VRAI - Fed Keeps Chasing Its Tail

Summary

- U.S. equity markets posted their worst week since June after CPI data showed an unexpected acceleration in headline inflation, likely keeping the Fed on course to further tighten monetary policy.

- Declining in four-of-the-past five weeks and effectively erasing its summer rebound from mid-June to mid-August, the S&P 500 dipped 5.2% on the week while the tech-heavy Nasdaq dipped nearly 6%.

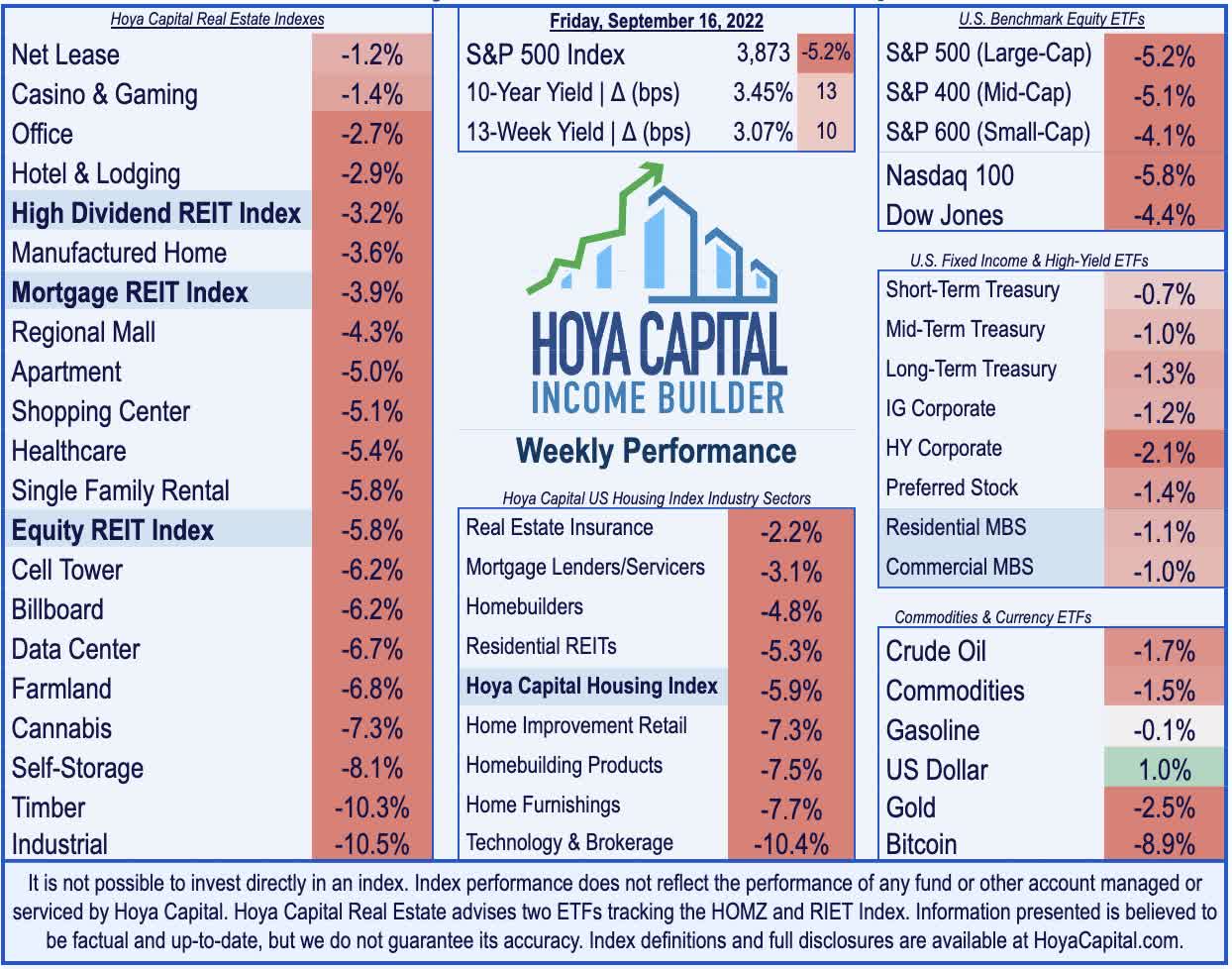

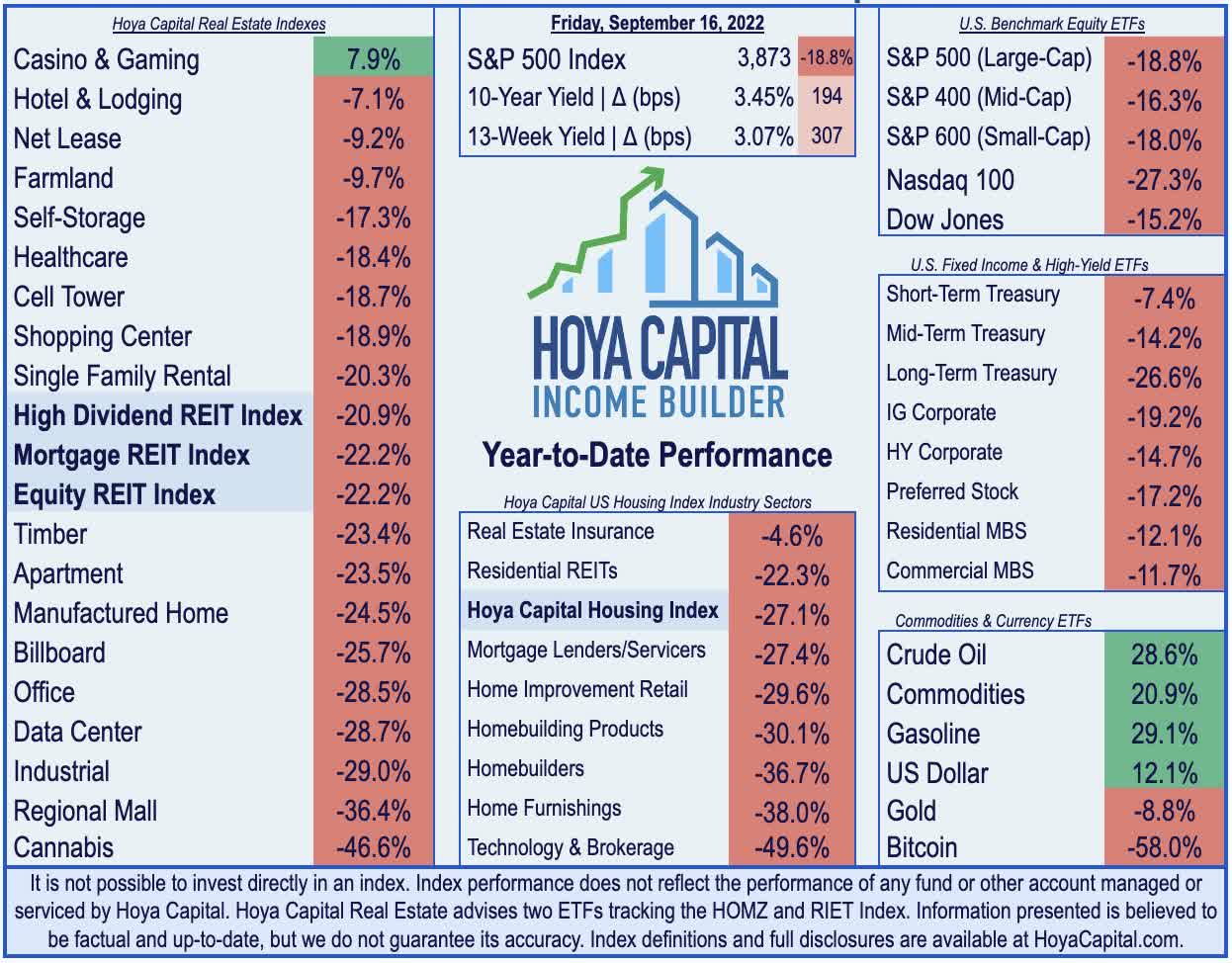

- Real estate equities were also broadly lower on the week despite a generally positive slate of dividend and M&A news. The Equity REIT Index dipped 5.8% while mortgage REITs declined 3.9%.

- Peak Inflation? Depends on who you ask. While the closely-watched CPI report this week showed an unexpected acceleration in August, the balance of the inflation reports showed that real-time price pressures have cooled considerably over the past quarter.

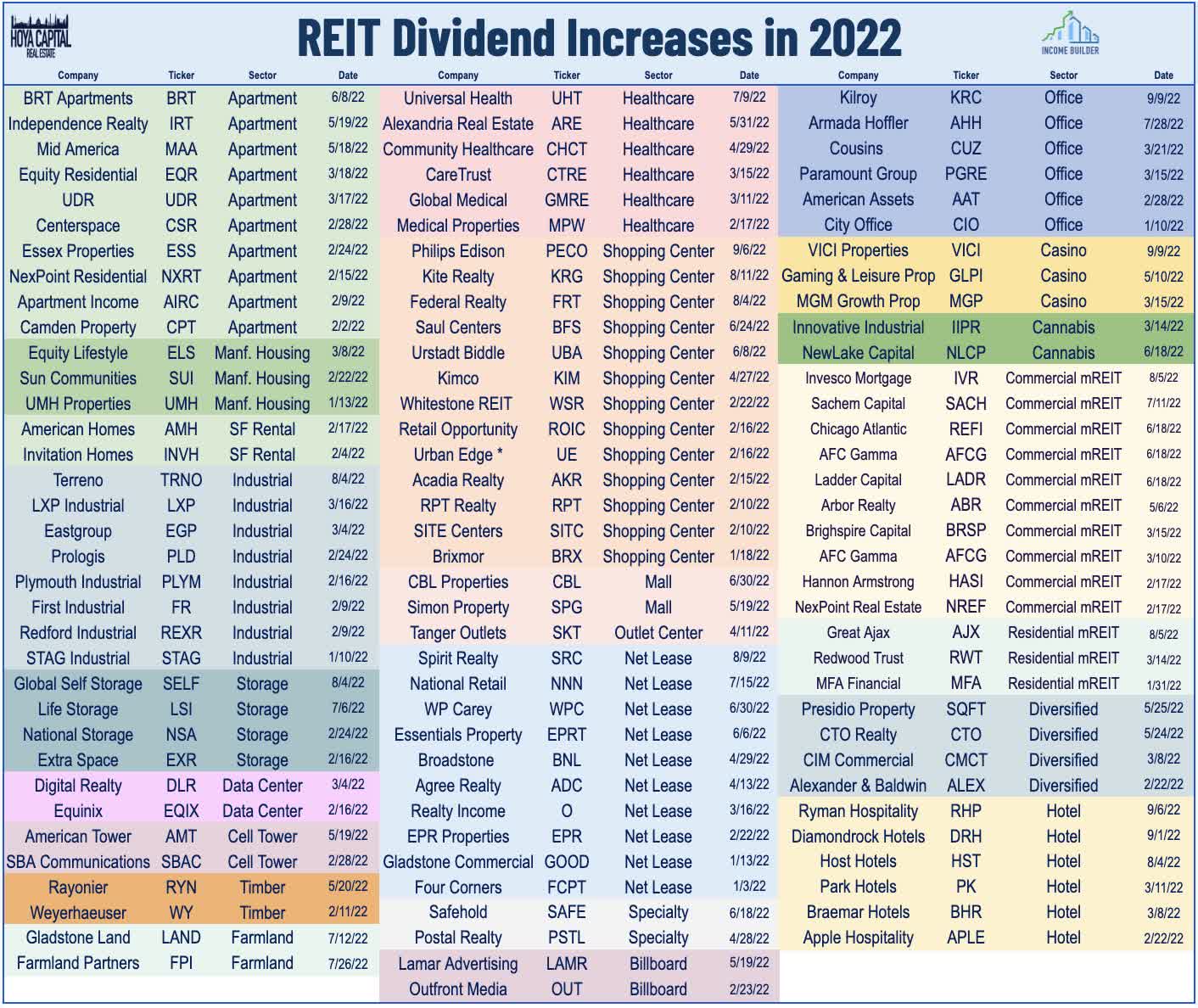

- There were several bright spots amid an otherwise rough week of performance across the real estate sector. Four more REITs raised their dividends this week, bringing the full-year total across the real estate sector to 106 while STORE Capital surged following a takeover bid.

This is an abridged version of the full report published on Hoya Capital Income Builder Marketplace on September 12th.

Real Estate Weekly Outlook

U.S. equity markets posted their worst week since June after the closely-watched CPI report showed an unexpected acceleration in headline inflation last month, likely keeping the Federal Reserve on course to deliver another "jumbo rate hike" in the week ahead. Concern has mounted that the central bank risk compounding a pandemic-era policy error by rapidly tightening monetary conditions based on "stale" data as the hot CPI report - which uses a methodology prone to significant lags - seemingly overshadowed a plethora of more real-time inflation metrics and economic reports suggesting that the U.S. and global economy has downshifted considerably in recent months.

{kind=link}

Declining in four of the past five weeks and effectively erasing its summer rebound from mid-June to mid-August, the S&P 500 dipped 5.2% on the week, bringing its year-to-date dip back to the cusp of the "bear market" threshold of 20%. The tech-heavy Nasdaq 100 dipped nearly 6% to drag its year-to-date declines to over 27%. Real estate equities were also broadly lower on the week despite a generally positive slate of dividend and M&A news. The Equity REIT Index dipped 5.8% on the week with all 18 property sectors in negative territory while the Mortgage REIT Index declined 3.9% and homebuilders remained under pressure as the 30-Year Mortgage Rate jumped above 6.0% for the first time since November 2008.

{kind=link}

The carnage across bond markets continued as well with the 10-Year Treasury Yield and 2-Year Treasury Yield each climbing to their highest weekly close in fifteen-year as traders currently price in an 80% probability of a 75 basis point rate. Crude Oil finished lower by 2% while the US Dollar Index climbed to 20-year highs. Clashing with comments from Fed Chair Powell in late August referencing "strong" underlying economic momentum, package delivery giant FedEx ( FDX ) plunged more than 20% on the week after warning that it will likely miss its profit target, citing weakness in Asia and challenges in Europe, and expects conditions to weaken further in the quarter ahead amid weaker global volume. The warning follows another soft slate of economic data this week that led to downward revisions in several GDP forecasts that now project a third-straight quarter of GDP contraction for the first time since the 2008 Great Financial Crisis.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

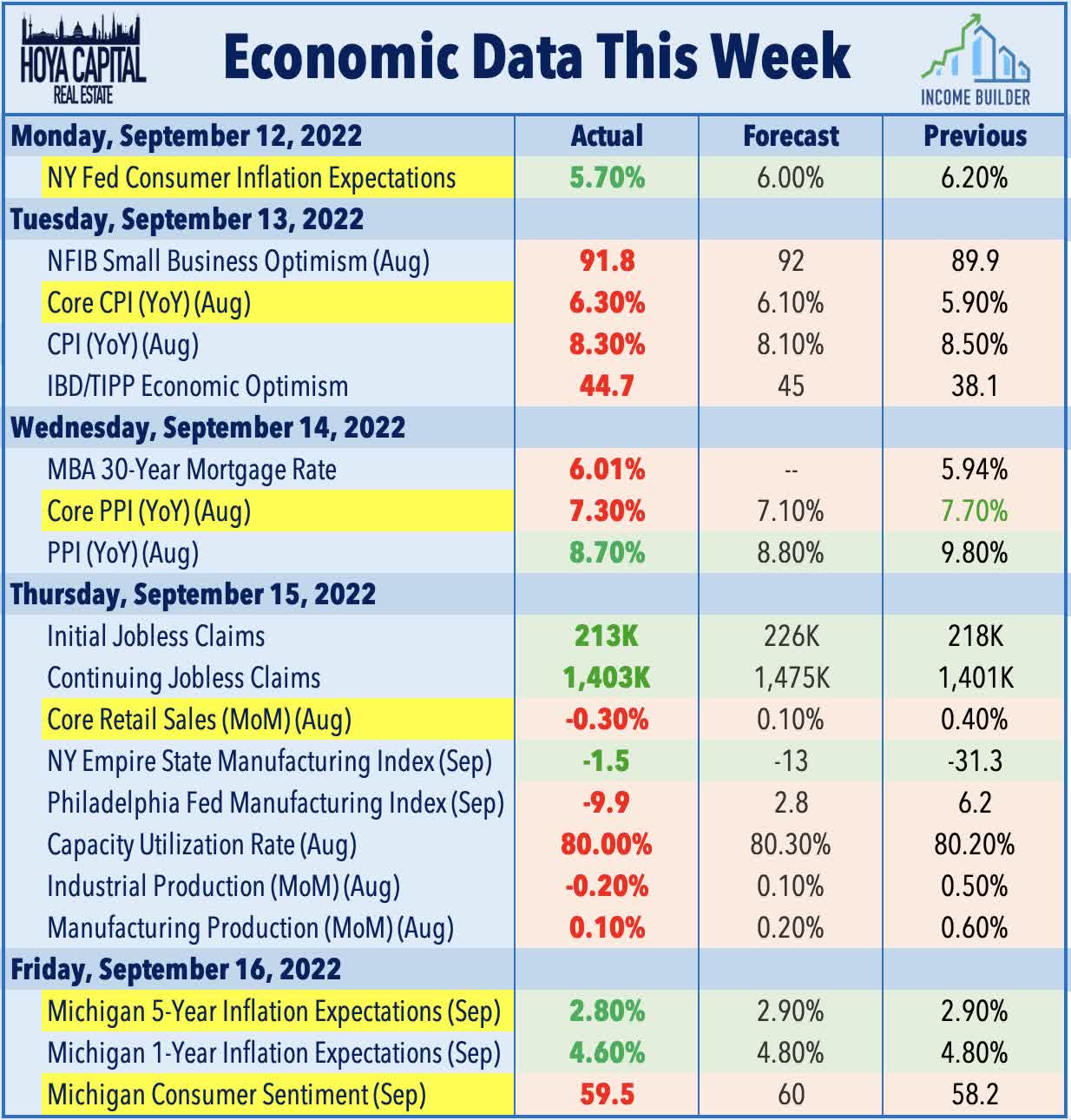

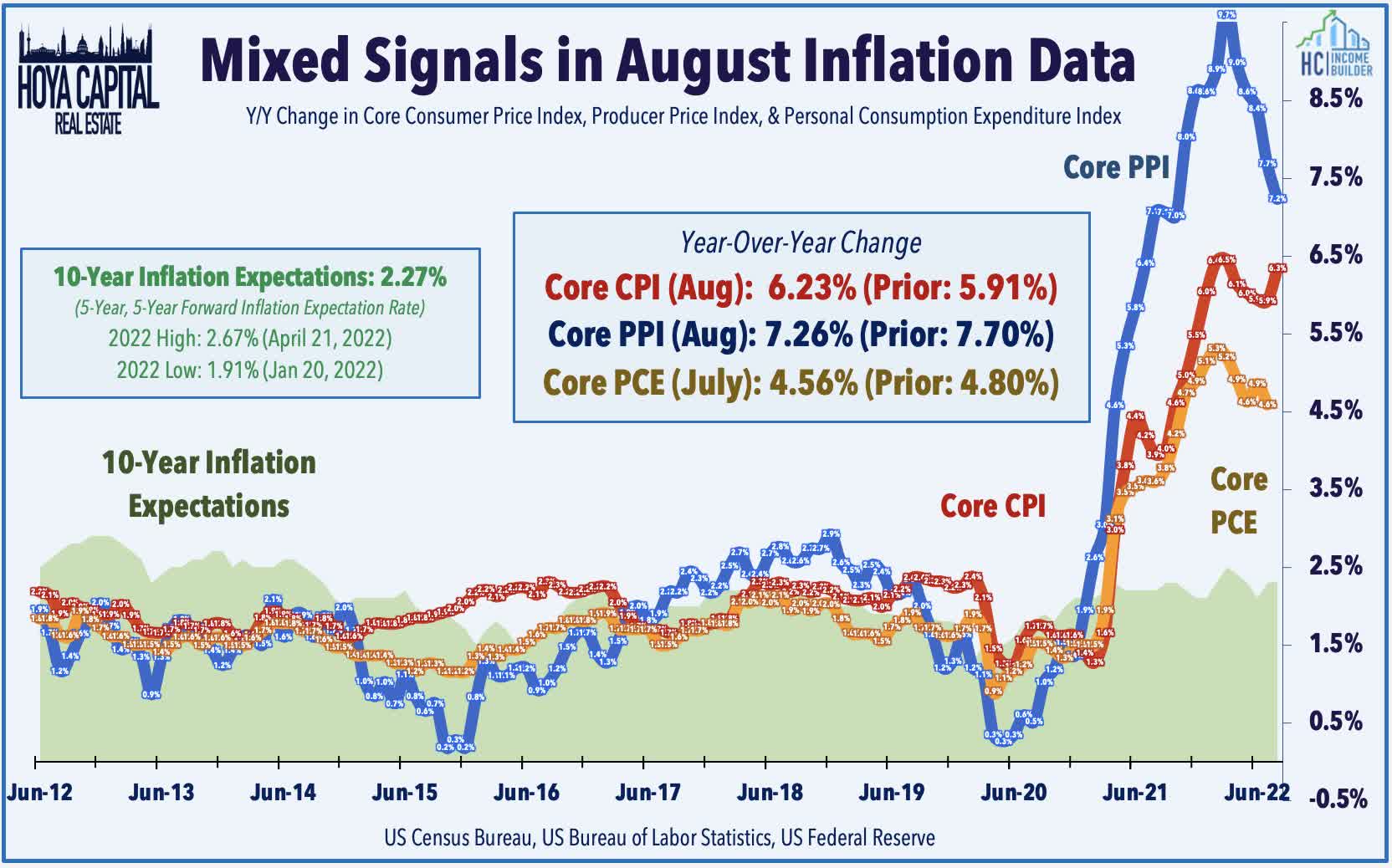

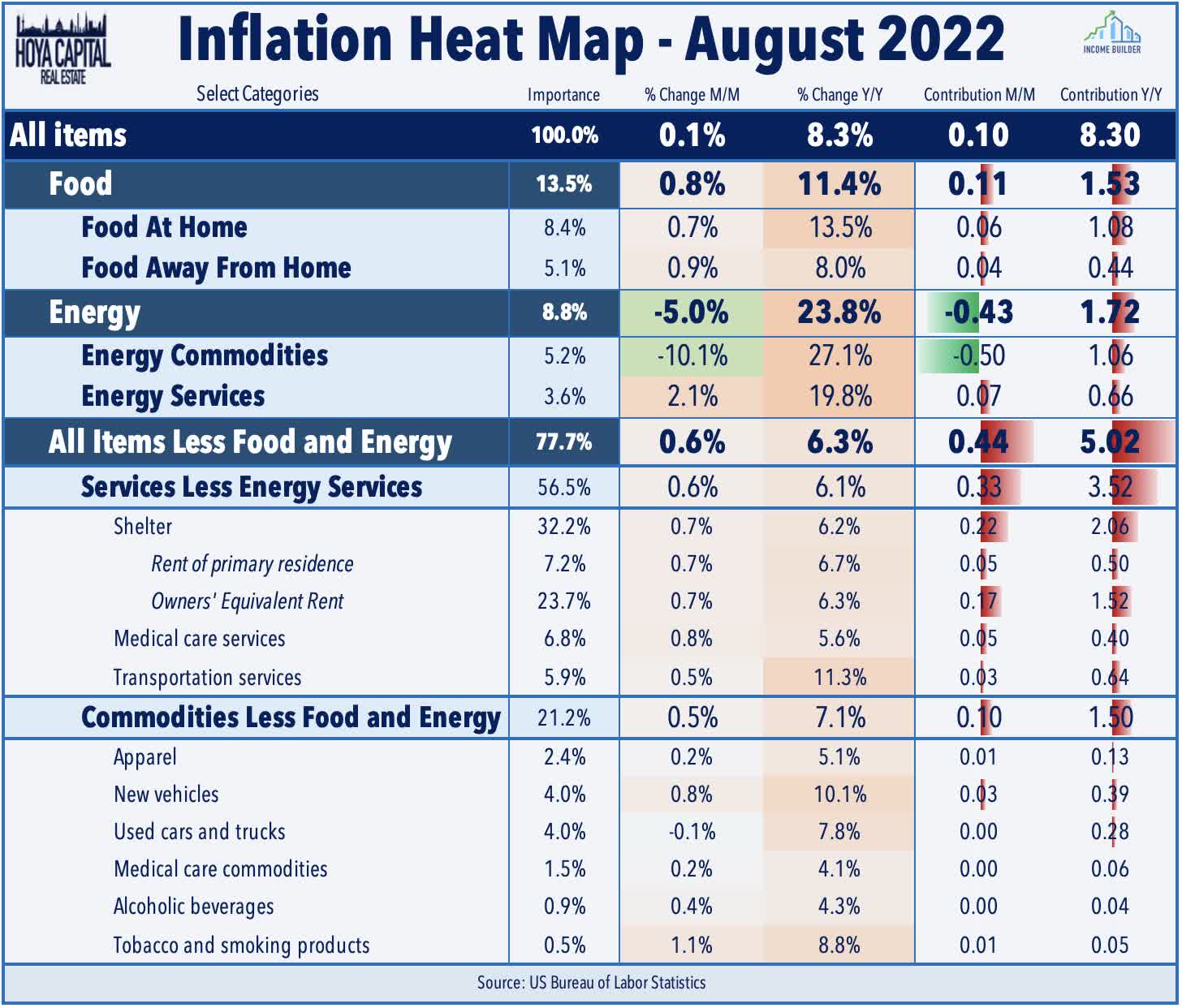

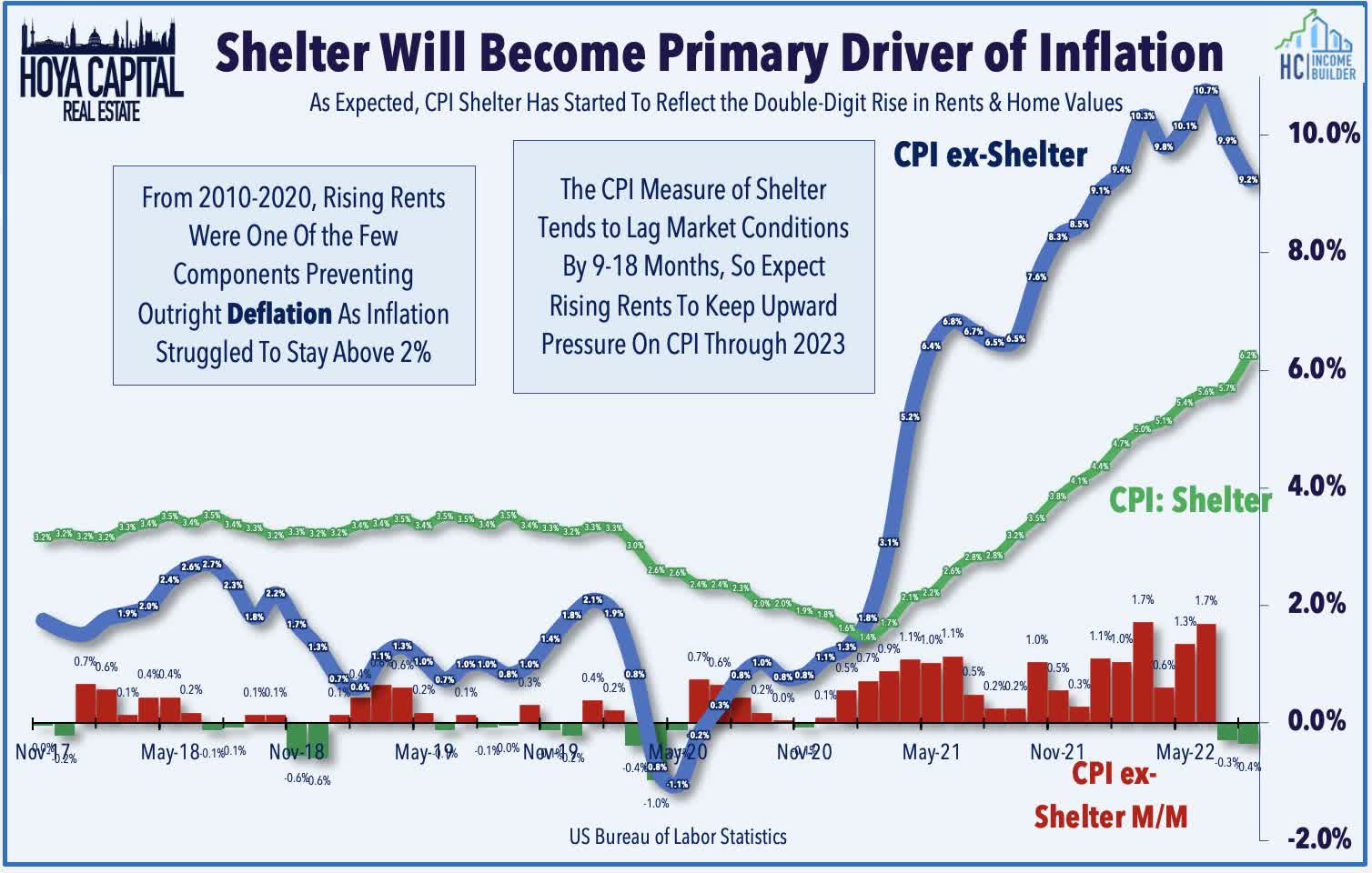

Peak Inflation? Well, it depends who you ask. While the closely-watched CPI report this week showed that consumer prices unexpectedly accelerated in August, the balance of the inflation reports this week showed that real-time price pressures have cooled considerably over the past quarter amid a sharp slowdown in global economic growth, underscored by the largest six-month plunge in the Citi US Inflation Surprise Index since 2006. The annual increase in the headline Consumer Price Index came in hotter-than-expected at an 8.3% year-over-year rate in August - hotter than the 8.1% expected - while Core CPI actually accelerated to a 6.3% annual rate - hotter than the 6.1% rate expected. Following the hotter-than-expected CPI report, investors received some better news on the inflation front the following day as wholesale prices fell in August for a second-straight month as plunging commodities prices cooled or reversed the pace of goods and transportation inflation.

{kind=link}

What goes around comes around. As we've cautioned for the last year, the CPI Index was substantially understating the real-time increase in the single-largest component of the index - Shelter - since mid-2021 due to the sampling methodology which only collects "same-unit" data twice per year . The Dallas Fed published a report highlighting the data issues at the BLS, finding a 16-month lag between the BLS inflation series and real-time market pricing of home prices and rents - and for several years we've highlighted the "smoothing" effects seen in the CPI: Shelter which effectively renders the index as a rolling two-year average of actual shelter inflation. Market-based indexes of rents and home values - including reports from residential REITs - recorded 10-20% year-over-year rental rate increases beginning in June 2021, but these double-digit increases have since moderated to levels that are more in-line with post-GFC averages. The delayed effects of this Shelter inflation is beginning to show up - and it's hitting quite hard.

{kind=link}

The shelter index rose 6.2% over the last year - the highest annual increase since 1982 - accounting for about 40% of the total increase in all items less food and energy. But while the month-over-month headline CPI increased by 0.1% in August - a disappointment that triggered the sharp sell-off across equity and bond markets - the CPI Excluding-Shelter Index posted its steepest decline since the pandemic, dipping 0.36% following a 0.29% decline in the prior month - the steepest two-month decline since the depths of the pandemic - suggesting that "real-time" inflation is indeed decelerating even as headline metrics suggest otherwise. Combined with the cooler-than-expected PPI report, declining survey-based measures of consumer inflation expectations seen in reports from the New York Fed and the University of Michigan , and the Cleveland Fed's Inflation Nowcast model which implies significant real-time price deflation over the past two months, it would appear that further monetary tightening would be a significant policy mistake.

{kind=link}

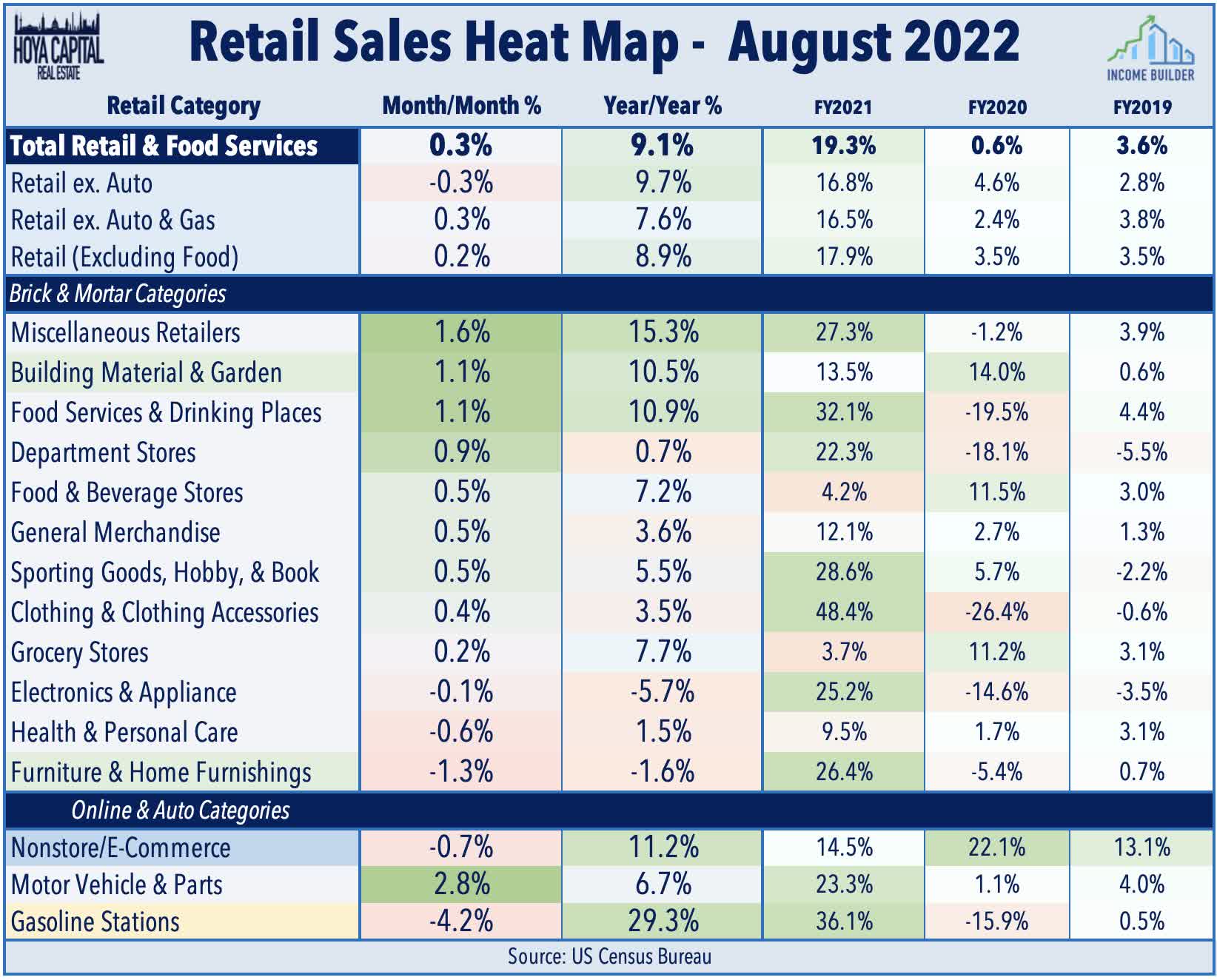

The balance of the major economic data reports this week were consistent with this theme - seemingly solid on the headline-figure, but weaker under the surface. The BLS reported that retail sales activity increased modestly in August, rising 0.3% on a month-over-month basis - a "beat" on the headline figure - but a downward revision to the prior month resulted in a weaker-than-expected total sales figure. On a year-over-year basis, total retail sales were higher by 9.1% - below the 9.3% forecast - as lower spending at the gasoline station was offset by an uptick in spending on automobiles, home improvement stores, and at restaurants. Excluding the volatile Motor Vehicles & Parts category - which jumped 2.8% for the month - sales decreased 0.3% in August, below the estimate for a 0.1% increase and likely reflecting some combination of lower "real" spending and declining prices.

{kind=link}

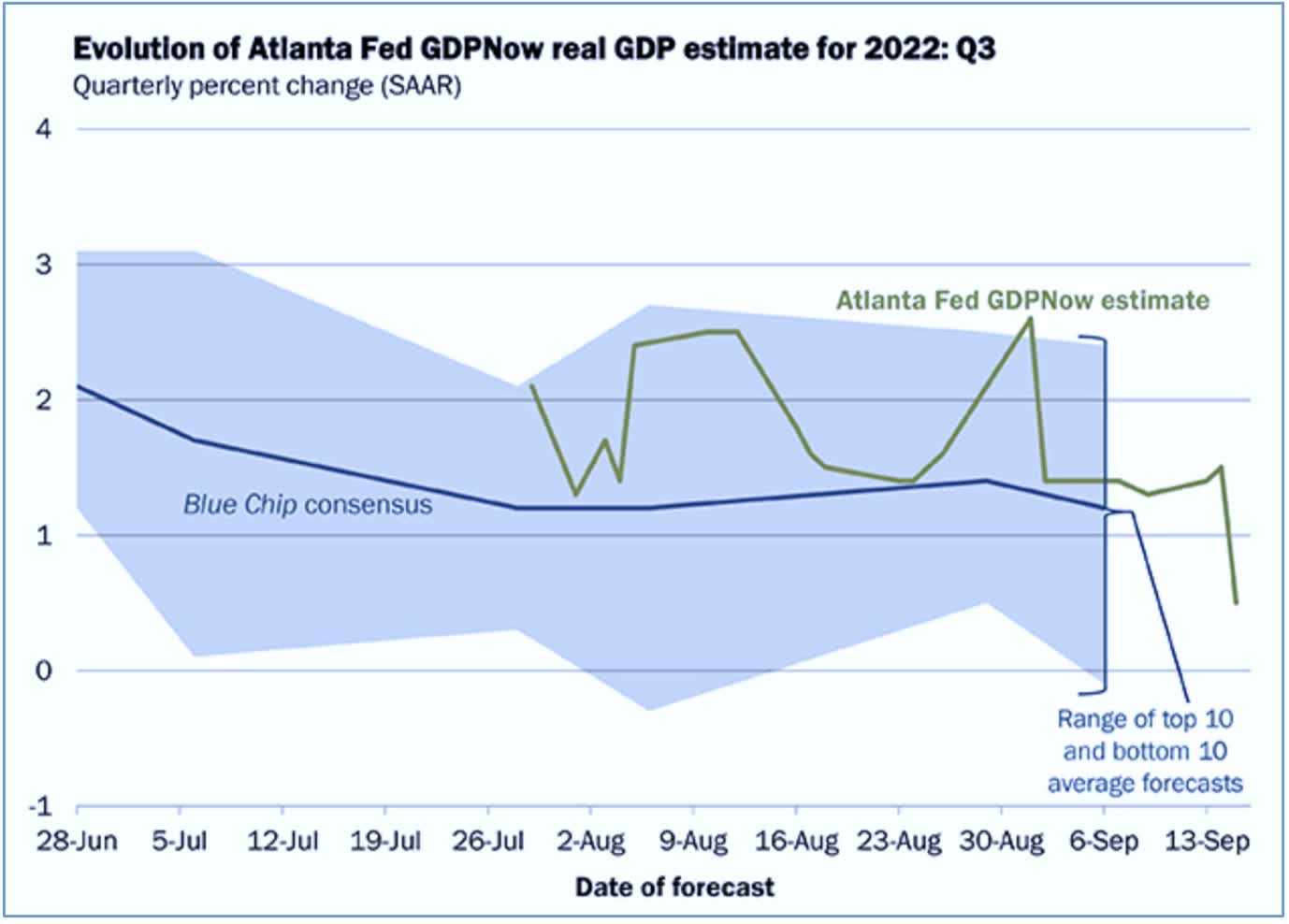

The weak retail sales data - together with the weaker-than-expected industrial production data - prompted another downward revision to the Atlanta Fed's GDPNow model, which is now dangerously close to projecting a third-straight quarter of GDP contraction. The Atlanta Fed's model - which accurately foretold the unexpected contraction last quarter - now forecasts GDP growth of just 0.5% in Q3 - down sharply from its 2.6% forecast two weeks ago. The Atlanta Fed's metric tracking the Blue Chip consensus - based on the monthly Blue Chip Economic Indicators survey - now projects negative GDP growth at the median in its latest survey, down sharply from the prior forecast of 1.3%. Third quarter GDP will be released on October 28th - less than two weeks before the U.S. midterm elections. The U.S. has not recorded three-straight quarters of GDP contraction since the Great Financial Crisis.

{kind=link}

Equity REIT Week In Review

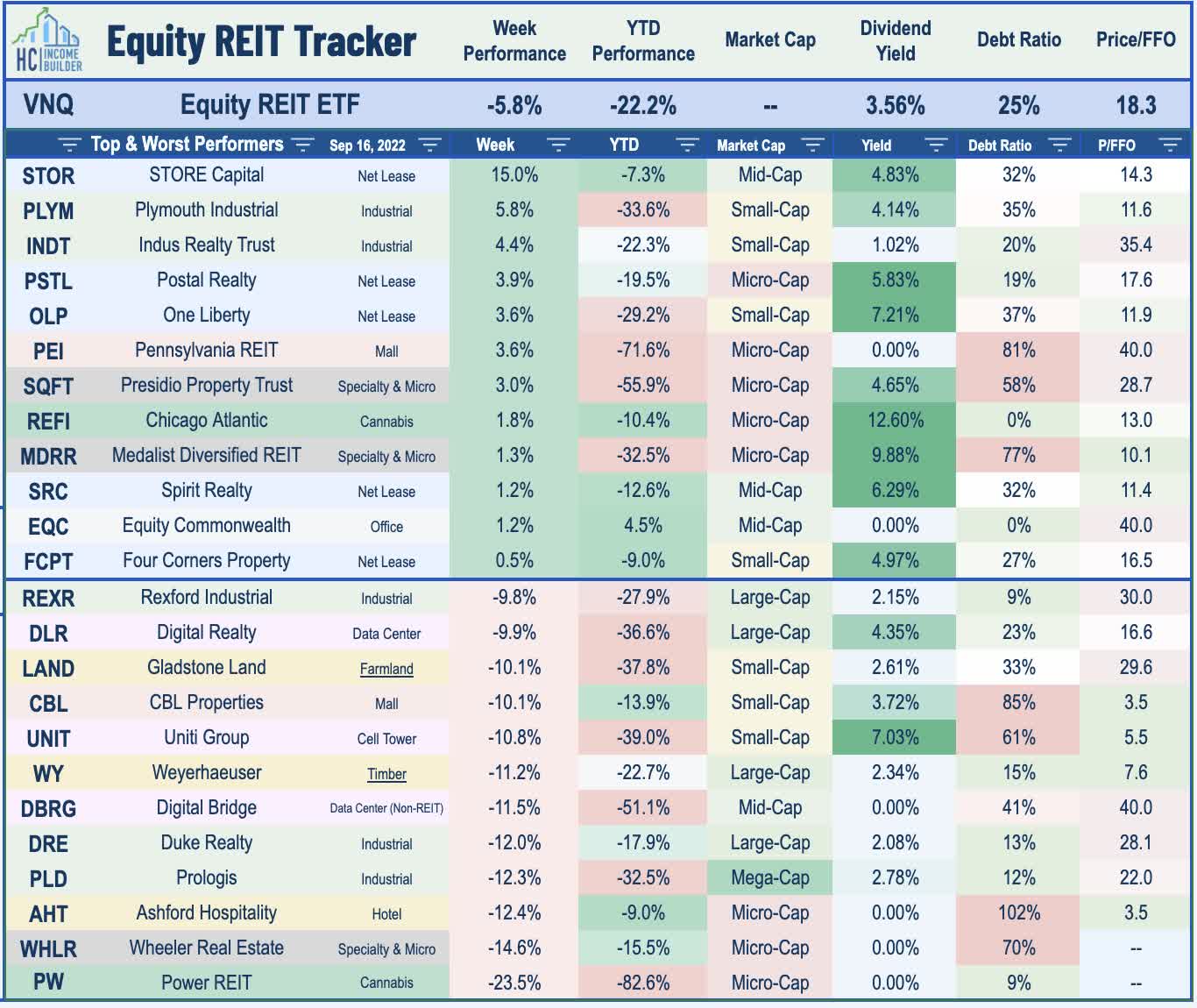

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

There were several bright-spots amid an otherwise rough week of performance across the real estate sector. Four more REITs raised their dividends this week, bringing the full-year total across the real estate sector to 106. Innovative Industrial ( IIPR ) - which has been slammed this year on concerns over credit and rent payment issues among its cannabis cultivator tenants - hiked its quarterly dividend by 3% while fellow cannabis REIT NewLake Capital Partners ( OTCQX:NLCP ) hiked its quarterly dividend by 6% - its second hike this year. Realty Income ( O ) - the largest net lease REIT - raised its monthly dividend by 0.2% to $0.248/share. Elsewhere, hotel REIT Xenia Hotels ( XHR ) resumed its dividend that had been suspended since July 2022, declaring a $0.10/share quarterly dividend , representing a forward yield of roughly 2.5%.

{kind=link}

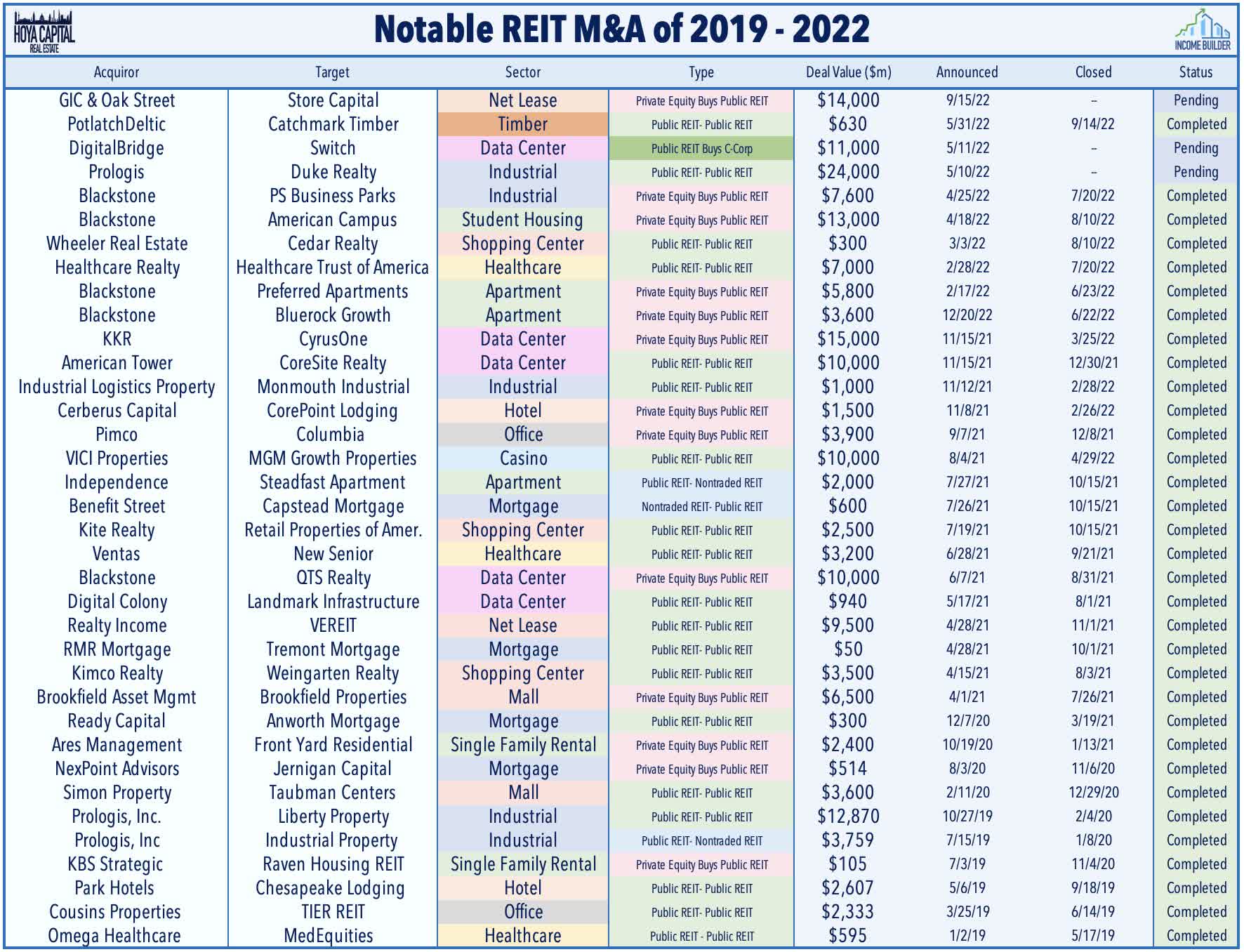

Net Lease : STORE Capital ( STOR ) - our second largest holding in the REIT Focused Income Portfolio - surged 15% on the week after it announced that it reached a deal to be acquired by GIC and Blue Owl's Oak Street for $32.25 in cash - a 20.4% premium to STOR's last closing price. The deal is expected to close in Q1 2023 and STOR's third-quarter dividend will be its final dividend until the closing. The closing of the transaction is not subject to any financing conditions and the definitive merger agreement includes a 30-day "go-shop" period that will expire on October 15, 2022. The acquisition of STOR - the third largest net lease REIT behind Realty Income ( O ) and W. P. Carey ( WPC ) follows a quiet four months of REIT major M&A. We analyzed the net lease sector in a report published this week - Net Lease REITs: Inflation Risk Persists - which analyzed why net lease REITs are still on-pace for double-digit earnings growth even as rent growth has significantly lagged inflation.

{kind=link}

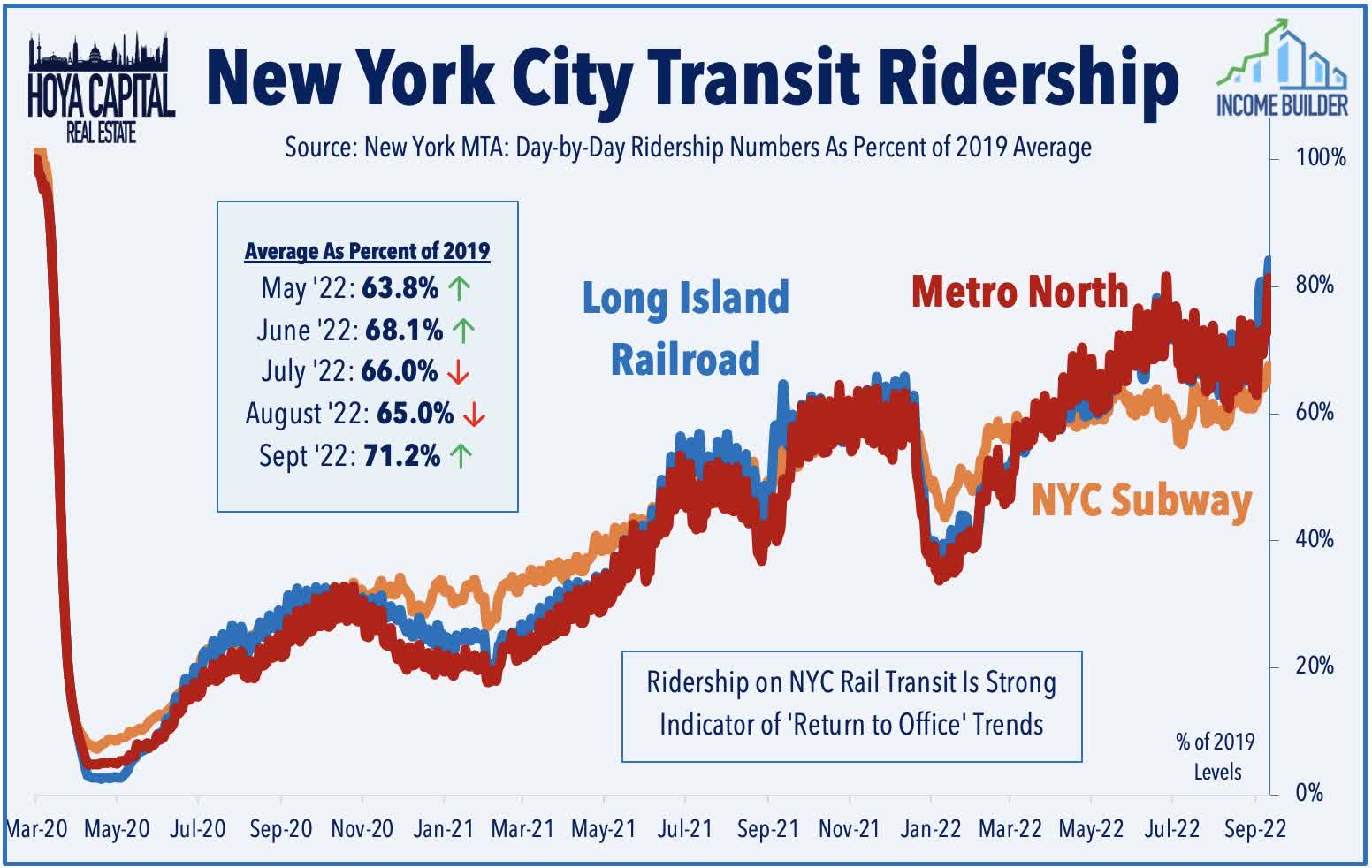

Office : Also among the better-performing sectors this week, office REITs were buoyed by reports indicating that the long-awaited 'return to the office' has finally picked-up the pace. Recent ridership data from the New York MTA - which has historically correlated with office utilization data from Kastle and others - indicates that many workers appear to indeed be returning to the office after the Labor Day holiday. The 10-Day average ridership on NYC's Rail system increased to its highest level since the pandemic at nearly 80% by the end of last week. NYC-focused REIT SL Green ( SLG ) was among the better performers this week after announcing a pair of transactions. Following a long-running dispute with Chinese-based HNA Group, SLG will fully acquire 45 Park Avenue - a 1.8M-square-foot, 44-story, Class A office property near Grand Central Station and plans to redevelop the property. SLG also announced that it will sell 414,317 SF of space it owns at 885 Third Avenue, better known as "The Lipstick Building" to Memorial Sloan Kettering Cancer Center for $300.4M and will retain the remaining 219k SF.

{kind=link}

Hotel : Sunstone Hotel ( SHO ) was among the better performers this week after it provided a business update which noted that it achieved an Average Daily Rate in Q3 that was 16.9% higher than the same period in 2019, which offset a 14.5-percentage-point drop in occupancy compared to the 2019-level, resulting in total Revenue Per Available Room that was 2.7% below 2019-levels. Hersha Hospitality ( HT ) dipped 6% on the week despite announcing a deal to sell two of its West Coast properties - Hotel Milo Santa Barbara and Pan Pacific Seattle - for $125MM, or approximately $455,000 per key and intends to use the proceeds from the sale to pay down approximately $45M of debt. According to recent TSA Checkpoint data , travel demand has again moderated a bit over the past couple weeks following a late-summer surge that saw throughput exceed 100% of pre-pandemic levels for the first time since March 2020. Meanwhile, STR reported that U.S. hotel Revenue Per Available Room ("RevPAR") was 24.6% above 2019-levels in the Labor Day week as Occupancy Rates improved to 103% of 2019-levels while Average Daily Rates were 20.9% above the pre-pandemic average.

{kind=link}

Storage : Among the hardest-hit property sectors on the week, storage REITs were slammed despite a strong read-through on Producer Price Index data showing effective year-over-year self-storage rent growth of over 16% in August. This week, Extra Space ( EXR ) announced a $590M acquisition of Storage Express, which owns 107 storage properties in Indiana, Ohio, Illinois, and Kentucky. The acquisition included all Storage Express assets, including trademarks, contracts, licenses, intellectual property and 14 future development sites. EXR also acquired a storage software operating platform dubbed E-Tracker, which supports Storage Express locations. The deal was funded partly by the issuance of $125.0M in operating partnership units, with the cash balance drawn from its credit facilities, the company said. As discussed in our recent Storage REIT report, acquisition and consolidation opportunities should remain plentiful over the next decade for these storage REITs following the late-2010s supply boom, and we have indeed seen acquisition activity ramp up over the past several quarters as these REITs acquired more than $13B in assets over the past year.

{kind=link}

Casino : This week we published Casino REITs: Taking Some Chips Off the Table on the Income Builder Marketplace. The lone property sector in positive-territory this year, Casino REITs have defied macro headwinds much like their traditional net lease peers, benefiting from an upward valuation re-rating and institutional acceptance. Casino REITs have become a favorite for investors seeking inflation-hedged assets. VICI Properties ( VICI ) boasts inflation-linked escalators on 96% of its leases while Gaming and Leisure Properties ( GLPI ) benefits from indirect inflation hedges linked to tenant performance. The recent outperformance can be attributed to VICI's inclusion in the S&P 500 in June following its merger with MGM Properties, becoming the fastest REIT to be included in the benchmark. For the critical Las Vegas market, robust leisure demand has fueled a near-full recovery in hotel occupancy despite still-weak convention-related demand, but we note that tenant operators aren't immune from the risks of a potentially prolonged recession.

{kind=link}

Mortgage REIT Week In Review

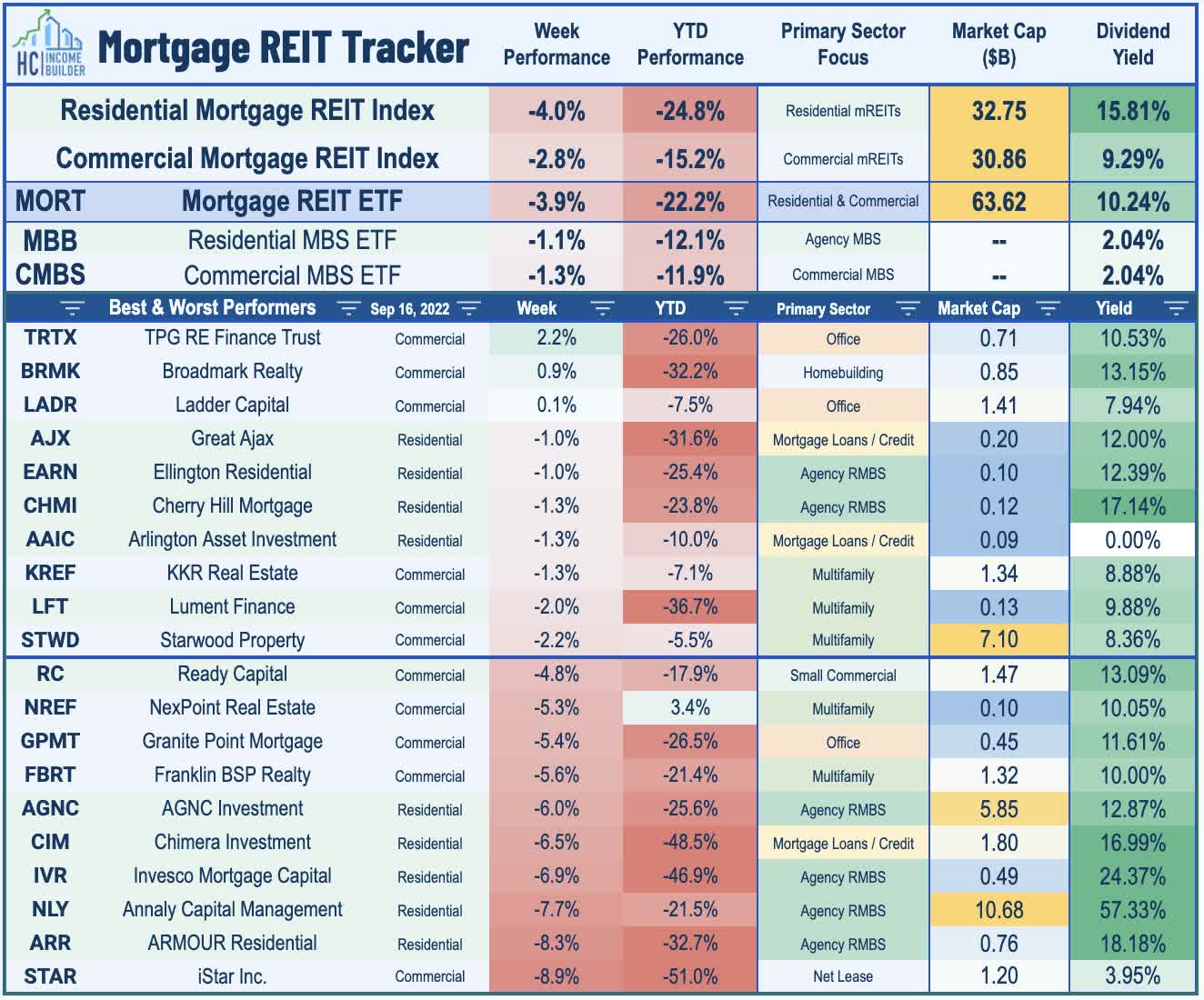

Mortgage REITs also were actually relative outperformers on the week despite continued pressure on mortgage-backed bond ( MBB ) valuations that have now erased all of their mid-year rebound from mid-June through early August amid the hawkish pivot in Fed commentary. Ladder Capital ( LADR ) was among the leaders this week after it hiked its quarterly dividend for the second time this year to declare $0.23/share, a 4.5% increase from its prior dividend of $0.22 - one of 13 mREITs that has raised its dividend this year. On the flip side, Orchid Island ( ORC ) confirmed its new post-reverse-split monthly dividend rate of $0.16/share - one of 4 mREITs that have cut their dividend this year. More than a dozen mREITs declared dividends that was consistent with their current levels this week including Starwood Property ( STWD ), Blackstone Mortgage ( BXMT ), AGNC Investment ( AGNC ), KKR Real Estate ( KREF ), and TPG Real Estate ( TRTX ).

{kind=link}

REIT Capital Raising & REIT Preferreds

The Hoya Capital REIT Preferred Index finished lower by 1.9% this week - slightly underperforming the broader iShares Preferred and Income Securities ETF ( PFF ) which declined 1.4% - and pushing its year-to-date declines back to roughly 15.5% on a price return basis. This week, AGNC Investment's ( AGNC ) new preferred series began trading - its 7.75% Series G Fixed-Rate Cumulative Redeemable Preferred Stock under the symbol AGNCL. AGNC noted last week that it intends to use the $150M net proceeds to expand its portfolio and general corporate purposes which it noted may include the redemption of its 7.000% Series C ( AGNCM ) Fixed-to-Floating Preferred. It was a quiet week of REIT capital raising activity, but of note, Moody's affirmed Regency Centers' ( REG ) "Baa" credit rating and revised its outlook to positive from stable.

{kind=link}

2022 Performance Check-Up

Nearing the end of the third quarter, Equity REITs are now lower by 22.2% on a price return basis for the year while Mortgage REITs are also lower by 22.2%. This compares with the 18.8% decline on the S&P 500 and the 16.3% decline on the S&P Mid-Cap 400. Within the real estate sector, casino REITs are now the lone property sector in positive territory for the year while ten REIT sectors are lower by at least 20%. At 3.45%, the 10-Year Treasury Yield has climbed 194 basis points since the start of the year - its highest weekly closing-level since May 2010 - and well above its prior ten-year highs of 3.25% seen back in late 2018. The Two-Year Treasury Yield , meanwhile, closed the week at its highest level since November 2007.

{kind=link}

Economic Calendar In The Week Ahead

While all eyes will be on the Federal Reserve in the week ahead, we'll also see a jam-packed slate of housing data - the industry that is bearing the brunt of the aggressive tightening path through the historic surge in mortgage rates. On Monday, we'll see NAHB Homebuilder Sentiment data for September which is expected to decline to the lowest level since 2014 - excluding the brief pandemic dip in April and May 2020. On Tuesday, we'll see Housing Starts and Building Permits data which is expected to show a further pull-back in home construction activity to post-pandemic lows. On Wednesday, Existing Home Sales data is also expected to dip to the lowest levels since 2014 excluding the pandemic shutdown months. The main event will be on Wednesday with the FOMC Interest Rate Decision in which Fed is expected to hike rates by 75 basis points for a third-straight meeting to a 3.25% upper-bound - levels last seen in July 2005.

{kind=link}

For an in-depth analysis of all real estate sectors, be sure to check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Fed Keeps Chasing Its Tail