XPRO - Expro Group: International Offshore And New Offerings Strengthen Its Position

2023-05-18 11:48:56 ET

Summary

- New exploration activities in offshore West Africa and Eastern Mediterranean will stimulate demand for Expro Group's products in 2023.

- In Q1, XPRO acquired DeltaTek Global to increase its penetration into cementing jobs.

- Free cash flow remained negative, but the company has no debt.

- The stock is relatively undervalued compared to its peers.

XPRO Gathers Steam

My previous article discussed Expro Group Holdings' ( XPRO ) strengths and weaknesses. Recently, XPRO has stressed LWI (Light Well Intervention) activities and built strategic alliances to provide Subsea technologies. The offshore deepwater project backlog will expand its high-end TRS and Subsea landing stream capacity. Internationally, offshore West Africa and Eastern Mediterranean will stimulate demand for the company's products. Also acquired DeltaTek Global to increase its cementing job market in the Gulf of Mexico, West Africa, and Asia Pacific.

However, in the near term, the situation can remain volatile due to the recessionary condition in the US, which can affect its revenues and operating margin adversely in Q2. Free cash flow has remained negative over the past year, which also concerns investors. Continuing the share repurchase program can keep the pressure on its cash flows. Nonetheless, the stock is relatively undervalued versus its peers. Investors would do well to "hold" the stock, expecting higher returns in the medium term.

The Current Initiatives

{kind=link}

In Q1, XPRO made inroads in vessel-deployed Light Well Intervention (or LWI) systems in offshore Australia. Over the next few quarters, the company plans to build on vendor management and service partner coordination in LWI activities. It has recently entered a strategic alliance with another OFS company to provide Subsea technologies related to completion, decommissioning, and interventional work. The quarter also marked a $40 million contract for a multi-well development in subsea Angola.

XPRO's management believes in multiyear development and capacity expansion in the energy sector. So, the company's long-term outlook is favorable. With various factors supporting an elevated energy price, an addition to the LNG export capacity and improved international and offshore markets will lead to a more robust medium-term demand. However, in the near term, the situation can remain volatile due to the recessionary situation in the US. It appears the US onshore market may have reached a plateau.

In Q2, the North Sea region can see activity ramp up. Considering the slow momentum in the US, a rapidly growing international market, and an improvement in the cost structure, the company's adjusted EBITDA margin can expand by more than 300 basis points in Q2.

How Will The Market Affect Its Outlook?

Several years of underinvestment in the offshore market and recovery of energy demand from the pre-pandemic levels would require operators to replace produced reserves and add capacity. This would meet demand in multiple US basins and Latin America. The environment will create pricing tailwinds from 2023 through 2024. Higher prices will induce new exploration activities in several geographies, including offshore West Africa and the Eastern Mediterranean. This situation would create scope for pricing gains for XPRO.

The company's management expects its FY2023 revenues to increase by 17% compared to FY2022. Adjusted EBITDA can increase significantly (by 81%) during this period. The support costs and cash taxes are expected to be 20% and 3% as a percentage of revenue, respectively. Annual incentives grew in Q1 due to a seasonal build in working capital. Typically, cash flows tend to improve in 2H 2023.

Acquisition And Other Strategies

In Q1, XPRO acquired DeltaTek Global to increase its penetration into the Gulf of Mexico, West Africa, and Asia Pacific. DeltaTek offers a range of open water cementing solutions, which lowers rig time and cost savings due to better quality cementing operations. The company focuses on a premium well construction product line for deepwater and ultra-deepwater development in key growth markets. Investors may note that because well construction and drilling indicate early cycle activities, Expro becomes part of the initial stages of offshore development projects. So, the backlog of offshore deepwater projects expanded its high-end TRS and Subsea landing stream capacity.

The Q1 Drivers

{kind=link}

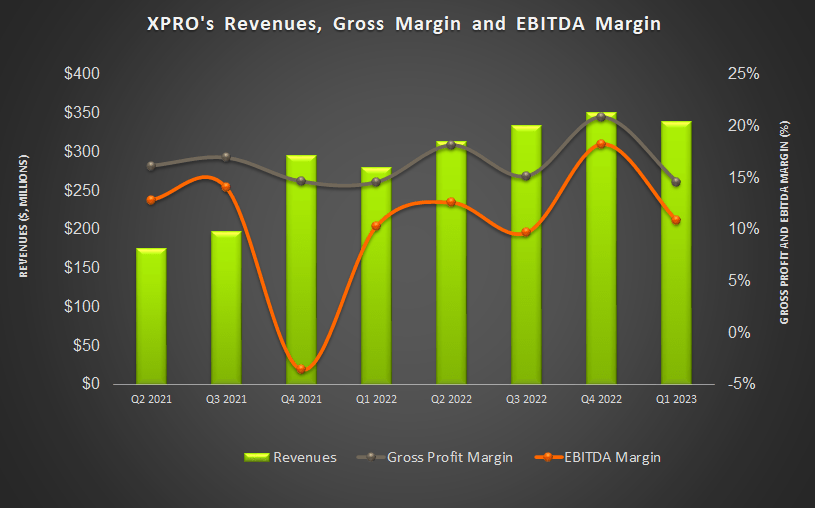

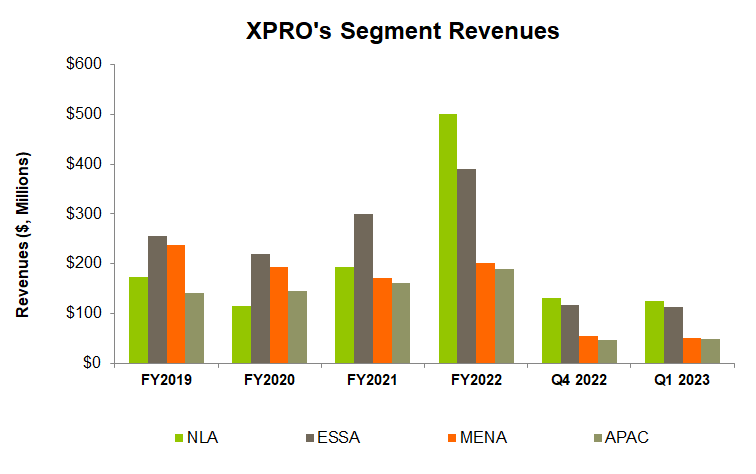

From Q4 2022 to Q4 2023, the company's revenue decreased by 3%. Geographically, the Middle East-North Africa (or MENA) division registered the steepest decline (8% down) during this period, while the Asia-Pacific (or APAC) was the only region to see revenue growth (4% up). The slow activity in the winter season in the Northern Hemisphere and customer budget constraints affected its revenues adversely.

The company's adjusted EBITDA declined sharply (43% down) sequentially in Q1 due to LWI-related commissioning costs on several projects and unrecoverable mobilization start-ups in Asia Pacific. Also, an adverse activity mix in the ESA and MENA regions also impacted the margin. In Q1, the company's gross and EBITDA margins expanded by 640 basis points and 740 basis points, respectively.

Cash Flows And Liquidity

In Q1 2023, XPRO's cash flow from operations (or CFO) turned positive compared to a year ago, led by a sharp rise in revenues in the past year. Although free cash flow remained negative, it improved remarkably over the past year. It kept its FY2023 capex guidance unchanged at ~$125 million, or 53% higher than in FY2022.

As of March 31, XPRO had no debt. Its liquidity was $316 million on March 31. Out of the $50.0 million in repurchases target through November 2023, it has spent $23 million until now at an average price of $13.88 per share, lower than its current price ($17.14).

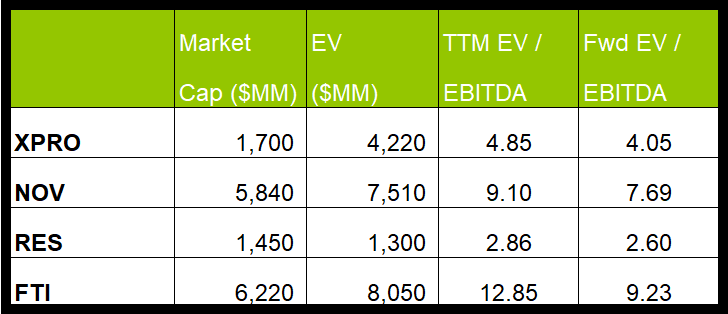

What Does The Relative Valuation Imply?

Author created and Seeking Alpha

{kind=link}

XPRO's current EV/EBITDA multiple (4.9x) contraction to the forward EV/EBITDA multiple (4.1x) is nearly as steep as its peers' (NOV, RES, FTI) average fall. This typically implies a similar EBITDA growth and an at-par EV/EBITDA multiple. The stock's current multiple is lower than its peers' average of 8.3x. So, the stock is undervalued versus its peers at the current level.

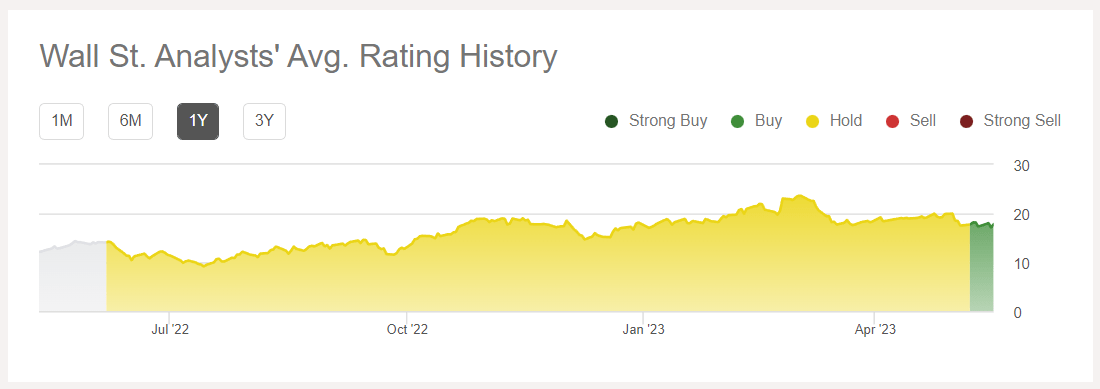

Target Price And Analyst Rating

{kind=link}

In the past three months, three Wall-street analysts rated XPRO a "Buy." Three analysts rated it a "Hold," while none recommended a "Sell." The consensus target price is $25.4, which yields 41% returns at the current price.

Why Do I Keep My Call Unchanged?

{kind=link}

I was reasonably cautious about XPRO in my previous article. I articulated its strengths and weaknesses. While order flow and projects in well construction services, subsea well access services, and well flow management in various international geographies would offer an upside, the long lead time in subsea projects would defer revenue generation for an extended period. I wrote :

subsea well access services and well flow management business from South America, Asia, and Sub-Saharan Africa should become its primary driver, especially when international markets account for 80% of its business. To boost the bottom line, it is on target to achieve its cost and revenue synergies within 36 months from the Frank's International acquisition. However, lower subsea well access revenue in Australia and Malaysia partially offset the growth.

In Q1, the company made noticeable progress in vessel-deployed LWI systems offshore. The North Sea region and other international regions can see activity ramp up. The company's acquisition of DeltaTek Global also increased its penetration into the Gulf of Mexico, West Africa, and Asia Pacific. However, the US onshore market may have reached a plateau. Despite the promises in the medium term, I think the activity slowdown in the Northern Hemisphere and customer budget constraints would require maintaining the "hold" call on the stock.

What's The Take on XPRO?

{kind=link}

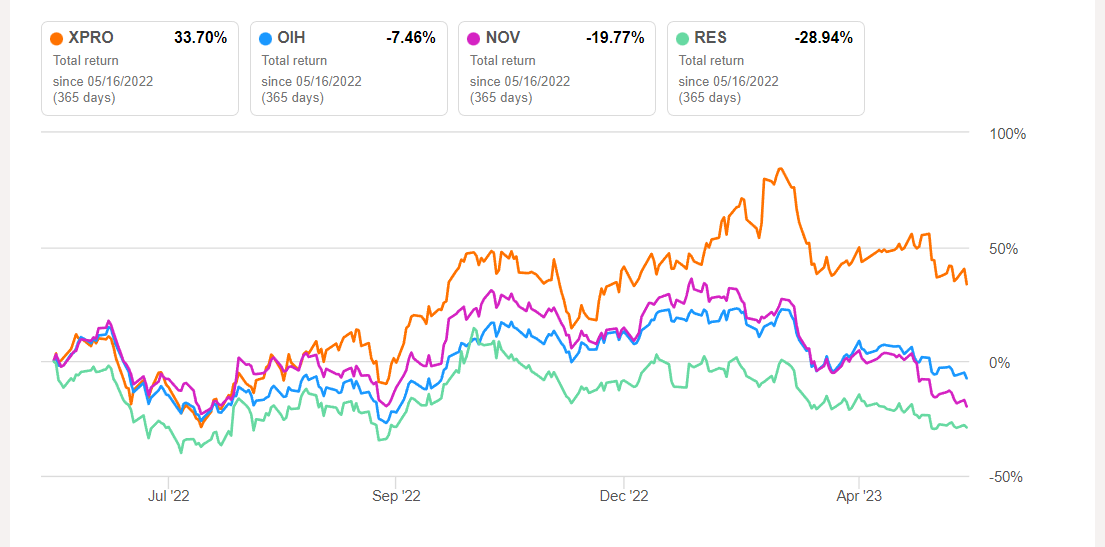

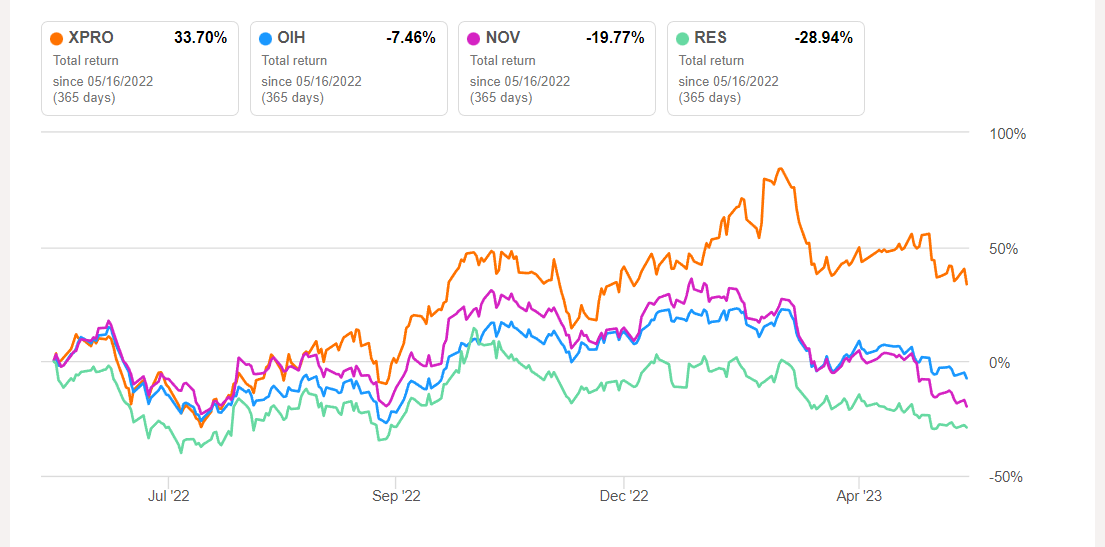

Under the renewed policy adopted in 2023, XPRO has stressed vendor management and service partner coordination in LWI activities. The offshore and deepwater industry is in a multiyear development and capacity expansion mode. The backlog of offshore deepwater projects will expand its high-end TRS and Subsea landing stream capacity. Higher prices will induce new exploration activities in several geographies, stimulating demand for the company's products. So, the stock outperformed the VanEck Vectors Oil Services ETF ( OIH ) in the past year.

Slow activity in the winter season and customer budget constraints affected its revenues and operating margin adversely in Q1. Negative free cash flow can damage the company's ability to continue with the share repurchase program. Despite the obstacles, I would keep my "hold" position unchanged, given the relative undervaluation versus its peers.

For further details see:

Expro Group: International Offshore And New Offerings Strengthen Its Position