SRRTF - Extremely High Yield REITs: Danger And Opportunity

2023-12-05 06:37:39 ET

Summary

- There are 19 equity REITs with yields greater than 9%, ranging up to 19%.

- High dividend yields in REITs are partly due to cheap valuations relative to the broader market.

- This article will discuss how to assess the underlying fundamentals and potential risks.

There are 19 equity REITs with yields greater than 9% ranging all the way up to 19%. With dividends that large, the yield alone is sufficient to generate a great return. However, this is a space that comes with just as many traps as opportunities.

This article will discuss the key aspects of fundamental analysis necessary to navigate the risky yet bountiful high yield REITs.

- Origin of high dividend yields

- The 19 highest yielding equity REITs

- Characteristics of extremely high yields

- Dividends are a secondary attribute

- Dividend coverage

- Quality of coverage

- Leverage

We will then get into which of the high yielders are opportunities and which are just plain dangerous.

Origin of high dividends

REITs in general have higher yields than the broader market. This is partially by design as REITs are a pass-through entity meant to distribute the majority of their income to investors. In a normal environment, REITs would yield 100 to 200 basis points more than the S&P.

Today, however, REITs are trading quite cheaply relative to history while the S&P is at a somewhat elevated valuation against current earnings. As such, the dividend gap is wider than normal.

- REIT dividend yield - 4.28%

- S&P dividend yield - 1.62%

With a high base yield of 4.28% for the REIT index, a simple bell curve of variance within the index results in a significant portion of constituents having very high yield. Presently, 19 REITs are yielding in excess of 9%.

19 REITs at 9% to 19% yields

Here is the list.

S&P Global Market Intelligence

Right off the bat, you may notice some commonalities.

Characteristics of very high yields

There is usually a reason a stock is trading at such a high yield with the 3 most common themes being the following:

- Troubled property sector

- Lack of trust in management

- Obscurity

In the list of REITs above you will see a lot of office, some hotel, and both marijuana-related REITs. These areas have legitimate fundamental concerns, so the market demands a higher yield to invest.

Beyond the property sectors this list includes mistrusted management such as RMR managed companies like Service Properties Trust ( SVC ) and Ashford managed companies like Braemar ( BHR ).

Office Properties Income ( OPI ) is both RMR managed AND office, which is probably why it tops the list at 19.3% yield.

Obscurity refers to stocks that are just not on people's radar due to extremely small size or some other aspect that makes them unknown.

Dividends as an investment criteria

While many investors look to dividend yield as a key reason to own or not own a stock, I would like to caution that dividends are not themselves a fundamental factor. It is the underlying cashflows that are the key fundamental factor and then the dividend is just a choice.

A company's board can initiate, raise, cut or eliminate the dividend at any time. That said, there are some fairly reliable ways to anticipate changes in dividends.

- Payout Ratio

- Quality of earnings

- Leverage

Payout Ratio

Dividends can distort the apparent value of a stock by simply having different payout ratios. If one is searching based on a stock's dividend yield it might only look like a good deal because the payout ratio is higher. That dividend might not be supported by earnings which would suggest that level of yield might be subject to a cut.

I think many investors operate under a false assumption that REIT tax law keeps dividend payout ratios in a certain range. While it is true that REITs have to pay out 90% of taxable income to maintain REIT status, taxable income is a very different number than true earnings. REIT taxable income is sheltered by accounting depreciation of their properties so a REIT can have high cashflow and yet quite little taxable income. As such, dividend policy is largely just elective.

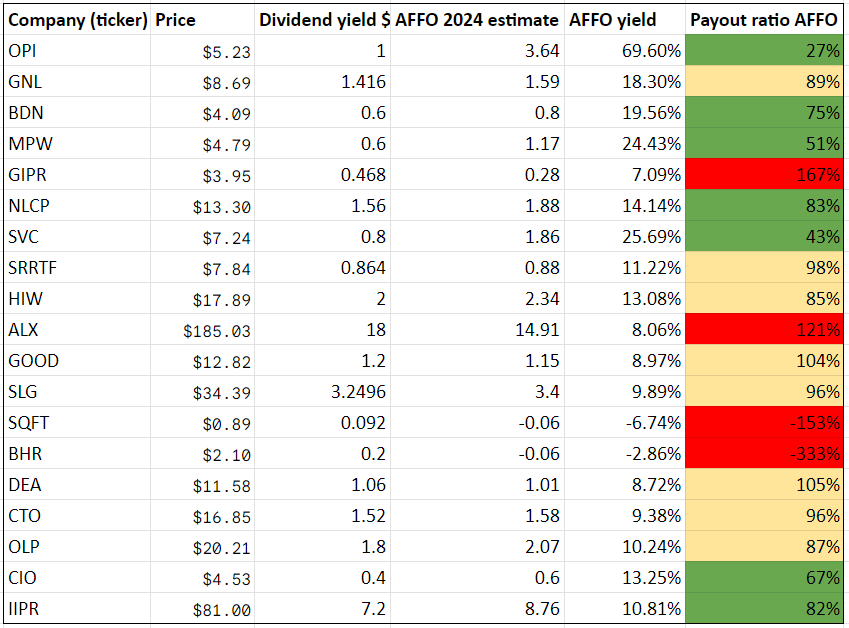

Looking again at the highest yielding equity REITs we have tabulated their payout ratios based on consensus 2024 AFFO estimates (the REIT earnings metric most applicable to dividend sustainability). Note the huge spread in payout ratios.

{kind=link}

OPI, despite having a whopping 19% dividend yield only pays out 27% of its AFFO. Medical Properties Trust ( MPW ) also has a low payout ratio at 51% of forward AFFO.

On the flip side, 4 of these companies have dangerous payout ratios.

Generation Income Properties is paying a dividend that is 167% of its forward AFFO. Alexander's ( ALX ) pays 121% of its AFFO. Presidio and Braemar actually have negative AFFO so their dividends are at particularly high risk. Unless these companies can find some growth quickly, that yield is not sustainable.

A high yield with a low payout ratio seems like a good combination and it can be, but there are more factors to consider. Even if earnings are sufficient to cover the dividend now, earnings might not stay that high. Thus, it behooves an investor to carefully consider the quality of earnings and leverage.

Quality of earnings

Quality earnings for a REIT are those that can sustainably be earned by a property. Many of the companies in this list have poor-quality earnings because the current level of NOI is not likely to remain.

Offices have traditionally had long lease terms and rental rates used to be substantially higher than they are now. Additionally, office tenants tend to be large investment-grade companies so the tenants are largely staying current on that rent. As such, despite the widely publicized struggles of office REITs, most are still pumping out a large amount of earnings.

However, over time, those earnings are likely to decline as leases expire which will result in both vacancy and reduced rental rates in the square footage that does find a new tenant. Thus, all payout ratios are not created equal and even if a company has a low payout ratio the dividend could still be at risk over time if the earnings are of low quality.

The extent to which earnings degrade is influenced by many factors with some of the larger factors being:

- Percentage of properties that are currently earning more than sustainable earnings

- The magnitude of drop in market rental rates and market occupancy rate

- Leverage

Once these factors are considered it provides a significantly different picture as to what the best dividend yields are.

OPI, for example, looked phenomenal at the headline numbers with huge AFFO resulting in its 19% dividend yield having ample coverage with a 27% payout ratio.

It looks much worse in all the quality parameters. A large portion of its portfolio will be subject to NOI decline as leases come due. These NOI declines will be amplified by high leverage as the company sits at 8.67X debt to EBITDA.

OPI is cheap enough that a significant level of decline is priced in so it becomes a judgement call as to the forward outlook. Will the fundamental performance be better or worse than what is priced into the stock?

I don't have a strong opinion on OPI one way or the other, the main point I am making here is that the investment decision on it needs to be far more complex than just looking at the yield with a great payout ratio and thinking it is an income play.

Thus far, we have largely discussed how to spot the plethora of dividend traps. Now I want to turn to what I view as the opportunities in the high yield REIT space.

Opportunity in misunderstanding

Most high yield stocks trade at a high yield for a reason.

The key for selecting which stocks to invest in is to figure out whether the characteristic making the stock trade at such a high yield will actually impact fundamental performance.

Earlier we mentioned 3 main reasons stocks trade at high yields:

- Bad management

- Bad property sector

- Obscurity

In each of these categories, there could be opportunity if the market perception is different than the fundamentals.

Bad management absolutely destroys value so it should trade at high yield to make up for the risk, but what about companies where management is merely perceived to be bad but is actually aligned with shareholders?

I believe that is the case with Medical Properties Trust. Ed Aldag (CEO of MPW) has become one of the most controversial and mistrusted managers in REITs. This lack of trust shows up in the stock price with a 13% dividend yield, well-funded by AFFO at a 51% payout ratio.

The pricing implies a near-criminal level of conduct with a high chance of significant fraud or other catastrophe. This is an angle that has been amplified by the bears and short attackers. Given the amplification, I can entirely understand why the market has come to view it this way.

The opportunity lies in the delta between the market's perception and the facts. If one examines the fundamentals of MPW compared to the rest of the healthcare REIT sector I think the majority of what is going on is just sector-level difficulties.

Healthcare broadly has struggled with profitability since the pandemic. MPW took a hit along with everyone else. MPW's AFFO/share is down, but it really hasn't been disproportionately hurt compared to Ventas or Welltower or the SNF REITs.

It has simply been a tough few years for healthcare. Looking at the actual decisions made such as property acquisitions/sales, tenant negotiations and other aspects that directly impact fundamentals, I believe MPW has done an adequate to good job traversing the challenging environment.

Thus, the opportunity is to buy a decent company with decent management that is trading at the pricing of a company on the verge of collapse.

Property sector misconception-based opportunity

Gladstone Commercial ( GOOD ) along with much of this list trades at a very high dividend yield due to office exposure.

Yet it is distinctly different than the rest of the list. Most of the others are close to 100% office while GOOD is primarily industrial. Much of the hit to GOOD's AFFO per share has been the result of selling office and buying industrial.

Since industrial is a much stronger asset class it trades at lower cap rates so there was some NOI lost in making the transition. As of 3Q23 GOOD achieved 59% industrial.

GOOD

It is even higher now as post-quarter activity continues in this direction.

2024 is likely the trough year as further transition to industrial weighs on AFFO through the cap rate differential, but growth is expected to resume in 2025.

{kind=link}

It is certainly an awkward transition during which to invest, but coming out the other side it represents the opportunity to buy an industrial REIT that is presently trading at an office REIT multiple.

Opportunity through obscurity

The microcaps should trade at a high yield. Presidio ( SQFT ) and Generation Income Properties ( GIPR ) have market capitalizations of around $10 million. Having a market cap of $10 million is too small to be efficient resulting in overhead expense eating up a large portion of revenue.

It is possible they will get bought out by a larger company which could be a big win for shareholders, but it is also possible they will continue to exist and be overburdened by G&A resulting in a steady decline.

A stock being this small is a real burden, but a stock simply being unknown to the market doesn't hurt its fundamentals.

One Liberty Properties ( OLP ) is largely unknown to the market because they don't do much outreach and don't host quarterly conference calls. OLP is a steady sort of company that has been around for decades with consistent earnings. I think it will stay in this state resulting in it being a solid income play.

Slate Grocery REIT ( SRRTF ) is Canadian domiciled with U.S. properties making it awkward to trade for both U.S. and Canadian investors. I believe that is the primary reason it trades at such a high yield because otherwise, it does not resemble the rest of the group.

Grocery-anchored shopping centers are a growth sector and SRRTF is particularly well positioned in population growth sunbelt markets combined with a low supply of competing properties.

It is annoying to own the stock because of withholdings that I have to claw back when I file my taxes, but for me, that small administrative burden is well worth getting to own a growth REIT at just over 8X AFFO.

Our stance on the extremely high yielders

As a high-risk and high-reward area, one should tread carefully. Within the high yield REITs I see quite a few pitfalls.

2MC

But there are also some great stocks. Here are the ones I find opportunistic at the present valuation:

2MC

Some of the other ones are problematic but also so incredibly cheap that they could be opportunistic when traded wisely and with caution.

2MC

For further details see:

Extremely High Yield REITs: Danger And Opportunity