OZKAP - Familiar Concerns Dogging Bank OZK But It Will Take Time To Prove Out The Credit Quality Once Again

2023-10-24 10:37:32 ET

Summary

- Bank OZK's third-quarter numbers were good, but beats on pre-provision profit aren't going to do much to soothe worries about the credit quality of the bank's construction-heavy loan portfolio.

- Bank OZK's unique operating model focuses on commercial real estate and construction lending that other banks avoid, and that has worked well for the bank across multiple credit cycles.

- A high deposit beta isn't surprising or concerning, but investors will be keenly focused on criticized loan metrics and charge-offs in the coming quarters.

- If credit losses through this cycle are typical of prior cycles, Bank OZK is meaningfully undervalued, but it will likely take at least a year for the cycle to play out.

If there are constants in the bank sector, one of them has to be that every time the credit cycle turns, investors start to worry that Bank OZK 's ( OZK ) underwriting will suddenly be exposed and significant credit losses will hammer away at the bank's earnings and capital. It hasn't happened yet, and I don't think it's happening now, but it's one of those "is what it is" situations that investors have to accept as part of the bank's unusual operating model - a model that sees the company actively seeking commercial real estate and construction development lending that other banks walk away from (and/or can't really accurately price).

Since my last update on this company , the shares have lost value, but not nearly as much as the average regional bank comp - down around 6% to 7% versus down 26%. I do think the shares are undervalued, but there's no question that Bank OZK has elevated deposit pricing risk compared to many other regional banks and if this credit cycle truly is different, future losses could be more meaningful than I expect.

A Strong Quarter, But It Won't Matter

With the deposit pricing/deposit beta cycle still playing out and the credit cycle still likely in the early stages, I don't think good quarters from Bank OZK make all that much difference, and indeed the shares didn't react to what was otherwise a fundamentally strong set of results.

Revenue rose about 23% year over year and 3% quarter over quarter, beating expectations by a little less than $0.07/share (or 2.5%). Net interest income rose 25% yoy and 3% in FTE terms, beating by about 3% or $0.075/share. Net interest margin was a little better than expected, beating by 5bp (improving 2bp yoy and declining 27bp qoq to 5.05%), while earning assets beat expectations by about 2% and grew 7% sequentially.

Adjusted core non-interest income was flat yoy and down about 3% qoq, missing by $0.01, but only making up less than 7% of revenue.

Operating expenses rose 11% yoy and came in flat sequentially, beating by more than $0.03, with an efficiency ratio (32.6%) that's among the lowest of the banks I follow regularly. Adjusted pre-provision profits rose 29% yoy and 4% qoq, beating by around 6% or $0.10/share. Provisioning was higher than expected, taking $0.03/share back out relative to sell-side expectations.

Tangible book per share rose about 15% yoy and 2.5% qoq.

Aggressive Balance Sheet Growth When Others Are Pulling Back

Bank OZK management has previously said that they're most excited about the times in which other banks are pulling away from business in their core markets. That would certainly apply to today as larger banks in particular are pulling back on commercial real estate (or CRE) and construction lending. While demand is softer as would-be borrowers have their own concerns about the economy and rates, Bank OZK is still generating high levels of loan growth.

Loan balances increased by more than 7% qoq, exceeding expectations by about 5%, with organic loans up closer to 8% qoq. Construction lending continues to lead the way, with close to 14% sequential growth, though CRE lending was up close to 6% (note: I exclude multifamily from CRE lending; this category was up about 3%).

Loan yields remain robust, rising more than two points from last year and 14bp qoq to 8.58%, and Bank OZK's loan beta is around 62%, one of the strongest I've seen as the bank does so much lending at floating rates. While paydowns did grow in the quarter (up about 7%), loan fundings grew almost 20%.

Bank OZK has never had a strong core deposit base, and that's the nature of the business - the bank's clientele doesn't generate a lot of deposits for the bank and it's not your typical community-based deposit-gathering institute. That means a lower skew to cheaper non-interest-bearing deposits and a much higher reliance on more expensive time deposits and brokered deposits.

Overall deposits rose more than 6% sequentially, with non-interest-bearing deposits down more than 5% (at around 17% of total deposits). Total deposit costs rose almost 50bp qoq to 2.9%, while interest-bearing deposit costs rose almost 60bp to 3.5%. Bank OZK is paying some of the highest CD rates around (recently offering 5.6% for a 13-month CD), and as a resident of North Carolina, I can tell you that they're actively looking for consumer CD customers. Not surprisingly, then, OZK has one of the highest betas in the space, with a cumulative interest-bearing deposit beta of around 63% by my calculation.

Credit Isn't A Problem... Until It Is

The loans that OZK underwrites are widely seen as risky, and indeed, if you don't know what you're doing, you'll lose a lot of money lending to these complex office, retail, hospitality, and mixed-use developments. The "but" is that OZK has been at this a long time and the historical loss rates have been well below the averages - and remember, those averages are much more "plain vanilla" lending.

{kind=link}

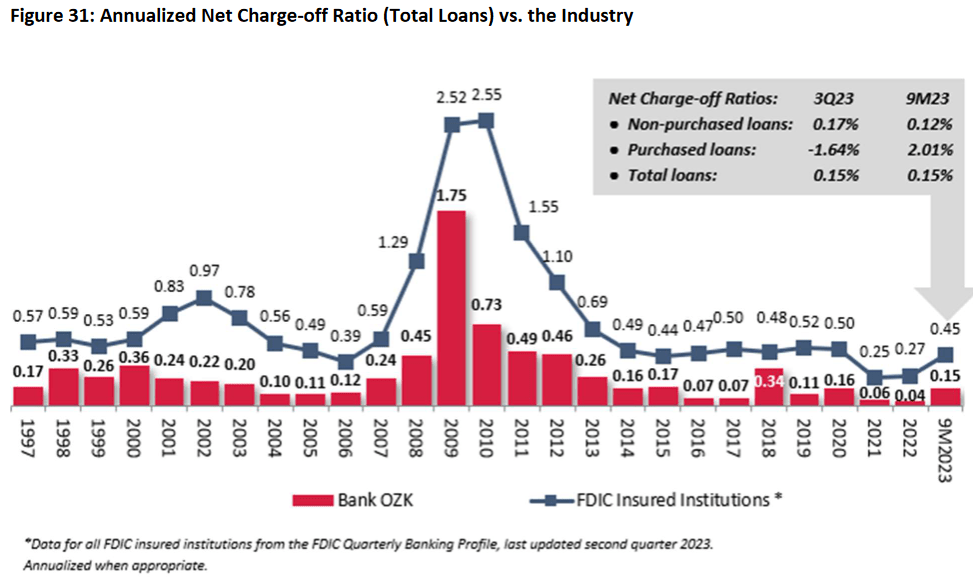

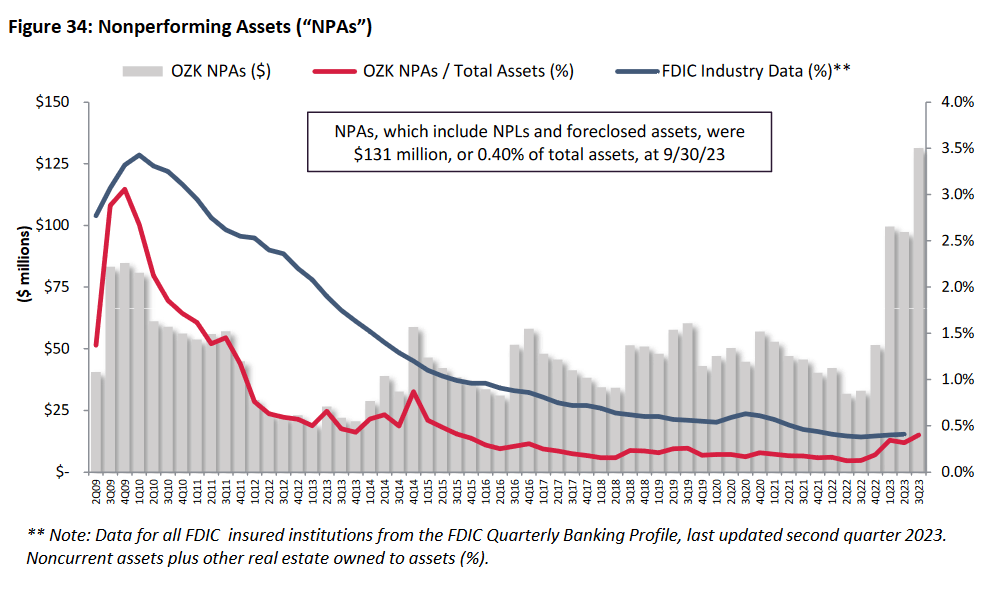

Looking at the recent stats, a non-performing loan ratio of 0.25% isn't all that concerning and charge-offs remain comfortably low at 0.15%. The non-performing asset, ratio, though has been shooting up and is not only at the highest level since 2015, it's about to cross the average of all FDIC-insured institutions, something that hasn't happened in prior credit crises.

{kind=link}

I can understand why OZK isn't for some investors. The office category is close to 9% of loans and construction and development is close to 40%. While OZK has been through many credit cycles, we haven't seen one where office vacancies and falling appraisal values have occurred quite like this. Still, OZK underwrites with an intense focus on asset quality and developer equity, and the company recently sold 99% of its OREO ("other real estate owned", typically real estate acquired through foreclosure) portfolio at a zero estimated loss.

There are certainly different factors playing into this credit cycle - rates are the highest they've been in a long time, and again what we're seeing in the office market isn't typical. So maybe this will be the time that OZK sees outsized losses, but it's just not showing up in the numbers yet and management has been gradually building up reserves (1.2% on outstanding loans).

The Outlook

I'm still expecting OZK to generate long-term core earnings growth of around 6%, and that of course assumes that the bank doesn't have major credit losses through this next phase of the cycle. Ultimately, that's really what the buy/hold/sell discussion comes down to - you either believe that OZK will navigate this credit cycle well, or you don't. The rest is mostly just backfilling the details. I do expect higher charge-offs from here, but I'm expecting them to top out around 0.50% in late 2024/early 2025.

Discounting those core earnings back and using a higher discount rate (+200bp) for the next few years (to account for the "it is different this time" cycle risk, I still get a fair value in the mid-$50s. I get a fair value of around $57 using a modified ROTCE-based P/TBV and P/E; the former assumes a ROTCE of 14% in FY'24/'25 (versus 17% this quarter), while the latter uses a 20% discount to the more typical 12.5x forward multiple for the shares.

The Bottom Line

If OZK navigates this new credit cycle as it has past cycles, the shares are meaningfully undervalued. Until concerns about deposit pricing and credit, and especially credit, start to ease, though, it's hard to see the shares rerating dramatically higher. Investors more interested in collecting dividends during the wait may want to look at the preferreds ( OZKAP ), but the risk there is pretty much the same - if OZK's credit quality turns into a large smoking crater, it'll hit both common and preferreds. I don't expect that to happen, though, and while there are a lot of banks that I like these days, this is a name more risk-inclined investors may want to consider.

For further details see:

Familiar Concerns Dogging Bank OZK, But It Will Take Time To Prove Out The Credit Quality Once Again