XPRO - Expro Group Faces Revenue Headwinds As Activity Drops

2023-12-01 17:31:49 ET

Summary

- Expro Group Holdings N.V. reported Q3 2023 financial results below expectations, citing challenges in restarting its LWI segment and reduced drilling activity.

- The global market for oilfield services is projected to reach $346 billion by 2027, driven by increasing production needs and technological improvements.

- However, given the firm's particular challenges, I'm Neutral [Hold] on Expro Group Holdings shares in the near term.

A Quick Take On Expro Group Holdings

Expro Group Holdings N.V. ( XPRO ) reported its Q3 2023 financial results on October 26, 2023, missing both revenue and consensus earnings estimates.

The firm provides a range of oilfield services to exploration & production firms worldwide.

Given the challenges the company is facing in restarting its LWI segment, reduced drilling activity in North and Latin America and increasing competition in certain North American basins, I’m not optimistic about Expro’s growth trajectory in the near term.

My outlook on XPRO is, therefore, Neutral [Hold] at this time.

Expro Group Overview And Market

UK-based Expro Group was founded to provide a growing range of oilfield services on a global basis.

The firm is headed by Chief Executive Officer Mike Jardon, who joined the firm in 2011 after a career in various senior roles at Schlumberger, a major oilfield services company.

The company’s primary offerings include the following:

-

Well construction

-

Well intervention and integrity

-

Well flow management

-

Subsea well access

-

Geothermal solutions

-

Carbon capture and storage.

Expro acquires customers through its direct business development and marketing efforts.

According to a 2020 market research report by Fortune Business Insights, the global market for oilfield services of all types was estimated at $268 billion in 2019 and is forecasted to reach $346 billion by 2027.

This represents a forecast CAGR (Compound Annual Growth Rate) of 6.6% from 2020 to 2027.

The main drivers for this expected growth are increasing production needs by E&P firms and ongoing technological improvements in well-site services.

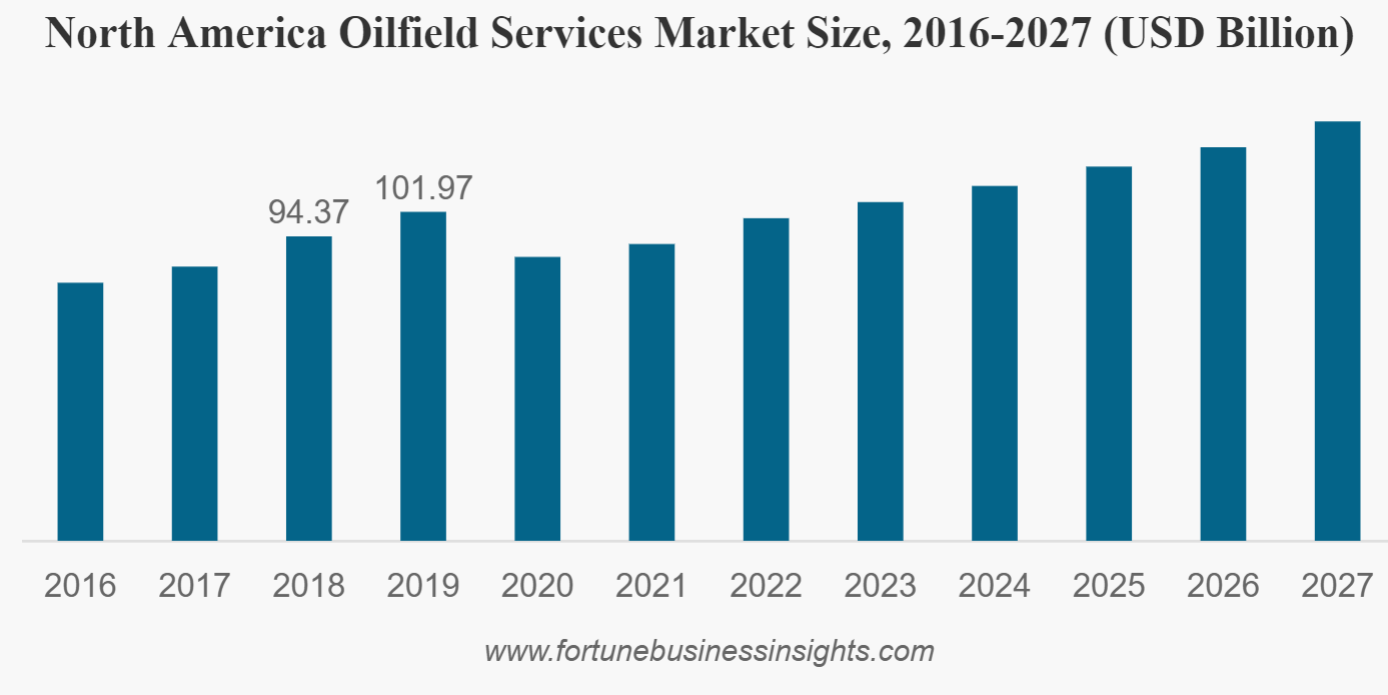

Also, the chart below shows the approximate historical and projected trajectory of the North American oilfield services market through 2027:

{kind=link}

Major competitive or other industry participants include:

-

Schlumberger

-

Halliburton

-

Baker Hughes

-

Weatherford.

Expro Group’s Recent Financial Trends

Total revenue by quarter (blue columns) has continued to rise year-over-year; Operating income by quarter (red line) has been reduced to just above breakeven:

Seeking Alpha

Gross profit margin by quarter (green line) has varied within a range without any discernible trend; Selling and G&A expenses as a percentage of total revenue by quarter (amber line) have remained flat at 4% in the last three quarters:

Seeking Alpha

Earnings per share (Diluted) have dropped into negative territory in Q3 2023:

Seeking Alpha

(All data in the above charts is GAAP.)

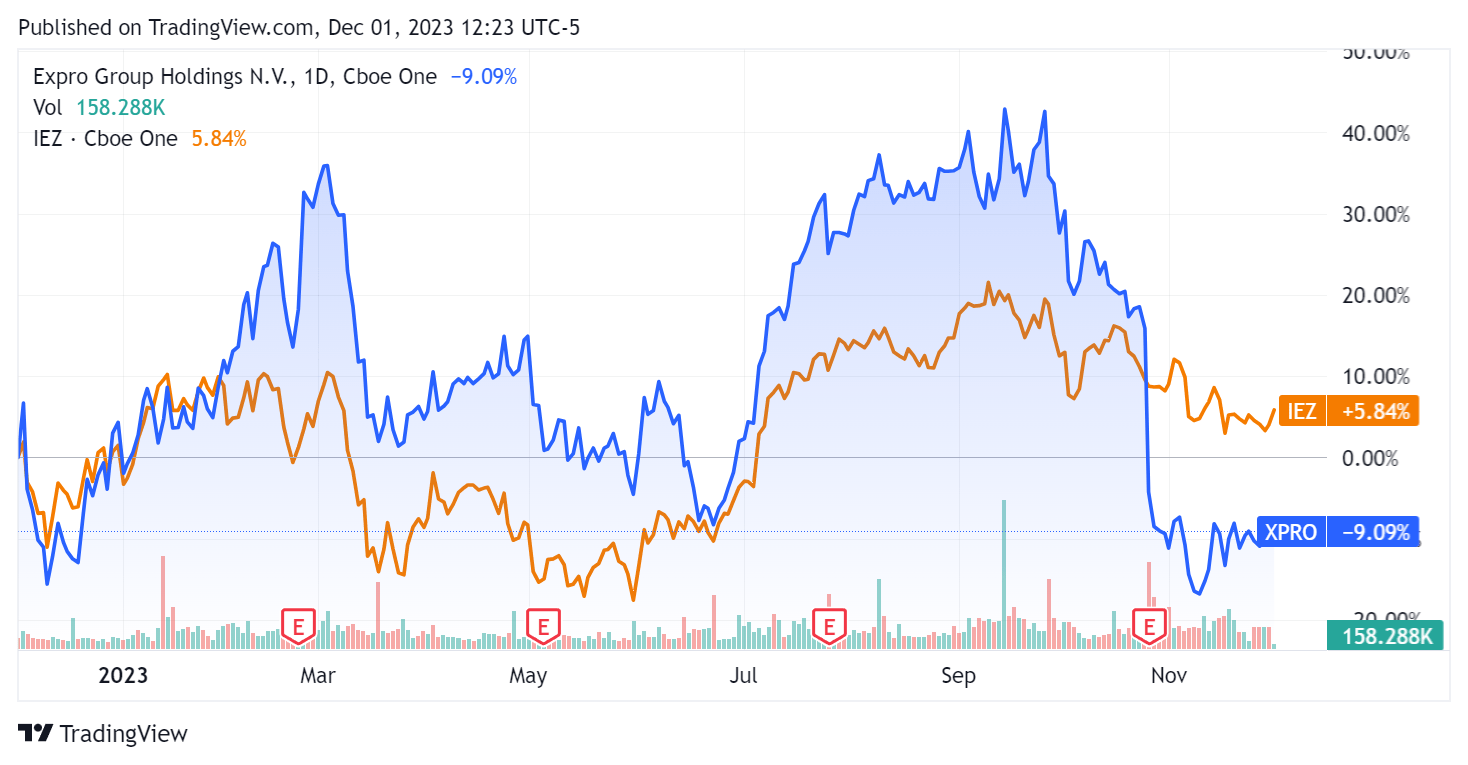

In the past 12 months, XPRO’s stock price has fallen 9.09% vs. that of the iShares U.S. Oil Equipment & Services ETF ( IEZ ) rise of 5.84%:

{kind=link}

For balance sheet results, the firm ended the quarter with $255.3 million in cash and equivalents and $50.0 million in total debt, all of which was categorized as long term.

Over the trailing twelve months, free cash flow was $82.6 million, during which capital expenditures were $115.9 million. The company paid $18.2 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Expro Group Holdings

Below is a table of relevant capitalization and valuation figures for the company:

| Measure (Trailing Twelve Months) |

| Amount |

| Enterprise Value / Sales |

| 1.1 |

| Enterprise Value / EBITDA |

| 8.1 |

| Price / Sales |

| 1.2 |

| Revenue Growth Rate |

| 19.0% |

| Net Income Margin |

| 14.0% |

| EBITDA % |

| 13.7% |

| Market Capitalization |

| $1,730,000,000 |

| Enterprise Value |

| $1,610,000,000 |

| Operating Cash Flow |

| $198,470,000 |

| Earnings Per Share (Fully Diluted) |

| $0.01 |

| Forward EPS Estimate |

| $1.14 |

| Free Cash Flow Per Share |

| $0.76 |

| SA Quant Score |

| Sell - 2.25 |

(Source - Seeking Alpha.)

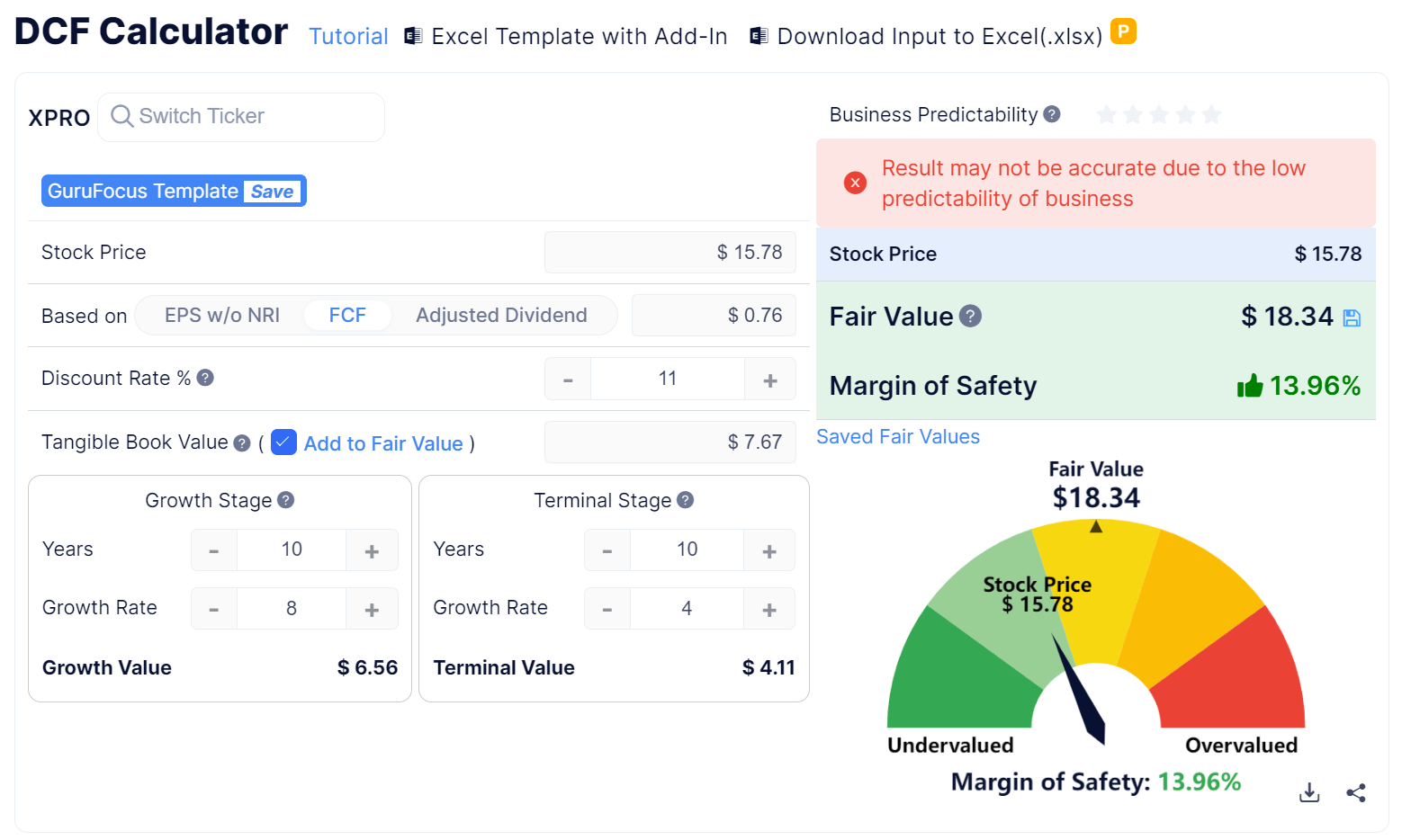

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm’s projected growth and free cash flow:

{kind=link}

Based on the DCF, the firm’s shares would be valued at approximately $18.34 versus the current price of $15.78, indicating they are potentially currently undervalued.

However, the firm’s cash flow generation has been "lumpy" and at a historically high rate in the most recent trailing twelve-month period, so the result may be less accurate due to unpredictability in future cash flows.

Commentary On Expro Group Holdings

In its last earnings call (Source - Seeking Alpha ), covering Q3 2023’s results, management’s prepared remarks referenced its recent Australia offshore incident involving a vessel-deployed LWI (Light Well Intervention) system failure.

The system will likely take several months to recover, and the company has suspended all of its vessel-deployed LWI operations as a result.

Its failure has highlighted challenges with "the best service delivery alternative and the most appropriate apportionment of commercial risk amongst stakeholders."

The company's Q3 results also reflected reduced drilling activities in North American and Latin American regions.

Expro is contending with an oversupply of tubular running services in areas of the U.S. onshore market, with competitors cutting prices to grow market share, so it is redeploying equipment away from the most-impacted markets accordingly.

In the earnings call, I tracked the frequency of keywords and terms mentioned by management or analysts:

Seeking Alpha

The chart shows that the company is facing a number of challenges and headwinds in the most recent quarter.

Analysts questioned management about restructuring the U.S. onshore TRS unit and reconsidering its LWI business approach in light of the Q3 failure incident.

Management responded that it is reducing its U.S. TRS business to obtain better margins and redeploy assets as opposed to divesting.

For its LWI segment, leadership is reevaluating its vessel provider partnership and considering different operating and partnership models to produce better results and avoid failures.

Total revenue for Q3 2023 rose by 10.6% year-over-year, but gross profit margin fell by 0.6%.

Operating income remained barely positive, although falling sequentially by a substantial amount.

The company's financial position is strong, with ample liquidity, minimal debt and strong free cash flow generation.

Looking ahead, the consensus revenue estimate for the full year 2023 suggests top line growth of 17.2% over 2022.

If achieved, this would represent a substantial decline in revenue growth rate versus 2022’s growth rate of 55% over 2021.

Given the challenges the company is facing in restarting its LWI segment, reduced drilling activity in North and Latin America and increasing competition in certain North American basins, I’m not optimistic about Expro’s growth trajectory in the near term.

My outlook on Expro Group Holdings N.V. stock is, therefore, Neutral [Hold] at this time.

For further details see:

Expro Group Faces Revenue Headwinds As Activity Drops