PACWP - Fed Not Done But Should Be

2023-05-29 09:00:00 ET

Summary

- U.S. equity markets hovered around nine-month highs this past week as surprisingly solid economic data and earnings reports offset pressures from hawkish central bank rhetoric and a debt ceiling stalemate.

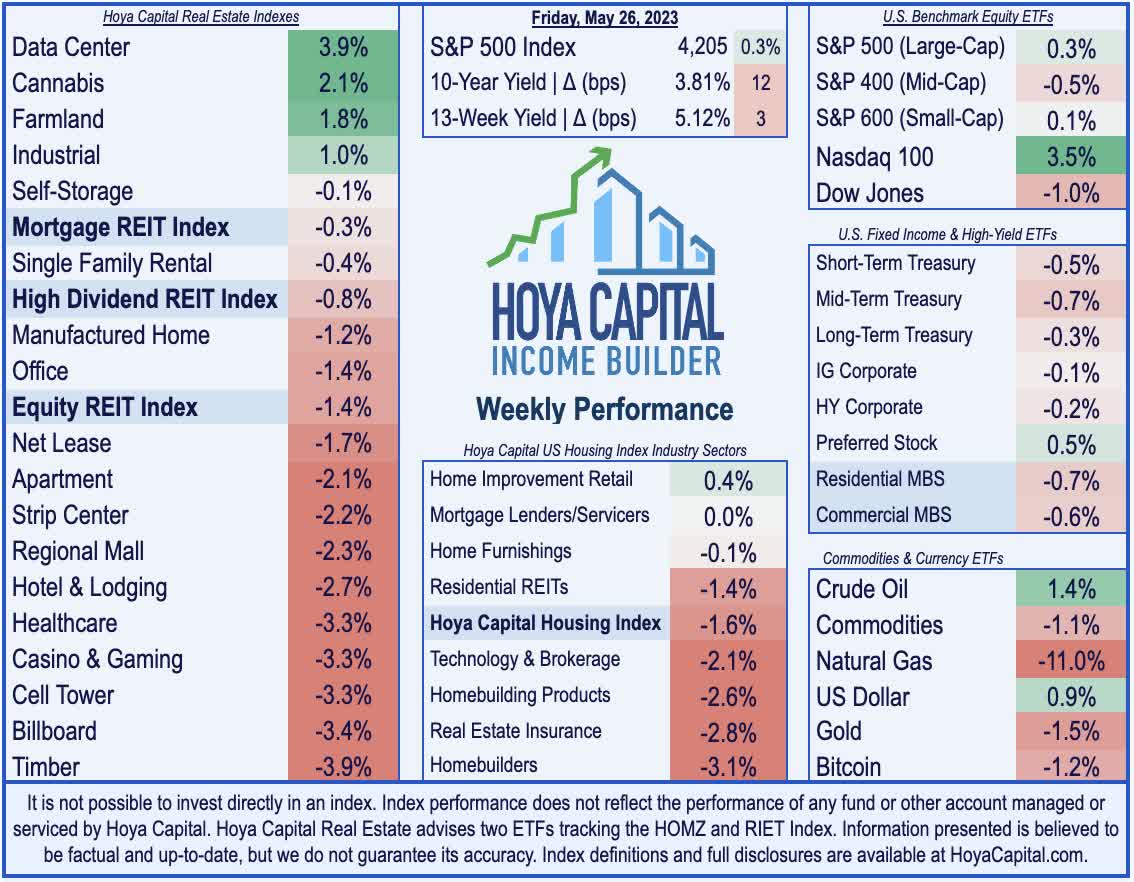

- Posting its highest end-of-week close since August, the S&P 500 advanced 0.3% this week while the tech-heavy Nasdaq 100 rallied 3.5% to set fresh 52-week highs.

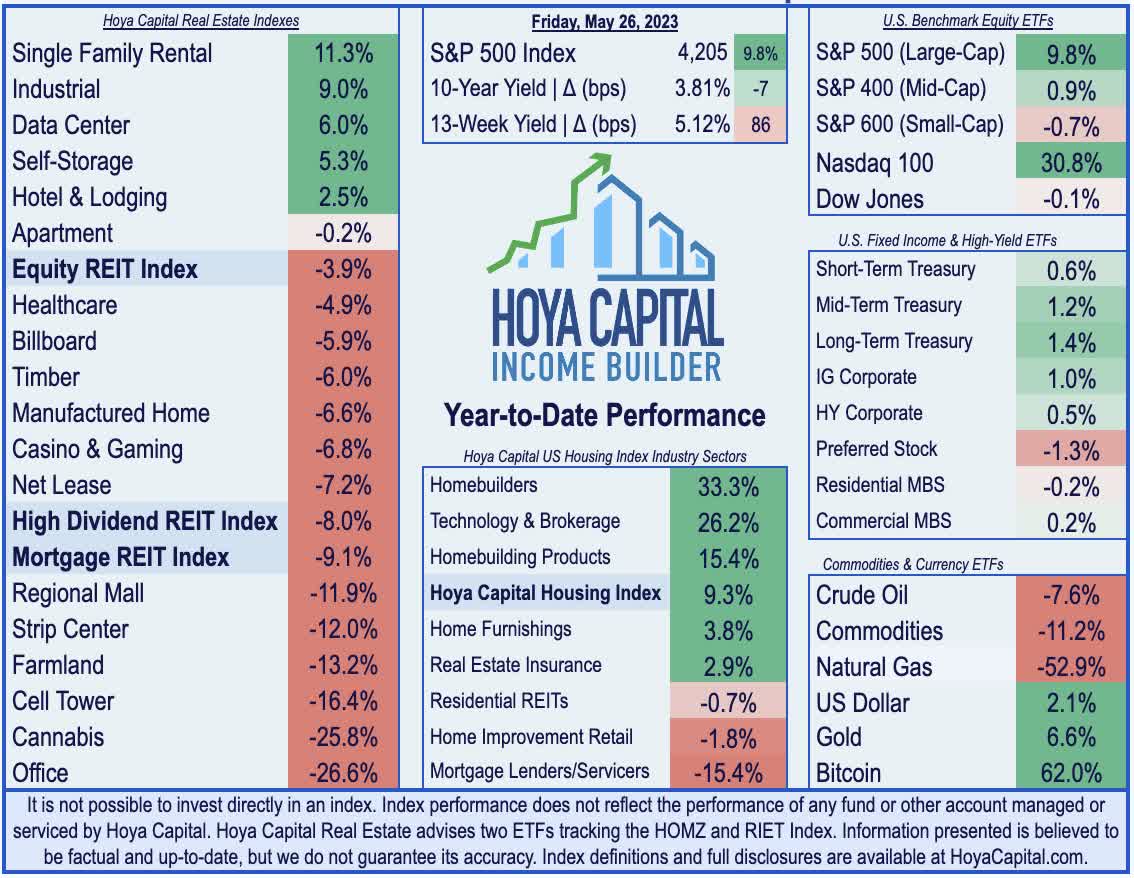

- Real estate equities were also laggards for a second-straight week, however, pressured by a rebound in benchmark interest rates. The Equity REIT Index declined 1.4% while Mortgage REITs declined 0.3%.

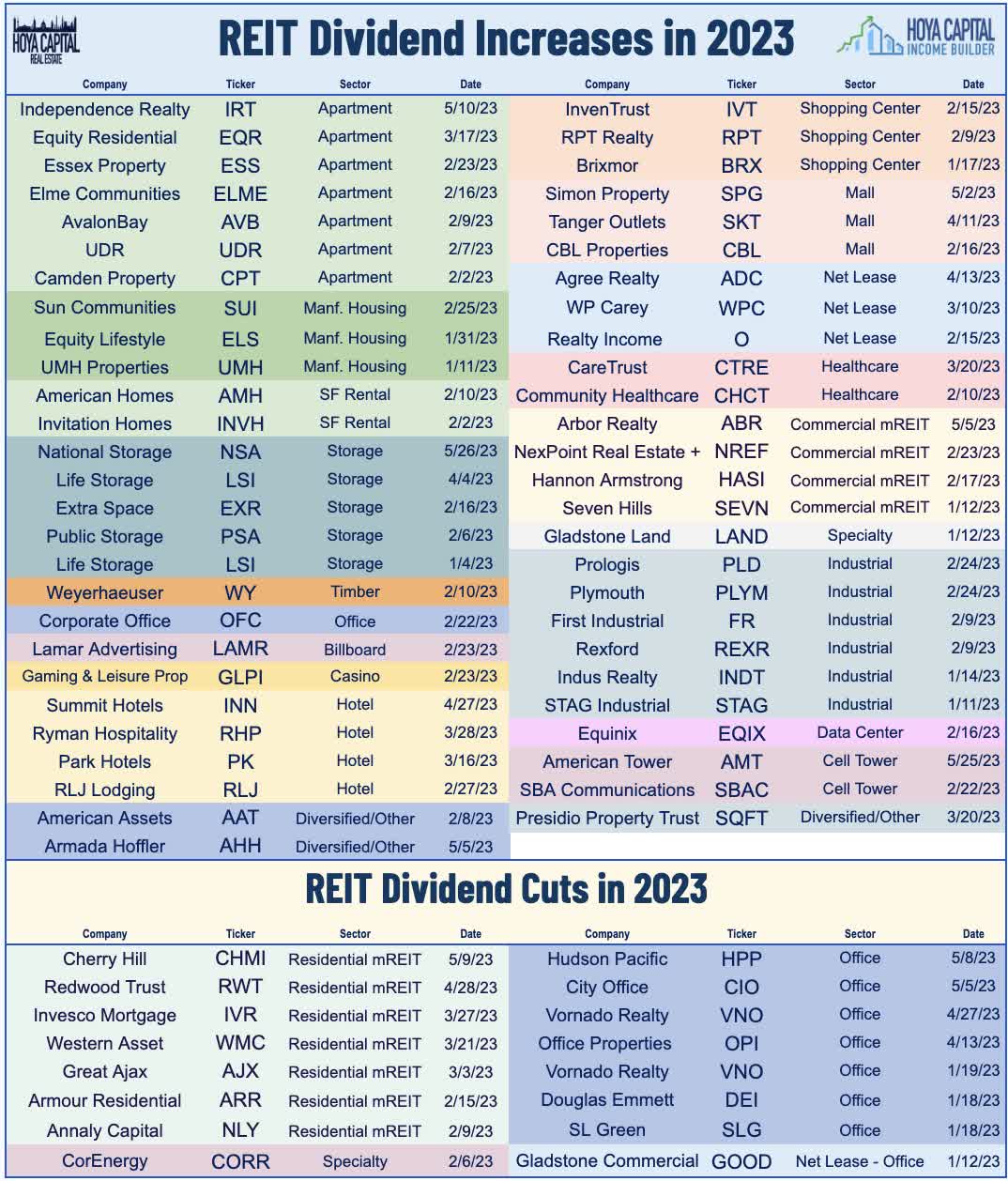

- Another week, another handful of REIT dividend hikes. National Storage and American Tower both raised their dividends. 53 REITs have raised their dividends this year, while 16 have lowered payouts.

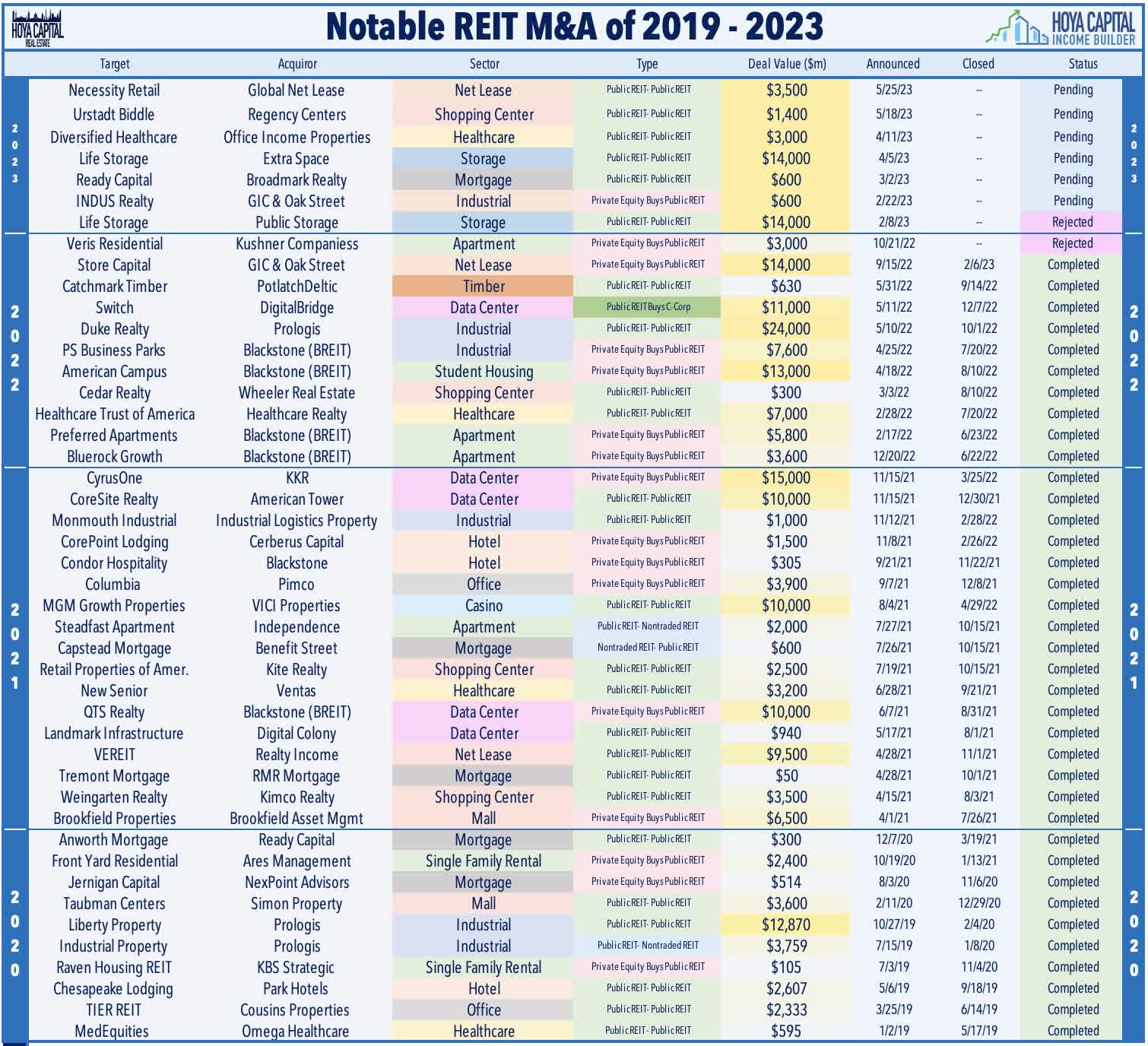

- M&A was also a theme in the REIT space as a pair of externally-managed REITs advised by AR Global - Global Net Lease and Necessity Retail REIT - announced plans to merge and internalize their management under the Global Net Lease banner.

Real Estate Weekly Outlook

This is an abridged version of the full report and rankings published on Hoya Capital Income Builder Marketplace on May 26th.

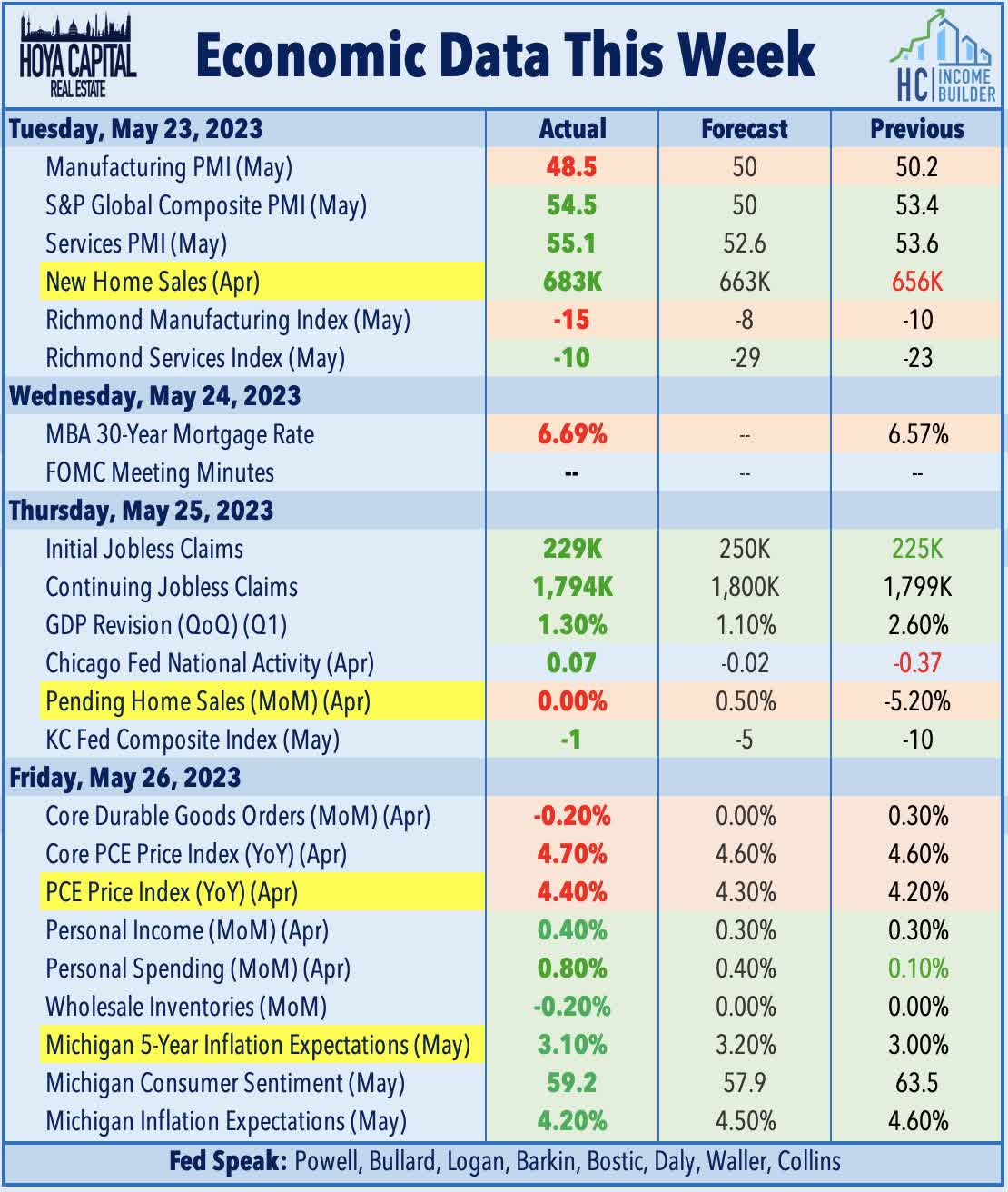

U.S. equity markets hovered around nine-month highs this past week as surprisingly strong economic data and earnings reports offset pressures from hawkish central bank rhetoric and an ongoing debt ceiling stalemate. Benchmark interest rates rose to their highest level since March as Fed officials continue to talk tough on the need for further monetary tightening, a hawkish outlook that gathered some support this week by economic data showing continued resilience in labor markets, stabilization in housing markets, and some persistence in the headline inflation metrics in both the U.S. and Europe.

{kind=link}

Posting its highest end-of-week close since August, the S&P 500 advanced 0.3% this week, while the tech-heavy Nasdaq 100 rallied 3.5% to set fresh 52-week highs. Gains this week were notably top-heavy, however, as the Mid-Cap 400 slipped 0.5% while the Small-Cap 600 finished flat. Real estate equities were also laggards for a second-straight week, pressured by the rebound in benchmark interest rates. The Equity REIT Index declined 1.4% this week, with 14-of-18 property sectors in negative territory, while the Mortgage REIT Index finished lower by 0.3%. A rebound in mortgage rates also pressured homebuilders and the broader Housing Index , offsetting strong earnings results from luxury homebuilder Toll Brothers and data showing a reacceleration in New Home Sales to 13-month highs.

{kind=link}

The relatively strong slate of economic data, a slightly hotter-than-expected inflation print, and concern over a potential technical default lifted the 2-Year Treasury Yield and 10-Year Yield to their highest levels since the collapse of Silicon Valley Bank in early March. Among the notable bits of Fed commentary this week, St. Louis Fed President Bullard said that he believes that two more rate hikes are necessary this year, while Minneapolis Fed President Kashkari - who is one of the twelve voting members - commented , "it's a close call either way: raising another time in June or skipping." Swaps markets now imply a 65% chance of a June hike, up from less than 5% in mid-May after their prior meeting. Technology ( XLK ) stocks powered the gains this week following strong earnings results from Nvidia ( NVDA ), while other more-defensive and yield-sensitive segments were under pressure. The Commodities ( DJP ) declined to their lowest-level of the year this week and are now more than 25% lower on a year-over-year basis.

{kind=link}

Real Estate Economic Data

Below, we recap the most important macroeconomic data points over this past week affecting the residential and commercial real estate marketplace.

{kind=link}

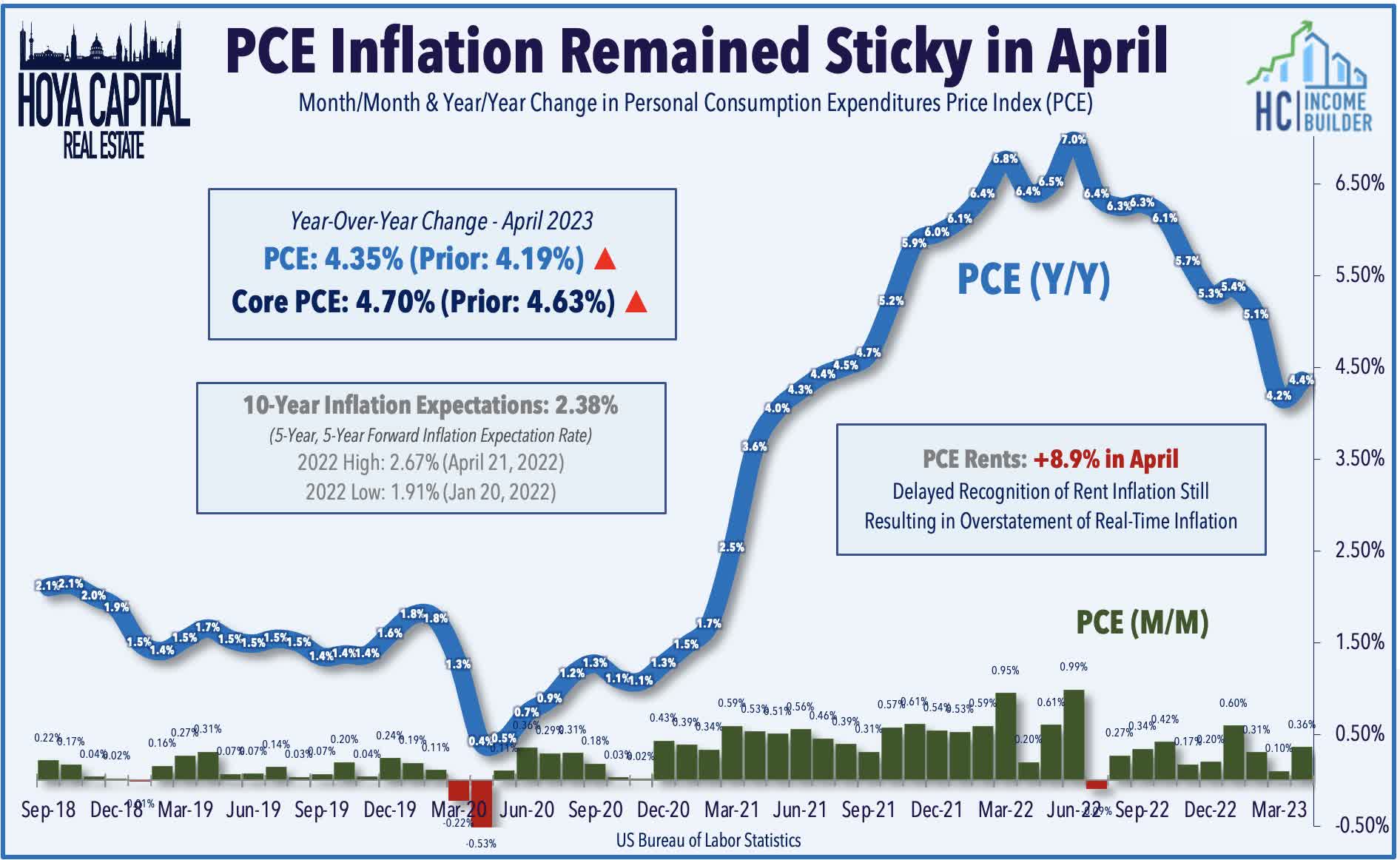

Snapping the stretch of "good news" on the inflation front seen over the past several months, the closely-watched PCE Index posted a hotter-than-expected reading in April driven, in part, by the delayed recognition of rent and home price increases seen from mid-2021 through mid-2022. The Personal Consumption Expenditures (PCE) Price Index rose 0.4% in April - the highest increase since January - after rising 0.1% in March. In the 12 months through April, the PCE Index increased 4.35% - a slight reacceleration from the 4.19% increase in March. Notably, the PCE Index suffers from similar distortions from the lagging recognition of shelter inflation as the CPI Index. The housing component of the PCE Index increased more than 8% in April despite real-time metrics showing that rents and home prices are roughly flat on a year-over-year basis. Excluding housing, we calculate a 2.9% year-over-year increase in the PCE Index, which is already roughly in-line with the Fed's target. We observe similar effects with the CPI Index, noting that when the BLS Rent Index is replaced with the Zillow ZRI Rent Index, we observe that "real-time CPI" is averaging only 1% over the past nine months.

{kind=link}

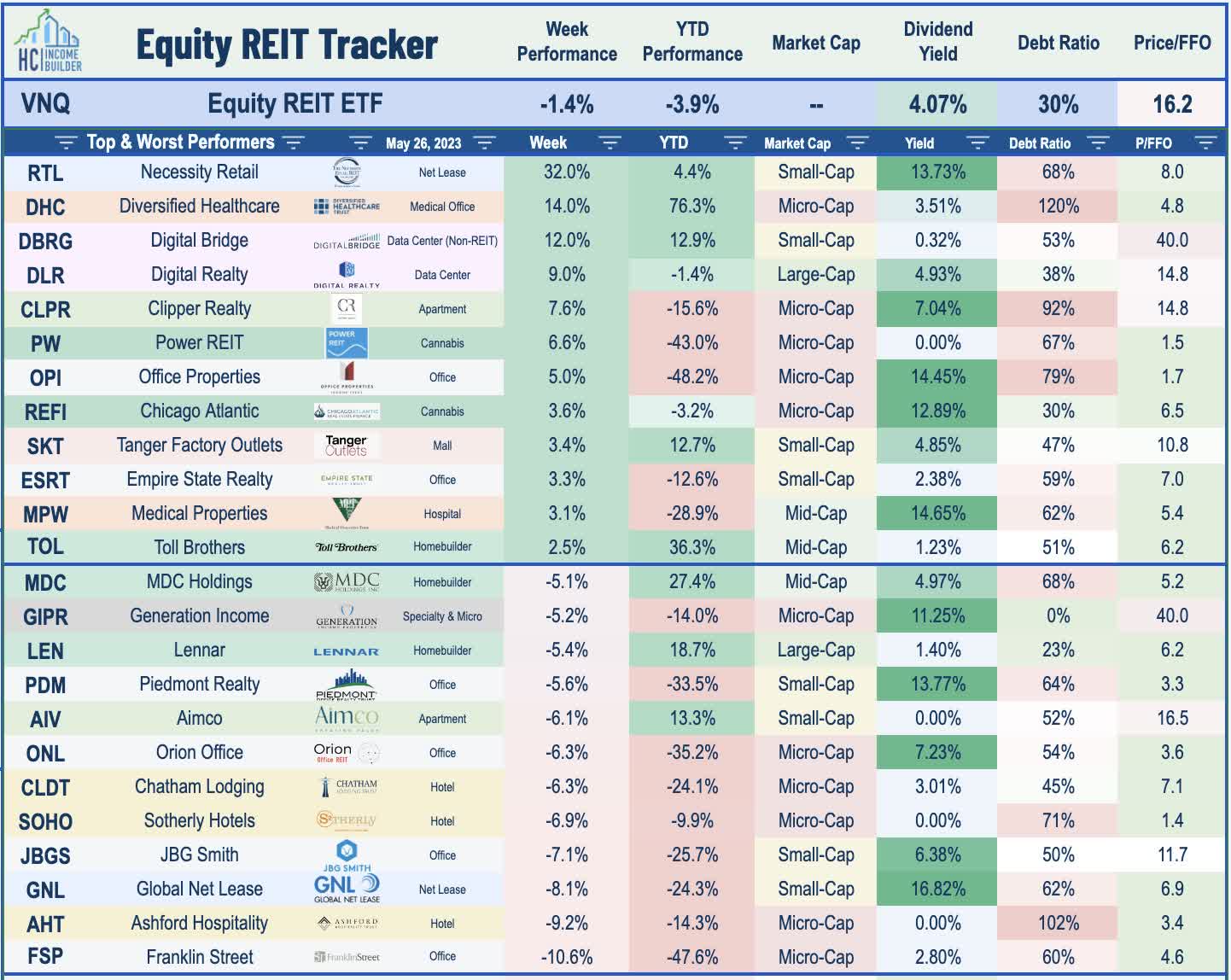

Equity REIT Week In Review

Best & Worst Performance This Week Across the REIT Sector

{kind=link}

Another week, another handful of REIT dividend hikes. National Storage ( NSA ) - which we own in the Focused Income Portfolio - raised its quarterly dividend by 2% to $0.56/share, representing a forward dividend yield of roughly 6.2%. American Tower ( AMT ) raised its quarterly dividend by 1% to $1.57/share, but the one-cent increase for the second quarter was below AMT's historical average increase of two cents. The pair of dividend increases lifted the full-year total across the REIT sector to 53, which are offset by 16 dividend cuts. Meanwhile, a trio of office REITs maintained their dividends despite speculation that cuts may be imminent. Brandywine Realty ( BDN ) maintained its quarterly dividend at $0.19/share , representing a dividend yield of roughly 20.5%. Kilroy Realty ( KRC ) maintained its dividend at $0.54/share, representing a dividend yield of 8.0%. Douglas Emmett ( DEI ) maintained its dividend at $0.19/share , representing a dividend yield of 6.7%. Apartment REIT AvalonBay ( AVB ), storage REIT Extra Space ( EXR ), and data center REIT Digital Realty ( DLR ) also held their dividends steady.

{kind=link}

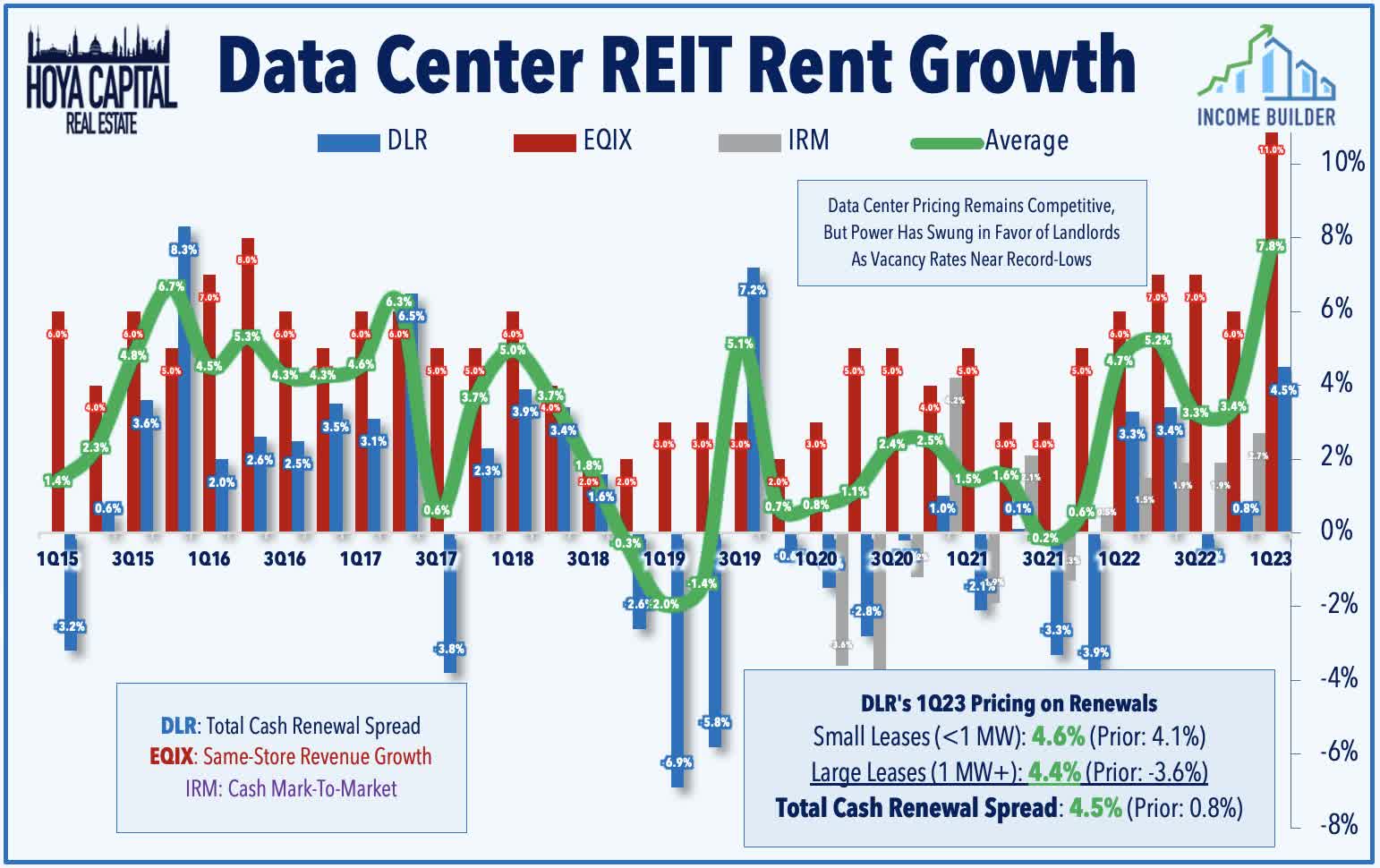

Data Centers : Speaking of Digital Realty ((DLR)), the data center REIT rallied 9% on the week after chip maker Nvidia ((NVDA)) reported blowout first-quarter results driven by strength in its data center business. Nvidia - which surged more than 20% this week to bring its market cap to the cusp of $1 trillion - said that it is "significantly increasing its supply of data center chips" to meet "surging" demand resulting from investments in artificial intelligence ("AI"). NVDA commented, "a trillion dollars of installed global data center infrastructure will transition from general purpose to accelerated computing as companies race to apply generative AI into every product, service and business process." In our REIT Earnings Recap , we noted that data center REITs have seen improved pricing power in recent quarters as supply/demand conditions have tightened after a three-year stretch of lackluster rent growth. Last month, Equinix ( EQIX ) raised its full-year revenue and FFO outlook while also recording its strongest quarter of same-store revenue growth on record at 11%. Digital Realty reported similarly strong pricing trends, with renewal rent spreads rising 4.5% - its strongest quarter since 2019.

{kind=link}

Net Lease : M&A was also a theme this week as a pair of externally-managed REITs advised by AR Global - Global Net Lease ( GNL ) and Necessity Retail REIT ( RTL ) - announced plans to merge and internalize their management under the Global Net Lease banner. Management cited the benefits of improved scale, reduced leverage, and operating efficiencies, noting that the combined company would own roughly 1,350 properties with an aggregate enterprise value of $9.5B, making it one of the five largest net lease REITs behind Realty Income ( O ), W.P. Carey ( WPC ), National Retail ( NNN ), and Agree Realty ( ADC ). RTL surged more than 30% on the week while GNL dipped 8%. The deal comes amid a heated proxy battle led by activist firm Blackwells Capital, who announced their opposition to the merger and called the plan "another deceptive effort to skirt the ongoing proxy fight." Proxy advisory firms ISS and Glass Lewis each recommended last month that shareholders withhold support for several of AR Global's directors. As part of the proposed merger - which the firms expect to close in Q3 - GNL would reduce its quarterly dividend by 12% to $0.354 per share.

{kind=link}

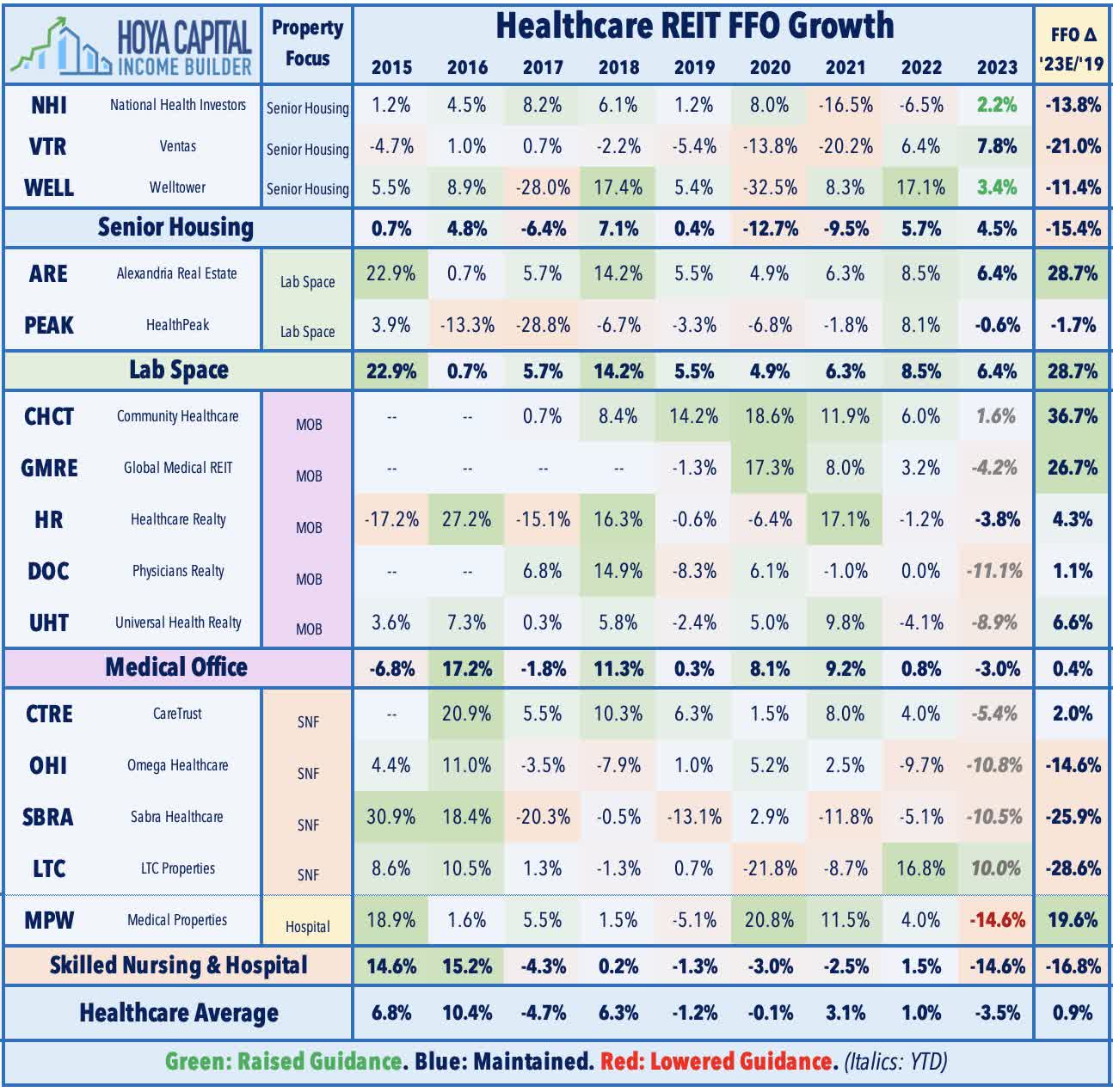

Healthcare : The aforementioned merger is not to be confused with the merger of another pair of externally managed REITs - Diversified Healthcare ( DHC ) and Office Properties Income ( OPI ) - one that is quite a bit more controversial with less clear strategic benefits for shareholders of either company. The drama intensified this week after a major shareholder of DHC said in a letter to DHC's board that it intends to vote against the company's proposed merger with OPI - a deal between two REITs that are externally managed by RMR Group which has sent shares of both firms sharply lower. Investor Flat Footed, which has a 7.4% stake in DHC, wrote that the deal "dramatically undervalues DHC" and argued that the firm should instead pursue strategic alternatives. The four REITs that are externally managed by RMR - which includes DHC and OPI along with hotel REIT Service Properties ( SVC ) and Industrial Logistics ( ILPT ) - have been among the worst performers over the past year due, in part, to their high debt loads.

{kind=link}

Healthcare : Embattled hospital owner Medical Properties Trust ( MPW ) - which has been in the cross-hairs of short sellers over the past year - was also the best-performers this week with gains of over 3% after it announced that its second-largest tenant - Prospect Medical - completed $375M in new financings from third-party lenders. MPW remains lower by over 30% this year, however, after reporting in February that Prospect had stopped paying rent - translating into an expected FFO decline of roughly 15% this year - but noted in its earnings report last month that it expects rent payments to resume in September. The announcement this week noted that after the refinancing, Prospect is substantially free of material debt or lease obligations outside of those to MPW and the new third-party financing. MPW also announced that it closed on its previously-announced sale of seven Australian hospitals for AUD$730M and expects close the remaining AUD$470 million in property sales and debt repayment during the current quarter at a 5.7% implied cap rate.

{kind=link}

Office : Empire State Realty ( ESRT ) gained more than 3% this week after it announced that Flagstar Bank will assume the entire 313k square foot lease at 1400 Broadway, which was formerly leased to Signature Bank before its closure by federal regulators in March. Flagstar Bank will pay $3/SF less compared to the prior lease, equating to a relatively modest 1.5% rent reduction over the duration of the lease. Other major terms of the lease - which runs through 2039 - will remain the same. The news prompted an upgrade from Evercore ISI analyst Steve Sakwa, who raised his estimate for 2023 FFO per share by six cents to $0.82. Last Friday, we published Office REITs: Just How Bad Is It? We discussed how the surge in interest rates has turned a weak-but-manageable situation into a bleak one, but there is more nuance to the prevailing narrative would suggest. Debt service expenses have been the primary culprit behind the wave of recent loan defaults from private equity firms Brookfield, Blackstone, and Pimco. Despite operating with generally more conservative debt levels, however, office REITs have experienced all the pain of private markets and then some.

{kind=link}

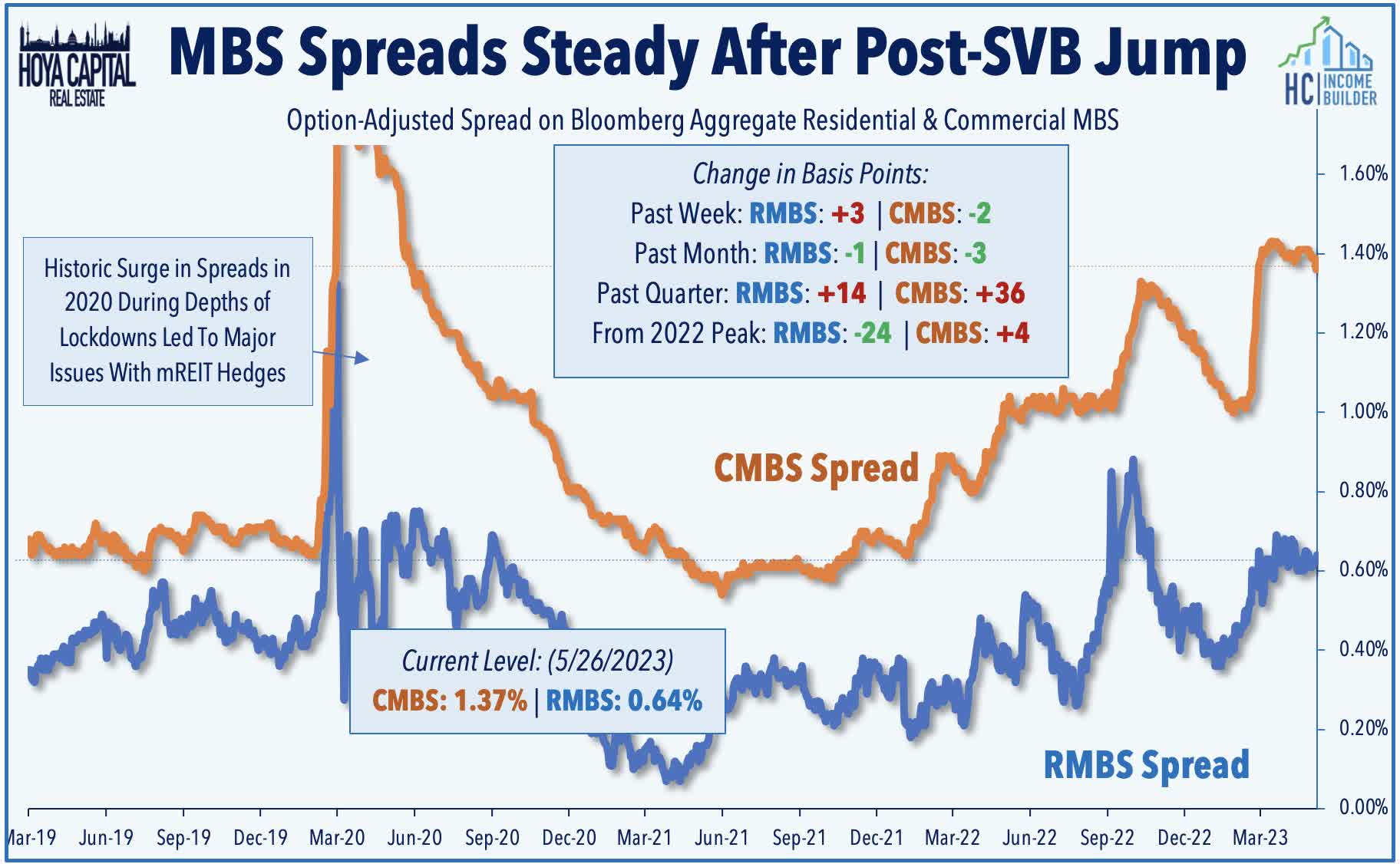

Sticking in the office sector, regional lender PacWest ( PACW ) - which has plunged 70% this year on concerns over the stability of its deposit base - rebounded nearly 25% this week after it disclosed a deal to sell a $2.7 billion portfolio of 74 real estate construction loans to Kennedy-Wilson Holdings ( KW ), a loan portfolio that consists primarily of office and multifamily-backed development properties. PacWest - which focused its real estate lending properties in California - held $4.6 billion in construction loans at the end of the first quarter, along with approximately $15B in other real estate-backed loans. Kennedy Wilson - also based in California - is a publicly-traded real estate asset manager with $23 billion in assets under management. PacWest also announced that it is selling its construction loan-focused real estate lending arm - Civic Financial Services - to Roc360. Commercial and residential mortgage-backed bond spreads have tightened a bit in recent weeks after a jump in the wake of the Silicon Valley Bank collapse in early March. Earlier this month, Fitch reported that CMBS delinquency rate decreased six bps to 1.70% in April from 1.76% in March as higher resolution volume outpaced a lower volume of new delinquencies.

{kind=link}

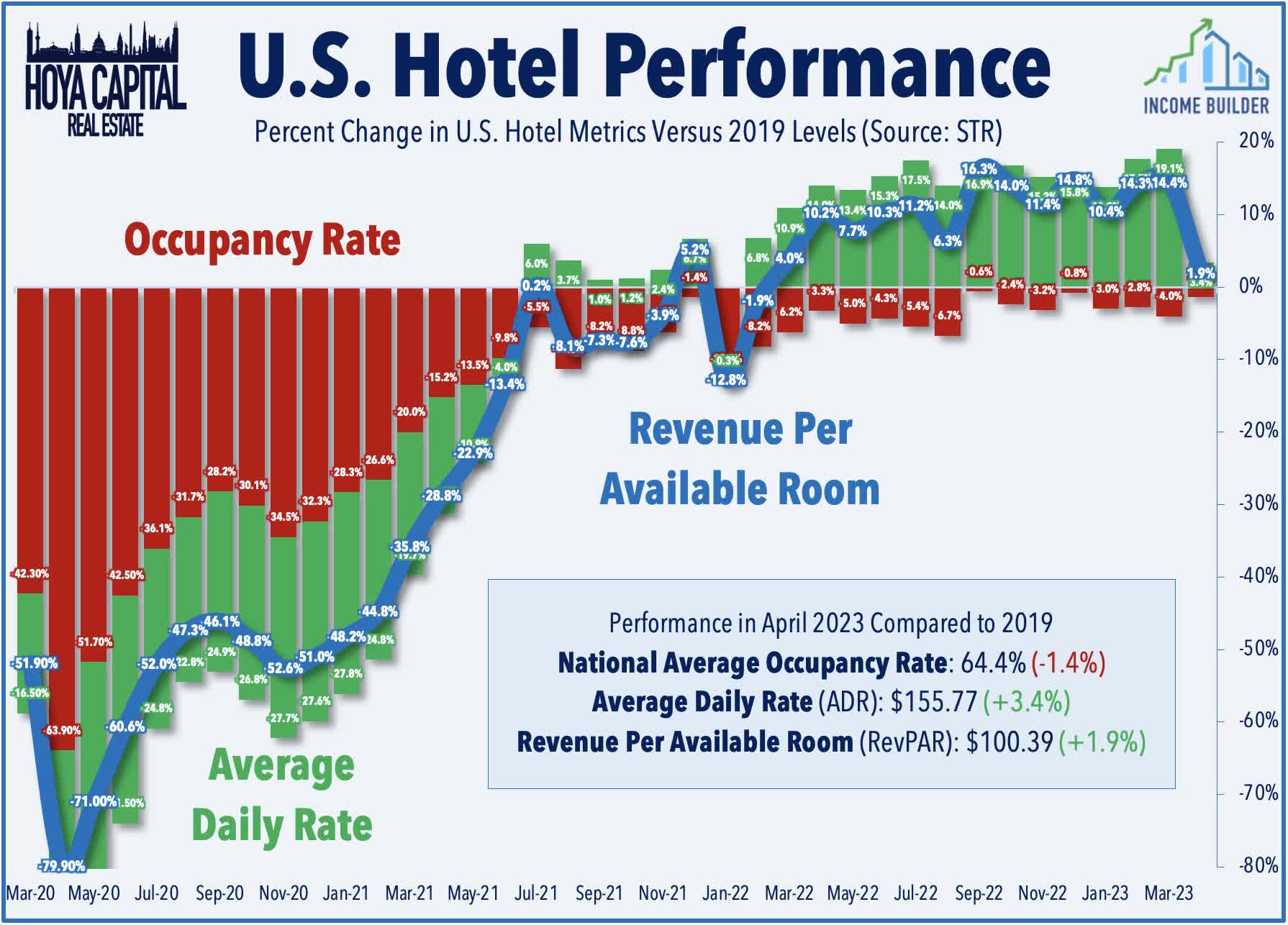

Hotels : Pebblebrook Hotel ( PEB ) declined about 3% on the week after providing an update on operating trends, commenting that Q2 results have so far been "in line with expectations" as "business and group demand trends remain positive, while leisure demand continues to be healthy but with less exuberance than last year." Consistent with the trends we discussed in Hotel REITs: The Pandemic Is Over, Now What published this week, PEB reported that it's seeing normalization in Average Daily Rates ("ADR") following last year's nearly 20% surge, with ADR actually turning negative in April on a year-over-year basis, down sharply from the 18.1% increase reported in the first quarter. The latest data from STR showed that the national average occupancy rate improved to 64.4% in April - just 1% below 2019 levels - but ADR and RevPAR growth slowed rather considerably. ADR rose by just 3.4% in April - down from the 19.1% growth in March. RevPAR increased 1.9% from last year, down from the 14.4% growth in March. With more onus on occupancy growth to drive performance this year, the lifting of the final pandemic-era travel restrictions earlier this month came at an opportune time as international travel demand is expected to provide a healthy occupancy tailwind over the coming quarters, especially for REITs focused in lagging coastal markets.

{kind=link}

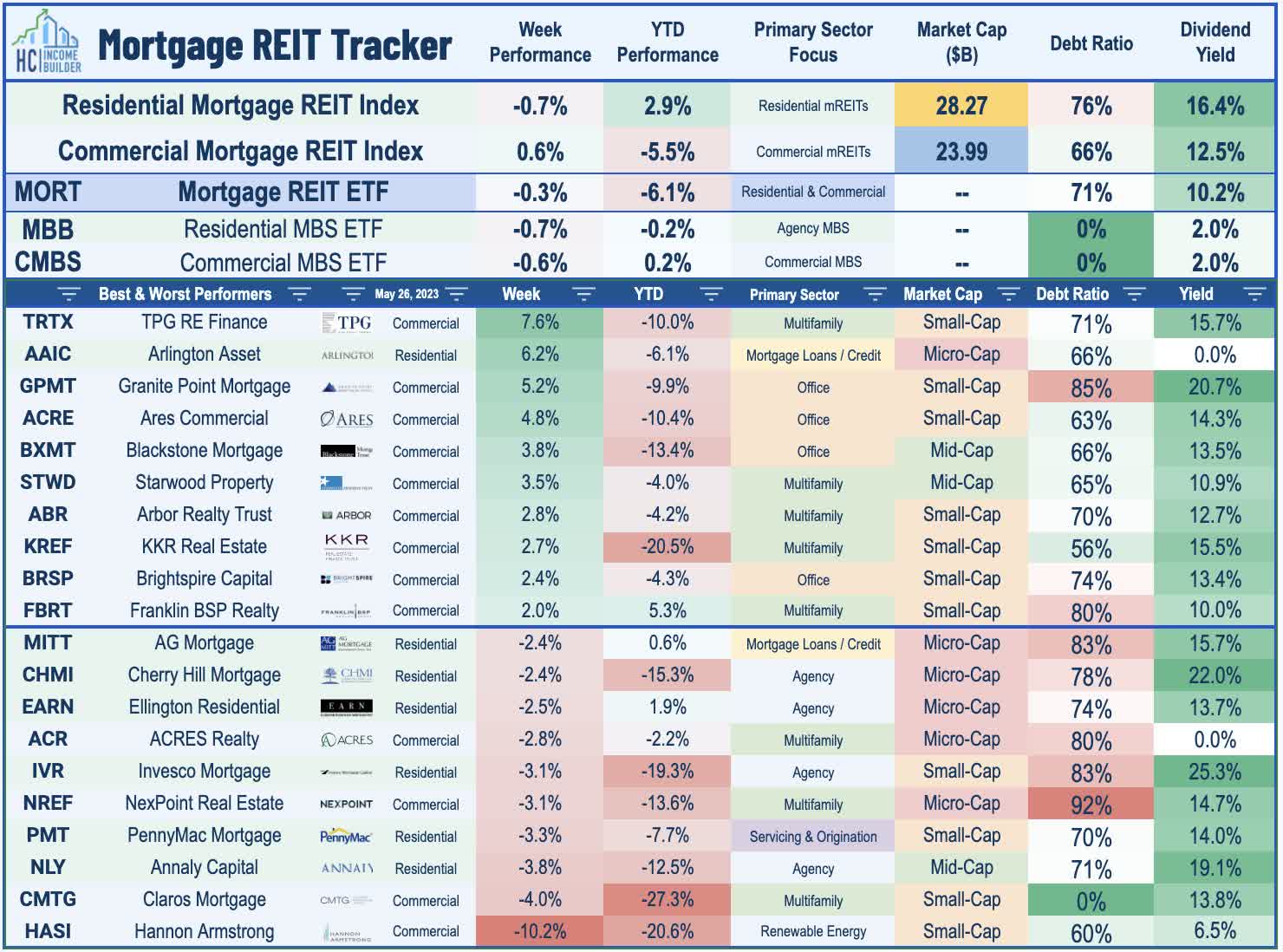

Mortgage REIT Week In Review

Mortgage REITs were mixed on the week as a rebound from office-focused commercial mREITs was offset by pressure on agency-focused residential mREITs. On a relatively slow week of newsflow in the mREIT space, Hannon Armstrong ( HASI ) dipped more than 10% after launching a $300M secondary common stock offering - one of the few secondary stock offerings this year in the REIT space. On the upside this week, Ellington Financial ( EFC ) advanced by about 2% after announcing that its estimated book value per share was $14.89 as of April 30, down about 1% from the $15.10/share at the end of Q1. EFC also maintained its quarterly dividend at $0.15/share, representing a dividend yield of 14.2%. Ready Capital ( RC ) also held its dividends steady at $0.40/share, representing a dividend yield of 15.3%.

{kind=link}

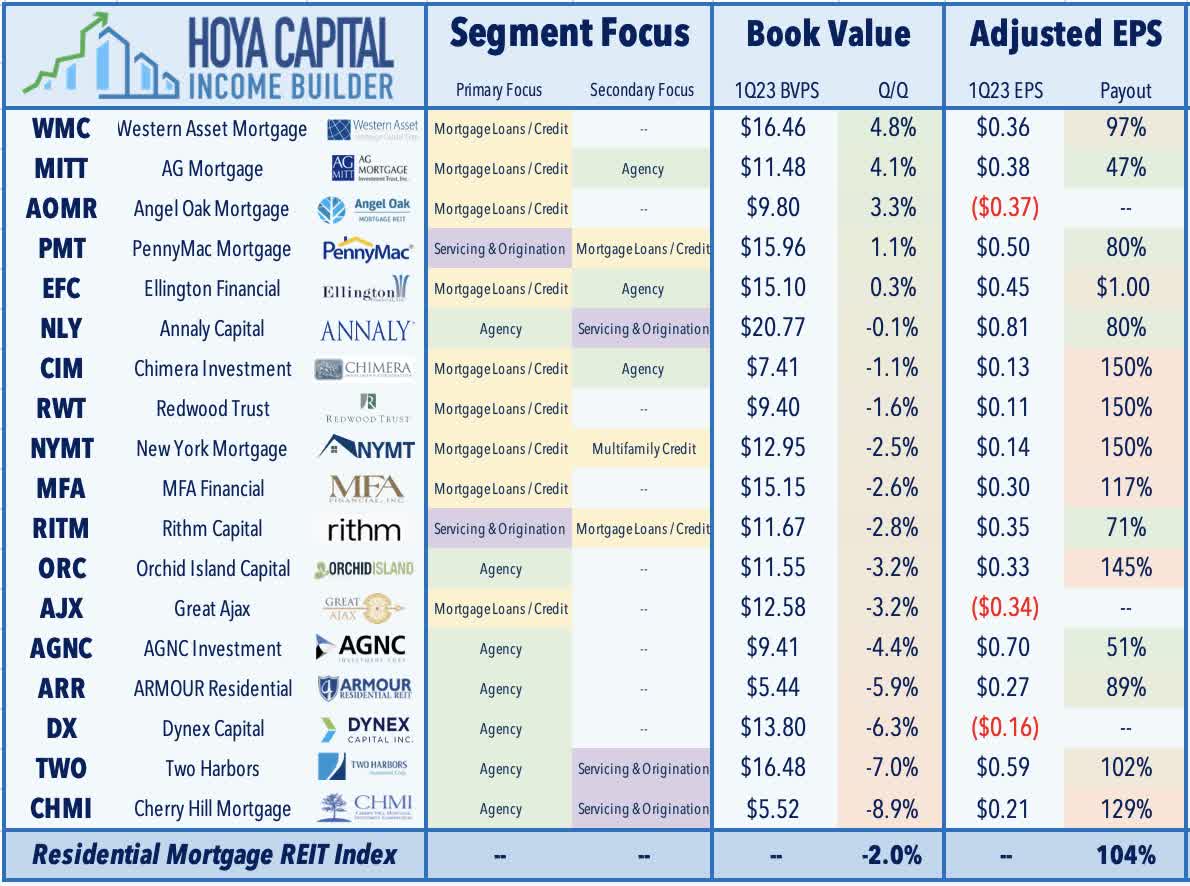

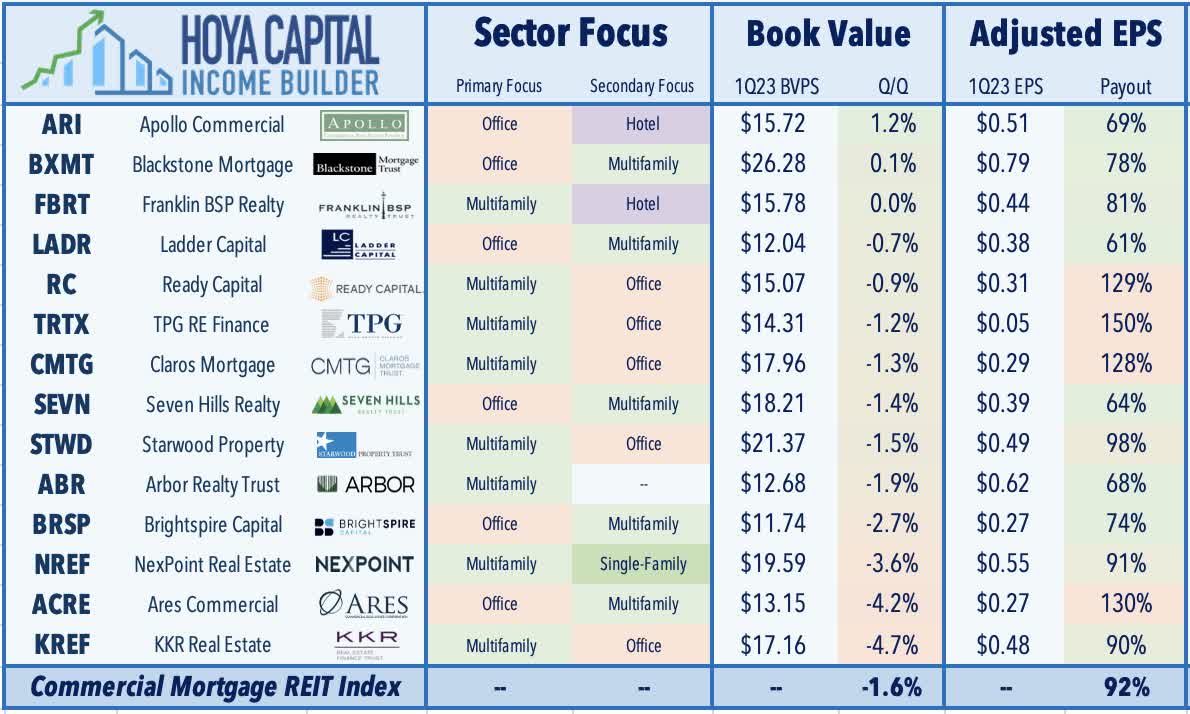

As noted in our Earnings Recap , residential mREITs reported an average decline in BVPS of 1.9% in Q1, while commercial mREITs reported a 1.8% average decline. Within the residential mREIT sector, credit-focused mREITs fared better in Q1 - reporting a slight increase in their Book Value Per Share ("BVPS") while agency-focused REITs reported an average decline in their BVPS of about 5% in Q1. Dividend coverage was stronger for commercial mREITs with about 75% of commercial mREITs covering their dividend with Q1 adjusted EPS while just 50% of residential mREITs covered their dividend.

{kind=link}

{kind=link}

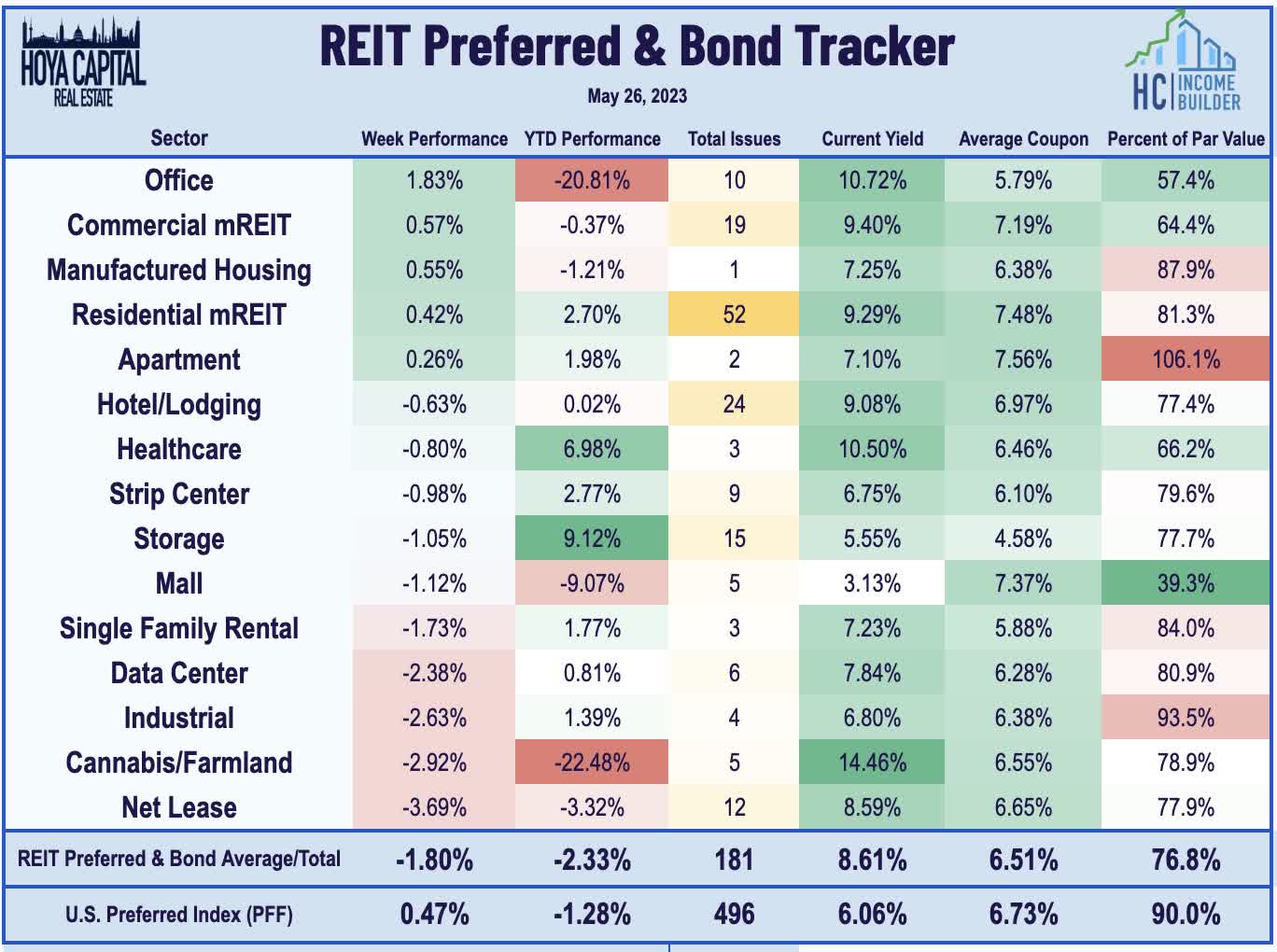

REIT Capital Raising & REIT Preferreds

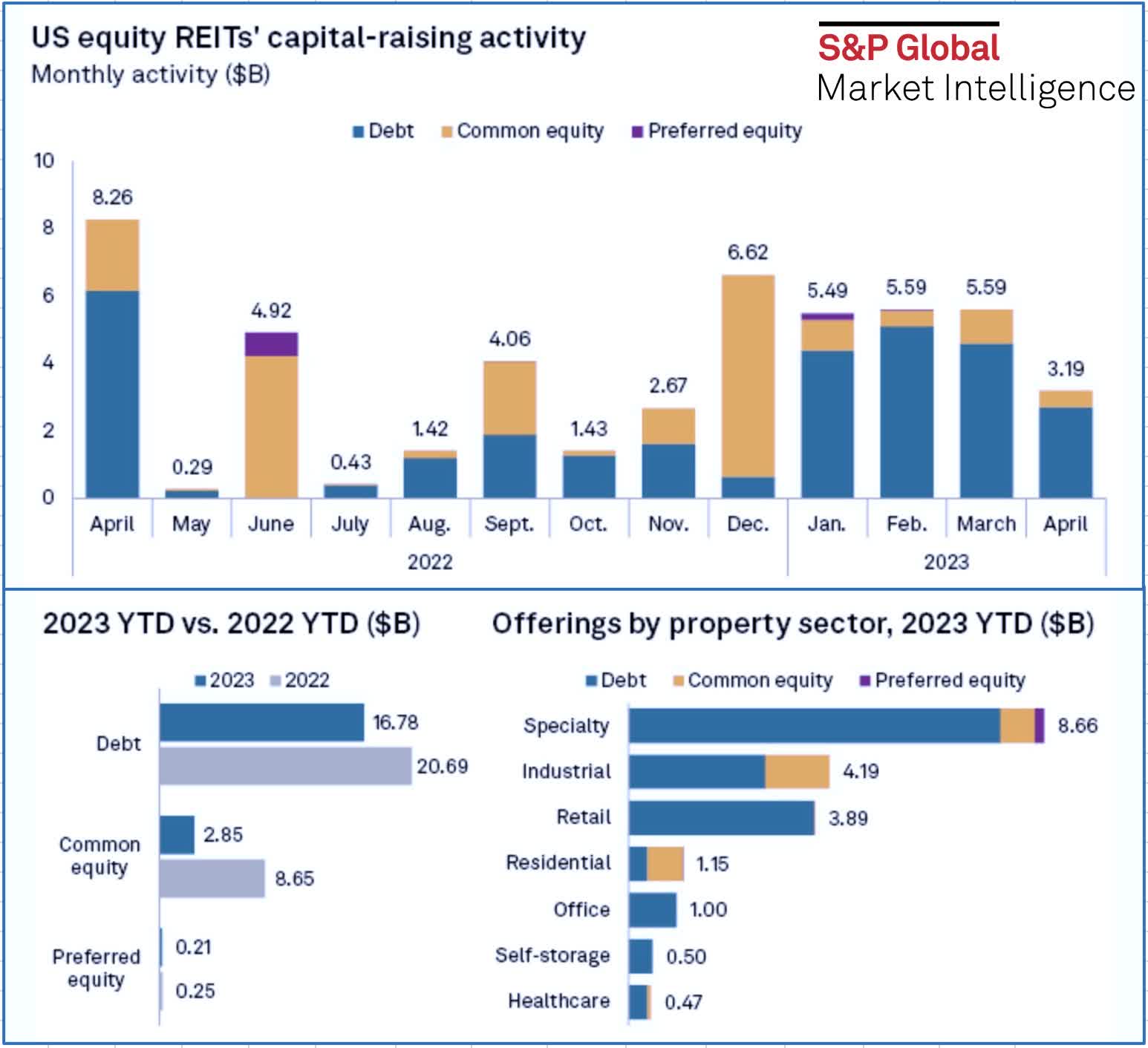

Several REITs were active on the capital-raising front this week. Cell tower REIT American Tower ((AMT)) priced $1.5B in new debt, split into two tranches: $650M of 5.250% notes due 2028 and $850M of 5.550% notes due 2033. Medical office building REIT Physicians Realty ( DOC ) closed on a $400 Million Term Loan maturing May 2028 along with a swap agreement to fix the variable component of the Term Loan at 3.59% for the duration of the borrowing period. Office Properties Income ((OPI)) announced that it has commenced the implementation of its financing strategy for its merger with Diversified Healthcare Trust ( DHC ) with the closing of a $30.7 million CMBS loan secured by an office building in Maryland at an all-in fixed interest rate of 7.21%. S&P Global Market Intelligence reported this week that U.S. equity REITs raised a total of $3.2 billion in April - below the $5.6 billion raised in March - and well below the $8.3 billion raised in April 2022. The offerings in April brought the year-to-date total to $19.85 billion, about 32.9% lower than the capital raised during the same period last year as REITs have significantly curtailed external growth activity since mid-2022.

{kind=link}

Back on the secondary markets, the REIT Preferred & Bond Index declined 1.8% on the week, lagging the 0.5% advance for the iShares Preferred ETF ( PFF ). Of note, Global Net Lease ((GNL)) announced that as part of its proposed merger agreement with Necessity Retail ((RTL)), both of RTL's preferred issues ( RTLPO ) and ( RTLPP ) will be automatically converted into newly-created preferred shares of GNL with substantially identical powers, preferences, privileges, and rights. Notable standouts on the upside this week included the suite of four preferreds of office REIT Vornado Realty ( VNO ), which posted gains of up to 4% while the preferred of Hudson Pacific ( HPP ) advanced nearly 8%. Retail and net lease REIT preferreds were under pressure, with weekly declines of over 3% from the preferreds of Spirit Realty ( SRC ), EPR Properties ( EPR ), and SITE Centers ( SITC ).

{kind=link}

2023 Performance Recap & 2022 Review

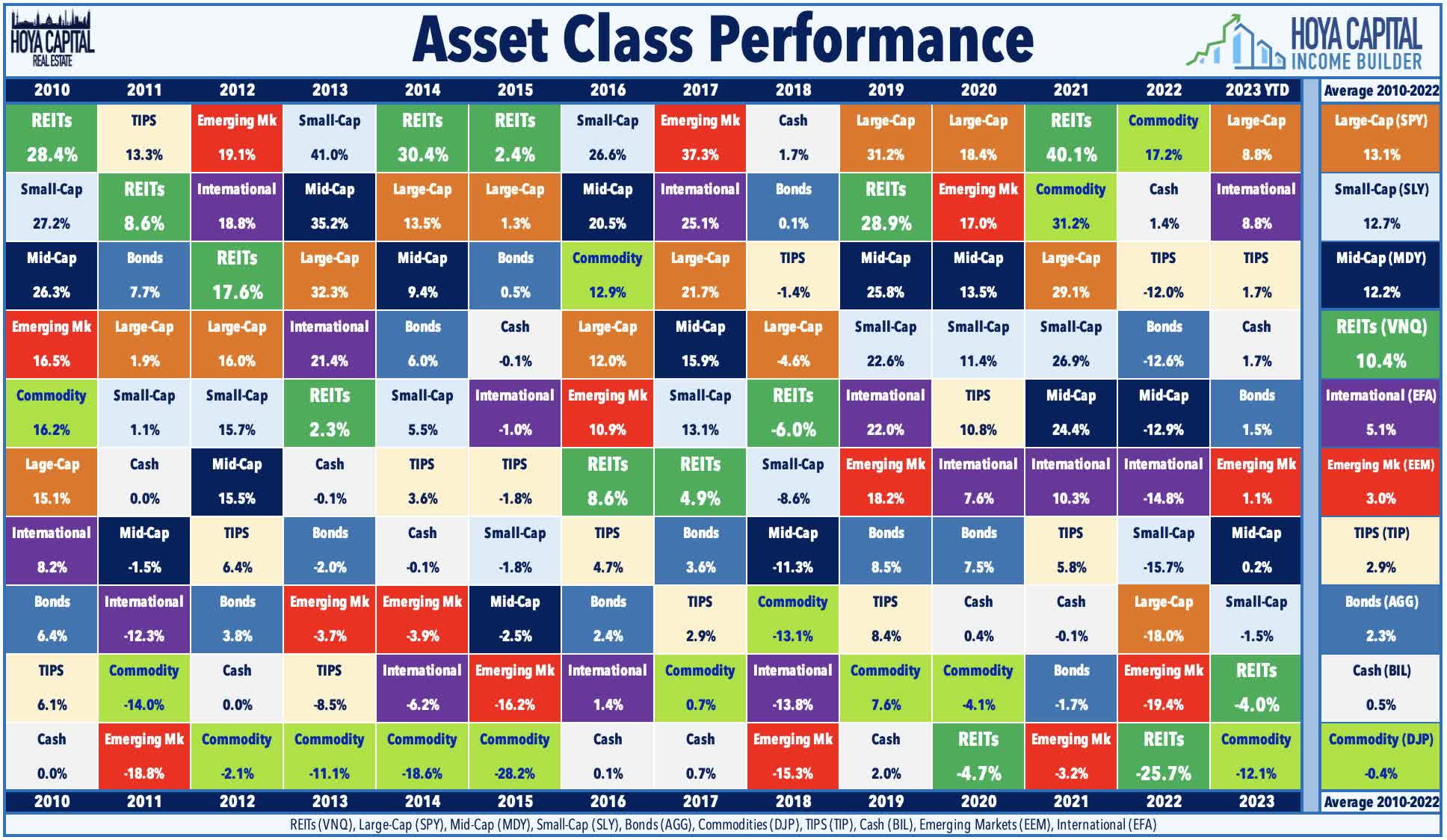

Through nearly five months of 2023, the Equity REIT Index is now lower by 3.9% on a price return basis for the year (-2.1% on a total return basis) while the Mortgage REIT Index is lower by 9.1% (-4.0% on a total return basis). This compares with the 9.8% gain on the S&P 500 and the 0.9% advance for the S&P Mid-Cap 400 . Within the real estate sector, 5-of-18 property sectors are in positive territory on the year, led by Single-Family Rental, Industrial, and Data Center REITs, while Office REITs have lagged on the downside. At 3.81%, the 10-Year Treasury Yield has declined by 7 basis points since the start of the year - up from its 2023 intra-day lows of 3.26%, but still below its late-2022 closing highs of 4.30%. The US bond market has stabilized following its worst year in history as the Bloomberg US Aggregate Bond Index has gained 1.2% this year. Crude Oil - perhaps the most important inflation input - is lower by 8% on the year and roughly 40% below its 2022 peak.

{kind=link}

There were few places to hide across financial markets in a historically brutal year for investors in 2022 that wiped out nearly a fifth of global financial wealth. The typically-steady US bond market delivered its worst year in history in 2022 with a loss of 13.01% on the Bloomberg US Aggregate Bond Index , which is over 4x larger than the previous worst year back in 1994 (-2.9%). Closing at 3.88%, the 10-Year Treasury Yield surged 237 basis points from the start of the year. Among the ten major asset classes, Commodities ( DJP ) was the only segment to see positive inflation-adjusted returns for the year. After leading the charge in the prior year, REITs finished in the basement of the performance tables among the ten major asset classes on a total return basis with declines of roughly 25%. Performance trends have largely reversed this year, with Commodities now in the basement in 2023.

{kind=link}

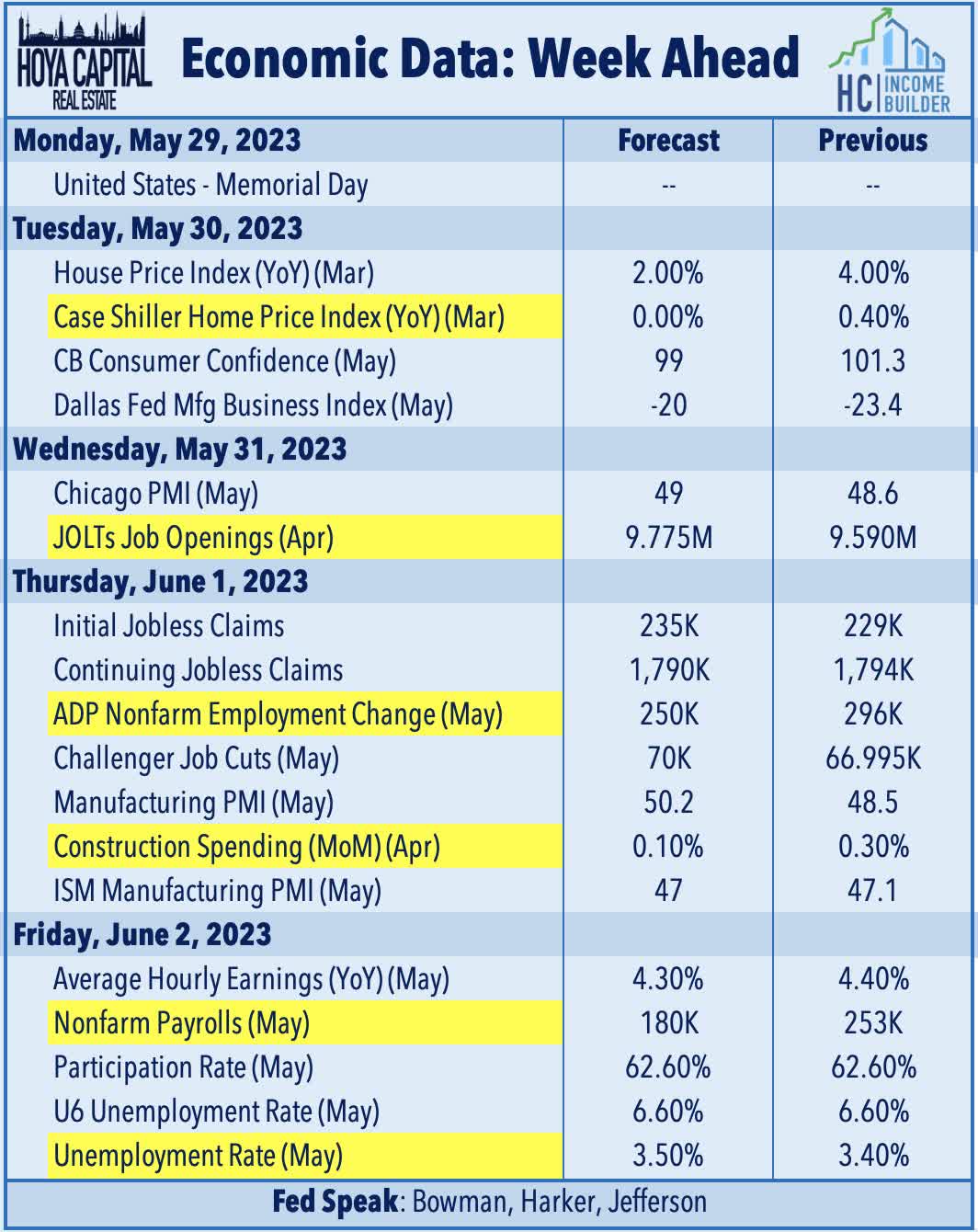

Economic Calendar In The Week Ahead

Employment data highlights a critical week of economic data in the week ahead, headlined by JOLTS report on Wednesday, ADP Payrolls data and Jobless Claims data on Thursday, and the BLS Nonfarm Payrolls report on Friday. Economists are looking for job growth of roughly 180k in May, which follows a solid month of April in which the economy added 253k jobs. The closely-watched Average Hourly Earnings series within the payrolls report - which is the first major inflation print for April - is expected to show a cooldown in wage growth in April to 4.3%. 'Good news is bad news' will likely be the theme of these reports as several Fed officials have pinned their decisions to pivot away from aggressive monetary tightening on a long-awaited cooldown in labor markets. As noted above, swaps markets imply a 65% probability that the Fed will hike rates by 25 basis points in their mid-June meeting to a 5.50% upper bound, continuing the swiftest rate hike cycle since the early 1980s. We'll also see housing data on Tuesday via the Case Shiller Home Price Index and Construction Spending data on Thursday and we'll see another busy slate of PMI data throughout the week. U.S. equity and bond markets will be closed on Monday in observance of Memorial Day.

{kind=link}

For an in-depth analysis of all real estate sectors, check out all of our quarterly reports: Apartments , Homebuilders , Manufactured Housing , Student Housing , Single-Family Rentals , Cell Towers , Casinos , Industrial , Data Center , Malls, Healthcare , Net Lease , Shopping Centers , Hotels , Billboards , Office , Farmland , Storage , Timber , Mortgage , and Cannabis.

Disclosure : Hoya Capital Real Estate advises two Exchange-Traded Funds listed on the NYSE. In addition to any long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index and in the Hoya Capital High Dividend Yield Index . Index definitions and a complete list of holdings are available on our website.

{kind=link}

For further details see:

Fed Not Done, But Should Be