RENT - Farfetch: Much Stronger Business Than You May Think

2023-03-21 15:31:44 ET

Summary

- Farfetch’s share price plummeted because investors were scared by its underperformance and delayed profitability path.

- Our analysis shows that underperformance was mainly caused by the macroeconomy and not company-specific mistakes.

- The profitability outlook seems reasonable and achievable. Equity dilution risks are low.

- Attractive valuation allows for gradual stock accumulation even if you prefer a margin of safety.

Co-authored by Mark Khabarov

Farfetch (FTCH), the luxury fashion platform, has been on a roller coaster ride over the past few years. The company's stock soared to nearly $70 per share in 2020, only to plummet to $4 in 2022. This drastic decline may have been due to investors' lack of appreciation for the company's plan to reach profitability. But is the situation truly dire, or is the current share price an attractive investment opportunity?

Farfetch began trading in late September 2018 and successfully raised $6.2 billion in its initial public offering, with a valuation of $8 billion. The company experienced tremendous growth in the following years, with a 4.7x increase in revenue and a 3.7x increase in gross merchandise volume (GMV), resulting in an impressive 57% take rate in 2022. Despite this remarkable growth, Farfetch's share price has taken a hit, with IPO investors losing almost 80% of their investment.

The company's market capitalization has fallen from $8 billion at the time of its IPO to below $2 billion today. Farfetch has been facing challenges on all fronts.

{kind=link}

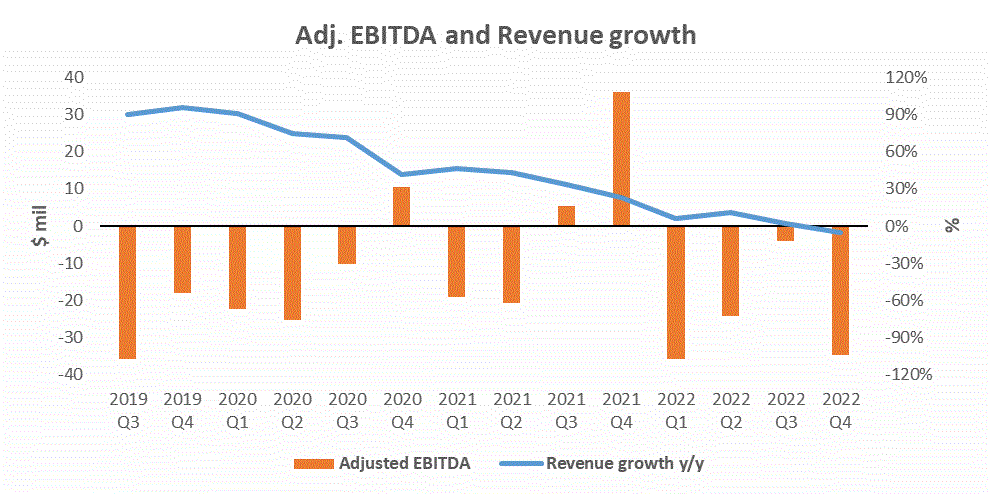

Revenue growth pace decreased to around 0%, while EBITDA has remained highly negative, despite the significant increase in business over the past few years. Its operating loss widened from $550 million to $850 million in the fourth quarter of 2022. It helped create fears that its business model is not sustainable. Plus, the company's cash reserves have decreased from $1.4 billion in the fourth quarter of 2021 to $0.4 billion in the fourth quarter of 2022, due to negative cash flow and ongoing acquisitions. In an attempt to support its cash position, Farfetch issued new debt in the fourth quarter of 2022, which may not have been the best idea for a company with a negative cash flow. The company borrowed $400 million with an original issue discount of 6.50%, which it fully drew upon issuance. The good news is that the loan must not be repaid until 2027.

Investors were further disappointed by Farfetch's Investor Day , where the company presented its long-term strategy, which indicated that positive EBITDA would only be achieved between 1% to 3% of revenue in 2023. This presentation led to a further decline in the company's share price.

At first glance, the decrease in Farfetch's share price appears justified, as the company has shifted from being a high-growth, cash-rich business to a zero-growth, M&A-obsessed entity. Before considering an investment in Farfetch, three key questions need to be answered: Will the slow growth continue, or does the company have a chance to return to a 20%-30% growth trajectory? Is there enough cash to weather market turmoil, or is a significant equity dilution looming at the current low price? And finally, does the current share price reflect all of the negative news, or is the valuation still high?

China, Russia, FX: Any hope for growth?

In 2020, Farfetch achieved an impressive 64% revenue growth, followed by 35% growth in 2021. However, the company's growth came to a halt in 2022. Farfetch attributed this slowdown to the unfavorable macroeconomic conditions in Russia and China. Specifically, the company had to stop its business in Russia after the start of the invasion in Ukraine, as Russia accounted for approximately 7% of the company's Gross Merchandise Value (GMV). Additionally, Farfetch experienced significant logistics bottlenecks due to China's strict quarantine policies, which prevented goods from entering the country. Although these issues were not felt so severely in the West, the Chinese government was much tougher on goods control in course of the zero-tolerance policy.

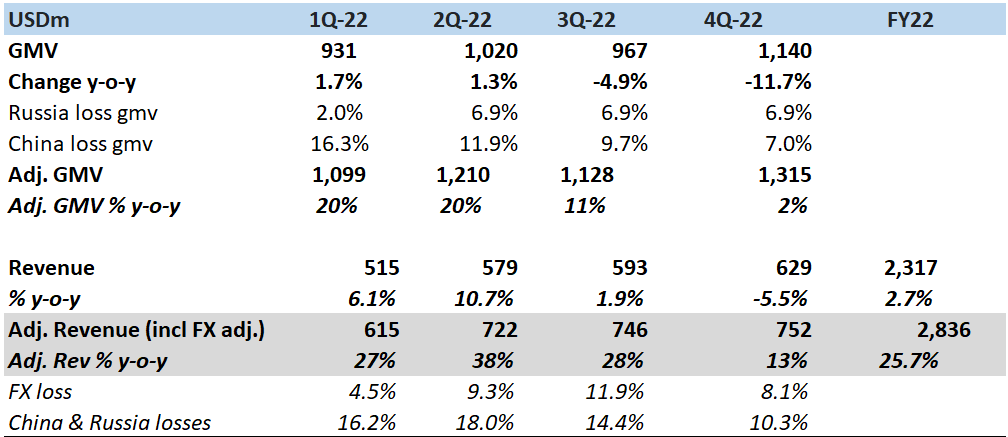

But can we take Farfetch's explanation at face value, or is the company trying to disguise some management failures with macro trends? To investigate this question, we analyzed past sales data and forecasts for Russia and China provided by Farfetch. Our analysis revealed that Russia accounted for roughly 7% of the total GMV in 2021 and was forecasted to grow at a rate of 70% per annum. We performed a similar analysis for China and adjusted revenue for losses driven by Chinese lockdowns. As for the FX rate, exchange rate development is driven by the fact that although the US is the largest market, Farfetch sells a lot of goods not in the USA but reports in USD. Hence, its non-USD sales are valued lower in USD if the USD appreciates. We saw exactly this in 2022.

To estimate the impact of these factors, we calculated the GMV and revenue losses attributable to Russia, China, and FX. Then we compared revenue adjusted for these macroeconomic factors with the initial Company's outlook. We relied solely on information from earnings call transcripts and financial reports.

{kind=link}

We got a difference of 7%. So initially the company was expected to grow by 33% over the entire year and revenue adjusted for macroeconomic factors increased by 26%. The company underperformed by 7%, but it is still acceptable given that inflation in the USA and Europe turned out to be much more persistent than initially expected. In the table below you can see a detailed revenue bridge.

{kind=link}

When we adjusted revenue for lockdowns in China, we thought, but were lockdowns so bad or did Farfetch just make some mistakes in China? To answer it we benchmarked Farfetch's performance with its peers. But before looking at it, let us see how the company commented in Q2 .

Chinese sales falling is not only Farfetch's problem. Chinese sales growth was in line with other peers, so if the company's peers' sales in China falling it is not surprising that Farfetch experienced the same. The reason for the decline is Chinese COVID restrictions in mainland China. If we compare it with vertically integrated companies in the fashion sector we could assume that the Farfetch issue is common in the industry. Richemont and LVMH underperformed the Chinese market by 22% and 8% respectively. Hermes Asian sales that is mostly consist of Chinese sales grew over the market by 6%. Hermes was more an exclusion from the overall trend and is probably driven by its special relation in China and the popularity of Birkin bag.

The comment below from LVMH ( LVMHF ) supports the view of Farfetch's management:

Needless to say, the business in China in the second quarter of the year was down heavy double-digit. So it's painful, but it shouldn't last or it will last as long as restrictions are being enforced.

Looking at other peers we see that Richemont ( CFRHF ) suffered too, but Hermes ( HESAY ) remained robust due to the exceptional popularity of Birkin bags in China.

Company's reports

In a nutshell, Hermes was an exception to the trend, while Farfetch performed in line with its peers. But what is good, is that negative factors in China started reversing due to the removal of most COVID restrictions. Given the lifting of restrictions in China, we see that the fashion industry shrugged off issues and is on the road to higher growth in the region.

Our analysis shows that Farfetch's underperformance in 2022 was driven by a very adverse macroeconomic mix rather than company-specific factors. Definitely, if recession kicks in it can affect Farfetch again. Therefore, it is important to understand if Farfetch has enough cash to go through a potentially difficult time and continue developing the business. Before looking at a detailed cash flow model, let us first understand how Farfetch positions itself for the next years.

New business model - What to expect?

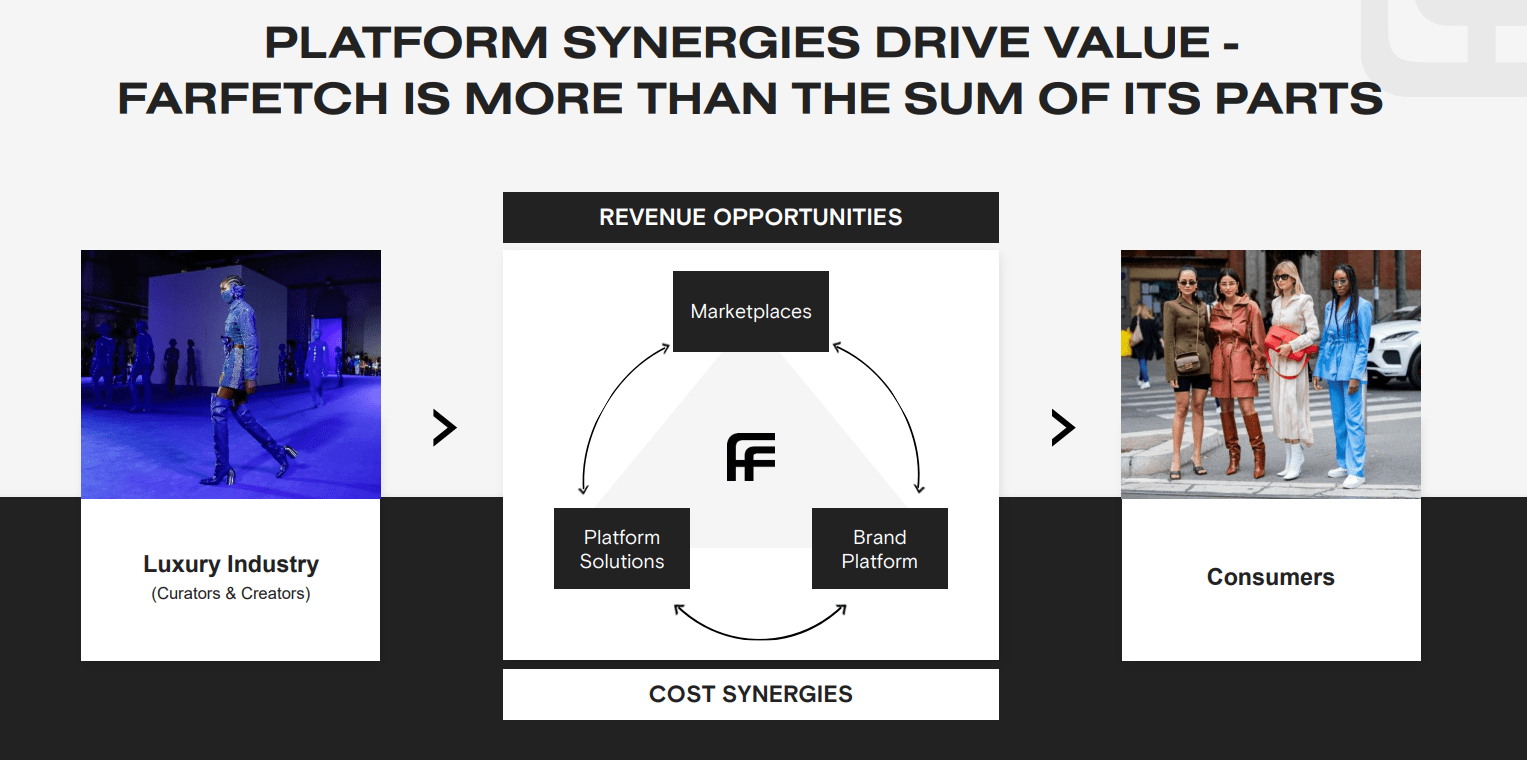

Farfetch is a global technology platform that connects consumers with luxury fashion products from around the world. If earlier it was just a marketplace for other brands and developer of its brands, then now it is aspiring to create the entire ecosystem for brands consisting of three businesses: Marketplace, Platform Solutions, and Brand Platform. It will basically be the shop and full-scale consultant for third-party products on top of its own brands.

{kind=link}

- The Marketplace business is the company's flagship offering, which is an online platform where consumers can shop for luxury fashion products from boutiques and brands around the world. Farfetch's marketplace offers a wide selection of products, including clothing, footwear, accessories, and beauty products, and connects consumers with over 1,300 boutiques and brands. Farfetch generates revenue through commission fees charged to sellers on its marketplace platform.

- The Platform Solutions business provides technology and logistics solutions to luxury fashion brands and retailers, enabling them to offer their products to consumers through their own digital channels. Farfetch's platform solutions include services such as e-commerce website design, digital marketing, and logistics management. By providing these services, Farfetch enables brands and retailers to enhance their online presence, expand their customer reach, and increase sales. Farfetch generates revenue through fees charged for these platform solutions.

- The Brand Platform business is a system of Farfetch's own brands that are sold within the Farfetch ecosystem. Farfetch Brand Platform can leverage Farfetch's technology, logistics, and customer reach to enhance their digital presence and grow their online sales. The Brand Platform offers brands a range of services, including website design, marketing, and customer service support.

Plus, the company recently concluded a partnership with Neiman Marcus Group that allows it to get a much better understanding of ongoing trends in fashion retail. It acquired a major stake in Yoox Net-A Porter increasing its market share in fashion e-commerce and announced a partnership with Reebok . Although all these steps contribute significantly to the company's growth strategy, they were a significant drain on the company's cash. Together with the protracted profitability path announced at the recent Capital Markets Day, it disappointed investors. But does profitability really look so bad? As usual, we took a deeper look.

Profitability path - Disappointing or encouraging?

To compare Farfetch's EBITDA margin with its peers, we first consolidated the three business segments into two. Farfetch's Brand & Solutions business is expected to generate a 20% EBITDA margin in 2025, while the marketplace segment targets a 5% margin. For benchmarking profitability targets against peers we split the companies based on their business model: companies that sell their own brands using their own logistics, marketing, and selling structure were classified under Brand & Solutions or Vertically Integrated, while companies that have a platform connecting customers and producers were classified under Marketplaces. Vertically integrated companies include LVMH, Hermes, Richemont, Kering ( PPRUF) , Lululemon ( LULU) , and Swatch Group ( SWGAY ), while Zalando ( ZLDSF ), My Theresa ( MYTE ), ThredUp ( TDUP) , and Rent the Runway ( RENT) are in the marketplace category. In the Vertically Integrated segment, the median EBITDA margin is about 25%, while 13% is in the Marketplace segment. But Zalando, the fashion e-commerce leader in Europe, generates a 6% EBITDA margin, which is in line with Farfetch's targeted margin. It is even more interesting that when Zalando was of a similar size to Farfetch, its EBITDA was also around zero. Another peer, ThredUp, targets a 20% margin, but it's more of "wishful thinking" than something tangible and should be taken with a pinch of salt in our view.

Company's reports

Thus we see that 2025 EBITDA margins presented by Farfetch look realistic and achievable given the company's strong track record during "normalized" macroeconomic conditions. On the other side, long-term margins especially for the marketplace business look more like a marketing trick rather than an achievable goal.

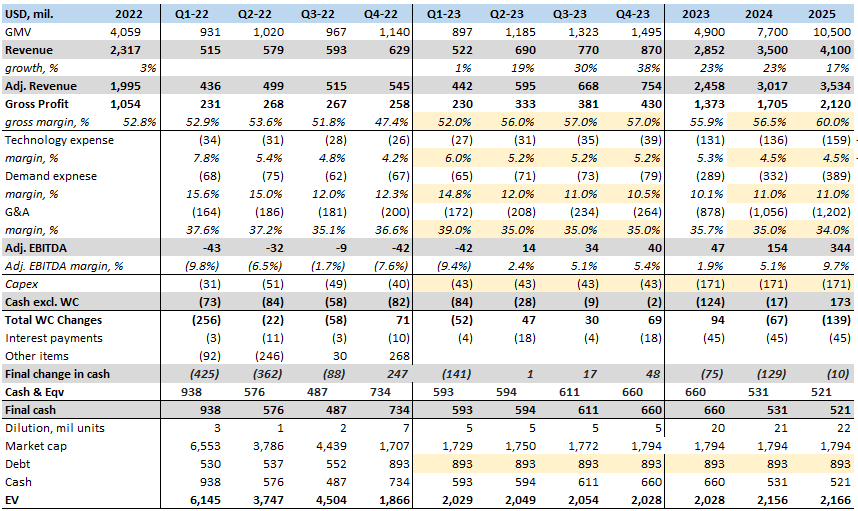

The further question that concerns us is if there is enough cash for Farfetch to go through a period of low profitability. To understand this we built projections reflecting management's case.

Business projection: Equity raise can be avoided

We took a deep dive into Farfetch's business model, analyzing how the company generates revenue and the resulting net cash changes. In 2023 Farfetch plans to benefit from its recently announced partnerships, while in 2024 should be boosted by the Net-a-Porter acquisition (approval pending). Thereafter the company should grow in line with the market. Many in the market are not happy that Farfetch expects to achieve a low EBITDA margin of 10%-13% in 2025, but I would not be so skeptical. As you saw in the previous part, it is quite natural for companies in this sector to have such margins.

{kind=link}

The key thing is how well Farfetch will be able to optimize its cash flow. If the company achieves what it plans to do, there will be a significant cash boost from Working Capital over late 2023 leading to a strong cash position.

By combining all the data into one model and assuming no further M&A activity from Farfetch, we determined that the company will spend more cash than it earns, but no further cash raises are needed. Additionally, we do not expect any significant equity dilution. Overall, we are optimistic about Farfetch's ability to manage its cash flow and maintain stable debt levels in the near future.

Valuation

To get a better sense of how Farfetch stacks up against its peers in the online marketplace and brand and solutions sectors, we conducted a thorough analysis of revenue and EBITDA projections. We looked at the EBITDA margins of integrated vertical companies over the past few years, multiplied them by estimated revenue figures for 2025, and arrived at EBITDA estimates. For marketplaces, we relied on the companies' projections for EBITDA margins, given that many of them are not yet profitable. We also calculated separate ratios for each of Farfetch's business segments. We then divided the market cap and EV by the weight of the current revenue for each segment, using revenue forecasts from Farfetch's own presentations. Finally, we compared Farfetch's P/S and EV/EBITDA ratios to the average ratios of its peers and found that there is significant upside potential for Farfetch. It's worth noting that the median EV/EBITDA of marketplaces was influenced by Zalando's high multiple, which is a reflection of its leading position in the industry.

{kind=link}

Risks

I see two main risks: M&A difficulties and the looming recession. A great part of the company's growth was coming from M&A activity. Today, Farfetch lacks the money to acquire other companies so aggressively as in the past. Plus, the market is basically closed for new money. It means that the company needs to grow organically optimizing its product mix and cost structure, otherwise 2025 targets are not reachable. And here we're coming to the second risk: recession threat. If the economy starts suffering, people will buy less luxury and the fashion industry will be slower in its digital transformation. This would be a headwind for Farfetch. If the growth stops abruptly, WC will drag on the Cash Flow as it did in 2022. It may lead to strapped liquidity and potential financial issues.

Conclusion

I find Farfetch a very attractive business. Its performance adjusted for macroeconomic shocks is strong, it has the potential to extract cash from its vast Working Capital and it is very attractively valued. What I do not like is that the business may return to growth only in late 2023 and only if the recession does not start. Despite a significant recession threat, an attractive valuation allows me to have some margin of safety by gradually investing over the next 12 months.

For further details see:

Farfetch: Much Stronger Business Than You May Think