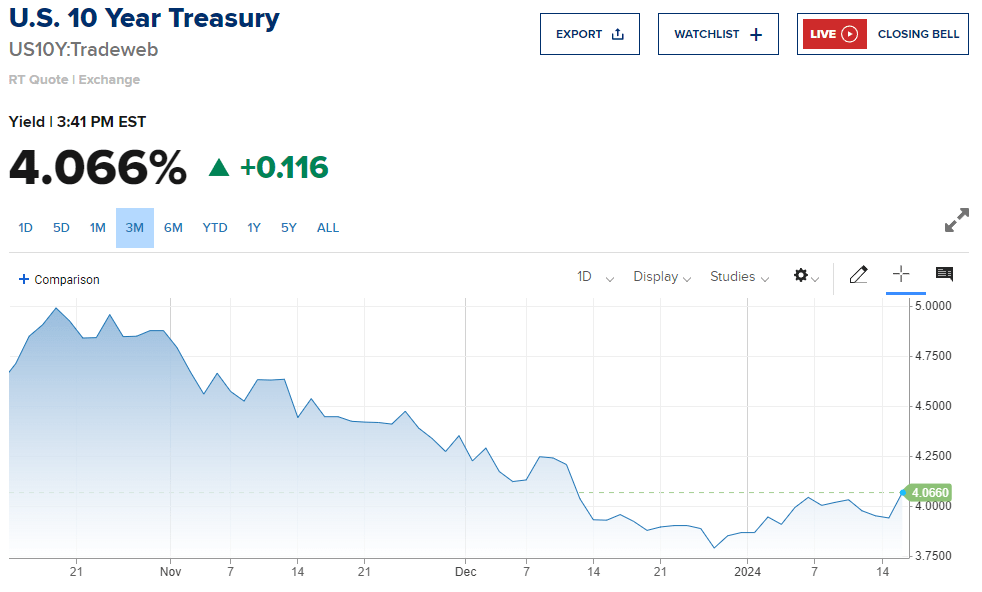

As I have mentioned a number of times both in this article and in past ones, the biggest reason for the massive rally in the stock and bond markets that has occurred since mid-October is an expectation that the Federal Reserve will rapidly reduce interest rates over the course of 2024. As of right now, the fed funds futures market anticipates six-and-a-half 25-basis point cuts between now and the end of December 2024. The market has priced bonds accordingly, which we can see in the fact that the market has bid up ten-year U.S. Treasury bonds so that their yield has dropped from 4.9880% to 4.066% over a roughly three-month period:

{kind=link}

In order for the market to be correct about its rate predictions, the Federal Reserve will have to cut the federal funds rate at every single meeting of the Federal Open Market Committee this year, starting with the one in March. That seems highly unlikely, which Federal Reserve Governor Chris Waller pointed out in a speech at the Brookings Institute. The speech itself is linked in the introduction to this article. One of the quotes is particularly telling, however:

When the time is right to begin lowering rates, I believe it can and should be lowered methodically and carefully.

With economic activity and labor markets in good shape and inflation coming down gradually to 2%, I see no reason to move as quickly and as rapidly as in the past.

Mr. Waller also reaffirmed the central bank's prediction from December that a maximum of three rate cuts would be appropriate this year, with the first coming in the second half of the year. That is nowhere near the market's expectations, and it is the reason why bond yields spiked in today's trading session. It is also why shares of the Eaton Vance Limited Duration Income Fund are down today. However, by most indications, the market is still far too optimistic about rate cuts, and it seems very likely that further losses will be coming for both stock and bond investors if Mr. Waller's statements are reflective of what the Federal Reserve's actions are likely to be.

There are more speakers from the Federal Reserve scheduled to speak this week, and if their statements are similar to Mr. Waller's then it seems likely that more losses are possible for this fund over the next few days. However, the lower duration of the fund's assets relative to other bond-focused closed-end funds should still allow its net asset value to hold up somewhat better than other funds. There is some downside risk to the shares, however, given their recent outperformance relative to the underlying portfolio.

Despite the potential for near-term declines, investors who already hold this fund might not want to sell out of it. As I mentioned in a recent article , there are some signs of stress in the repo money market. That stress could prompt the Federal Reserve to loosen monetary policy or even cut interest rates sooner than it really wants to. As such, it might be a good idea to hold onto this fund rather than exchange it for a pure senior loan fund, as this fund should outperform a floating-rate fund in such an event. Thus, it can be thought of as a way to hedge your bets.

Leverage

As was briefly discussed earlier, the Eaton Vance Limited Duration Income Fund employs leverage as a method of boosting the effective yield of its assets. I discussed how this works in my previous article on this fund:

Basically, the fund borrows money and then uses those borrowed funds to purchase bonds and other income-producing securities. As long as the purchased assets have a higher yield than the interest rate that the fund has to pay on the borrowed money, the strategy works pretty well to boost the effective yield of the portfolio. As this fund is capable of borrowing money at institutional rates, which are considerably lower than retail rates, that will usually be the case.

However, the use of debt in this fashion is a double-edged sword. This is because leverage boosts both gains and losses. As such, we want to ensure that the fund is not using too much leverage since that would expose us to excessive amounts of risk. I do not typically like to see a fund's leverage exceed a third as a percentage of its assets for that reason.

As of the time of writing, the Eaton Vance Limited Duration Income Fund has leveraged assets comprising 30.70% of its portfolio. This is less than the 31.42% leverage that the fund had the last time that we discussed it, which is not surprising. As we have already seen, the fund's net asset value has increased somewhat over the past three months, so the leverage naturally represents a smaller percentage of the fund's total assets. The fund has not been increasing its leverage as its net asset value has gone up, which is quite nice to see.

This fund has a lower level of leverage than many other closed-end debt funds. When we consider that its assets should be relatively less volatile than ordinary bonds, the fund should be able to carry somewhat higher levels of leverage than peers. As this fund is less leveraged, we should not need to worry too much about its use of leverage. This fund will lose a bit more than it would in the absence of leverage if our thesis about the Federal Reserve's future actions is correct, however.

Distribution Analysis

As mentioned earlier in this article, the Eaton Vance Limited Duration Income Fund has the primary objective of providing its investors with a very high level of current income. In pursuance of this objective, the fund invests primarily in leveraged loans and junk bonds, but there are other fixed-income assets in its portfolio as well. As is the case with all debt securities, these assets deliver the majority of their investment returns in the form of direct payments to their owners, which in this case is the fund. The inverted yield curve has resulted in the fund's focus on short-duration assets being a higher-yielding strategy than the one that is employed by a typical bond fund, which results in this fund having a higher income than we might expect. It even takes things a step further and borrows money that it uses to collect payments from more securities than it could purchase solely using its own equity capital. That effectively boosts the yield that the fund receives from its equity capital. It collects all of the payments that it receives from the bonds and debt securities in its portfolio and pays them out to its shareholders after it deducts its expenses from the total. This can be expected to give the fund's shares a fairly high yield.

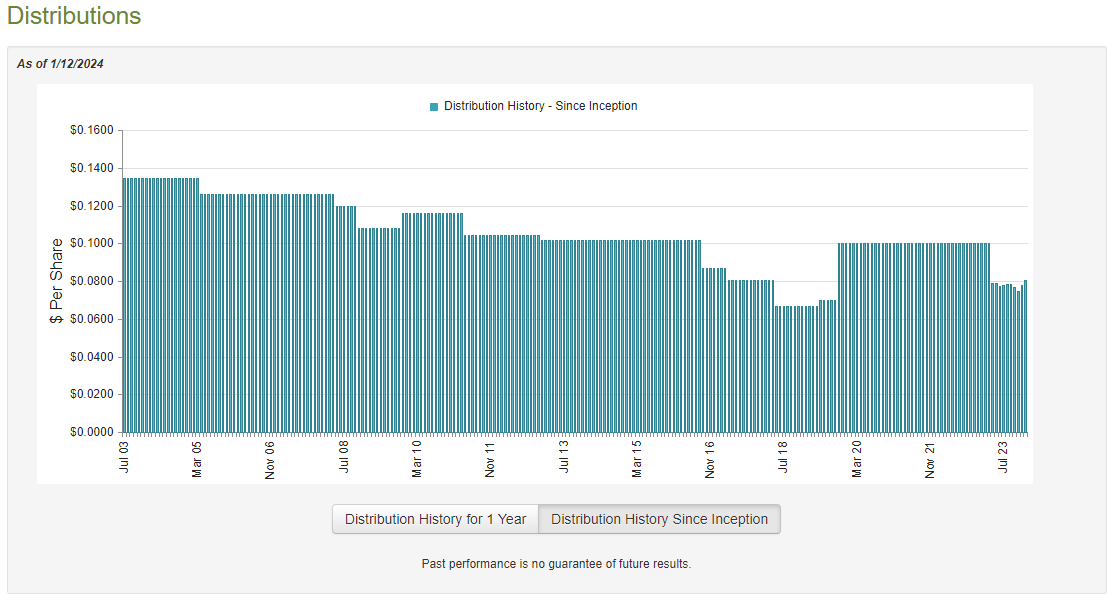

This is indeed the case as the Eaton Vance Limited Duration Income Fund currently pays a monthly distribution of $0.0803 per share ($0.9636 per share annually), which gives it a 10.04% yield at the current price. As mentioned in the introduction, this is a very respectable yield that compares very well to many other fixed-income closed-end funds. Unfortunately, the fund has not been especially consistent with respect to its distribution over the years. In fact, as we can see here, the fund has both raised and reduced its distribution multiple times over its history:

{kind=link}

The fact that the fund's distribution has varied quite a bit over its history might be a bit of a turn-off for those investors who are seeking to receive a safe and consistent level of income from the assets in their portfolios. However, it does make sense considering that the fund's income is fairly sensitive to interest rates. After all, the securities in the fund do not deliver the same price appreciation when interest rates decline, so the fund is a bit more dependent on coupon payments than some other bond funds. This is not a hard rule though, as the fund was able to boost its distribution during the post-pandemic period when interest rates were zero. However, we can still expect interest rates to play a role in the fund's ability to generate income and it is the fund's investment returns that determine the amount of money that it can pay out to the shareholders.

As I have pointed out numerous times in the past though, the fund's distribution history is not necessarily the most important thing for anyone who is considering buying the fund today. This is because a new investor will receive the current distribution at the current yield and will not be affected by any actions that it took in the past. As such, the most important thing for us today is how well the fund can sustain its current distribution. Let us investigate this.

Fortunately, we have a very recent document that we can consult for the purpose of our analysis. As of the time of writing, the fund's most recent financial report corresponds to the six-month period that ended on September 30, 2023. This is a newer report than the one that we had available to us the last time that we discussed this fund, which is quite nice to see. This report should give us a good idea of how well this fund weathered the challenging environment for most fixed-income securities that existed during the summer of 2023. During that period, long-term interest rates were rising, and bonds were generally declining in price. That naturally caused many fixed-income funds to suffer losses. This report will give us a good idea of how well this one managed to protect its portfolio value.

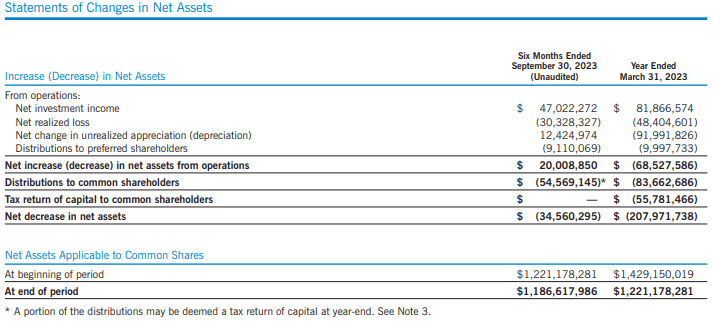

During the six-month period, the Eaton Vance Limited Duration Income Fund received $1,868,950 in dividends and $63,253,214 in interest from the assets in its portfolio. When we combine this with a small amount of income from other sources, we see that the fund had a total investment income of $65,465,860 during the period. It paid its expenses out of this amount, which left it with $47,022,272 available for shareholders. That was, unfortunately, not enough to cover the $54,569,145 that the fund paid out in distributions during the period. It did manage to get reasonably close to fully covering its distribution out of net investment income, however.

There are other ways through which the fund can obtain the money that it needs to cover its distributions. For example, it might be able to exploit the changes in bond prices that accompany interest rate movements to make some trading profits. The fund unfortunately failed at this task during the period. It reported net realized losses of $30,328,327 which was partially offset by $12,424,974 net unrealized gains. Overall, the fund's net assets declined by $34,560,295 after accounting for all inflows and outflows during the period.

This is certainly concerning, as the latest report points to the fund failing to cover its distributions for eighteen straight months.

{kind=link}

A fund cannot indefinitely sustain net asset value declines because these declines increase the return that the fund needs to earn in order to pay out a steady distribution. As everyone reading this is no doubt well aware, the larger the needed return the more difficult it is to achieve. This could point to the possibility of a distribution cut in the future if the fund cannot reverse the net asset value destruction that we see here.

Valuation

As of January 12, 2024 (the most recent date for which data is currently available), the Eaton Vance Limited Duration Income Fund has a net asset value of $10.67 per share but the shares currently trade for $9.52 each. This gives the fund's shares a 10.78% discount on net asset value at the current price. This is in line with the 10.55% discount that the shares have had on average over the past month.

This suggests that the shares are not overpriced relative to the fund's portfolio. That is very nice to see considering that the fund's shares have substantially outperformed the underlying assets over the past few months.

Conclusion

In conclusion, the Eaton Vance Limited Duration Income Fund could be a reasonable way to maintain some exposure to falling interest rates while limiting your risk if the Federal Reserve disappoints the market. There is a very real possibility that the market will be proven wrong, which will punish bonds. This fund's shares will undoubtedly decline but it should hold up better than many other bond funds. If for some reason something breaks in the money market and the central bank does start rapidly easing conditions, this fund will benefit. As such, I am inclined to maintain a hold rating on this fund, although investors should be prepared to experience some near-term share price declines.

For further details see:

EVV: Near-Term Share Price Declines Likely, But Remains A Hold