SSNLF - EWY ETF: Not A Perfect Product But Well-Positioned To Pick Up Steam (Rating Upgrade)

2023-11-23 07:48:13 ET

Summary

- EWY is a popular way to play South Korean equities, but we pick out a few structural flaws in relation to its next biggest peer - FLKR.

- Korean macros are convalescing well, and the recent pick-up in exports bodes well.

- The Korean government is taking steps to make the Won more attractive.

- Given the earnings potential on offer, valuations look very compelling.

- The risk-reward on the charts is another reason to get on board.

EWY vs. FLKR

Investors looking for unleveraged ETF access to South Korea-based equity portfolios currently have around 3 options to choose from; one of those options is the iShares MSCI South Korea ETF ( EWY ), a stalwart in this space, with a 23-year-old history, and close to $4bn in AUM.

EWY, is no doubt, very popular, and this can be gleaned from the superior daily dollar volumes witnessed in this counter, relative to the next biggest offering - the Franklin FTSE South Korea ETF ( FLKR ). For context, EWY's average daily volumes of over $200m, are over 100x greater than what FLKR generates.

As a result, EWY is often also seen as the preferred haven for short-sellers to get on board. Note that as things stand, over 11% of EWY's shares outstanding are currently short. In contrast, FLKR's short interest share is rather minuscule at less than 0.1%.

Where FLKR offers an edge is with regard to its efficiency, its stability, and its dividend profile. Firstly, the cost differential is rather massive; FLKR's expense ratio of just 0.09% is 6x lower than EWY's corresponding figure.

Then, FLKR is also less susceptible to churn offering investors the opportunity to ride with these equities across different cyclical swings. EWY's annual turnover ratio of nearly 30%, is 6x higher than FLKR's corresponding figure.

Then EWY's dividend profile is not the greatest; it pays dividends on an annual basis, but the outflows have actually declined by - 19% CAGR over the past 3 years. Conversely, FLKR distributes dividends twice a year (semi-annual divis can always be reinvested in other high-yield arenas if possible), and it has also grown its dividends at a healthy pace of +21% CAGR during the last 3 years. The inferior dividend outflows of EWY translate to a rather underwhelming yield of a little over 1%; in contrast, FLKR offers a yield that is over 3x larger than EWY at 3.27%!

Macro Considerations

South Korean macros haven't been tip-top, but they appear to be convalescing well, and we could be staring at a much better backdrop in FY24.

{kind=link}

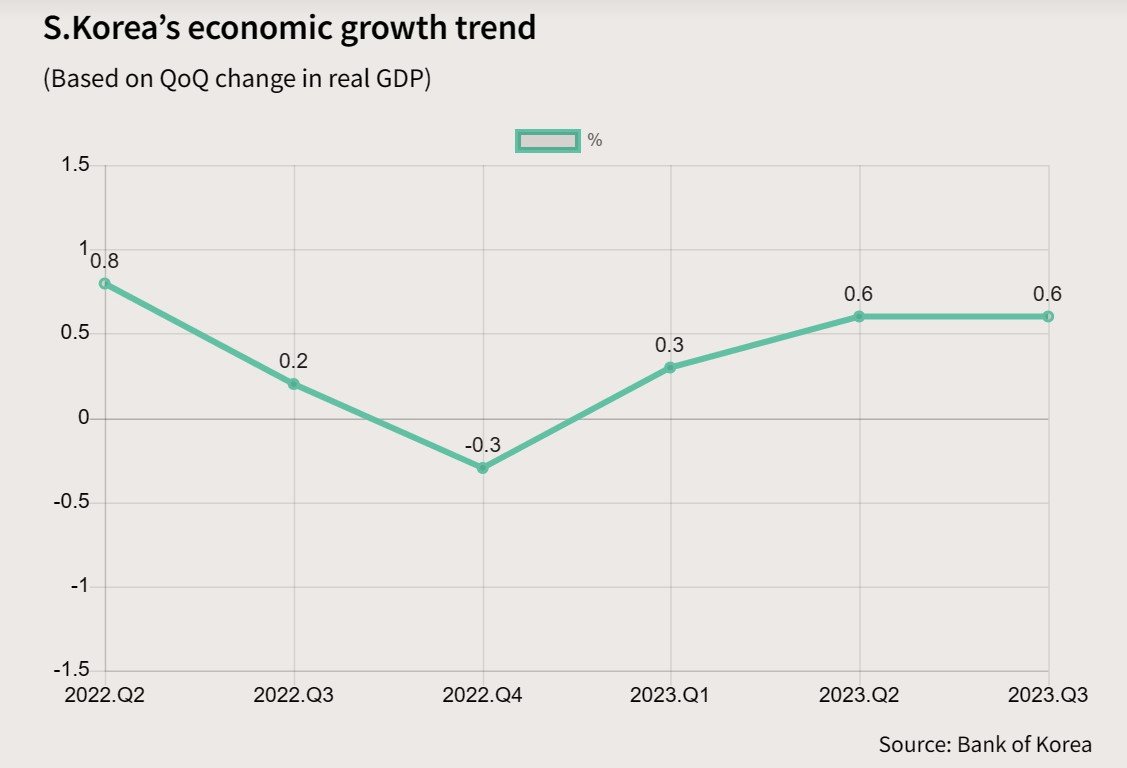

After a -0.3% QoQ slump last year, growth has quietly crept up in the subsequent periods with the pace of quarterly progress (0.6%) being maintained recently in Q3 as well. The expectation now is that GDP could improve even further by 0.7%, taking the FY GDP growth rate to 1.4%. Admittedly a 1.4% growth cadence is nothing to shout home about, particularly when you consider that the economy was previously growing at 3% p.a. on average, during the pre-pandemic phase (between 2005-2019). However, do also note that next year's growth forecast looks a lot healthier, with the IMF now expecting the economy to grow at a pace of 2.2% .

The chief driver of the economic improvement will most certainly be the country's exports. After 13 months of decline, export growth came in at 5% in October, and it appears that November too shall witness positive growth as the country's major export item- semiconductors appear to be witnessing decent momentum. Despite having fewer working days, for the first 20 days of this month, we've seen semiconductor sales improve by 2.4%. Improved trade dynamics will also reflect well on the likes of Samsung Electronics Co., Ltd. ( OTCPK:SSNLF ), and SK Hynix which jointly dominate EWY's portfolio with a 30% stake. In fairness, during their respective earnings events, the management of both companies had already flagged improved prospects of the memory market from Q4 itself. The adverse inventory adjustments at the customers' end have now normalized, and next year the PC and smartphone segments will also benefit from increased replacement demand for products sold at the start of the pandemic.

We also think the Korean regulatory authorities deserve a pat on the back for taking steps to improve the attractiveness of Korean Won-denominated assets. The authorities are looking to make the Korean won onshore market more accessible for foreign institutions, and that should certainly help boost the liquidity of the currency and bring down the volatility associated with what is essentially a risk-on currency. The impact of this will likely be felt from H2-24.

Closing Thoughts - Technical and Valuation Considerations

As implied in the initial section of this article, EWY suffers from some structural flaws relative to its next biggest peer- FLKR. However, if you're willing to overlook those deficiencies, and still go ahead with this option, do note that the risk-reward on the charts, and the valuation quotient of EWY looks rather healthy at this juncture.

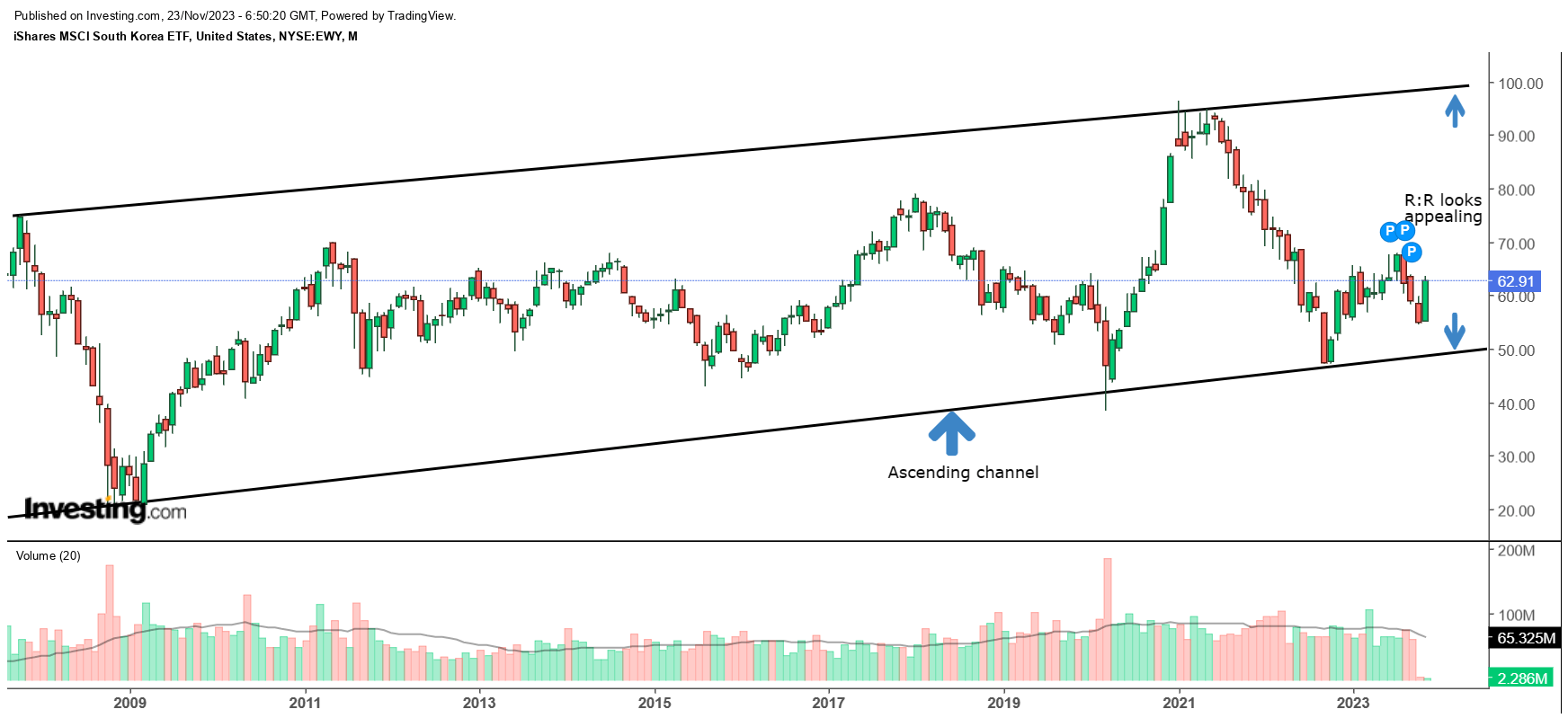

EWY's long-term monthly charts tell us that this is a product that has been leaving price imprints in the shape of an ascending channel. The boundaries of the channel appear to roughly hover around the $50 and $100 levels as things stand. Thus, given where the price is now at ($63 levels), you're essentially looking at a solid reward to risk of almost 3x

{kind=link}

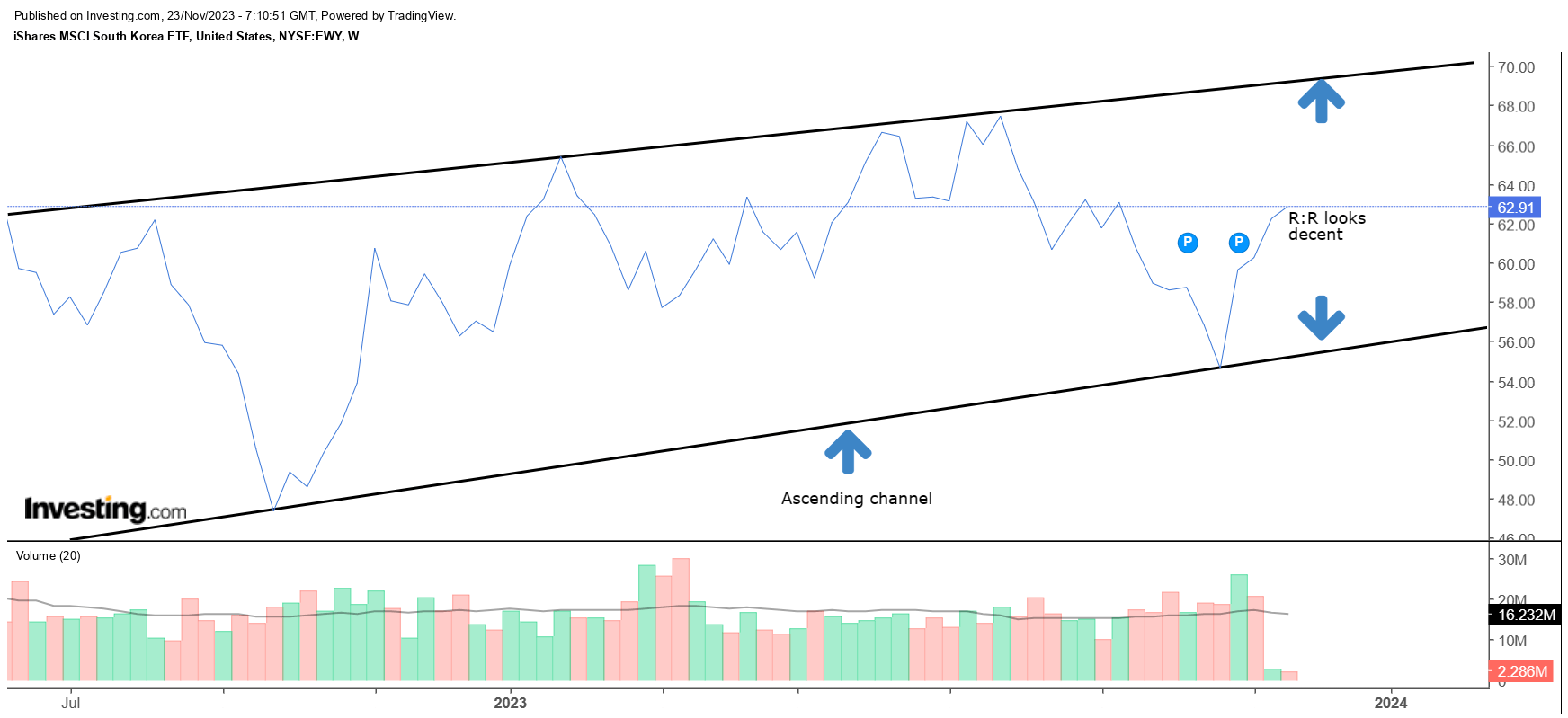

Now perhaps, you don't have such a long investment horizon, and you prefer to make tactical bets across a shorter time horizon. Well, in that case, one may switch over to the weekly chart. Even here, what we can see is that over the last 15 months, EWY has been trending up in the shape of an ascending channel, and given where the two boundaries currently are ($70 and $57), you're still looking at a decent reward to risk equation (albeit not as much as the monthly chart).

{kind=link}

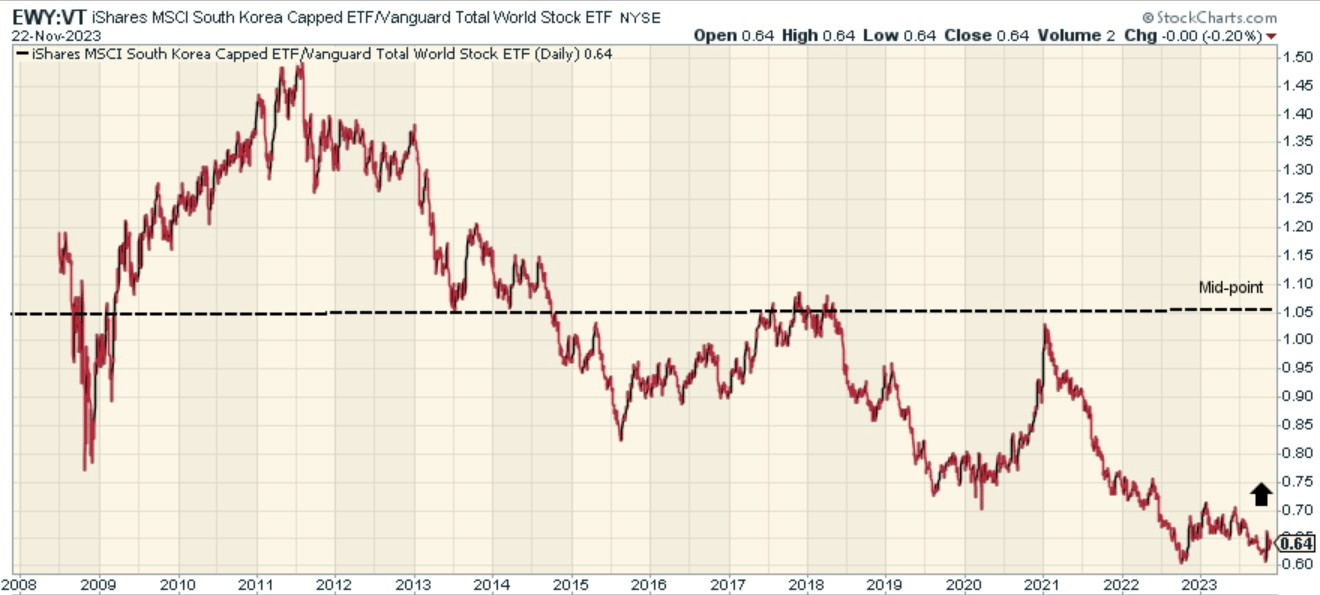

We'd also like to think that those fishing for suitable mean-reversion opportunities across the globe, could likely have South Korean equities on their wishlist. Note that EWY's relative strength versus a portfolio of global stocks is currently at rather low levels and around 40% off the mid-point of its long-term range.

{kind=link}

We also think EWY could garner further interest as the valuation to long-term earnings tradeoff looks remarkably attractive. As per Morningstar data, EWY is currently only priced at 9x price to earnings, yet it offers a healthy long-term earnings potential of 18%, implying a PEG of just 0.5x. Meanwhile, global stocks, as represented by the Vanguard Total World Stock Index Fund ETF Shares ( VT ) are priced at 14.3x and only offer long-term earnings growth of 10%.

To conclude, despite a few structural drawbacks of this product, we think EWY could represent a good BUY at these levels.

For further details see:

EWY ETF: Not A Perfect Product, But Well-Positioned To Pick Up Steam (Rating Upgrade)