FTCH - Farfetch: The Long Road Back To Regaining Credibility

2023-11-30 10:31:41 ET

Summary

- Luxury fashion marketplace Farfetch saw a 53.7% decline in stock price, hitting all-time lows yesterday after the company withheld results and withdrew its guidance.

- It's disappointing but not surprising, going by its weak recent performance compared to forecasts and history of downgrading its outlook well into the year.

- If it weren't for the company's exceptionally bullish forecasts, it could have avoided the stock price volatility. But even if it's more realistic now, it would take time for FTCH to regain credibility.

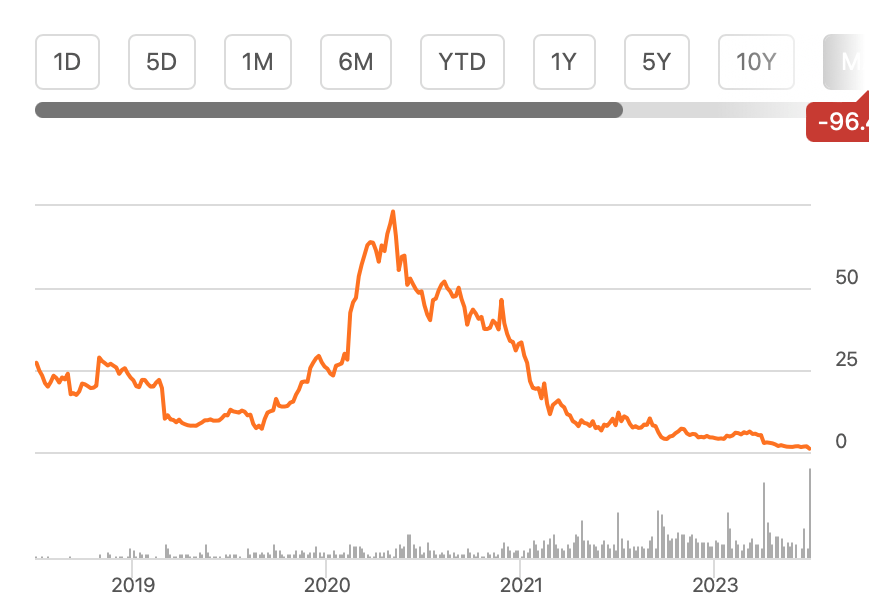

London based luxury fashion and accessories marketplace Farfetch ( FTCH ) was arguably one of the biggest movers in yesterday’s trading. It saw a huge 53.7% decline in price to all-time lows (see chart below). That the stock was ready to drop was evident even when I wrote about it in September, based on its weak performance and the limited credibility of its guidance. This prompted a Sell rating.

But it wasn't until yesterday that the price truly fell. Here I take a closer look at what prompted it and what's next for Farfetch.

{kind=link}

All time lows for Farfetch (Source: Seeking Alpha)

Why did the price plunge?

Yesterday’s sell-off was prompted by the exact concerns I had raised earlier, on both Farfetch’s performance and even more importantly, the outlook. As it happens, the company was due to release its third quarter (Q3 2023) results yesterday. It withheld them instead, saying that it expects to provide an update in due course. This in itself is odd considering that it was only on November 6 that the company had announced the date of its results release.

But the real alarm bell was the withdrawal of its guidance. Specifically, the company said the following:

The Company will not be providing any forecasts or guidance at this time, and any prior forecasts or guidance should no longer be relied upon.

The history of downgrades

This of course is hugely disappointing for investors, because it essentially indicates that investors should expect a downgraded outlook. But it’s not entirely bad, in so far as it reflects a tacit acknowledgement of the unreliable nature of the company’s past forecasts. This bears some explaining, going back to the start of 2022.

China related disruptions

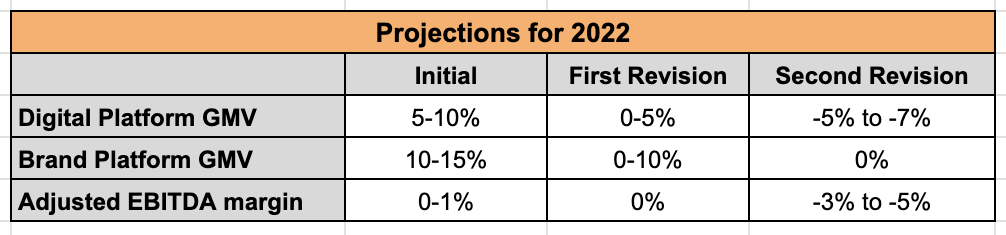

After positive initial forecasts, the company had downgraded expectations for the full year 2022 in both Q2 and Q3 2022 on weak performance. It had initially expected a 5-10% growth in gross merchandise value [GMV] for its important Digital Platform, which brought in over 85% of the company's total GMV in the year. By the time of the second revision, in Q3 2022, the company had reduced the forecast so much, that it now expected a decline of 5-7% in the segment.

Similarly, projections for the Brand Platform fell sharply too, to an expectation of no growth during the year. And it swung from a small positive adjusted EBITDA margin outlook to that of a loss (see table below).

{kind=link}

Source: Farfetch

However, at the time, the gap between performance and outlook could still be explained by the COVID-19 related disruptions in its second biggest market, China in particular, which had probably not been factored in. Until the process showed signs of repeating in 2023 as well, that is.

Continued underperformance in 2023

In Q2 2023, the company reduced guidance again. And significantly. It now expected total GMV to grow by 7.3% compared to initial expectations of a 19.5% growth. The adjusted EBITDA margin outlook was also revised downward (see table below)

{kind=link}

Source: Farfetch, Author's Estimates

This latest downgrade was harder to digest for two reasons. One, there was no unexpected external impetus for it. Sure, the US, its biggest market, has underperformed this year, which is evident in the numbers for consumer discretionary companies across the board. But it’s not unexpected, in the least. So it’s harder to justify. Moreover, unlike last year, the company doesn’t provide any explanations for the change in outlook either.

Secondly, even with the downgrade, it appeared unlikely that Farfetch would be able to achieve the targets going by the company’s performance so far in the year. Up to H1 2023, it saw a revenue growth of just 3.1% compared to projections of an 8.7% increase.

It appeared unclear at the time, where the growth spurt in H2 2023 would come from considering the continued sluggishness in the US and the lack of pickup so far in its China market. Similarly, its adjusted EBITDA margin forecasts looked like they wouldn’t materialise either. The company had seen negative margins of 7.3% and 6.4% in Q1 and Q2 2023 respectively.

Speculating 2023 outcomes

Now that guidance has been withdrawn, Farfetch's past performance is now the best gauge of what to expect. The company's revenue growth during H1 2023 is actually in line with the 3% rise seen in 2022.

Based on this, it’s fair to assume that we shouldn’t expect anything different for H2 2023 or the full year 2023. In fact, I’d think that the revenue increase could be even softer going by the continued weakness in the US market and the fact that demand from China hadn’t picked up for the company up to H1 2023.

There’s also no reason to expect that Farfetch would post an adjusted EBITDA profit going by both the losses in 2022 and in H1 2023.

Attractive market multiples, or not?

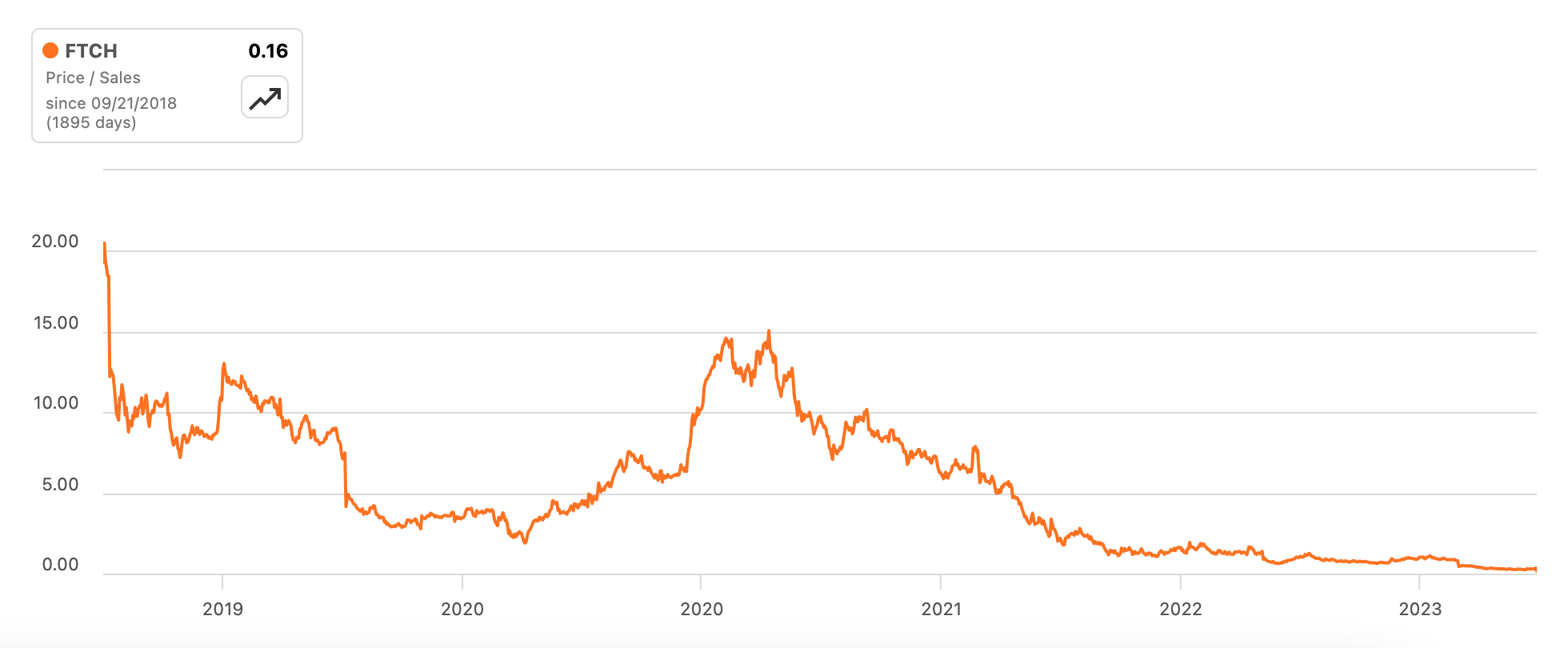

With the latest price drop, FTCH’s trailing twelve months [TTM] price-to-sales (P/S) ratio is now down to the lowest level ever of 0.16x (see chart below). With no financial updates since I last wrote about it, this of course means that the P/S has fallen pretty dramatically from the low 0.39x levels even then. It also continues to trade way below the average P/S for the consumer discretionary sector at 0.85x.

{kind=link}

FTCH, TTM P/S (Source: Seeking Alpha)

But of course there’s a good reason why the stock is trading at the levels it is. In this case, the low valuation is not a reason to consider buying, but an indication of the fact that there’s almost definitely something negative unknown coming in its next financial update.

What next?

The key challenge with Farfetch, as I see it, is less its weak performance right now and more its rather bullish forecasts. If its outlook had been more conservative from the word go, the stock probably wouldn ’t have seen this kind of volatility. To this extent, the withdrawal of guidance is actually a positive in my view, if it leads to more realistic targets.

However, for now, I believe the damage has been done for the medium to long-term investor. And it will be a long road to regaining credibility again. But for short-term speculators, now is actually a good time to buy considering that the stock is at all-time lows now. It’s risky, but it might just get rewarded. I won’t base the rating on this, though. At least until the next financial update, I’m retaining the Sell rating on Farfetch stock.

For further details see:

Farfetch: The Long Road Back To Regaining Credibility