RILYM - Exchange-Traded Fixed-Income Portfolio Performance

Summary

- In June 2022, I published an article about the upcoming opportunity in fixed income, specifically baby bonds and fixed to floating-rate preferred shares.

- In July 2022, I published a second article with roughly 100 candidate baby bond and preferred shares for investment in a rising rate environment.

- Though the Federal Reserve is still raising short rates and allowing longer-duration securities to roll off its books (Quantitative Tightening), we are approaching a terminal rate and future opportunities.

- This article provides a summary of the performance of the exchange-traded fixed-income investments I made based on the June and July articles.

- This article also provides a list of candidate securities for future investment, depending on how aggressive the Federal Reserve gets at the end of this rate increase cycle.

Introduction

We had a very long bull market in bonds, culminating in the lowest interest rates we've had in the U.S. since the early 1960s. For several years, fixed-income assets (bonds, baby bonds, CDs, and preferred shares) were practically uninvestable. This most recent bout of inflation that resulted from shutting down the global economy due to COVID, disruption of the manufacturing and commodity supply chains, and over-stimulating the economy with stimulus dollars did a great deal of damage to prices of everyday goods and services. However, it also set the stage for a dramatic increase in interest rates engineered by the Federal Reserve through increases in the Federal Funds rate and Quantitative Tightening ((QT)).

The accelerated increase in interest rates has made fixed-income ((FI)) securities attractive again after nearly a decade of low and unattractive returns. The future opportunity in FI securities became fairly obvious by June 2022, and a few authors on Seeking Alpha increased their coverage on the approaching opportunity in FI securities. I published my first article on the subject in June and my second article in July. Today's article provides a summary of the performance of the exchange-traded components of the FI portfolio I built following the publication of those two articles and provides a list of those FI securities I have retained on my watch list for potential future investment.

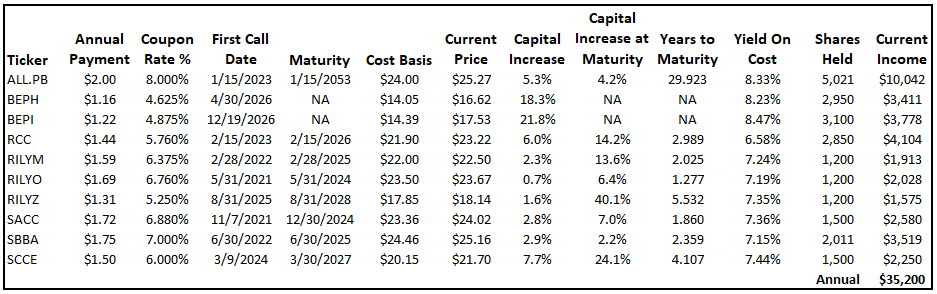

Baby Bond Portfolio Performance

To date, I have invested in the 10 baby bonds listed in the table below. The table provides a performance summary in terms of the average cost basis for each position, the capital increase (no losses) to date, the yield on my cost basis, as well as the current annual income each position generates.

{kind=link}

Readers will note the current capital increase, with the exception of BEPH and BEPI are modest at <8%. Aside from BEPH, BEPI, and ALL.PB, the longest maturity in the group, RILYZ, is only 5.5 years, by which time all seven of the short maturity securities in this portfolio will have been redeemed at their $25 par value, with several securities providing double-digit capital increases. I do plan to hold these baby bonds to maturity.

Readers will also note that I have calculated a yield on my cost of shares for each security. In previous article comments, a few bond purists have taken issue with my use of yield on cost. My position is that this spreadsheet is for my use and I use the yield on cost when evaluating potential swaps into other baby bonds. I also use a yield to maturity calculation in my swap evaluations but chose not to show that in this article.

The Federal Reserve has stated that we are very likely to see additional increases to the Federal Funds Rate ((FFR)) in their effort to tame inflation back down to 2% or less. So, as I noted above, the Federal Reserve is likely not yet done, and I expect to see at least two more 25 bps increases to the FFR before June 2023. This may result in reducing the valuation of those baby bonds in which I've invested and erosion of the current capital increase in the table above. If that happens, I will be looking to add to my current holdings. I may add to my RILYO position in the near term, and I am always looking for new potential FI investments.

This question/issue is likely to come up in the comments posted on SA, so I'll take a shot at preempting the discussion. B. Riley Financial ( RILY ) is currently the subject of a short report put out by WolfPack Research. I've read the entire report, found it to be a rather amateurish piece with assertions and conclusions supported by less than full facts/disclosures. Rida Morwa published a fairly detailed article on SA with similar conclusions to mine. While RILY does invest in distressed businesses and is probably not a sleep well at night ("SWAN") holding, the RILY baby bonds which I hold (as does Rida) are higher in the capital stack and fairly well insulated against Riley's cyclical business risks.

Finally, a word about BEPH and BEPI, which are baby bonds of Brookfield Renewable Partners L.P. (BEP), a Bermuda-based MLP. I have not yet received my 1099-DIV from Vanguard for definitive confirmation, but I have done the due diligence to understand that, because BEPI and BEPH are interest-paying bonds, there is no K-1 reporting. In addition, there is no foreign withholding tax on foreign corporation dividends and interest payments for securities held in qualified U.S. retirement plans (e.g., IRAs). Lastly, BEP does not generate UBTI.

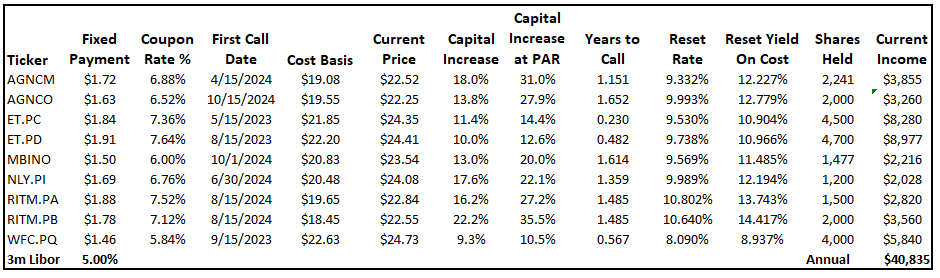

Fixed to Floating Preferred Stock Portfolio Performance

I have invested in 9 different preferred shares to date as listed in the table below. The table provides a performance summary in terms of the average cost basis for each position, the capital increase (no losses) to date, the yield on my cost basis, as well as the current annual income each position generates.

{kind=link}

Readers should note that my preferred share capital increase to date is much higher than for the baby bond portfolio. All are in the double digits except for WFC.PQ at 9.3%. I attribute this to two differences between the baby bonds I hold versus the preferred shares. Most preferred stock and all of those issues I hold are perpetual; they do not have a maturity date. Because they have no maturity, they behave like very long-term bonds. Long-term rates have dropped significantly from their late October highs, putting upward pressure on long-term FI valuations (strongly inverted yield curve). Secondly, all of the preferred stocks listed in the table above are fixed to floating ((FTF)) rate issues with near-term conversions, 1.65 years being the latest conversion to floating rate. In all cases, the floating reference rate (base rate) is the 3 month LIBOR, currently 4.87%. With the Federal Reserve now pushing higher for longer on the FFR, we are likely to have the 3 month LIBOR, and its SOFR successor, in the range of 4.25 to 5.25% at the first rate reset for these preferred shares. Typically, higher interest rates are viewed as putting downward pressure on long-term FI securities. For these fixed to floating rate shares, the coupon rate will reset higher at conversion, putting upward pressure on the share valuations.

I may not hold the preferred shares long term as it will depend on what the Fed does with interest rates if/when inflation has returned to the 2% or less target. Fixed to floating rate conversions are your best friend when rates are strongly rising but turn into your worst enemy when rates are strongly falling.

I do have a handful of preferred shares for potential future investment, most of which are also fixed to floating rate issues. Future investments will depend on Fed actions with the FFR and QT as well as any major market dislocations (e.g., economic hard landing). My list of potential preferred share future investments include the following issues.

- ET.PE - FTF conversion 5/15/2024 at 3 month LIBOR + 5.161%

- MITT.PC - FTF conversion 9/17/2024 at 3 month LIBOR + 6.476%

- RITM.PC - FTF conversion 2/15/2025 at 3 month LIBOR + 4.969%

- RITM.PD - FTF conversion 11/15/2026 at 5 yr Treasury + 6.223%

- TWO.PC - FTF conversion 1/27/2025 at 3 month LIBOR + 5.011%

AG Mortgage Trust ( MITT ) is a lower quality (higher risk) holding that I have only recently added to my watch list. I'll be watching to see how MITT weathers this cycle of higher rates and the potential resulting dislocations in residential real estate loans.

Conclusion

I'm pleased with the performance of the baby bond holdings I've accumulated since late summer. The $35,200 annual income is pretty easy to like, and at maturity I'll get my cost basis plus a capital gain. I've limited my duration risk by choosing bonds with near-term maturities, and for those with longer maturities (BEPH, BEPI, and ALL.PB), I've chosen bonds with investment grade credit ratings.

I'm more pleased with the performance of the FTF preferred stocks I've accumulated. The $40,835 annual income the portfolio throws off is easy to like and my stream of dividends will either grow as the issues convert to floating rate or the issue will be called at its $25 par value, providing me with a double digit capital gain.

Given how well this has worked out, had I the opportunity of a do-over, I'd double or triple the capital investment I made in these FI securities.

For further details see:

Exchange-Traded Fixed-Income Portfolio Performance