XPRO - Expro Group: Strong Results Point To International Offshore Opportunities (Rating Upgrade)

2023-08-19 01:56:39 ET

Summary

- XPRO is expected to benefit from an uptrend in offshore and international activity, resulting in margin expansion and higher cash generation.

- The company faced challenges with non-productive time for LWI systems, but management believes these issues will gradually resolve.

- XPRO's outlook is positive, with increasing offshore projects, growing demand for plug and abandonment solutions, and a strong backlog of new projects.

XPRO Gains Momentum

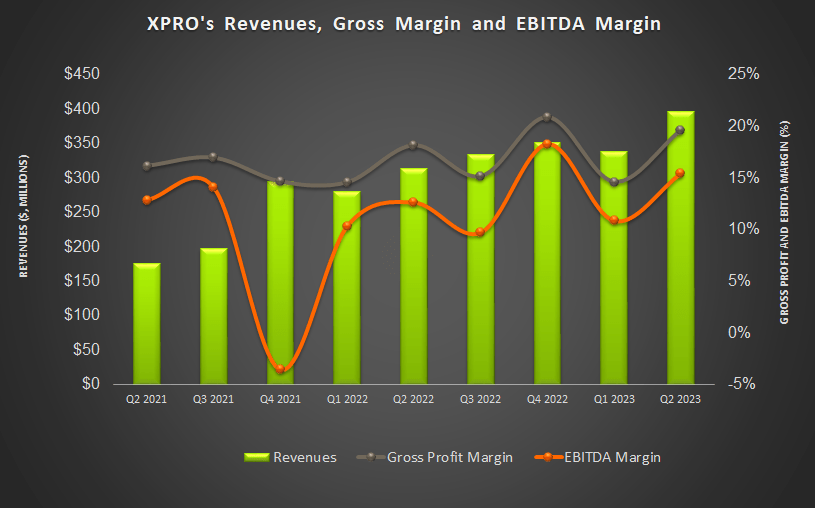

In my previous article , I discussed Expro Group Holdings' (XPRO) strategies. In recent times, a cyclical uptrend in offshore and international activity will benefit XPRO in the coming quarters. The commodity price stability has strengthened its production-related activities. Better pricing, costs, and capital discipline can result in margin expansion and higher cash generation. A stable backlog of $2 billion reflects various new projects and project extensions in the international markets.

The primary challenge in Q2 was the non-productive time for the LWI (Light Well Intervention), which resulted in non-reimbursable costs. But this can correct in the coming quarters. The stock is reasonably valued with a modest upside versus its peers. I think the positive factors will outweigh the obstacles. So, I upgrade it to a medium-term "buy."

Cost Reductions And Challenges

{kind=link}

XPRO's current business model partially depends on international and offshore energy activity. The company should benefit from the tailwind in the next several years because offshore rig count and international activity are on a cyclical uptrend. The company has rationalized its operations to reduce support costs. It has also realized the cost synergy targets. It focuses on asset utilization and increasing the drilling and completion activity to achieve a better activity mix.

The primary challenge in Q2 was the non-productive time for the LWI systems. The delays resulted in non-reimbursable costs in Q2. During the quarter, it worked on the operating issues with the LWI system, and the management believes it should resolve gradually. The company is increasing prices which will start reflecting in 2H 2023. This, plus the costs and capital discipline, is expected to improve its operating leverage and result in margin expansion and higher cash generation.

How Will The Market Affect Its Outlook?

XPRO's management estimated that approvals of the number of offshore projects in 2023 and project sanctions will increase until 2030. Producers will look to increase production as commodity prices stabilize. This will stimulate the company's production-related activities, including well flow management, well intervention, and the integrity of product lines. There is also growing demand for plug and abandonment solutions for the decommissioning market in Europe. An increase in exploration and appraisal in conventional shales, increased carbon capture, and storage projects indicate a positive long-term outlook for the company.

During Q2, XPRO captured $300 million in new work orders. It has a stable backlog quarter-over-quarter, amounting to $2 billion. Its Eni Congo project is on time, and the facility can become operational in 1H 2024. Based on the robust order booking, in FY2023, its adjusted EBITDA can reach $1.5 billion while the EBITDA margin can hover around the 20%-mark. This reflects a year-over-year margin expansion of 400 basis points.

Identifying The Headwinds

In the near term, XPRO has a few margin headwinds. The LWI-related non-productive time accounted for 150 basis point margin contraction in Q2. The company also adopted a conservative approach on the margin from the onshore pretreatment facility in Congo. The project resulted in a 150 basis point margin contraction in Q2. However, profitability on both these accounts is expected to improve over Q3 and Q4.

The Q2 Drivers

{kind=link}

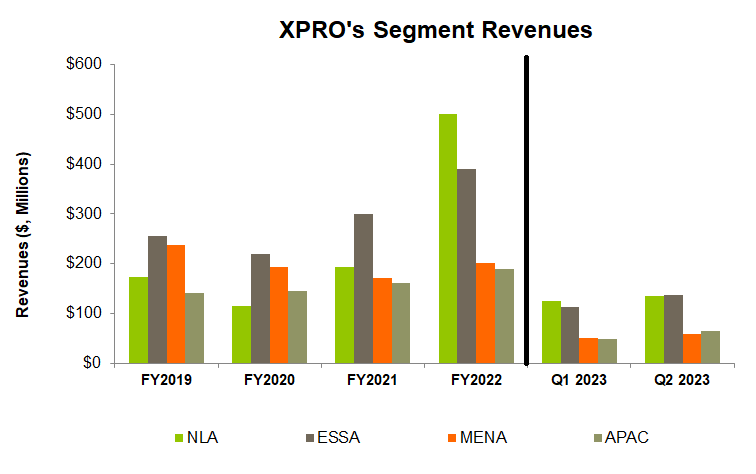

From Q1 to Q2, the company's revenue increased by 17%. Geographically, the Asia Pacific (or APAC) division registered the steepest rise (34% up) during this period, followed by Europe and Sub-Saharan Africa (or ESSA) (21% up). North and Latin America, on the other hand, moved most sluggishly (7% up). Increased subsea direct hydraulic drill stem testing, well testing, and downhole sampling contributed to the APAC region's growth. In Ghana, where the company has been operating since 2012, it received a subsea packages contract extension amounting to $50 million in Q2.

The company's adjusted EBITDA increased sharply (73% up) sequentially in Q2 despite the LWI-related margin headwinds. A more favorable activity mix and lower support costs caused operating profit to improve.

Cash Flows And Liquidity

In 1H 2023, XPRO's cash flow from operations turned positive compared to negative CFO a year ago, led by a rise in revenues in the past year. However, its free cash flow remained negative due to the increase in capex. In FY203, higher revenues and better working capital management should lead to higher cash flows. The company kept its FY2023 capex guidance unchanged from the previous quarter.

As of June 30, XPRO had no debt. Its liquidity was $311 million on June 30. In 1H 2023, it spent $10 million in share repurchases.

What Does The Relative Valuation Imply?

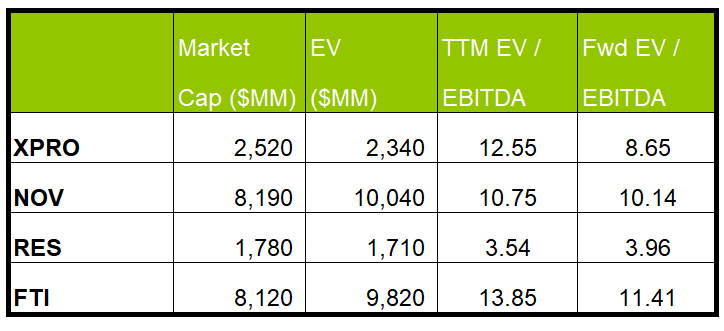

Author Created And Seeking Alpha

{kind=link}

XPRO's forward EV/EBITDA multiple (8.7x) is expected to contract versus the current EV/EBITDA multiple (12.6x). The rate of contraction is much steeper than its peers' ([[NOV]], [[RES]], [[FTI]]) average fall. This typically implies a higher EBITDA growth, which can translate to a higher EV/EBITDA multiple. The stock's current multiple is higher than its peers' average of 9.4x. Comparatively, however, XPRO's EBITDA growth is steeper. So, the stock is reasonably valued with a modest upside versus its peers.

Target Price And Analyst Rating

{kind=link}

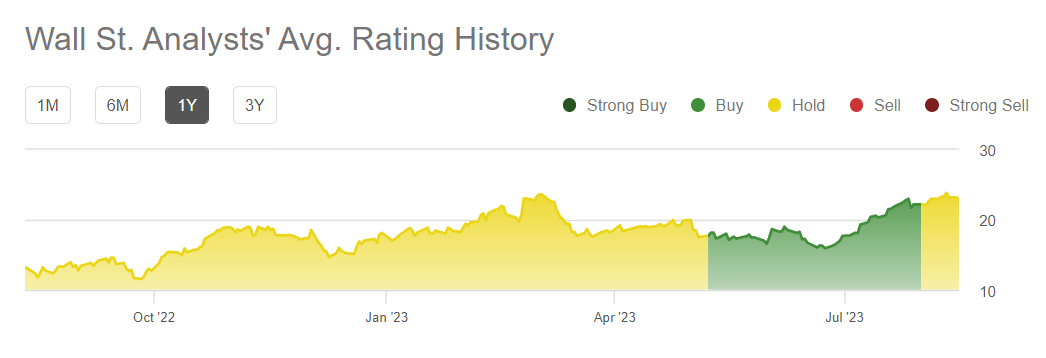

In the past 90 days, two Wall-street analysts rated XPRO a "Buy." Four analysts rated it a "Hold," while none recommended a "Sell." The consensus target price is $25.6, which has a 12% upside potential at the current price.

Why Am I Upgrading?

I was reasonably optimistic about XPRO in my previous article. Its vessel-deployed LWI systems were doing well, while the company's acquisition of DeltaTek Global increased its penetration into the Gulf of Mexico, West Africa, and Asia Pacific. However, a northern hemisphere activity slowdown and customer budget constraints held it back. I wrote :

The backlog of offshore deepwater projects will expand its high-end TRS and Subsea landing stream capacity. Higher prices will induce new exploration activities in several geographies, stimulating demand for the company's products.

In Q3, the North Sea and other international regions can see activity ramp up. The activity slowdown in the northern hemisphere, and customer budget constraints still prevail. Despite that, higher offshore energy production should aid its well flow management, well intervention, and the integrity product lines. The company's cost management efforts will also improve its margin. So, I am upgrading it to a "buy."

What's The Take On XPRO?

{kind=link}

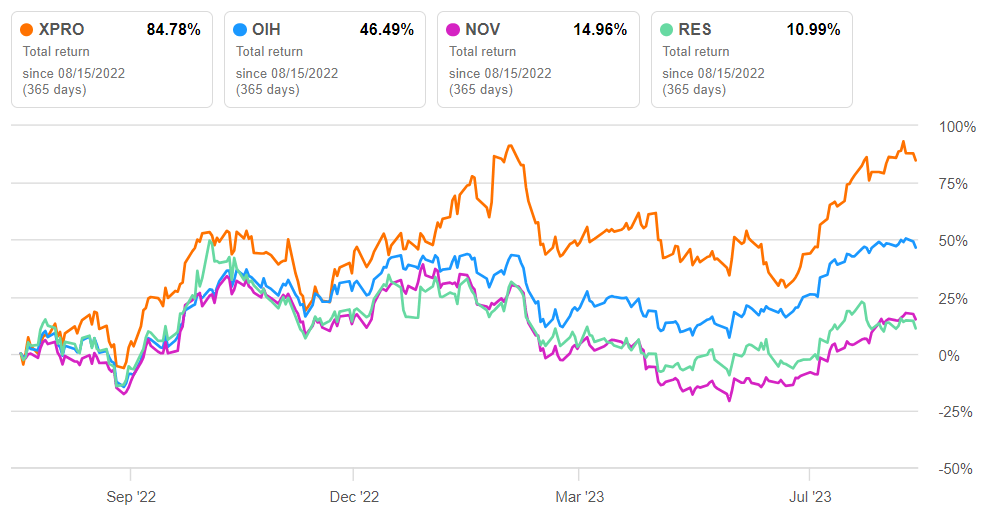

With higher approvals of the number of offshore projects, I expect the project sanctions will increase until 2030. It has also forayed into carbon capture operations. In Q2, its revenues and adjusted EBITDA increased significantly, especially in the APAC region, which shows the momentum on its side. So, the stock outperformed the VanEck Vectors Oil Services ETF (OIH) in the past year.

But the company's negative free cash flow can concern investors. Better working capital management can improve cash flows in the coming quarters. Given the relative valuation, investors might want to "buy" the stock for healthy returns in the medium-to-long term.

For further details see:

Expro Group: Strong Results Point To International Offshore Opportunities (Rating Upgrade)